![General Liability Insurance For Contractors [Ultimate Guide]](https://brooksinstx.com/wp-content/uploads/tosten/General-Liability-Insurance-For-Contractors-_Ultimate-Guide__1764025857-1080x675.jpeg)

Contractors face significant financial risks every day on job sites. One lawsuit or accident can destroy years of hard work and savings.

General liability insurance for contractors provides essential protection against third-party claims, property damage, and bodily injury lawsuits. We at Brooks Insurance help Texas contractors secure the right coverage to protect their businesses and maintain their professional reputation.

What Does General Liability Insurance Cover for Contractors

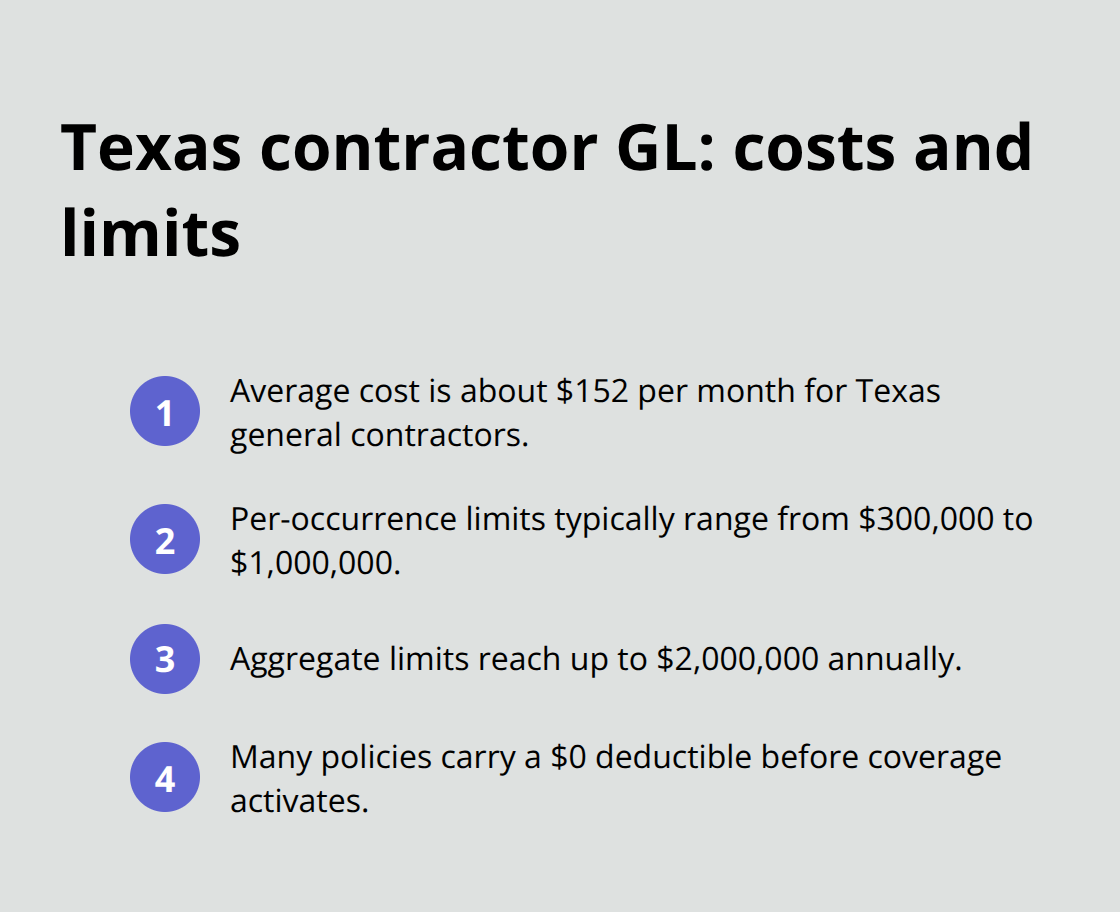

General liability insurance for contractors protects your business against third-party claims that involve bodily injury, property damage, and personal injury lawsuits. This coverage includes medical expenses when a client suffers harm on your job site, repairs for damaged customer property, and legal defense costs for claims related to your business operations. The average monthly cost for Texas general contractors runs approximately $152, which makes this protection an affordable safeguard against potentially devastating financial losses. Standard policies typically offer coverage limits that range from $300,000 to $1 million per occurrence, with aggregate limits that reach up to $2 million annually.

Core Coverage Components That Protect Your Business

The three main coverage areas include bodily injury protection when someone suffers harm due to your work activities, property damage coverage for client belongings you accidentally damage, and personal injury protection against claims like copyright infringement or defamation. Most policies carry a $0 deductible, which means you pay nothing out-of-pocket before coverage activates. However, general liability insurance excludes your own work product, workers’ compensation claims, and pollution incidents (these require separate specialized policies).

How General Liability Differs from Other Business Insurance

Workers’ compensation insurance covers your employees and averages $306 monthly for Texas contractors, while commercial auto insurance protects company vehicles with minimum liability limits of $30,000 per person. Tools and equipment insurance averages $34 monthly and protects your gear regardless of location with typical coverage limits between $3,000 to $5,000. Professional liability insurance covers errors and omissions in your work, while builder’s risk insurance protects structures during construction phases.

Texas Legal Requirements and Practical Necessities

Texas law requires workers’ compensation for businesses with employees, but general liability insurance remains voluntary yet practically essential for contractors who want to secure clients and protect their business assets. Commercial General Liability insurance protects business owners against claims of liability for bodily injury, property damage, and personal injury. Most clients now require proof of insurance before they award contracts, which makes this coverage a business necessity rather than just financial protection. The next consideration involves determining exactly how much coverage your specific contracting business needs to stay properly protected.

Why General Liability Insurance Is Non-Negotiable for Contractors

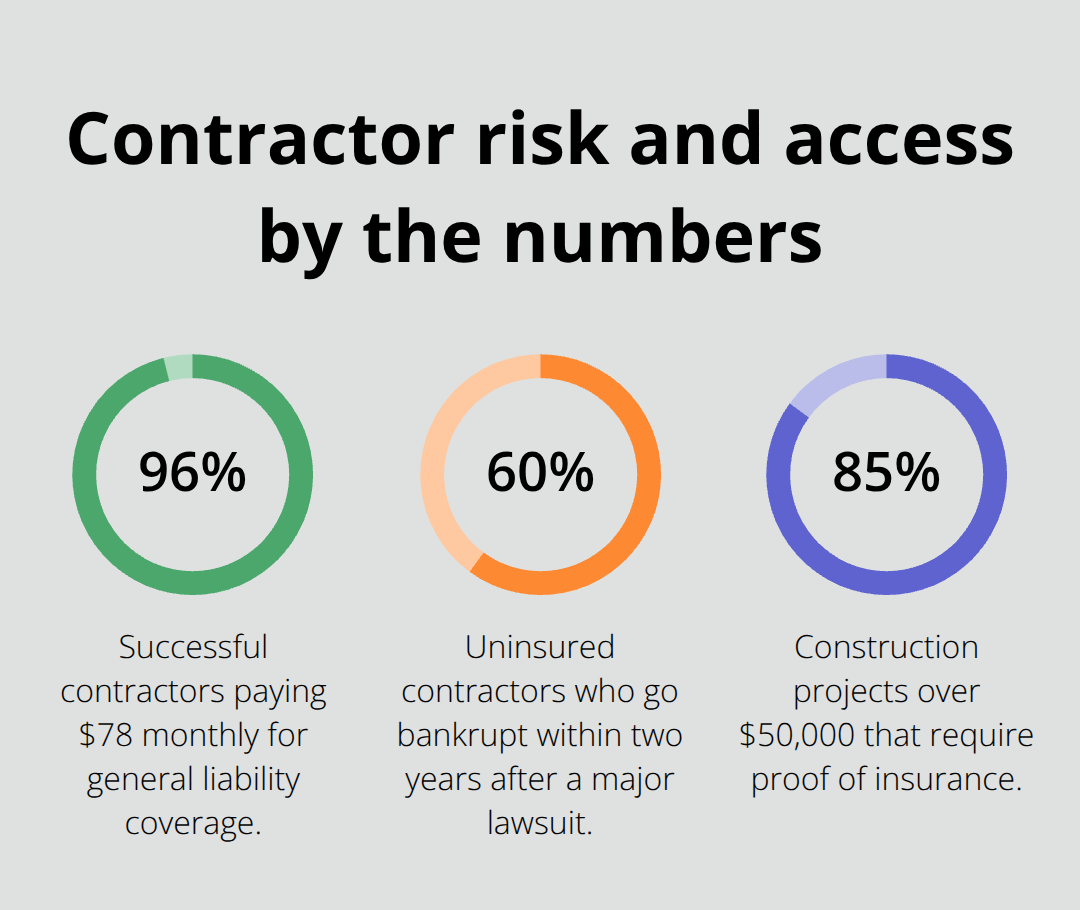

Construction lawsuits cost Texas contractors an average of $75,000 per claim according to industry data, and 96% of successful contractors pay just $78 monthly for general liability protection that prevents these devastating losses. When a client slips on wet concrete at your job site or your equipment damages expensive landscaping, general liability insurance covers medical bills, property repairs, and legal defense costs that would otherwise bankrupt your business. Texas contractors face particular risks from unpredictable weather conditions and strict building regulations that increase accident probability.

Financial Protection That Prevents Business Destruction

General liability claims against contractors average between $25,000 and $150,000, but policies provide coverage limits up to $2 million annually for serious incidents. Without insurance, contractors must pay these costs from personal assets and business savings, which forces 60% of uninsured contractors into bankruptcy within two years of a major lawsuit. Professional liability claims for project mistakes add another layer of financial risk, with average settlements that reach $45,000 for design errors or construction defects (particularly common in complex commercial projects).

Client Requirements Drive Business Opportunities

Municipal contracts and commercial clients now require proof of insurance before they award 85% of construction projects worth over $50,000. Contractors without general liability coverage lose access to these profitable opportunities and limit themselves to smaller residential jobs with higher competition. Insurance certificates demonstrate financial responsibility and professional credibility that separates established contractors from unlicensed competitors who cannot secure major projects.

Legal Defense Costs Exceed Settlement Amounts

Attorney fees for defending construction lawsuits can be substantial, and frivolous claims still require expensive legal representation. General liability policies cover these defense costs automatically, while uninsured contractors face immediate out-of-pocket expenses that drain cash flow during lengthy court proceedings (which can last 18-24 months for complex cases). These legal costs accumulate quickly and often exceed the actual settlement amounts, which makes insurance protection financially smart even for contractors who believe they follow perfect safety protocols.

The selection of appropriate coverage limits requires careful analysis of your specific business risks and project values to match protection with actual exposure levels.

How Much Coverage Do You Actually Need

Texas contractors must match coverage limits to their actual project values and risk exposure rather than accept minimum policy amounts that leave gaps in protection. A contractor who handles $500,000 residential projects needs different coverage than one who manages $2 million commercial builds, yet many contractors purchase identical $1 million policies without analysis of their specific exposure. The standard approach involves calculation of your largest single project value, then secures coverage limits that exceed this amount by at least 50% to account for legal fees and additional damages.

Calculate Coverage Based on Project Values

Contractors who work on projects worth $300,000 should carry minimum coverage of $500,000 per occurrence, while those who handle million-dollar commercial work require $2 million limits to avoid personal asset exposure. Commercial property damage claims vary significantly based on project type and scope, but luxury home projects can generate claims that exceed $400,000 when expensive finishes suffer damage. Professional liability coverage becomes essential for contractors who perform design work or manage subcontractors, with claims that can reach substantial amounts for project delays or specification errors.

Industry-Specific Risk Factors Affect Premiums

Roofing contractors face higher premiums because their work generates more claims than general construction, while electrical contractors pay premium increases due to fire risks. Professional services pay around $675-780 per year, while construction companies face costs of $2,400 or more depending on business size and revenue. Workers compensation remains mandatory for Texas contractors with employees, but sole proprietors should consider voluntary coverage to protect against job-related injuries.

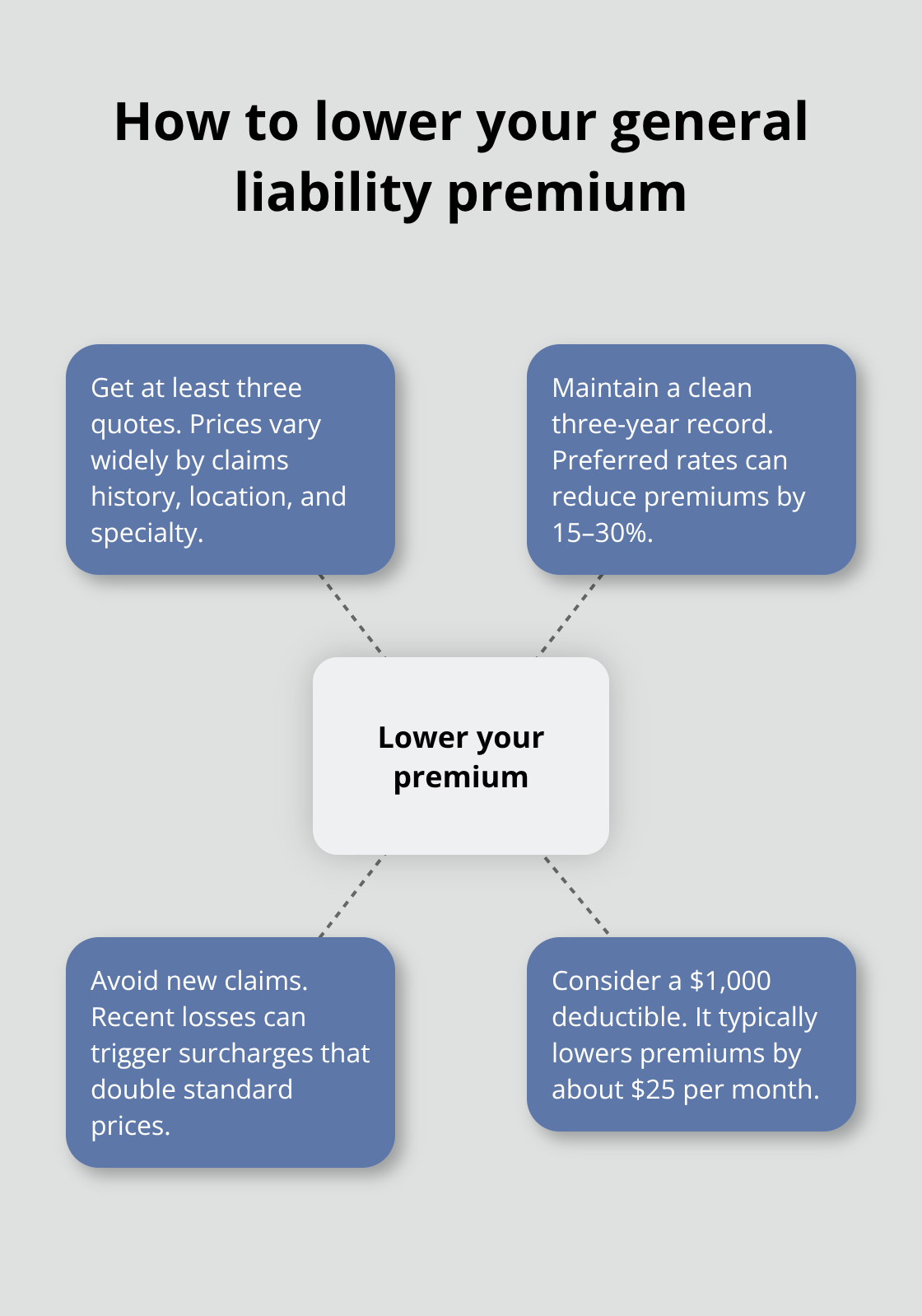

Quote Comparison Strategy That Saves Money

Request quotes from at least three carriers because prices vary dramatically based on your claims history, location, and work specialty. Contractors with clean records over three years qualify for preferred rates that reduce premiums by 15-30%, while those with recent claims face surcharges that double standard prices. Deductibles impact monthly costs significantly, with $1,000 deductibles that reduce premiums by approximately $25 monthly compared to zero-deductible policies.

Policy Type Selection Affects Long-Term Protection

Most successful contractors choose occurrence-based policies over claims-made coverage because occurrence policies protect against future claims related to current work, even after policy cancellation. The application process requires accurate revenue projections, employee counts, and detailed work descriptions because misrepresentation voids coverage when claims arise.

Final Thoughts

General liability insurance for contractors prevents lawsuits from destroying your business, with Texas contractors who pay just $152 monthly on average for coverage that handles claims averaging $75,000. This protection covers third-party injuries, property damage, and legal defense costs while it builds client trust through proof of financial responsibility. Without coverage, contractors face personal bankruptcy risk and lose access to 85% of profitable commercial projects that require insurance certificates.

You need accurate assessment of your project values and risk exposure to determine appropriate coverage limits. Contact multiple carriers for quotes because prices vary significantly based on your work specialty, claims history, and location (occurrence-based policies provide better long-term protection than claims-made coverage). Choose policies that protect against future claims related to current work even after policy cancellation.

We at Brooks Insurance represent multiple top-rated carriers and help contractors secure proper protection while they maintain affordable premiums through careful policy selection. Our licensed agents understand Texas contractor needs and provide access to competitive rates with comprehensive coverage options. Contact us today to protect your contracting business with the right general liability insurance for contractors.