Flood insurance costs have shifted significantly in 2025, with new pricing models affecting property owners nationwide. Many homeowners ask “how much is flood insurance” as premiums vary widely based on location and risk factors.

We at Brooks Insurance see Texas property owners facing unique challenges with updated flood zone maps and changing coverage options. Understanding current rates helps you make informed decisions about protecting your property.

What Does Flood Insurance Actually Cost in 2025

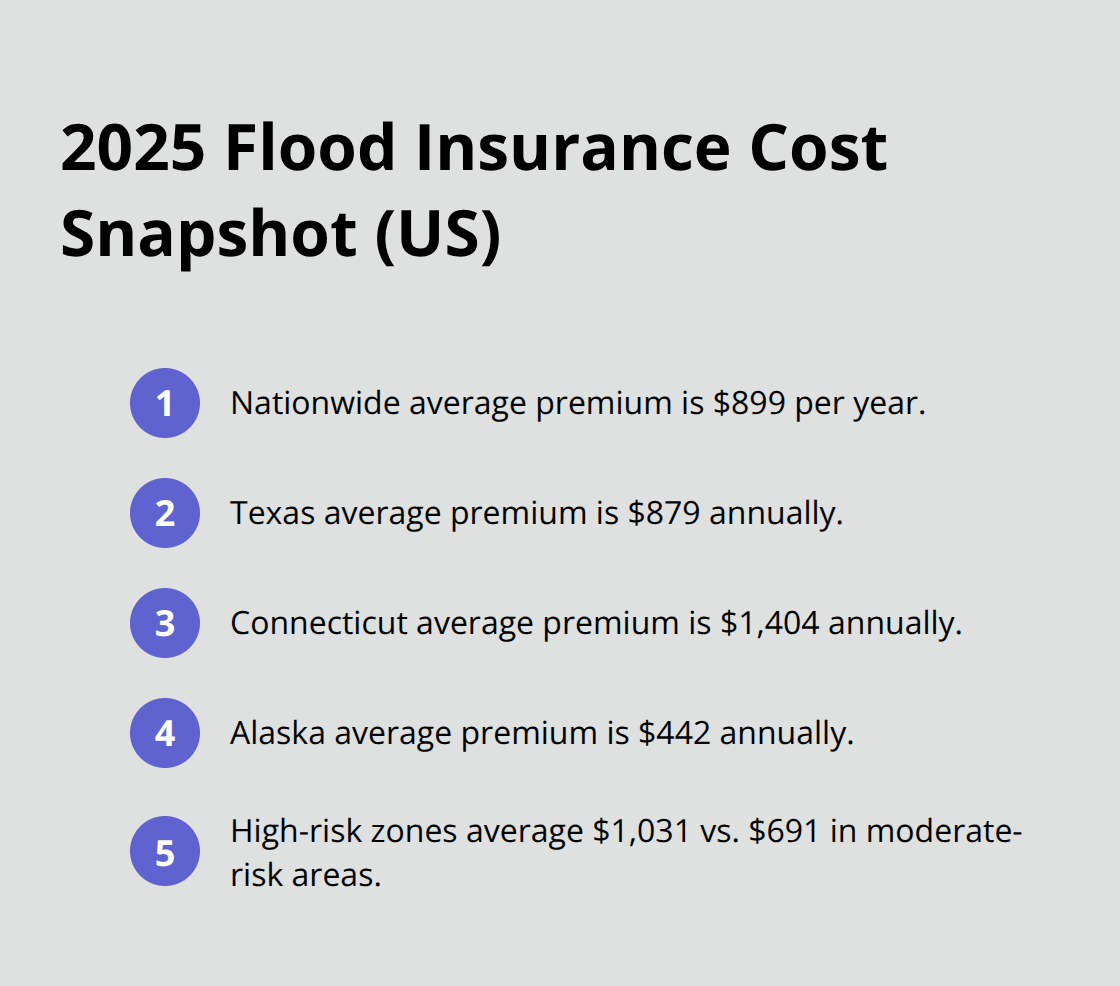

The National Flood Insurance Program sets the baseline with an average annual premium of $899 nationwide, according to NerdWallet’s analysis of NFIP rates. Texas property owners pay slightly less at $879 per year, but this varies dramatically by location. Connecticut homeowners face the steepest costs at $1,404 annually, while Alaska residents pay just $442. High-risk flood zones carry premiums that average $1,031 per year, compared to $691 for properties in moderate-risk areas.

Private Market Competition Changes the Game

Private insurers now offer competitive alternatives to NFIP policies, often with better coverage limits and replacement cost benefits. While NFIP caps dwelling coverage at $250,000 and personal property at $100,000, private carriers frequently provide higher limits. The catch lies in eligibility requirements and geographic availability, particularly in hurricane-prone coastal areas where private insurers may restrict new policies.

Risk Rating 2.0 Creates Winners and Losers

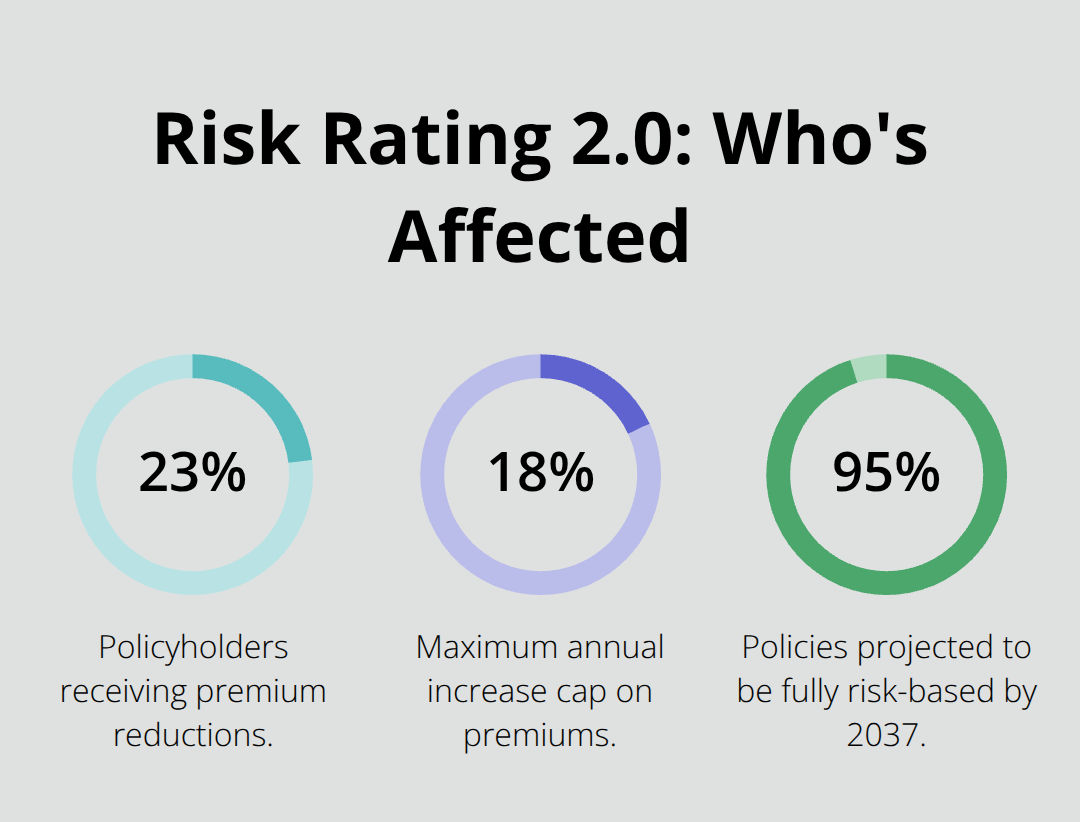

FEMA’s new pricing model affects 23% of policyholders with premium reductions, while others face annual increases (capped at 18% per year). The Government Accountability Office projects that 95% of policies will reflect full risk-based pricing by 2037. Properties with basements in high-risk zones see premiums jump 15% to 20% higher than similar homes without basements.

Risk Rating 2.0 was fully implemented as of April 1, 2023.

Elevation Certificates Unlock Significant Savings

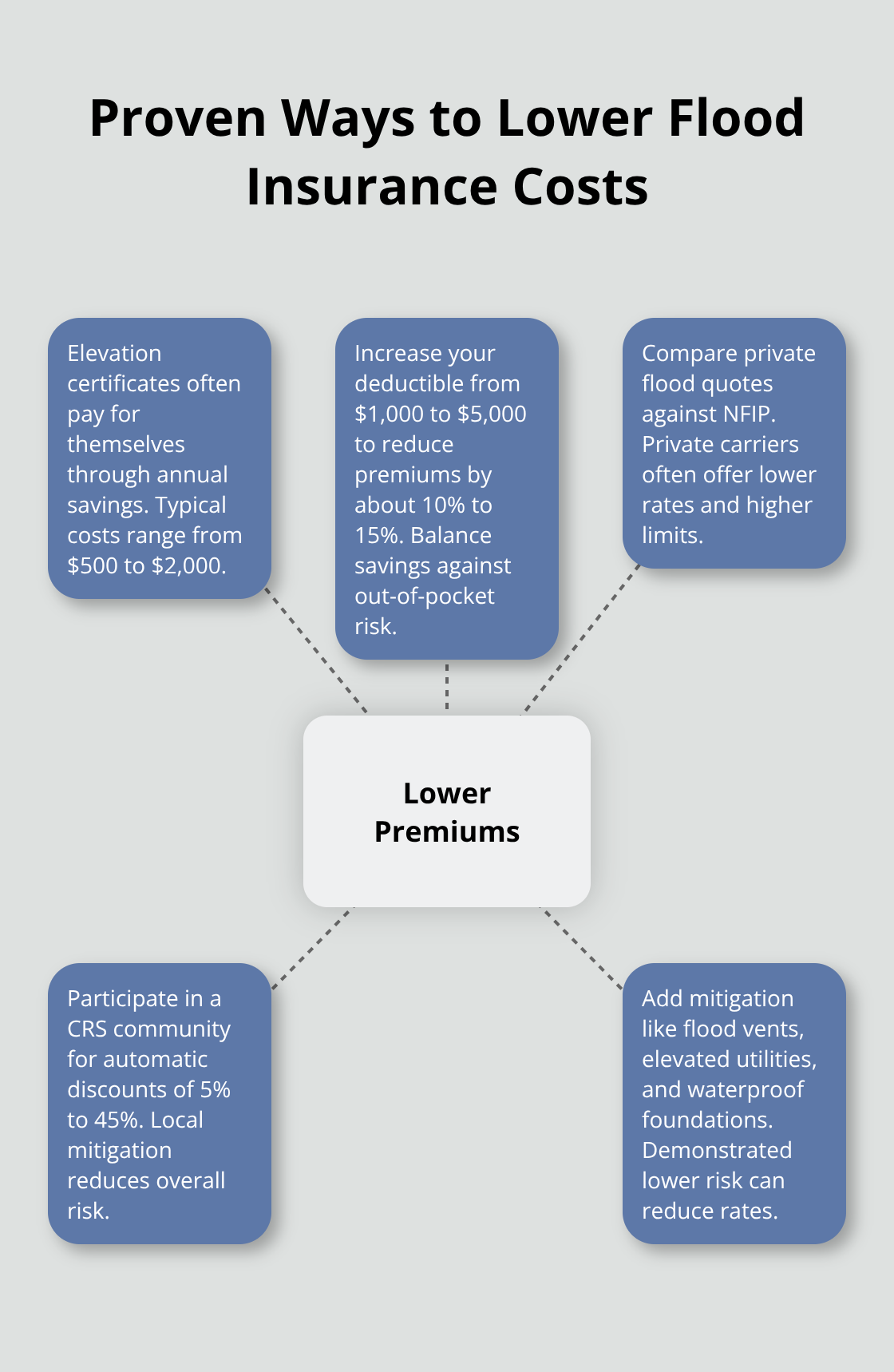

Property owners can reduce rates significantly with elevation certificates, which cost between $500 to $2,000 but often pay for themselves through lower premiums. These certificates document your home’s elevation relative to the base flood elevation in your area. The documentation helps insurers calculate more accurate risk assessments (and often lower rates) for properties that sit above expected flood levels.

Understanding these cost factors helps you evaluate which coverage options work best for your specific property and budget situation.

What Determines Your Flood Insurance Rate

Your flood zone designation drives premium calculations more than any other factor. Properties in high-risk zones labeled A or V face annual premiums that average $1,031, while moderate-risk areas average $691 according to NFIP data. FEMA’s flood maps identify areas with a 1% annual flood chance, which means homeowners in these zones have a 25% probability of flood damage during a typical 30-year mortgage period.

The elevation of your home relative to the base flood elevation matters significantly. Homes built above this level qualify for substantial discounts, while those below face premium penalties that can add hundreds of dollars to annual costs.

Construction Details That Impact Your Rate

Your home’s foundation type, age, and construction materials directly affect premium calculations under Risk Rating 2.0. Homes with basements in flood-prone areas pay 15% to 20% higher premiums because basements increase damage potential and claims costs. Mobile homes and manufactured housing typically carry higher premiums due to their vulnerability to flood damage.

Elevated utilities, flood vents, and waterproof foundations can reduce rates when they demonstrate lower risk to insurers. The replacement cost of your home also factors into calculations (higher-value properties pay proportionally more for coverage).

Coverage Choices Control Your Annual Cost

NFIP policies max out at $250,000 for structure coverage and $100,000 for personal property, but you can purchase less coverage to reduce premiums. A $5,000 deductible instead of $1,000 can cut your annual premium by 10% to 15%, though you’ll pay more out-of-pocket during claims.

Private insurers often offer higher coverage limits and replacement cost coverage instead of actual cash value, which affects rates significantly. Evaluate your true replacement costs before you select coverage limits (underinsurance creates financial gaps that standard homeowners policies won’t fill).

These rate factors work together to create your final premium, but smart property owners can take specific steps to reduce their annual costs through strategic improvements and policy choices.

How Can You Cut Your Flood Insurance Costs

Property owners can reduce annual premiums through strategic improvements and smart policy choices. Elevation certificates represent the single most effective cost-reduction tool, typically costing $500 to $2,000 but delivering annual savings that often exceed the initial investment.

These certificates document your home’s elevation above base flood levels. Homes that sit two feet above base flood elevation may qualify for rate reductions based on FEMA data. Property owners who install flood vents, elevate utilities above potential flood levels, and waterproof foundations can further reduce rates when they demonstrate lower risk to insurers.

Private Insurance Often Beats NFIP Rates

Private flood insurers frequently offer lower premiums than NFIP policies, particularly for properties outside high-risk zones. Private carriers provide replacement cost coverage instead of actual cash value, higher coverage limits beyond NFIP caps, and faster claims processing.

Texas property owners should compare at least three private quotes against NFIP rates before they purchase coverage. Private insurers may restrict coverage in hurricane-prone coastal areas, but inland properties often qualify for significant savings.

Community Programs Deliver Additional Discounts

The Community Rating System offers premium discounts of 5% to 45% for properties in communities that implement flood risk reduction measures. These communities maintain levees and manage stormwater systems to reduce overall flood risk.

Property owners benefit when their local governments participate in these programs (the discounts apply automatically to eligible policies). Communities that take proactive flood management steps help all residents save money on their annual premiums.

Deductible Adjustments Lower Annual Costs

Property owners who increase their deductible from $1,000 to $5,000 typically reduce annual premiums by 10% to 15%. Higher deductibles mean you pay more during claims, but the annual savings can be substantial.

Evaluate total out-of-pocket costs against annual savings before you select higher deductibles. Flood damage claims can be substantial, so the deductible represents a relatively small portion of typical claim amounts.

Final Thoughts

Flood insurance costs in 2025 vary dramatically based on location and risk factors, with Texas property owners paying an average of $879 annually compared to the national average of $899. The answer to how much is flood insurance depends on your flood zone designation, property elevation, and coverage selections. High-risk zones command premiums of $1,031 per year while moderate-risk areas average $691 annually.

Private insurers often beat NFIP rates and provide superior coverage options including higher limits and replacement cost benefits. Property owners can reduce premiums through elevation certificates, strategic deductible choices, and flood mitigation improvements that demonstrate lower risk to insurers. Communities that participate in flood risk reduction programs offer automatic discounts that range from 5% to 45% on annual premiums.

Texas property owners should evaluate their flood risk through FEMA maps and obtain multiple quotes from both private carriers and NFIP before they purchase coverage. Property improvements and smart policy choices can deliver substantial annual savings (elevation certificates alone often pay for themselves through reduced premiums). We at Brooks Insurance help Texas residents compare flood insurance options and find coverage that fits their specific needs through our licensed agents.