Texas businesses face significant financial risks from lawsuits and accidents every day. General liability insurance Texas coverage protects companies from property damage claims, bodily injury lawsuits, and advertising disputes.

We at Brooks Insurance help Texas business owners navigate these complex coverage decisions. The right policy can mean the difference between surviving a lawsuit and closing your doors permanently.

What General Liability Insurance Covers in Texas

Property Damage Claims Hit Texas Businesses Hard

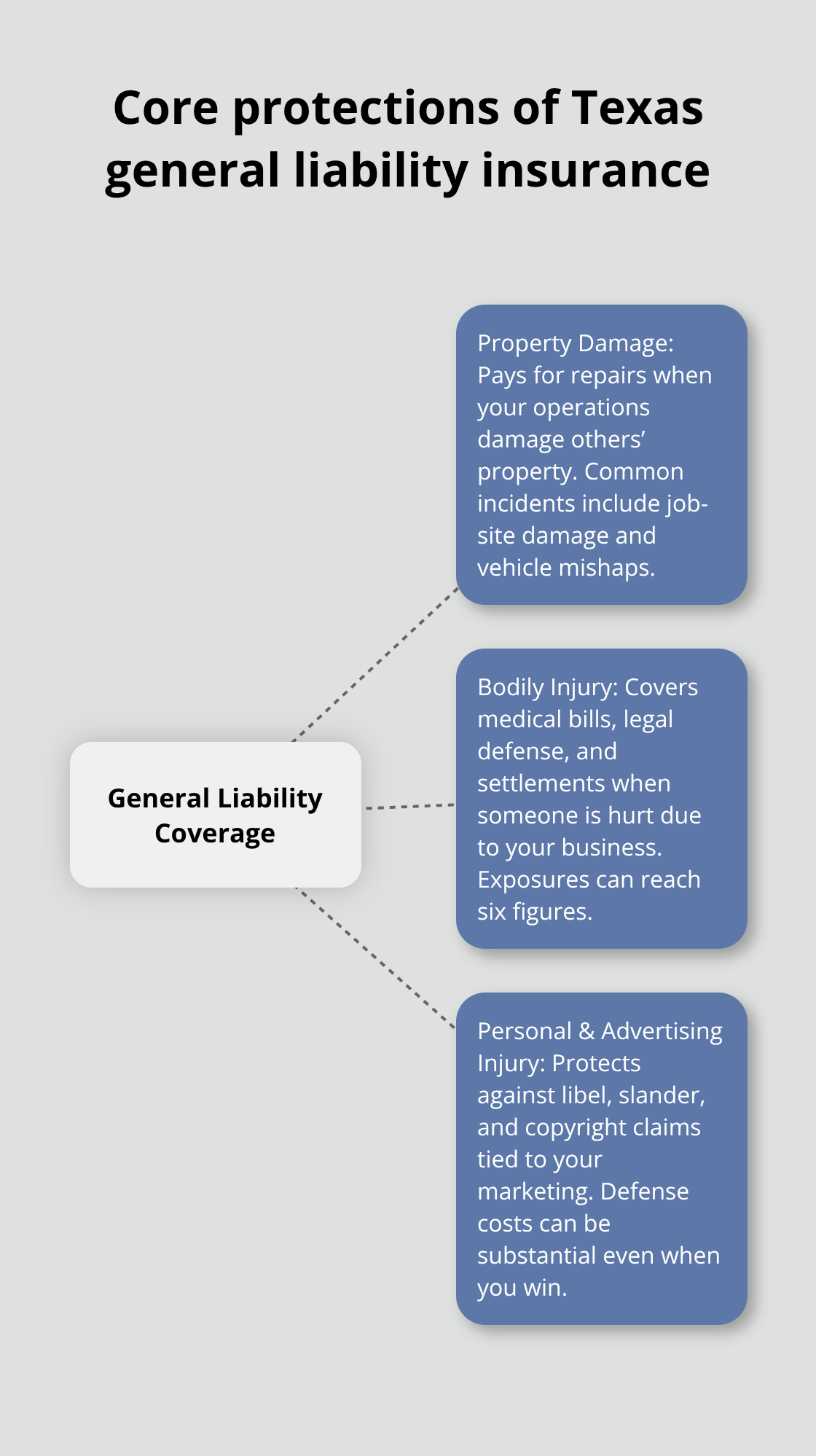

General liability insurance in Texas protects your business against three major categories of claims that can devastate your finances. Property damage coverage pays for repairs when your business operations cause harm to someone else’s property.

A contractor who accidentally damages a client’s flooring faces repair costs that often exceed $10,000. A delivery truck that backs into a customer’s fence creates immediate liability for replacement expenses.

The median monthly cost for this protection reaches $60 according to Progressive Insurance data from 2024. This affordable rate protects against expensive repair bills that frequently climb into thousands of dollars. Texas businesses in construction and delivery services face the highest exposure to property damage claims.

Bodily Injury Coverage Prevents Financial Ruin

Bodily injury coverage handles medical expenses and legal costs when someone gets hurt on your business premises or due to your operations. A customer who slips on a wet floor in your office creates hospital bills that exceed $50,000, plus potential lawsuit damages that can reach six figures. Texas businesses face higher premiums in densely populated areas (like Houston and Dallas) due to increased claims frequency.

The policy covers emergency room visits, surgery costs, rehabilitation expenses, and lost wages for injured parties. A single accident forces many businesses to liquidate assets when they lack proper coverage. Medical bills from serious injuries often start at $25,000 and escalate quickly with complications or extended treatment.

Personal and Advertising Injury Protection Covers Legal Battles

Personal and advertising injury protection covers claims related to libel, slander, copyright infringement, and false accusations. Competitors who claim your marketing materials copy their ideas file lawsuits that cost thousands in defense fees. Customers who allege your advertising contains false statements create legal exposure that many businesses underestimate.

Texas law requires clear disclosure of claims-made policy status in bold type on documentation. The average rate of $85 monthly for new customers provides protection against lawsuits that cost $25,000 to $100,000 in legal defense fees alone. Most businesses win these cases but still pay substantial legal costs throughout the process.

These three coverage areas work together to protect Texas businesses from the most common liability exposures, but state-specific requirements add another layer of complexity to your insurance decisions.

Texas-Specific Requirements and Regulations

Texas does not mandate general liability insurance for most businesses, which creates a dangerous misconception among business owners. While state law lacks universal requirements, specific industries face strict coverage mandates that carry severe penalties for non-compliance. Electricians must maintain liability coverage to operate legally, and businesses that contract with government entities face mandatory coverage requirements. Most commercial leases require general liability insurance, which makes coverage practically mandatory for retail stores, restaurants, and office-based businesses. Texas law requires that commercial general liability policy forms receive approval from the commissioner before issuance, which adds regulatory oversight to your coverage decisions.

Large Risk Exemptions Create Advantages

Texas defines large risks as policyholders with property values that exceed $5 million. These businesses receive exemption from prior approval requirements under Texas Insurance Code, which allows greater flexibility in coverage terms and conditions. Policy forms for large risks bypass standard approval processes, which enables customized coverage that smaller businesses cannot access. This exemption creates significant advantages for businesses that qualify but requires careful navigation of complex policy language. The Texas Department of Insurance oversees compliance with insurance regulations while it provides consumer protection resources for businesses of all sizes.

Claims Rules Protect Your Rights

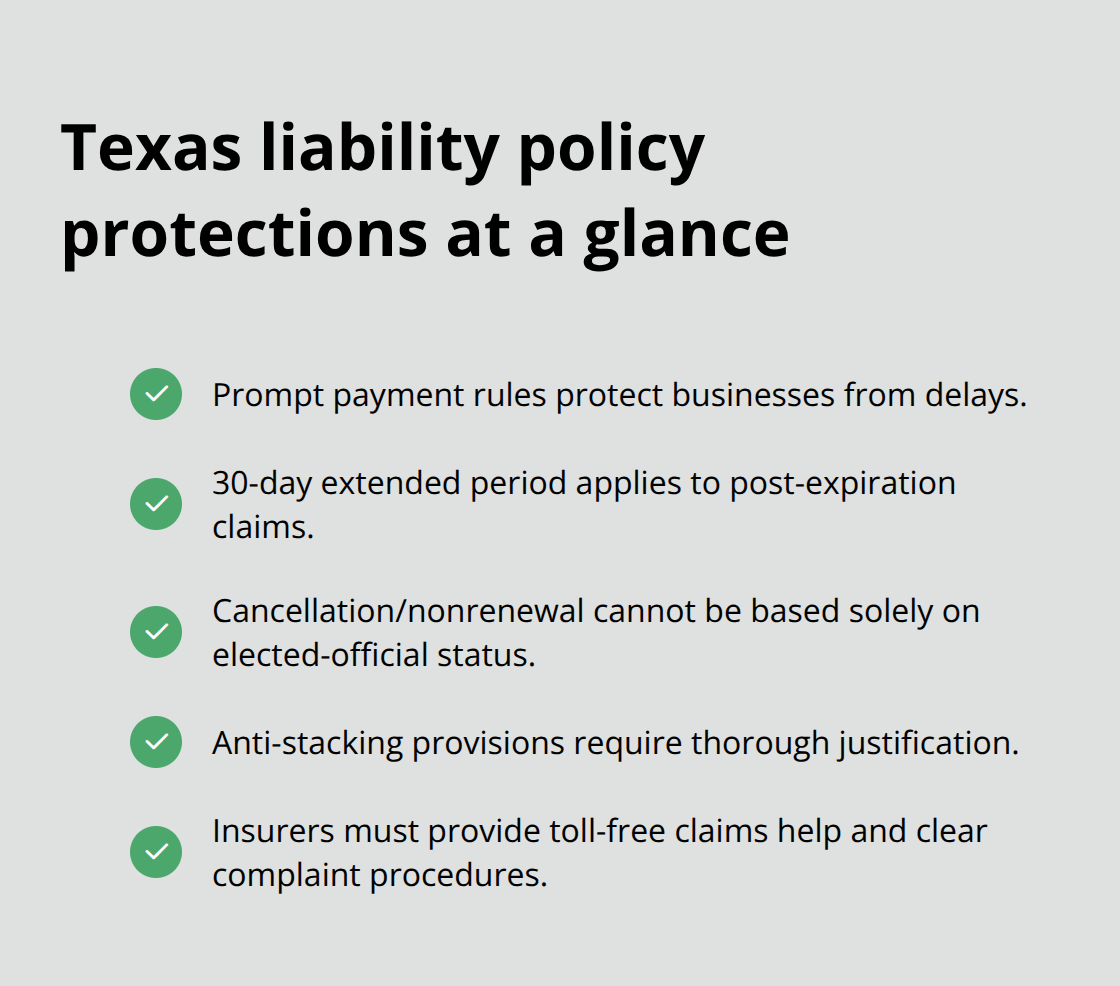

Texas law mandates prompt payment of claims under liability insurance policies, which protects businesses from delayed compensation during critical periods. Insured parties receive guaranteed 30-day extended periods for claims made after policy expiration (which enhances coverage effectiveness beyond the policy term). Cancellation or nonrenewal cannot occur solely based on status as an elected official, which prevents political discrimination in coverage decisions.

Anti-stacking provisions require thorough justification for approval, which protects businesses from unfair coverage limitations. Insurers must maintain toll-free numbers for claims assistance and provide clear complaint procedures in language that policyholders understand.

Policy Form Requirements Add Complexity

Texas requires that liability insurance exclusions clearly define terms, particularly in abuse-related exclusions where definitions must be precise. Claims-made policy status must appear prominently in bold type on policy documentation (per state disclosure requirements). A minimum two-year period applies to any contractual limitations on the time to bring suits related to insurance claims. Arbitration agreements in Texas insurance policies must adhere to policy language and cannot be unjust or misleading to policyholders. These requirements protect consumers but add layers of complexity that businesses must navigate when they select appropriate coverage limits and policy structures.

How Do You Select the Right General Liability Coverage

Risk Assessment Determines Your Premium Costs

Your business risk exposure depends on industry classification and physical operations. Texas construction businesses face average premiums around $928 monthly due to high accident rates, while dentists pay approximately $22 monthly according to industry data. Employee count directly impacts rates because more workers increase accident potential.

Businesses with multiple services like manufacturing, delivery, and installation pay higher premiums than single-service operations due to expanded risk exposure. Geographic location matters significantly – densely populated areas like Houston and Dallas command higher rates due to increased claims frequency. New businesses pay premium surcharges because they lack established safety records, while companies with clean claims histories receive favorable rates from insurers.

Coverage Limits Determine Your Financial Protection

Texas businesses typically select coverage between $500,000 and $2 million per occurrence, with $1 million per claim and $2 million aggregate limits as standard recommendations. Higher coverage amounts increase premiums but provide better protection against catastrophic lawsuits that frequently exceed $100,000 in legal defense costs alone.

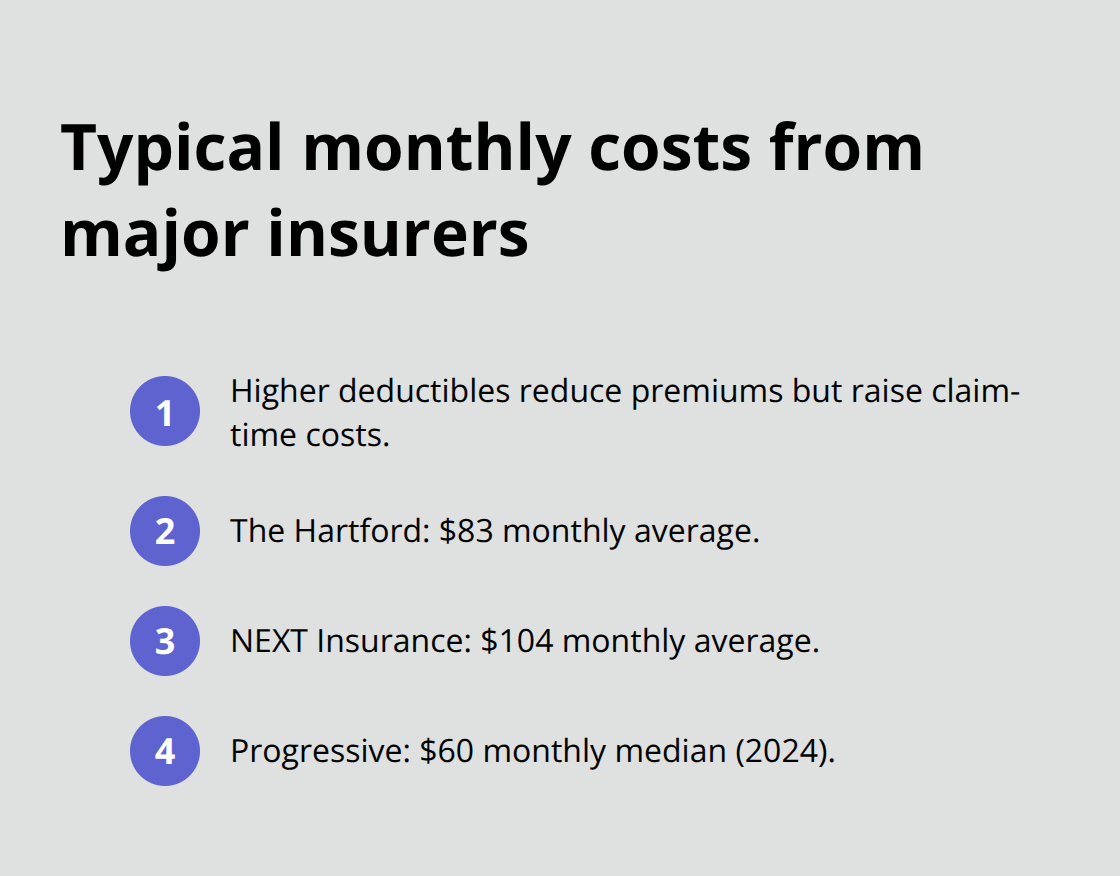

Higher deductibles reduce monthly premiums but increase out-of-pocket expenses during claims. The Hartford offers competitive rates at $83 monthly average, while NEXT Insurance averages $104 monthly but excels in customer service ratings. Progressive Insurance reports median costs of $60 monthly for general liability policies in 2024.

Umbrella policies provide additional coverage beyond standard limits for businesses that face elevated lawsuit risks.

Rate Comparison Requires Strategic Evaluation

Quote comparisons from at least three insurers provide the best rate analysis, but coverage levels must remain equivalent for accurate comparisons. Discounts frequently apply for safety programs, claims-free history, and bundled policy purchases with the same carrier (which can reduce overall costs significantly).

Risk purchasing groups offer lower costs through pooled buying power for similar businesses. The Texas Property and Casualty Insurance Guaranty Association is a nonprofit unincorporated legal entity composed of all member insurers, which makes licensed carriers safer choices than surplus lines options. Businesses should provide detailed claims history and risk management documentation to agents for accurate pricing. Monthly costs range from $17 to $928 depending on industry risk levels, business size, and coverage selections (with most small businesses paying between $60-$104 monthly).

Final Thoughts

General liability insurance Texas coverage protects your business from financial devastation caused by property damage claims, bodily injury lawsuits, and advertising disputes. The median monthly cost of $60 provides protection against legal defense fees that typically range from $25,000 to $100,000 per case. Texas businesses without coverage face bankruptcy when serious accidents occur, while insured companies continue operations during legal challenges.

Accurate risk assessment and quote comparisons from multiple carriers help you secure the right coverage. We at Brooks Insurance provide personalized service from licensed agents who understand Texas regulations and industry-specific requirements. Our comprehensive approach helps you select appropriate coverage limits while you avoid expensive gaps that leave your business vulnerable to lawsuits and claims.

The right general liability insurance Texas policy makes the difference between surviving a lawsuit and permanent business closure. Independent agencies represent multiple top-rated insurance companies, which gives you access to competitive rates and comprehensive coverage options. Brooks Insurance connects you with experienced local agents who help Texas businesses navigate complex insurance decisions with confidence.