![Commercial Auto Insurance in Texas [2025 Guide]](https://brooksinstx.com/wp-content/uploads/tosten/Commercial-Auto-Insurance-in-Texas-_2025-Guide__1766704172-1080x675.jpeg)

Running a business in Texas means your commercial vehicles need proper protection. Commercial auto insurance in Texas isn’t optional-it’s a legal requirement that shields your company from costly accidents and liability claims.

We at Brooks Insurance know that choosing the right coverage can feel overwhelming. This guide walks you through everything you need to know to protect your fleet.

What Businesses Actually Need Commercial Auto Insurance

Texas Law Demands It-And the Penalties Are Real

Commercial auto insurance in Texas isn’t optional. State law requires minimum liability coverage of $30,000 per person and $60,000 per accident in bodily injury liability, plus $25,000 for property damage. Any vehicle you operate primarily for business purposes-a delivery van, contractor truck, food truck, or service vehicle-must carry this coverage to stay legal. The penalties for operating without it hit hard: fines up to $350 for a first offense and up to $1,000 plus possible license suspension for repeat violations. This requirement exists because accidents happen, and when they do, someone needs to pay the medical bills, repair costs, and legal fees.

Your Personal Auto Policy Won’t Protect Your Business

This distinction catches many business owners off guard. Your personal auto insurance explicitly excludes business use, which means it will not cover work-related accidents. If an employee uses a personal vehicle for work tasks and causes an accident, your business faces substantial liability exposure. A single accident can cost tens of thousands in medical bills, vehicle damage, and legal fees-all of which fall on your company’s shoulders. The gap between personal and commercial coverage creates real financial risk that most business owners underestimate until a claim arrives.

Which Businesses Face the Highest Risk

Construction companies, delivery services, retailers with fleet vehicles, manufacturing facilities with service vehicles, and any operation involving contractor trucks or equipment transport all need commercial auto coverage. Each type of business carries different exposure levels. A contractor transporting expensive equipment faces different risk than a small consulting firm with a single company car. The average cost of commercial auto insurance in Texas runs about $218 per month, but this varies dramatically based on your fleet size, vehicle type, driver records, and coverage limits.

Matching Coverage to Your Actual Operations

Choosing adequate coverage means assessing your actual risk level rather than just meeting minimum legal requirements. A one-size-fits-all approach leaves gaps in protection or wastes money on unnecessary coverage. Your fleet size, the types of vehicles you operate, where you operate them, and your drivers’ records all influence what coverage you truly need. An independent agency like Brooks Insurance helps you match coverage to your specific business operations instead of forcing you into a standard policy that may not fit your situation.

The Real Cost of Underinsurance

Many business owners try to cut costs by reducing coverage limits or skipping optional protections. This strategy backfires when accidents happen. Minimum liability limits often prove insufficient to cover actual damages in serious accidents. Uninsured motorist coverage, collision protection, and comprehensive coverage address gaps that liability alone cannot fill. Your coverage decisions today determine whether your business survives a major accident or faces financial devastation.

Understanding your legal obligations and actual risk exposure sets the foundation for smart coverage decisions. The next step involves examining the specific types of coverage available and what each one actually protects.

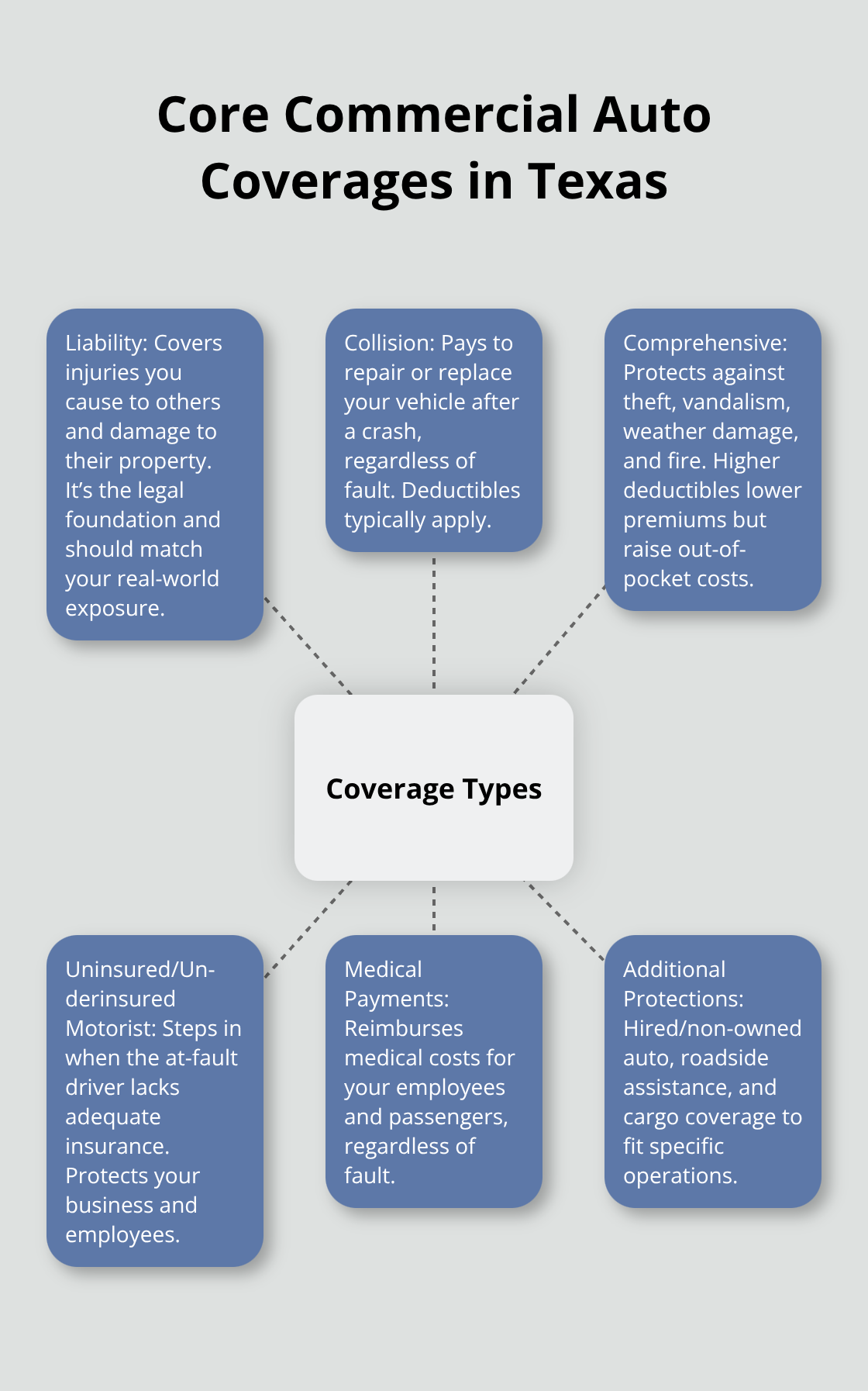

Coverage Types and What They Protect

Liability Coverage Forms Your Foundation

Liability coverage forms the foundation of commercial auto insurance in Texas, and it splits into two independent parts. Bodily injury liability covers medical expenses, lost wages, rehabilitation costs, and legal fees when your vehicle injures someone else. Property damage liability pays for damage your vehicle causes to someone else’s property-their car, a storefront, utility pole, or merchandise. Texas minimum auto insurance requirements establish minimums for bodily injury and property damage coverage.

These minimums often fall short of actual accident costs. A serious multi-vehicle collision involving multiple injuries can easily exceed $100,000 in damages, leaving your business responsible for the gap between your policy limits and actual claims. Higher limits protect most commercial operations because one accident can wipe out years of business profits.

Property Damage Limits Match Your Exposure

Property damage limits should align with what your vehicles transport and where they operate. A contractor vehicle transporting expensive equipment justifies higher limits than a service van making local deliveries. The coverage you select today determines whether your business absorbs losses or your insurance policy does.

Collision and Comprehensive Coverage Protect Your Assets

Collision coverage pays to repair or replace your vehicle after an accident regardless of fault. Comprehensive coverage protects against non-collision losses like theft, vandalism, weather damage, and fire. These coverages operate with deductibles-typically $500 to $1,000-that you pay out of pocket before insurance activates. Higher deductibles lower your premiums but increase your out-of-pocket costs when accidents occur.

Uninsured and Underinsured Motorist Coverage Fills Critical Gaps

Uninsured and underinsured motorist coverage addresses a critical gap: when the at-fault driver carries insufficient insurance or none at all, this coverage protects your business and employees. According to the Insurance Information Institute, roughly one in eight drivers nationally operate without insurance, and Texas sees similar rates. If an uninsured driver causes $50,000 in damages and carries zero insurance, your uninsured motorist coverage pays the difference between their liability and your actual losses.

Underinsured motorist protection covers situations where the at-fault driver’s limits fall short of damages-say their policy maxes at $30,000 but damages total $75,000. Most Texas commercial policies include medical payments coverage too, which reimburses medical costs for your employees and passengers regardless of who caused the accident. This eliminates the need to wait for liability claims to resolve before your team receives treatment reimbursement.

Additional Protections Address Specific Business Needs

Beyond these core coverages, your business may benefit from hired and non-owned auto coverage if employees use personal vehicles for work tasks, roadside assistance for breakdowns, or cargo coverage if you transport goods. The right combination of coverages depends entirely on your fleet composition, operations, and risk tolerance. Selecting appropriate coverage limits and optional protections requires honest assessment of your actual exposure rather than simply meeting minimum legal requirements.

How to Pick the Right Policy for Your Fleet

Selecting commercial auto insurance demands honest assessment of your actual operations rather than guessing at coverage needs. Start with documentation of every vehicle your business operates, including purchase price, age, and primary use. A delivery van worth $35,000 justifies different coverage than a $120,000 contractor truck hauling specialized equipment. Next, count your active drivers and pull their driving records-this matters because insurers price policies heavily on driver history. One driver with multiple violations can double your premiums across the entire fleet. Document your annual mileage per vehicle and primary operating areas within Texas, since local risk profiles vary dramatically. Houston’s congested urban driving creates different exposure than rural Hill Country operations.

This documentation becomes your foundation for requesting accurate quotes and selecting appropriate limits.

Getting Real Numbers from Multiple Insurers

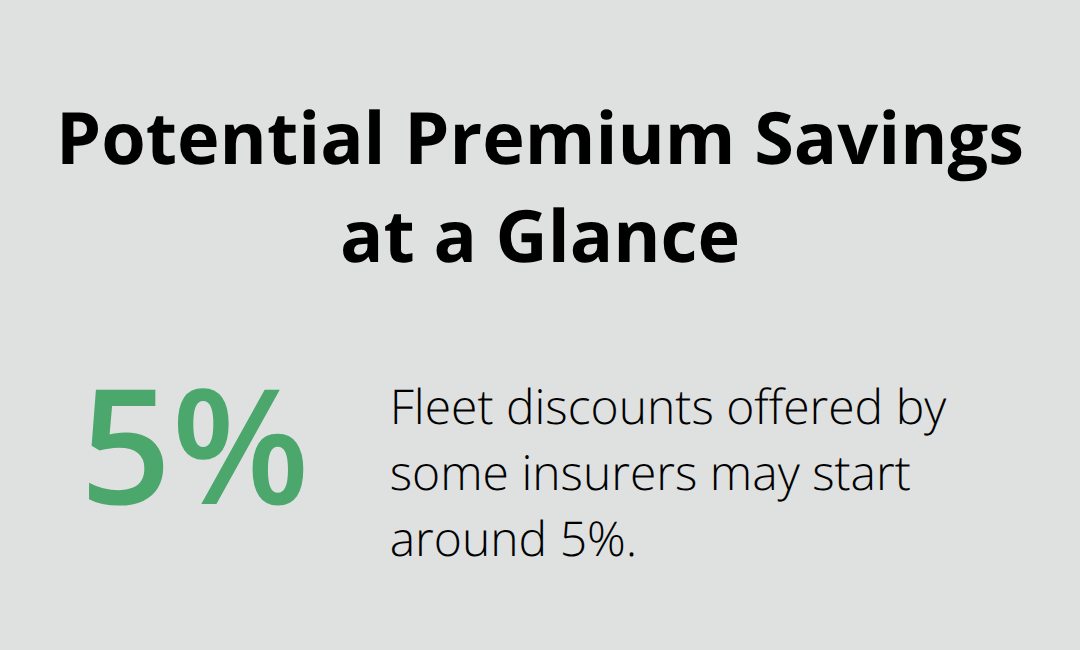

Never accept the first quote you receive-this is where most business owners leave money on the table. Contact at least three insurers and provide identical information to each one so comparisons remain valid. State Farm, Progressive, and Travelers all compete aggressively for Texas commercial accounts, and their pricing varies significantly. Progressive’s telematics programs like Smart Haul can reduce premiums by around $1,056 annually for new truck customers, while fleet discounts start around 5 percent. State Farm emphasizes personalized agent service across Texas, and Travelers provides risk-management resources that help reduce future losses.

As an independent agency, we represent multiple top-rated carriers, which means you access a larger selection of coverage options and pricing than working with a single company. Talk to a licensed insurance agent to find out what coverage works best for your commercial needs. Request quotes with identical deductibles and limits so you compare actual coverage rather than different policy structures. Most insurers provide quotes within 24 hours, and you should receive a certificate of insurance immediately after purchase if you need proof of coverage for business purposes.

Deductibles Shape Your Out-of-Pocket Costs

Your deductible selection directly impacts monthly costs-choosing a $1,000 deductible instead of $500 typically reduces premiums 15 to 25 percent. However, this only makes sense if your business can absorb that $1,000 out-of-pocket expense when accidents occur. Many contractors and service businesses set deductibles at $500 because they operate on thin margins and cannot afford larger unexpected expenses.

Premium Factors That Drive Your Rates

Your premium depends on factors beyond your control: vehicle type and age, your location within Texas, coverage limits selected, and each driver’s complete record (including violations and accidents). A five-year-old Ford Transit van costs less to insure than a new heavy-duty pickup because repair costs differ significantly. Operating primarily in Dallas creates different rates than operating in rural areas due to accident frequency and theft patterns in those regions. The Texas Department of Insurance reports that commercial auto premiums average about $218 monthly statewide, but this reflects only liability coverage-adding collision and comprehensive increases costs substantially.

Uncovering Hidden Discounts

Request quotes that show how each factor affects your premium so you understand what drives your costs. Some insurers offer discounts for safety equipment, driver training programs, or fleet maintenance records that reduce claim frequency. Ask specifically about these discounts because they often get overlooked during the quoting process.

Final Thoughts

Commercial auto insurance in Texas protects your business from financial devastation when accidents happen. The minimum liability limits of $30,000 per person and $60,000 per accident represent legal requirements, not adequate protection for most operations. Your actual exposure depends on fleet size, vehicle types, driver records, and operating locations across Texas.

The path forward starts with honest assessment of your vehicles, drivers, and operations. Document everything: vehicle values and ages, driver records, annual mileage, and primary operating areas. Request quotes from multiple insurers using identical information so you compare actual coverage rather than different policy structures, then evaluate deductible options based on what your business can absorb out of pocket.

We at Brooks Insurance have spent over 50 years helping Texas businesses find the right commercial auto insurance coverage. As an independent agency, we represent multiple top-rated carriers, which means you access a larger selection of coverage options and pricing than working with a single company. Contact Brooks Insurance today to discuss your commercial auto insurance Texas requirements and receive personalized quotes that reflect your actual business operations.