One accident on a job site can cost your contracting business thousands of dollars in liability claims. At Brooks Insurance, we see contractors in Texas face real financial risk every single day without proper protection.

Commercial general liability insurance for contractors isn’t optional-it’s the foundation of a responsible business. This coverage protects you when accidents happen, clients get hurt, or property damage occurs on your projects.

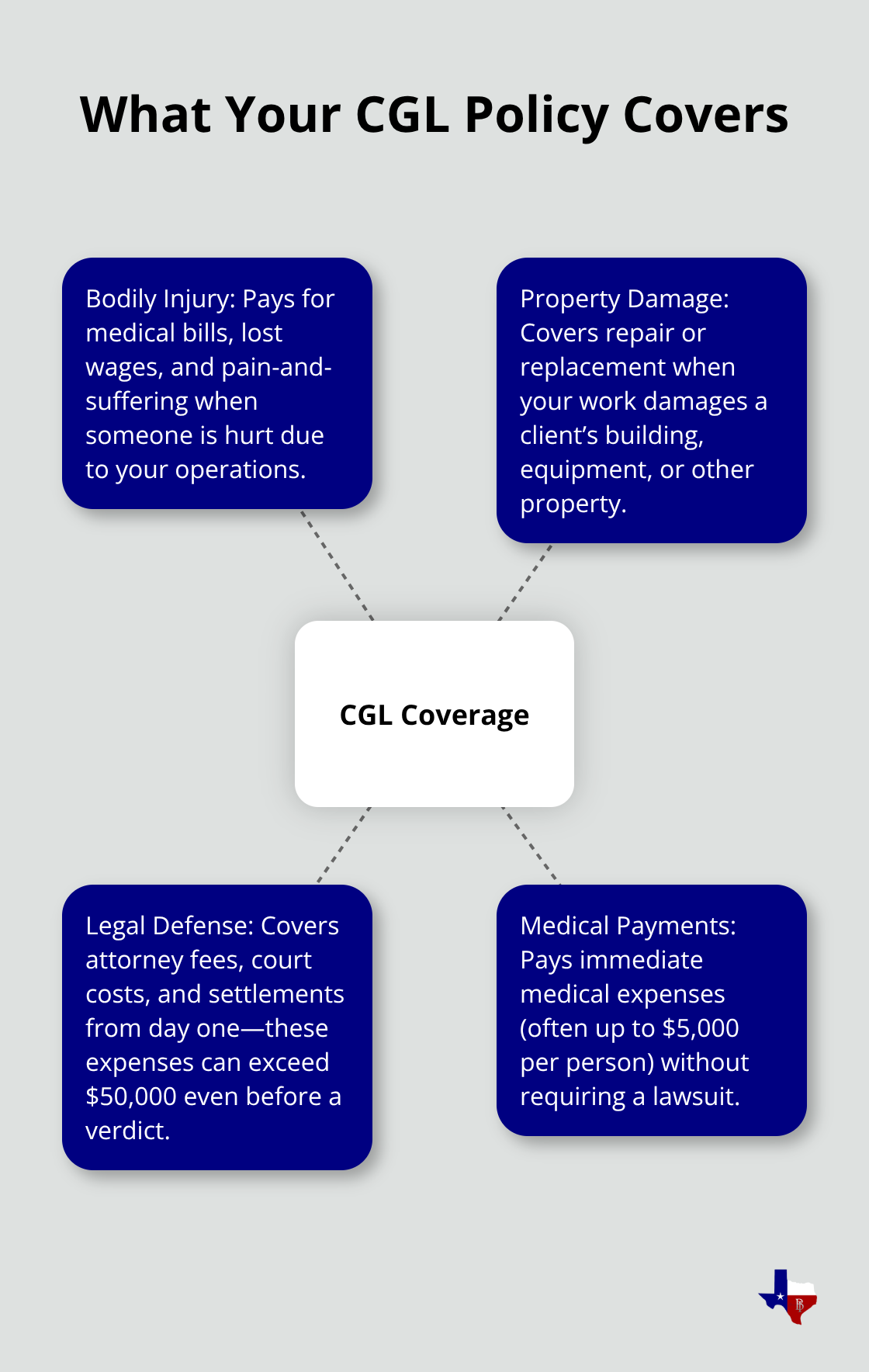

What Your Commercial General Liability Insurance Actually Pays For

Commercial general liability insurance covers three distinct categories of expenses that can devastate a contracting business without proper protection. Bodily injury claims cover medical bills, lost wages, and pain-and-suffering awards when someone gets hurt because of your work or operations. Property damage claims cover repairs or replacement costs when your work damages a client’s building, equipment, or other assets. Your policy also pays for legal defense costs from the moment a claim is filed, including attorney fees, court costs, and settlement negotiations-expenses that can easily exceed $50,000 even before a verdict. Medical payments coverage handles immediate medical treatment for injuries on your job site, typically up to $5,000 per person, without requiring the injured party to file a formal lawsuit.

Bodily Injury and Property Damage: Your Primary Protection

Bodily injury coverage protects you when a worker, client, or bystander suffers an injury on your job site or as a result of your work. Texas contractors face real exposure on every project-a slip-and-fall injury could result in a $100,000+ medical claim plus ongoing lost wages. Property damage claims are equally serious. If your crew accidentally damages a client’s HVAC system or structural elements during renovation work, repair costs can exceed $50,000 within days. This coverage applies whether the injury or damage happens at the job site or away from it, making it your broadest protection against third-party claims.

Legal Defense Costs: The Hidden Expense You Can’t Ignore

Most contractors overlook legal defense costs until they face a claim. Even if you win a case, defending yourself against a frivolous claim costs $25,000 to $75,000 in attorney fees alone. Your policy covers these costs from day one, which protects your cash flow and prevents you from draining business reserves to pay lawyers. This means you can focus on your work while your insurer handles the legal burden.

Medical Payments: Fast Resolution Without Fault Determination

Medical payments coverage pays medical expenses immediately without determining who caused the injury, reducing friction with clients and keeping your reputation intact. This coverage (typically up to $5,000 per person) is your fastest claim resolution tool because it bypasses the lengthy fault-finding process that slows down traditional claims. When an injury happens on your job site, this coverage pays right away, which demonstrates professionalism to your clients and prevents small incidents from becoming major disputes.

Understanding what your policy covers is only half the battle. The real question is whether your coverage limits match the actual risks your contracting business faces on the job.

Why Your Contracting Business Needs This Coverage

Job site accidents aren’t rare occurrences that happen to other contractors-they’re predictable business expenses. A worker trips on scaffolding and breaks an arm. A crew member’s power tool damages the client’s newly installed flooring. A subcontractor accidentally punctures a water line inside the wall. Each scenario costs money, and without commercial general liability insurance, that money comes directly from your business account.

Texas contractors face real exposure on every single project. A slip-and-fall injury can result in medical bills exceeding $100,000 plus ongoing lost wages and pain-and-suffering claims that push settlements toward $250,000 or higher. Property damage claims move even faster-if your crew damages a client’s HVAC system or structural elements during renovation work, repair costs can exceed $50,000 within days.

The financial impact isn’t theoretical. According to the Construction Industry Safety Coalition, about 5,500 nonfatal construction injuries occur weekly in the United States, with many resulting in six-figure claims. Without liability coverage, a single serious accident can wipe out months or years of profit.

Clients Won’t Work With Uninsured Contractors

Most commercial and residential clients require proof of general liability insurance before work begins. Larger projects demand minimum coverage limits of $1 million per occurrence and $2 million aggregate-amounts that protect both you and the client if something goes wrong. Permit authorities in Texas also review insurance requirements for certain projects, particularly those involving structural work or work in occupied buildings.

If you can’t provide a certificate of insurance, you lose the job. General contractors working on residential properties often face strict requirements from homeowners’ insurance carriers, who won’t allow work to proceed without documented liability coverage. Commercial clients-property managers, developers, facility directors-automatically exclude uninsured contractors from their vendor lists. This means your lack of coverage directly reduces your ability to bid on profitable work. Even smaller residential clients increasingly request certificates of insurance as a basic due diligence step, making it harder to land consistent work without it.

Protect Your Business Assets From Catastrophic Claims

A major claim without adequate insurance doesn’t just disappear-it attaches to your personal and business assets. If you face a $500,000 judgment and carry only $300,000 in coverage, the remaining $200,000 becomes your personal liability. Creditors can pursue your business bank accounts, equipment, vehicles, and in some cases your home. General liability insurance separates your personal wealth from your business liability, creating a legal shield that protects what you’ve built.

The cost of this protection is remarkably low compared to the exposure. Most general liability policies for contractors in Texas cost between $56 and $221 per month based on current market data, with an average around $79 per month for basic coverage. That’s less than the cost of a single premium material order or a day of labor, yet it protects against claims that could exceed six figures.

Coverage Limits Matter More Than You Think

Your policy’s per-occurrence and aggregate limits determine how much protection you actually have when claims arrive. A $300,000 per-occurrence limit sounds adequate until you face a serious injury claim that exceeds it. Many contractors discover too late that their limits don’t match their actual exposure, leaving them personally liable for the difference. The right coverage limits depend on your project size, the types of work you perform, and what your clients require in their contracts. Reviewing your existing contracts reveals the minimum insurance requirements your clients impose-and those minimums should inform your coverage decisions. Your annual revenue and total business assets also matter; contractors with higher revenue streams and more equipment at risk typically need higher limits to protect their financial position.

Understanding what coverage you need sets the stage for selecting limits that actually protect your business from the real risks you face on job sites.

How to Choose the Right Coverage Limits for Your Contracting Business

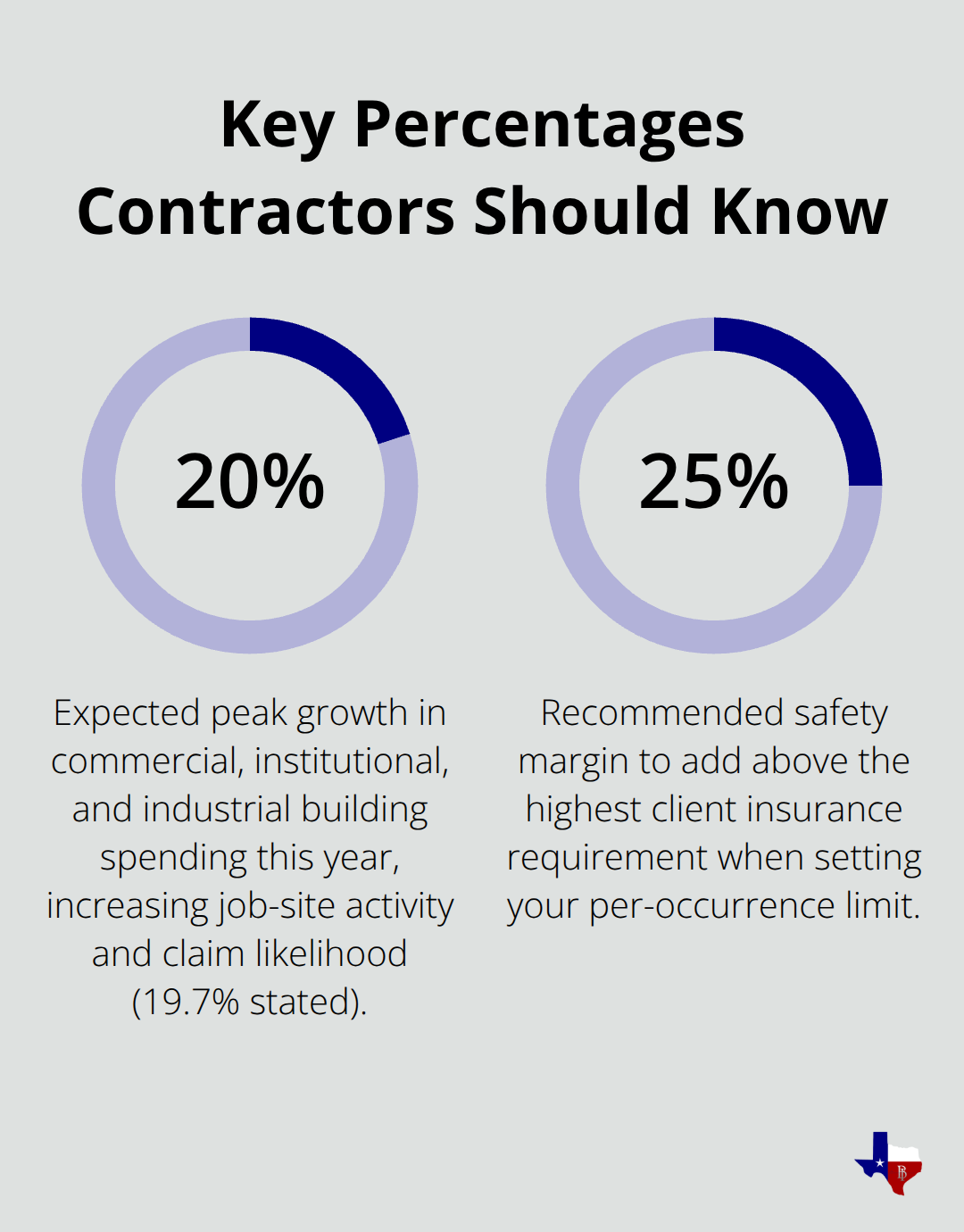

Choosing coverage limits feels abstract until you face a real claim. The $300,000 per-occurrence limit that seemed reasonable during your initial quote becomes dangerously inadequate when a serious injury claim lands on your desk. The right approach starts with three concrete factors: the specific work you perform, what your clients contractually demand, and the financial scale of your business. Roofing contractors face different injury risks than demolition crews, and high-rise work carries exposure that residential remodeling doesn’t. A client renovation project worth $500,000 typically requires minimum coverage of $1 million per occurrence and $2 million aggregate, but a $2 million commercial build-out may demand $2 million per occurrence limits. Your annual revenue directly influences your exposure too-a contractor pulling $1 million annually faces different financial consequences from claims than one generating $5 million in revenue. Leading industry economists expect spending growth for commercial, institutional and industrial buildings to peak at 19.7% this year, meaning more projects are active, more job sites exist, and statistically more claims will occur. That increased activity makes your coverage limits a business survival decision, not an insurance checkbox.

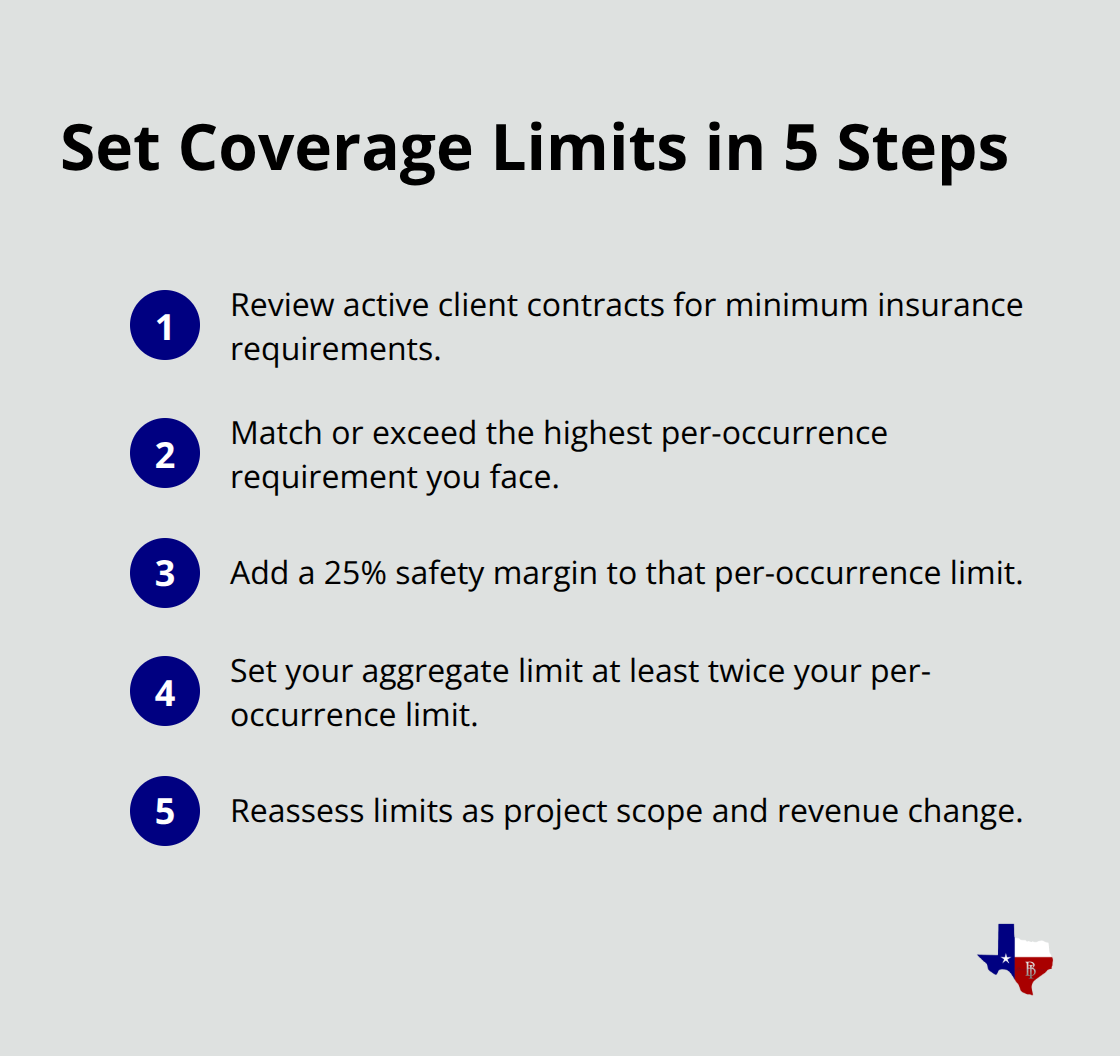

Review Your Client Contracts First

Start with every active client contract you hold-not the ones you might get, but the agreements you’re currently working under. These contracts specify minimum insurance requirements, and those numbers represent your clients’ risk assessment of what you need. If three major clients require $1 million per occurrence and two require $2 million, your coverage should meet the highest requirement or exceed it. Permit authorities in Texas also impose requirements for certain project types, particularly structural work and renovations in occupied buildings. Your contracts reveal the actual demands your clients place on your business, and ignoring those demands costs you jobs.

Calculate Your Asset and Revenue Exposure

Your business assets and annual revenue create the second critical data point. If your contracting operation owns $300,000 in equipment, vehicles, and tools, a $300,000 per-occurrence limit leaves you personally liable for any claim exceeding that amount. A single serious injury claim (averaging $100,000 to $250,000 based on Construction Industry Safety Coalition data) consumes your limit quickly, and a catastrophic claim pushing $500,000 or higher wipes out your coverage entirely. Contractors generating $2 million in annual revenue typically need higher limits than those doing $500,000 annually because their larger projects attract proportionally larger claims. The cost difference between a $1 million and $2 million per-occurrence limit averages only $20 to $40 monthly based on current Texas pricing, making the upgrade financially trivial compared to the protection it provides.

Set Limits That Match Your Actual Exposure

Many contractors assume their basic coverage is sufficient because the monthly premium feels manageable, but that reasoning ignores the actual financial exposure your projects create. Evaluate your three largest active projects and identify the highest client insurance requirement among them, then set your per-occurrence limit at or above that threshold. Your aggregate limit-the total your policy pays across all claims in one year-should be at least double your per-occurrence limit, protecting you against multiple claims.

A contractor facing two $800,000 claims in the same year with only a $1 million aggregate limit pays the second claim partially out of pocket. The math is straightforward: assess your current contracts, identify your highest requirement, add 25 percent for safety margin, and lock in that limit. This approach eliminates guesswork and ties your coverage directly to the real work you perform.

Final Thoughts

Commercial general liability insurance for contractors protects your cash flow when accidents happen, satisfies client requirements that determine which jobs you can bid on, and shields your personal assets from claims that exceed your limits. Without it, a single serious injury or property damage incident eliminates years of profit and threatens everything you’ve built. Your clients will demand proof of coverage before work begins, and your contracts specify minimum limits you must carry.

The practical reality is straightforward: set coverage limits that match your real exposure by reviewing your active client contracts and identifying the highest insurance requirement among them. Add 25 percent as a safety margin, then set your per-occurrence limit at that threshold. Ensure your aggregate limit is at least double your per-occurrence limit to protect against multiple claims in a single year, and this approach ties your coverage directly to the actual work you perform.

We at Brooks Insurance understand the specific risks Texas contractors face on job sites every day. Contact us today for a personalized quote that reflects your contracting business’s real needs-visit brooksinstx.com or call our team to discuss your commercial general liability insurance for contractors options and get protected before your next project begins.

Disclaimer: The information provided in this blog is for general informational purposes only and does not constitute legal, financial, or insurance advice. Coverage options, terms, and availability may vary. Please consult with a licensed professional for advice specific to your situation