Your business needs a certificate of general liability insurance to protect itself from costly lawsuits and third-party claims. Whether you’re a contractor, consultant, or service provider in Texas, this document proves you have active coverage.

At Brooks Insurance, we’ve helped countless Texas businesses understand why this certificate matters and how to get one quickly. This guide walks you through everything you need to know.

What a Certificate of General Liability Insurance Actually Is

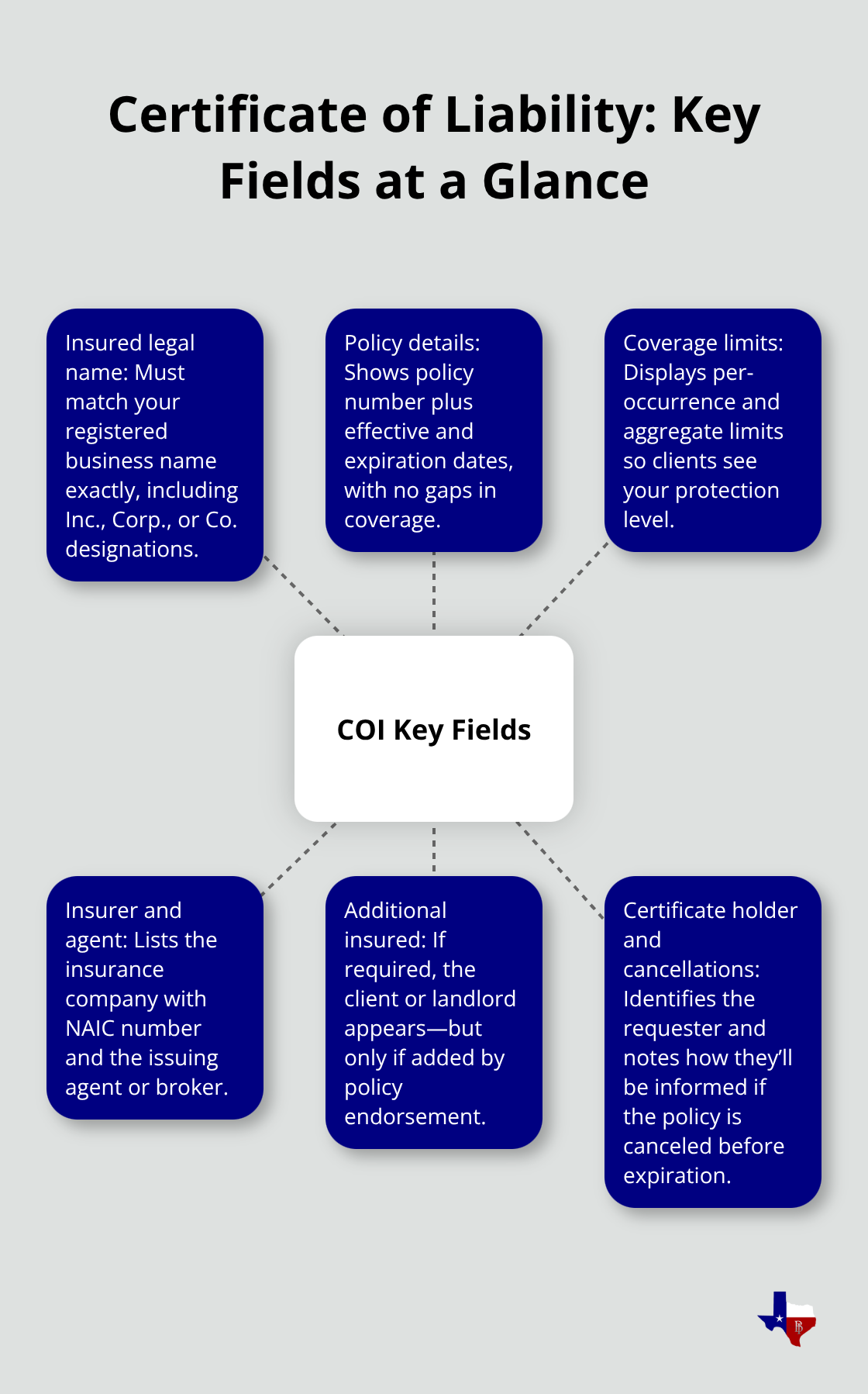

A certificate of liability insurance is a one-page document that proves your business carries active coverage for third-party bodily injury and property damage claims. It’s not the insurance policy itself-it’s proof that the policy exists. The certificate lists your policy number, coverage limits, the insurance company’s name, your business name, and the dates your coverage is active. Think of it as a snapshot of your insurance status at a specific moment in time. When a client, landlord, or contractor asks for proof of insurance before work begins, this certificate is what you provide. The document follows the ACORD 25 form, an industry standard created by ACORD, a nonprofit standards organization that ensures consistency across the insurance industry worldwide.

Who actually needs this certificate

Contractors, service providers, consultants, and vendors in Texas need certificates regularly. If you work on client sites, rent commercial space, or supply services to businesses, someone will ask for one. Landlords require certificates before leasing space to ensure tenants carry liability coverage. Construction clients demand them before allowing work to start on their properties. Event venues request certificates from vendors and performers. Many government contracts, including work with the State Fire Marshal’s Office in Texas, require a current certificate showing general liability coverage. If you own a small business with employees or handle client projects, you need this certificate ready. The document protects both you and the other party by clearly showing who carries the financial responsibility if something goes wrong.

What information appears on the certificate

The certificate displays the insured’s full legal name exactly as registered (including Inc., Corp., or Co. designations). It shows your policy number, effective date, and expiration date with no coverage gaps. The coverage limits appear prominently, showing how much protection you carry per occurrence and in total.

Your insurance company’s name and NAIC number are listed, along with the agent or broker who issued the certificate. If a client or landlord requires additional insured status, their name appears on the certificate as well, though this requires them to be added to your actual policy, not just the certificate. The certificate holder field shows who requested the certificate-typically your client or landlord. A cancellation notice section informs the certificate holder if your policy is canceled before the expiration date.

Verifying accuracy before you submit

Mismatched information or expired dates can delay projects or damage business relationships. Check that the insured name matches your business registration exactly. Confirm the policy expiration date falls after your project completion date. Verify that all coverage types listed match what you actually purchased. If you added anyone as an additional insured, confirm their name appears correctly on the certificate. Many businesses maintain a digital repository of current certificates so they can provide updated documents on demand to multiple clients. This approach saves time and prevents the embarrassment of sending outdated proof of coverage.

Moving forward with your certificate

Now that you understand what a certificate is and why businesses request it, the next step involves learning how to obtain one and what happens when you request it from your insurance provider.

How to Get and Use Your Certificate

Request your certificate immediately after purchase

Your general liability policy automatically generates a certificate once coverage becomes active, so no extra step or fee applies to obtaining one. Most Texas insurance companies deliver certificates within hours or by the next business day, though some providers now offer instant digital issuance through online portals. You request the certificate from your insurance agent or through your insurer’s online account dashboard by providing your policy number and specifying who should be listed as the certificate holder. The certificate holder is whoever requested the document-typically your client, landlord, or contractor. Processing happens nearly instantaneously with many modern platforms, meaning you can often send proof of coverage to a demanding client the same day you purchase your policy. When requesting your certificate, confirm that your business name matches your legal registration exactly, including all corporate designations like Inc. or Corp., since mismatched names create compliance issues, especially for State Fire Marshal’s Office registrations in Texas which require precise legal naming.

Understand how coverage limits affect your certificate

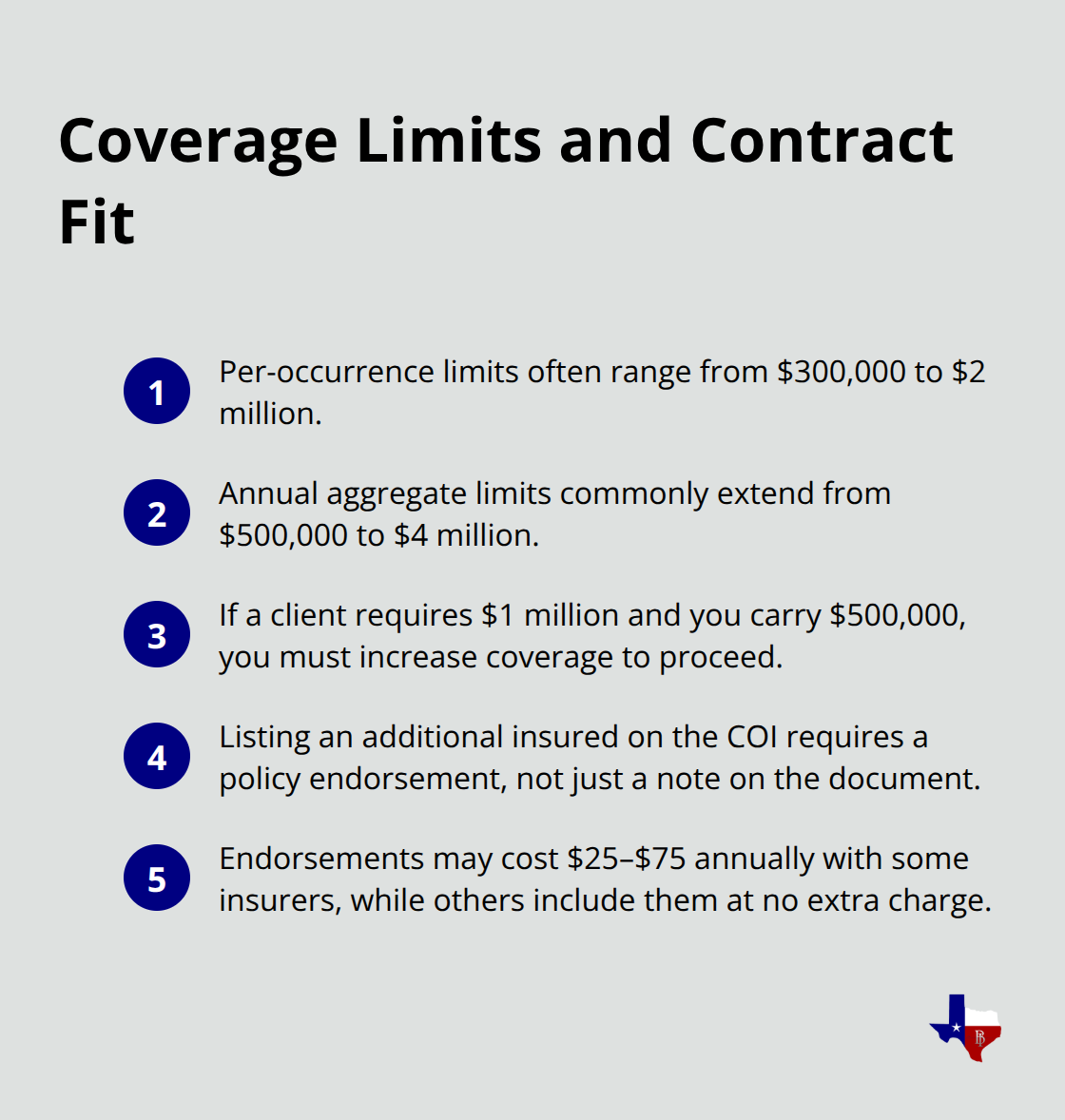

Coverage limits on your certificate directly reflect what you purchased in your actual policy, and this matters significantly because contractual requirements often specify minimum limits you must carry. General liability policies typically offer per-occurrence limits ranging from $300,000 to $2 million, with annual aggregate limits extending from $500,000 to $4 million depending on your business type and risk profile. If a client requires $1 million per occurrence and your certificate shows only $500,000, the contract won’t proceed until you increase coverage.

Adding someone as an additional insured on your certificate requires them to be added to your actual policy through an endorsement, not merely listed on the document-this is where many business owners get confused and waste time. Some insurers charge $25 to $75 annually for additional insured endorsements, while others include this at no extra cost, so clarifying this during purchase prevents surprises.

Keep your certificates current and organized

Your certificate remains valid only while your underlying policy stays active; once coverage expires, the certificate becomes worthless as proof even if you haven’t physically updated it. Many contractors and service providers mistakenly believe a certificate continues covering them after expiration, leading to project delays when clients request current proof. Maintaining a digital folder of your current certificates for each policy type-general liability, workers’ compensation, and professional liability if applicable-lets you respond instantly when clients demand documentation, preventing project start delays that cost you money.

Know what happens when you add additional insureds

Adding an additional insured to your certificate involves more than just listing a name on the document. Your insurance company must add them to your actual policy through a formal endorsement, which typically takes one to three business days. This endorsement grants the additional insured certain rights, such as notice if your policy is canceled or not renewed before the expiration date. However, being listed as an additional insured does not automatically grant them coverage under your policy unless the endorsement specifically extends protection to them. Clarifying these distinctions with your insurance agent prevents misunderstandings that could leave your client or partner unprotected when they believe they have coverage.

Understanding how to obtain and maintain your certificate sets the foundation for meeting client requirements, but knowing what information actually appears on the document and how to verify its accuracy prevents costly mistakes before you submit it to demanding clients or landlords.

Why Your Business Needs This Certificate

A certificate of general liability insurance protects your business from financial ruin when clients, landlords, or contractors hold you accountable for accidents. Without proof of coverage, you face two serious problems: first, you expose your personal assets to lawsuits if someone gets injured or property gets damaged at a job site, and second, you lose business opportunities because clients won’t work with uninsured vendors. The State Fire Marshal’s Office in Texas requires a current certificate showing at least $100,000 per occurrence and $300,000 total annual coverage before registering certain businesses, meaning you cannot legally operate in some sectors without this document. Construction projects, commercial leasing agreements, and event contracts all demand certificates before work begins, and missing this requirement delays your start date and costs you money.

Why clients demand this document before work starts

Clients request certificates because they need proof you will pay for damages if something goes wrong on their property or during your service delivery. A contractor working on a commercial renovation will not allow you on-site without seeing your certificate because your mistake could cost them hundreds of thousands in repairs, and they want assurance your insurance covers it. Landlords require certificates from tenants to verify liability coverage exists before leasing space, protecting themselves from tenant-caused fires, injuries, or property damage. If you cause an accident without active coverage, the injured party or property owner sues your client instead, making them liable for your negligence. This is why clients care less about your reputation and more about your certificate-it is the only proof that money exists to pay claims.

How additional insured status protects your relationships

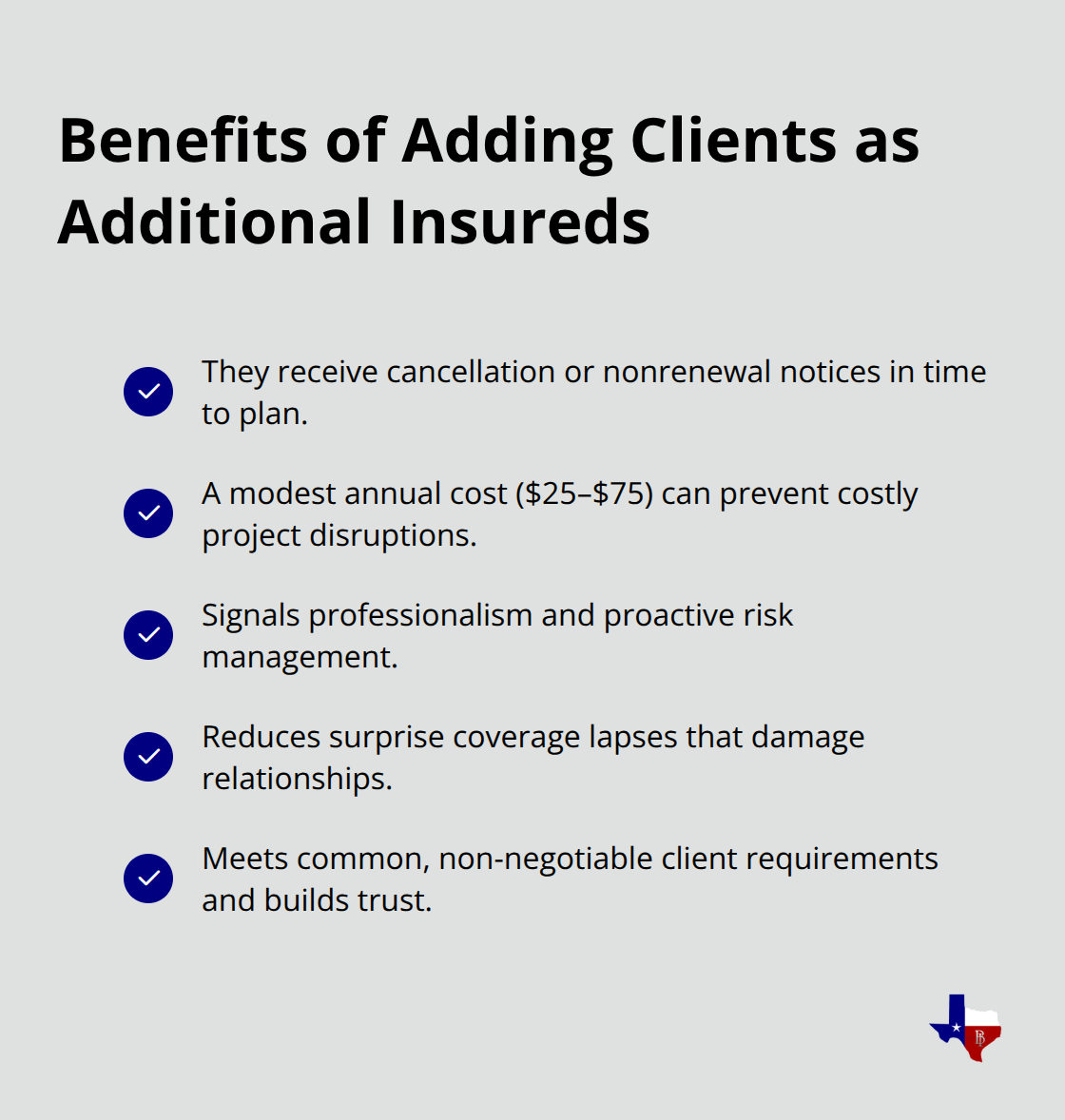

Adding a client as an additional insured on your policy does more than satisfy a contract requirement-it signals you take their risk seriously and have skin in the game if something goes wrong. When a client is added as an additional insured through a formal endorsement, they receive notice if your policy is canceled or not renewed before the expiration date, giving them time to find backup coverage or adjust their project timeline. This endorsement typically costs $25 to $75 annually depending on your insurer, but it prevents relationship-damaging surprises where your coverage lapses unexpectedly.

Many service providers resist adding additional insureds because they see it as extra cost, but clients view it as non-negotiable protection that shows you stand behind your work. Without this endorsement, your client could discover mid-project that your coverage ended, forcing them to halt work and find emergency coverage at premium rates.

What happens when you skip this step

Missing the additional insured requirement creates serious consequences. Your client may discover mid-project that you failed to add them as required by the contract, leading them to halt work immediately and demand you fix the problem before proceeding. This delay costs you money and damages your professional reputation with that client and their referral network. Some contracts include penalty clauses for missing insurance requirements, meaning you could face financial consequences beyond the lost work time. Texas businesses lose contracts every month because they failed to provide a current certificate when requested or forgot to add the client as an additional insured when the contract specified it.

Building trust through insurance transparency

Clients view your certificate as proof you operate professionally and take their protection seriously. When you provide a current certificate without being asked and proactively add them as an additional insured (when appropriate), you demonstrate that you understand their concerns and respect their risk management requirements. This approach strengthens long-term business relationships and makes you the preferred vendor over competitors who treat insurance as an afterthought. Your willingness to handle insurance details correctly signals that you will handle project details correctly as well.

Final Thoughts

A certificate of general liability insurance proves you operate professionally and protects your business from financial disaster when accidents happen on client property. This document meets contractual requirements, satisfies landlord demands, and builds trust with partners who need assurance before allowing you on-site. Without it, you lose business opportunities and expose yourself to legal liability that could devastate your personal finances.

Getting your certificate takes minimal effort once you purchase a general liability policy-request it from your insurance agent or through your insurer’s online portal, verify the information matches your business registration exactly, and keep it current as your policy renews. If clients require additional insured status, add them through a formal endorsement rather than simply listing their name on the document. This small investment in clarity prevents project delays and demonstrates you take their protection seriously.

The next step involves finding the right general liability coverage for your specific business needs, and coverage limits, pricing, and policy terms vary significantly between insurers. We at Brooks Insurance have spent over 50 years helping Texas businesses find the right coverage at competitive rates, and our licensed agents represent multiple top-rated insurance companies to give you a larger selection of options. Contact us today to speak with one of our agents about your certificate of general liability insurance needs.

Disclaimer: The information provided in this blog is for general informational purposes only and does not constitute legal, financial, or insurance advice. Coverage options, terms, and availability may vary. Please consult with a licensed professional for advice specific to your situation