One accident on a client’s property can cost your landscaping business thousands of dollars in liability claims. Without proper protection, a single injury or property damage incident could threaten your entire operation.

At Brooks Insurance, we help Texas landscaping companies understand why landscaping general liability insurance isn’t optional-it’s essential. This guide walks you through what coverage protects you, why you need it, and how to choose the right limits for your business.

What Your General Liability Coverage Actually Protects

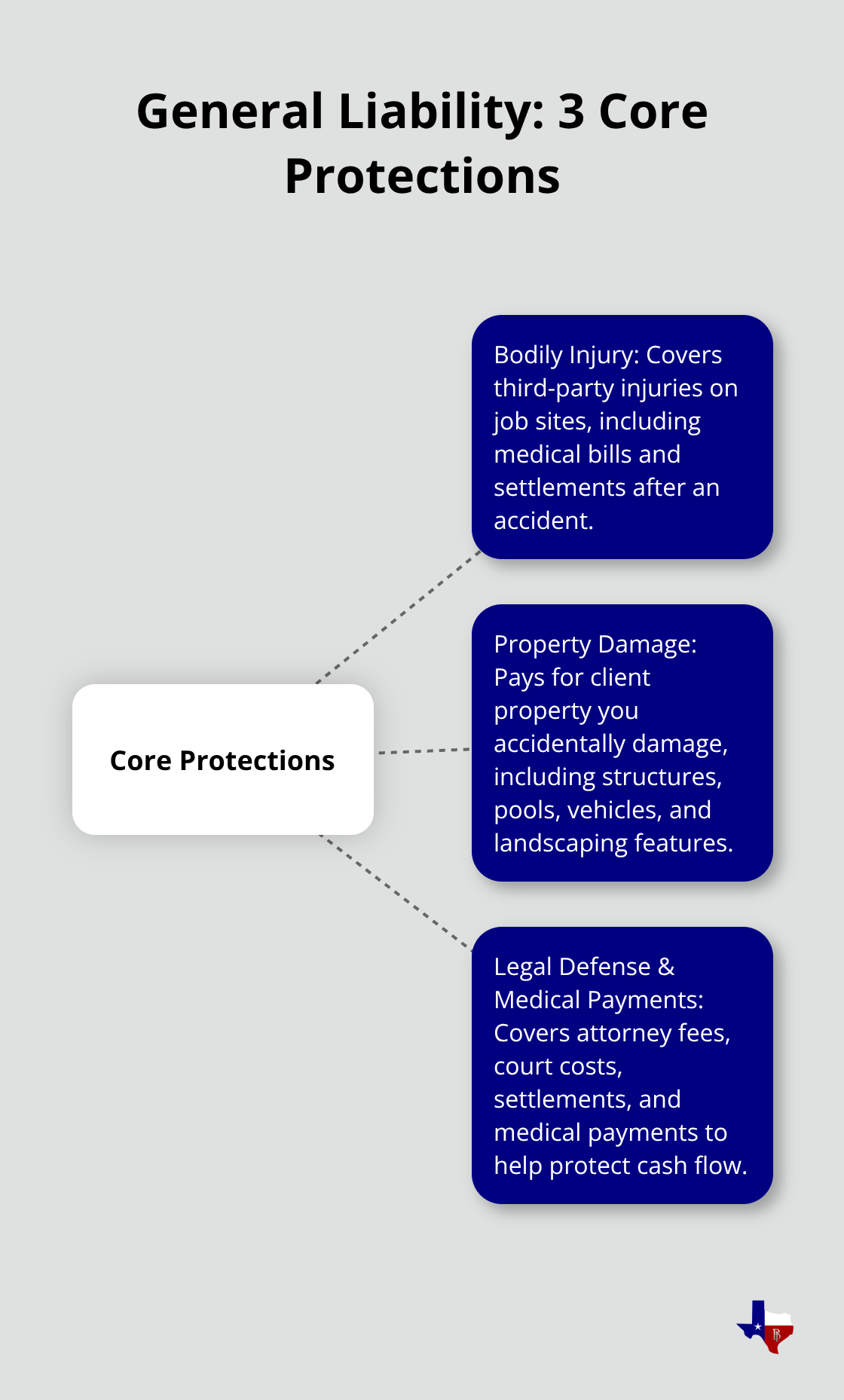

Three Core Areas of Protection

General liability insurance covers three main areas that directly impact your landscaping business. First, it protects you when a third party suffers bodily injury on a job site. If a homeowner trips over your equipment, gets struck by debris from a mower, or experiences an injury from pesticide exposure, your general liability policy covers their medical bills and any settlement or court judgment against you. Second, the policy covers property damage you cause to a client’s property. This includes damage to structures, pools, vehicles, or landscaping features that result from your work. A mower throws a rock through a window, irrigation work damages underground utilities, or equipment punctures a roof-all fall under this protection. Third, general liability covers your legal defense costs and medical payments. When a claim arises, your insurer pays for attorney fees, court costs, and settlements, protecting your cash flow when you need it most.

Additional Coverage You May Not Expect

Many policies also include personal and advertising injury coverage, which protects against copyright infringement claims or slander allegations related to your business activities. This layer of protection matters more than most landscapers realize, especially when you work across multiple client sites and handle sensitive business communications. The coverage extends beyond physical accidents to include reputational risks that can damage your business standing.

What General Liability Does Not Cover

What general liability does not cover matters just as much as what it does. The policy excludes injuries to your own employees, which is why workers’ compensation insurance remains separate. It does not cover damage to your own equipment or property, accidents involving your company vehicles, or professional mistakes in your work. This is why many Texas landscaping companies bundle general liability with commercial auto insurance, tools and equipment coverage, and workers’ compensation. General liability costs roughly $37 to $71 per month for landscapers, making it affordable protection against claims that could otherwise bankrupt your operation.

Standard Policy Limits and Real-World Requirements

The standard policy includes bodily injury limits typically ranging from $300,000 to $1,000,000 per occurrence, with annual aggregate limits from $300,000 to $2,000,000. Many clients and property managers in Texas now require proof of general liability before you work on their sites, especially HOAs and commercial properties. Without this coverage, a single accident forces you to pay medical bills, repair costs, and legal fees directly from your business account, leaving nothing for payroll or operations.

Understanding what your policy covers sets the foundation for protecting your business, but selecting the right coverage limits requires a closer look at your specific risk exposure and the types of projects you handle.

Why Your Landscaping Business Cannot Afford to Skip This Coverage

Accidents Happen on Client Property

Landscaping work happens on client property where accidents are not a matter of if but when. A homeowner trips over a hose, a mower throws a rock through a window, or irrigation work damages an underground pipe. According to the U.S. Bureau of Labor Statistics, Texas employed approximately 68,500 landscaping workers as of May 2023, and with that volume of activity comes real exposure to liability claims. Without general liability insurance, you pay these costs directly from your business account. A single claim for property damage can easily reach $5,000 to $15,000 just for repairs, and bodily injury claims routinely exceed $50,000 once medical expenses and legal fees accumulate.

Texas Market Demands Insurance as Standard

Many Texas landscapers operate under the assumption that one accident won’t happen to them, but claims data shows otherwise. HOAs and commercial property managers across Texas now demand proof of general liability before allowing any contractor on their sites. High property values in areas like Dallas–Fort Worth mean that property damage claims cost significantly more than they would in lower-value neighborhoods. Extreme Texas weather, including hail storms and flooding, also amplifies both the frequency and severity of damage claims. If a client’s pool suffers damage during a landscaping project or a structure gets struck by equipment during a storm, your liability exposure increases substantially. Without coverage, you cannot legally operate on many commercial contracts or residential communities that require insurance as a condition of work.

Litigation Costs Threaten Your Business Survival

General liability also protects you against lawsuits that could otherwise force you to liquidate assets or shut down operations entirely. An average business spends about $1.2 million annually on litigation costs, and landscaping companies face the same financial exposure. When a claim lands on your desk, your insurer covers attorney fees, court costs, and settlements rather than forcing you to drain your operating capital. Texas does not mandate general liability for private landscaping contractors, but the market does. Clients and property managers treat proof of insurance as a credential that signals professionalism and reduces their own liability exposure.

Affordable Protection Against Financial Ruin

The cost of general liability insurance at $37 to $71 per month is negligible compared to the financial devastation a single uninsured claim creates. You cannot control when accidents happen, but you can control whether you have the protection in place to survive them. As an independent agency with over 50 years of experience, Brooks Insurance works with Texas landscaping companies to match them with coverage that fits their actual risk profile and project types. The right policy transforms a potential catastrophe into a manageable claim that your insurer handles while you continue operations.

How to Choose the Right Coverage Limits for Your Landscaping Business

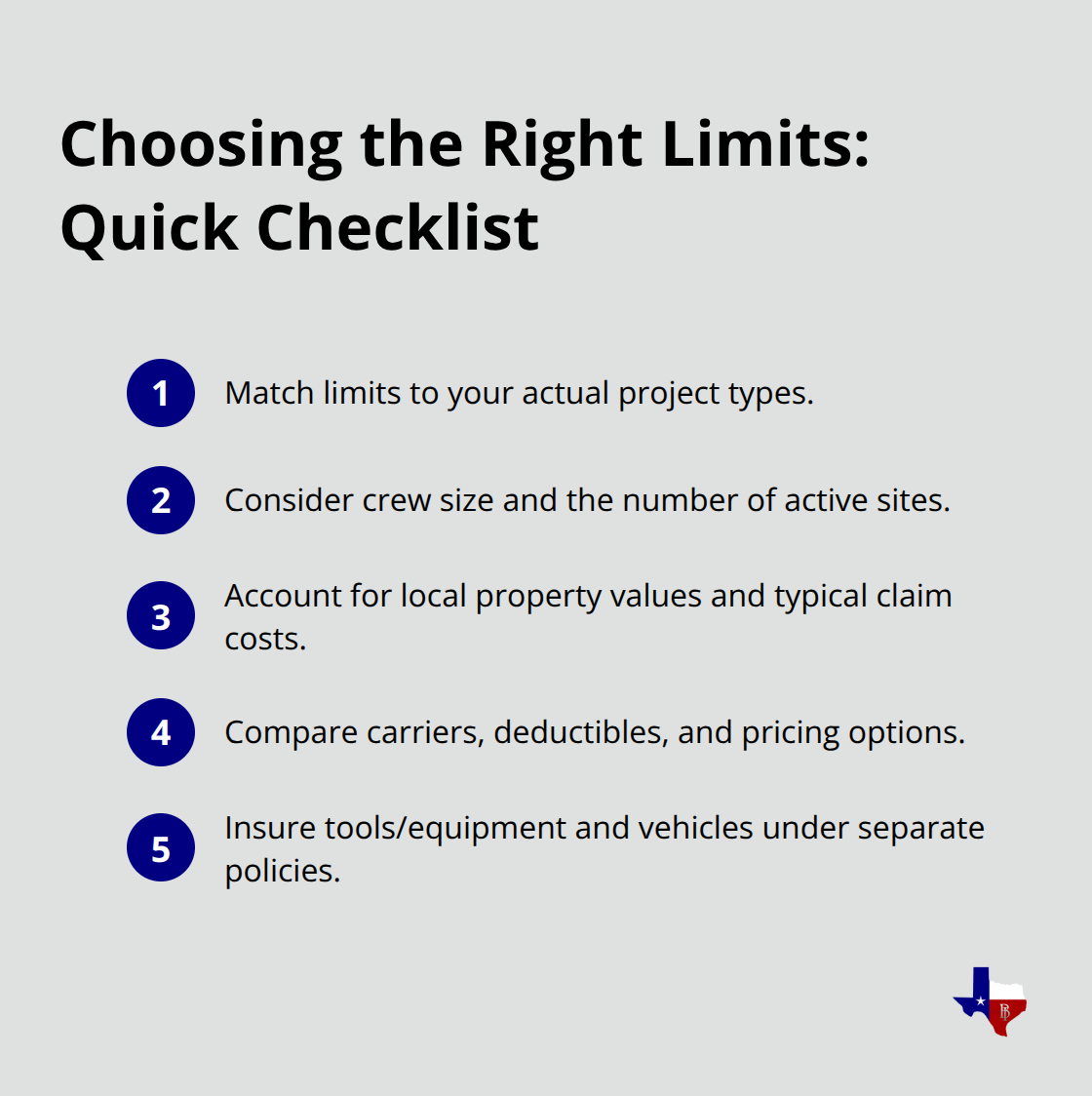

Match Coverage Limits to Your Actual Work

Start with your project types, not industry averages. A solo operator mowing residential lawns faces different risks than a crew installing irrigation systems or applying pesticides on commercial properties. The size of your operation matters too. If you have two employees, your exposure differs significantly from a ten-person crew working multiple sites daily. Texas landscapers commonly operate with $300,000 per-occurrence limits, but this baseline often underprotects against modern claim costs.

Account for Texas Property Values and Claim Costs

Property damage claims in Dallas–Fort Worth frequently exceed $10,000 because high property values mean repairs to pools, structures, and vehicles cost substantially more than in other regions. Bodily injury claims routinely reach $50,000 to $100,000 once medical expenses, lost wages, and legal fees accumulate. Landscapers in Texas should evaluate whether $500,000 or $1,000,000 per-occurrence limits make more sense for their specific work. A crew working on high-value commercial properties should seriously consider $1,000,000 limits with $2,000,000 annual aggregate coverage. The monthly cost difference between $300,000 and $1,000,000 limits is typically $15 to $25, making the upgrade affordable protection against underprotection that could devastate your business.

Compare Carriers and Deductible Options

Shop coverage from multiple carriers before deciding on limits, because pricing and available options vary significantly across insurers. Some carriers offer no deductible on liability claims, meaning you avoid out-of-pocket costs when a claim occurs, while others require $500 to $1,000 deductibles that reduce your monthly premium but increase your financial exposure per claim. An independent agency like Brooks Insurance can help you compare options across multiple carriers rather than limiting you to a single insurer’s offerings.

Protect Your Equipment and Vehicles Separately

Tools and equipment coverage, also called Inland Marine insurance, protects your mowers and trimmers whether on a job site or in transit. This costs roughly $33 to $64 per month and covers theft, vandalism, and accidents with per-item limits typically between $3,000 and $5,000. Many Texas landscapers skip this coverage and regret it when a truck is broken into or a high-value mower gets damaged during transport. Commercial auto coverage is separate from general liability and protects your vehicles during work use. A personal auto policy explicitly excludes business use, so a dump truck or pickup truck used for landscaping work must be covered under commercial auto insurance. Standard commercial auto policies provide combined single limits ranging from $85,000 on basic plans to $1,000,000 on comprehensive plans.

Bundle Policies and Pay Strategically to Reduce Costs

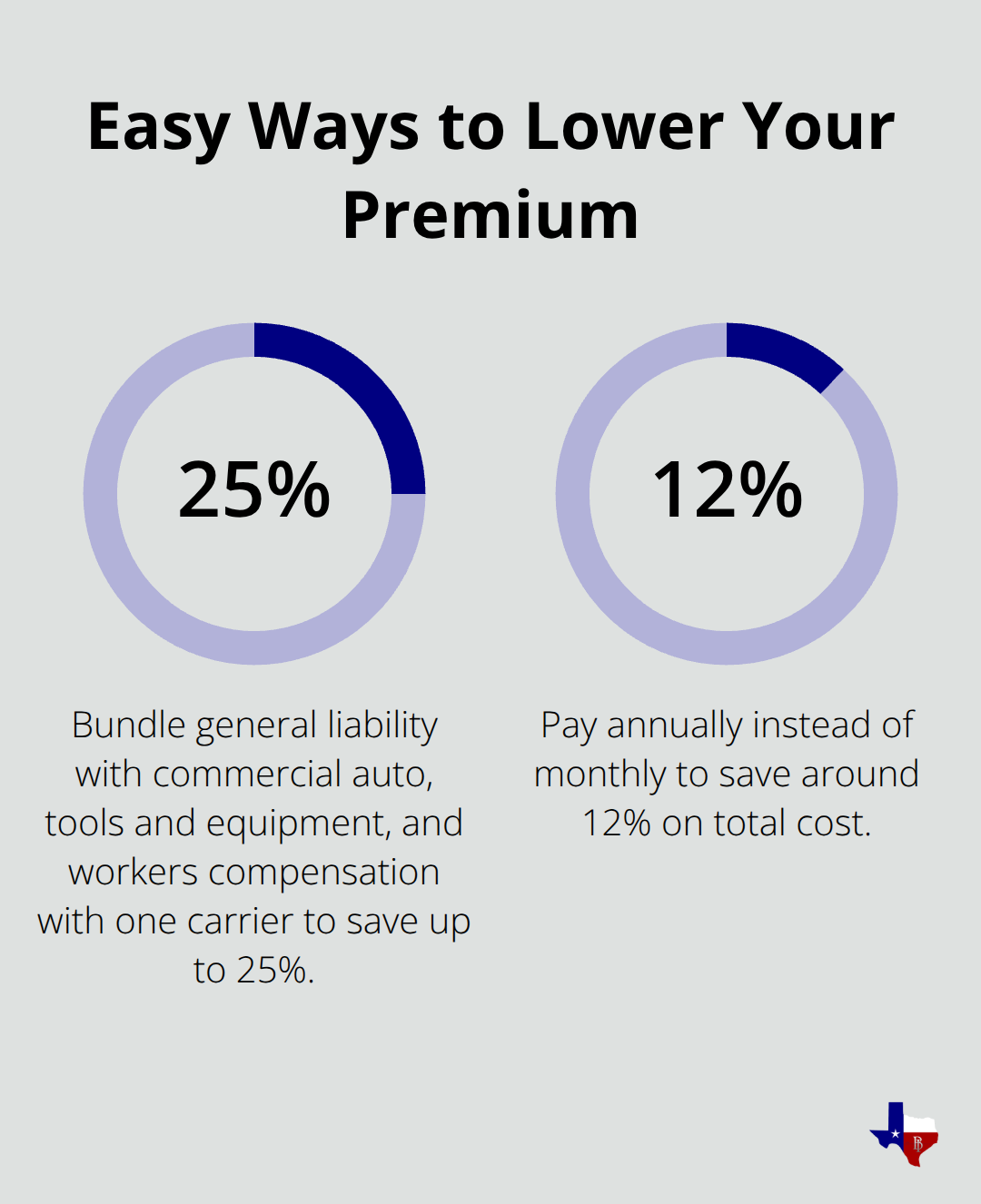

Workers compensation, while not mandatory for private employers in Texas, typically costs around $162 per month and protects your employees against work-related injuries. When you bundle general liability with commercial auto, tools and equipment, and workers compensation from the same carrier, you can save up to 25% on your total premium compared to purchasing policies separately. Annual payments instead of monthly payments also generate savings of around 12%, so paying upfront reduces your overall insurance cost substantially.

The key is matching your coverage limits to your actual risk, not copying what competitors carry or accepting whatever a broker recommends without question.

Final Thoughts

Landscaping general liability insurance protects your business from the financial devastation that a single accident can cause. Whether a client trips over equipment, a mower damages property, or irrigation work breaks an underground utility, your coverage handles medical bills, repair costs, and legal fees while you keep operations running. The cost of $37 to $71 per month is negligible compared to the thousands or tens of thousands of dollars a claim can cost without protection.

Assess your current risk exposure by listing the types of projects you handle, the size of your crew, and the property values where you work. Then compare coverage options across multiple carriers to find limits that match your actual needs rather than industry defaults. A $300,000 per-occurrence limit may leave you underprotected if you work on high-value properties in Dallas–Fort Worth, where repairs and medical claims routinely exceed that amount, so consider whether $500,000 or $1,000,000 limits make more sense for your operation.

Contact Brooks Insurance today to get a quote and start protecting your landscaping business with coverage that actually fits your operation. Our licensed agents understand the specific risks landscapers face across Texas and can help you match your policy limits to your business model. We represent multiple top-rated insurance companies, giving you access to a wider range of coverage options and pricing than you would find working with a single carrier.

Disclaimer: The information provided in this blog is for general informational purposes only and does not constitute legal, financial, or insurance advice. Coverage options, terms, and availability may vary. Please consult with a licensed professional for advice specific to your situation