Running a business means managing multiple risks. One of the biggest is protecting your company vehicles and the people who operate them.

At Brooks Insurance, we help Texas business owners understand what commercial auto insurance covers-and what it doesn’t. This guide breaks down the coverage types you need to know about.

What Commercial Auto Insurance Actually Covers

Personal auto policies explicitly exclude vehicles used for business purposes. If you use a company car to visit clients, make deliveries, or transport equipment, your personal auto policy will not cover accidents, theft, or damage. This gap leaves your business vulnerable to significant financial losses. Commercial auto insurance fills that gap by covering vehicles driven by employees or used for business activities. About 2.7 million small businesses in Texas rely on commercial auto to protect their work vehicles, which tells you how widespread this need is across the state. The coverage protects your business from liability claims when someone is injured or property is damaged due to your vehicle operations. It also covers physical damage to your own vehicles from collisions, theft, weather, or vandalism. Without it, a single accident involving a company vehicle could cost your business tens of thousands of dollars out of pocket.

When You Actually Need Commercial Coverage

Texas law requires minimum liability limits of 30/60/25, meaning $30,000 per person for bodily injury, $60,000 total per accident for bodily injury, and $25,000 for property damage. This minimum applies to any vehicle used for business purposes. Personal injury protection is also mandatory in Texas for liability policies unless you sign a written waiver. If you operate a food truck, run a cleaning service, manage a landscaping crew, work as an electrician, or offer NEMT services, commercial auto insurance is non-negotiable. Even contractors who occasionally drive to job sites need this coverage. The distinction matters because insurers treat business use as higher risk than personal commuting, which is why they exclude it from personal policies and require separate commercial policies.

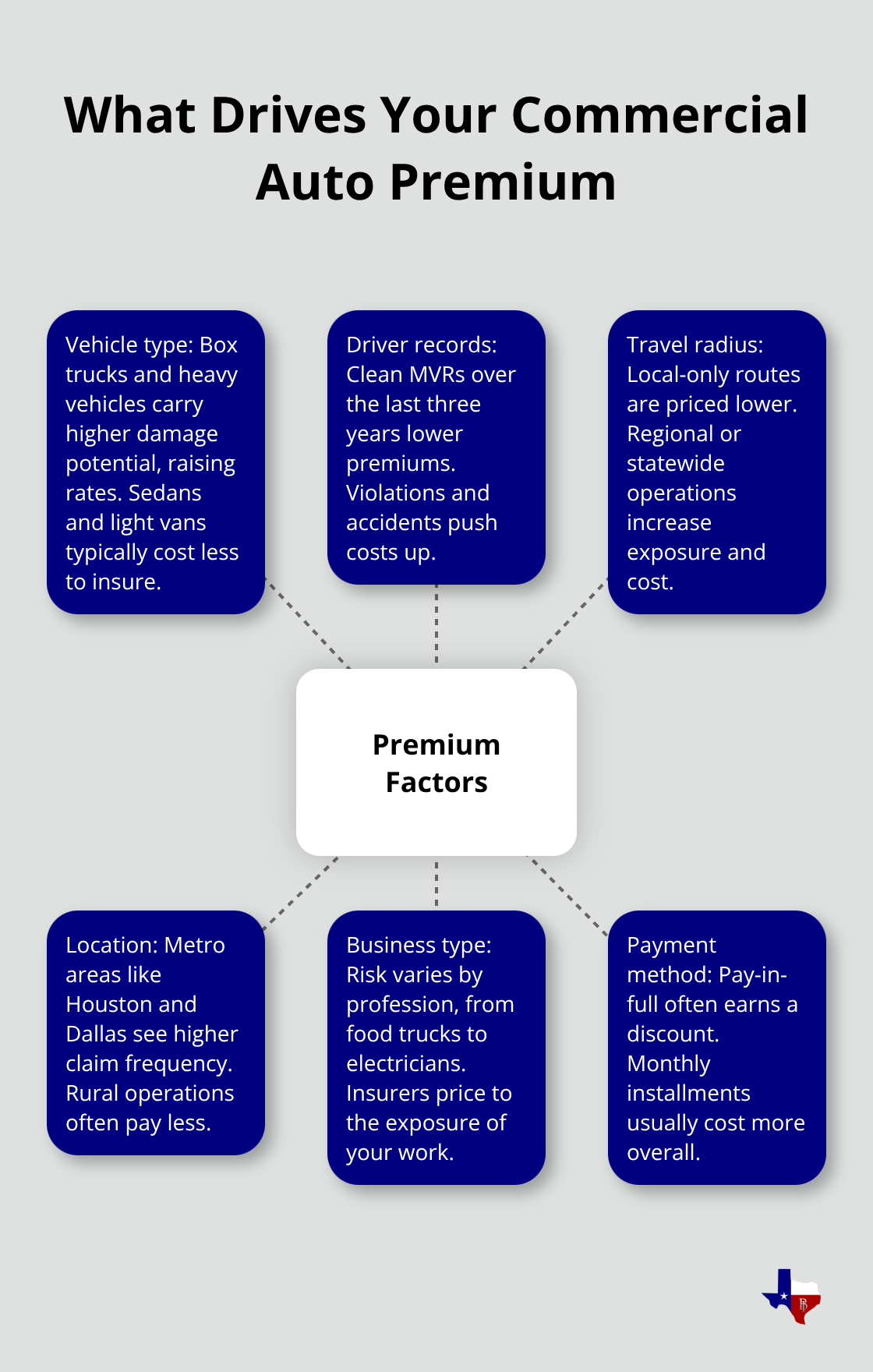

How Costs Vary Based on Your Operation

Your premium depends on several concrete factors. The type of vehicle matters significantly-a box truck costs more to insure than a sedan because of higher damage potential. Your drivers’ records over the last three years directly impact pricing. Travel radius affects cost too; local-only routes are generally cheaper than regional operations covering broader areas.

Location matters as well, with Houston and Dallas typically having higher premiums than rural areas due to increased claim frequency. Your business profession also influences rates. A food truck operation faces different risks than an electrician’s van, so they’re priced accordingly. If you pay your premium in full upfront, you can typically save 13% or more compared to monthly payments.

Coverage Options Beyond the Basics

Standard commercial auto policies cover liability and physical damage, but your business may need additional protections. Motor truck cargo coverage protects goods your vehicles transport. Garagekeepers liability covers customers’ vehicles in your custody. Non-owned vehicle coverage extends protection to employee personal vehicles used for work. Heavy trucks and specialty vehicles (tow trucks, dump trucks, box trucks) may require on-hook coverage to protect customers’ vehicles you’re towing or servicing. These add-ons address specific operational risks that standard policies don’t cover. The right combination of coverages depends entirely on what your business actually does and what assets you need to protect.

What Your Commercial Auto Policy Actually Pays For

Liability Coverage Protects Your Business from Others’ Claims

Liability coverage forms the foundation of commercial auto insurance, and Texas law makes it mandatory. This coverage pays for injuries or death to other people if you’re at fault in an accident, plus damage to their property. The state minimum of 30/60/25 means your insurer covers up to $30,000 per person for bodily injury, $60,000 total per accident for bodily injury, and $25,000 for property damage. These minimums are dangerously low. A single serious injury claim easily exceeds $30,000 in medical bills and lost wages. If you operate a delivery service or employ multiple drivers, you expose your business to massive liability. Most responsible Texas business owners carry limits of at least 100/300/100 or higher, which means $100,000 per person, $300,000 per accident for bodily injury, and $100,000 for property damage. Your liability coverage also includes legal defense costs, which can run $10,000 to $50,000 just to defend a claim, even if you win.

Collision and Comprehensive Coverage Protect Your Vehicles

Collision and comprehensive coverage protect your actual vehicles from damage. Collision pays for repairs or replacement when your vehicle hits another vehicle or object, regardless of who’s at fault. Comprehensive covers theft, vandalism, weather damage like hail or flooding, and fire. In Texas, severe weather causes thousands of comprehensive claims annually according to the Texas Department of Transportation. If you operate in Houston or coastal areas, comprehensive coverage becomes essential rather than optional. Hail storms and hurricanes strike regularly, and a single weather event can total multiple vehicles in your fleet without this protection.

Uninsured and Underinsured Motorist Coverage Fills a Critical Gap

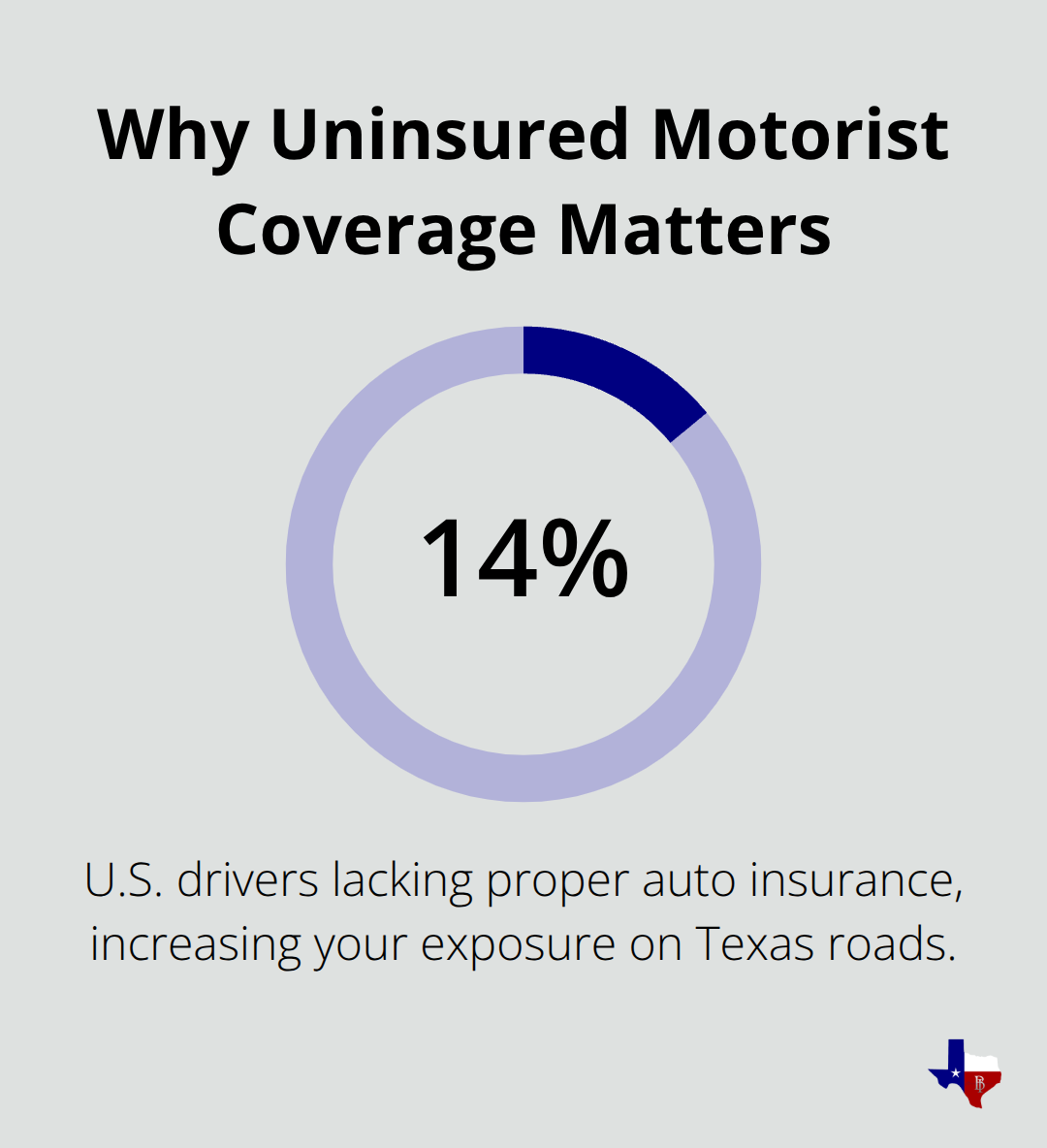

Uninsured and underinsured motorist coverage protects you when the other driver has no insurance or insufficient coverage. About 14% of U.S. drivers lack proper auto insurance, so this coverage addresses a real problem you’ll likely encounter on Texas roads. This protection applies to you and your employees, covering medical expenses and lost wages when an uninsured or underinsured driver causes an accident.

Your business depends on your drivers staying operational, and this coverage helps maintain that continuity.

Medical Payments and Personal Injury Protection Cover Your Team

Medical payments or personal injury protection covers medical expenses for you and your passengers after an accident, regardless of fault. In Texas, PIP is mandatory unless you sign a written waiver. This coverage typically includes lost wages, which matters significantly if your business depends on you or key employees being operational. If a driver is injured and cannot work for three weeks, PIP helps cover that income loss while they recover. The combination of these coverages-liability, physical damage, and protection for your own people-creates a comprehensive safety net that keeps your business operating after an accident.

Specialty Coverages Address Specific Business Risks

Beyond standard coverages, your operation may require additional protections tailored to your specific activities. Motor truck cargo coverage protects goods your vehicles transport. Garagekeepers liability covers customers’ vehicles in your custody. Non-owned vehicle coverage extends protection to employee personal vehicles used for work. Heavy trucks and specialty vehicles (tow trucks, dump trucks, box trucks) may require on-hook coverage to protect customers’ vehicles you’re towing or servicing. These add-ons address operational risks that standard policies don’t cover, and selecting the right combination depends entirely on what your business actually does. Understanding what each coverage type pays for helps you make informed decisions about which protections your operation truly needs.

What Commercial Auto Insurance Doesn’t Cover

Commercial auto insurance protects your business vehicles and operations, but it has clear boundaries. Your policy will not pay for damage or losses outside those boundaries, and misunderstanding these limits can leave you scrambling when a claim gets denied.

Personal Use of Company Vehicles Falls Outside Coverage

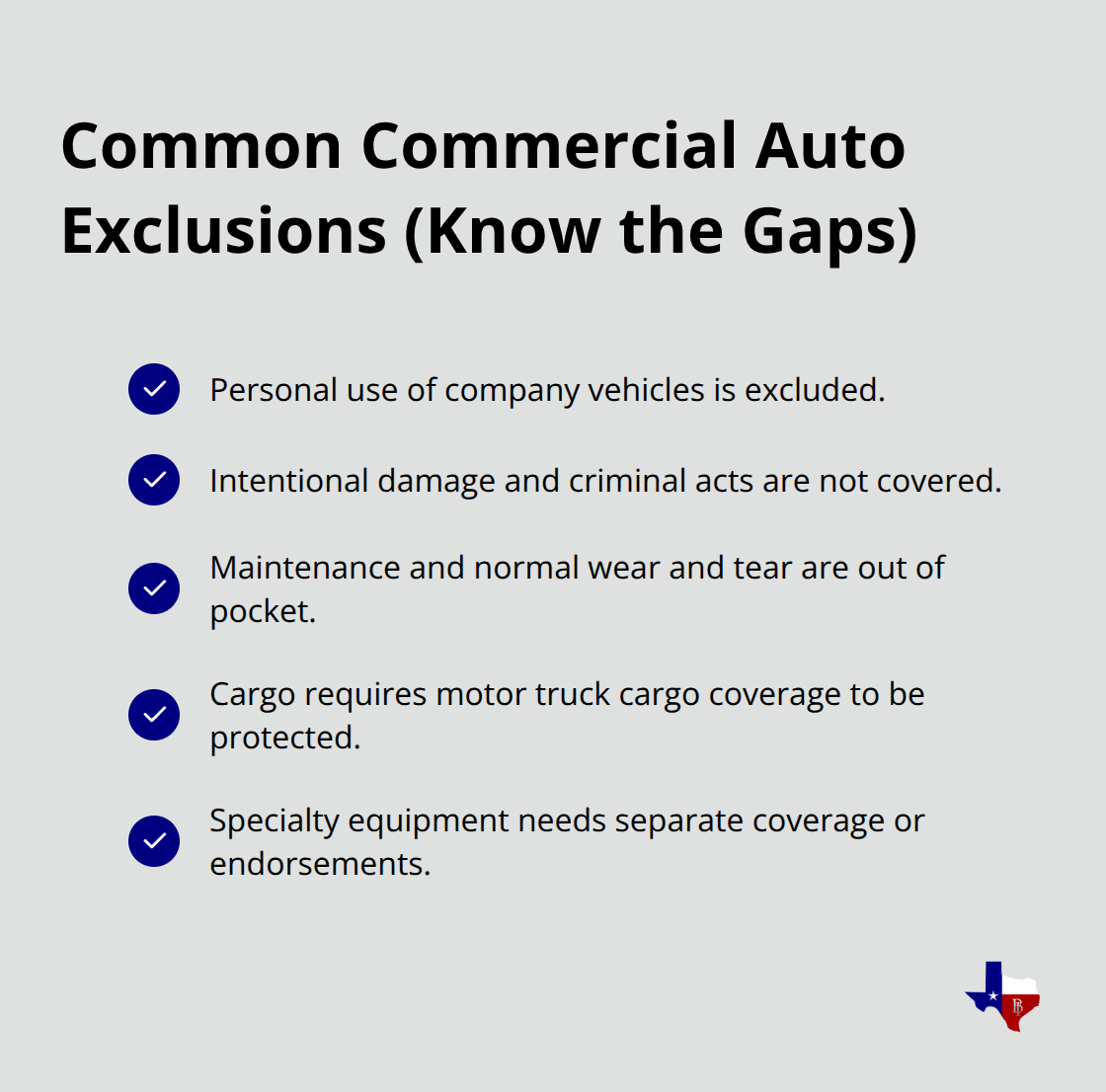

The most common exclusion involves personal use of company vehicles. If an employee takes a company vehicle to run personal errands unrelated to work, any accident during that trip falls outside commercial coverage. Texas courts treat personal use as a separate exposure that requires personal auto insurance, not commercial policies.

This distinction matters because your commercial insurer can deny claims if they determine the vehicle was being used for personal purposes at the time of the accident.

If your employee drives a company truck to pick up lunch for themselves, that constitutes personal use. If they drive to a client site and stop at a restaurant on the way, that constitutes business use. The line is clear in theory but murky in practice, which is why documenting your business use policies in writing protects both your company and your drivers.

Intentional Damage and Criminal Acts Receive No Coverage

Intentional damage and criminal acts never receive coverage under commercial auto insurance. If a driver deliberately crashes a vehicle to commit insurance fraud, the insurer will deny the claim and potentially pursue criminal charges. Vandalism by employees, theft orchestrated by staff, or damage caused by reckless behavior intended to harm the vehicle all fall outside coverage.

Maintenance and Wear and Tear Require Out-of-Pocket Payment

Maintenance costs and normal wear and tear are excluded from your policy. Your commercial policy covers accidents and sudden damage, not routine maintenance like oil changes, tire replacements, or brake pad wear. If a vehicle breaks down due to poor maintenance, you pay for repairs out of pocket. Regular vehicle maintenance helps reduce claim likelihood by ensuring headlights, wipers, brakes, and other parts function properly.

Cargo and Specialty Equipment Need Separate Endorsements

Cargo coverage requires a separate endorsement and does not apply to standard policies. If your business transports goods and those goods are damaged or lost, your basic commercial auto policy provides no protection. Motor truck cargo coverage is a distinct add-on that covers merchandise, equipment, or products your vehicles carry.

Specialty equipment like hydraulic lifts, refrigeration units, or custom toolboxes mounted on vehicles also requires separate coverage. These items are excluded from standard physical damage coverage because they represent additional value beyond the vehicle itself. Understanding what falls outside your policy prevents costly surprises when claims get denied.

Final Thoughts

Commercial auto insurance protects your Texas business from financial devastation when accidents happen. The coverage types we’ve discussed-liability, collision, comprehensive, uninsured motorist protection, and medical payments-form the foundation of what commercial auto insurance covers for your operation. Each coverage type addresses a specific risk your business faces on Texas roads.

Your policy needs change as your business evolves. When you add vehicles, expand your service area, or hire new drivers, your coverage gaps may widen. A policy that protected your operation last year may leave you exposed this year if your business has transformed. Specialty coverages like cargo protection or garagekeepers liability become essential once you start new service lines that your standard policy excludes.

We at Brooks Insurance help Texas business owners evaluate their coverage needs and find the right protection for their specific operation. Our licensed agents understand Texas commercial auto requirements and identify gaps in your current protection. Contact us at brooksinstx.com to discuss your coverage needs and receive a personalized quote that matches your business operation.

Disclaimer: The information provided in this blog is for general informational purposes only and does not constitute legal, financial, or insurance advice. Coverage options, terms, and availability may vary. Please consult with a licensed professional for advice specific to your situation