When you’re shopping for insurance in Texas, you’ll quickly notice that not all agencies work the same way. Some represent just one company, while others work with dozens of carriers to find you the best fit.

At Brooks Insurance, we believe understanding what an independent insurance agency is-and how it differs from other options-helps you make smarter coverage decisions. This guide walks you through the key differences and shows why many Texas consumers prefer working with independent agencies.

What Sets Independent Agencies Apart

An independent insurance agency works with multiple insurance carriers rather than being tied to a single company. This fundamental difference shapes everything about how we operate and serve you. In 2024, independent agencies wrote 61.5% of all property and casualty insurance in the United States according to the Big I Market Share Report, and they handled 87.2% of all commercial lines premiums. That market dominance exists because independent agencies deliver tangible value that consumers recognize and prefer.

Multiple Carriers Deliver Real Pricing Power

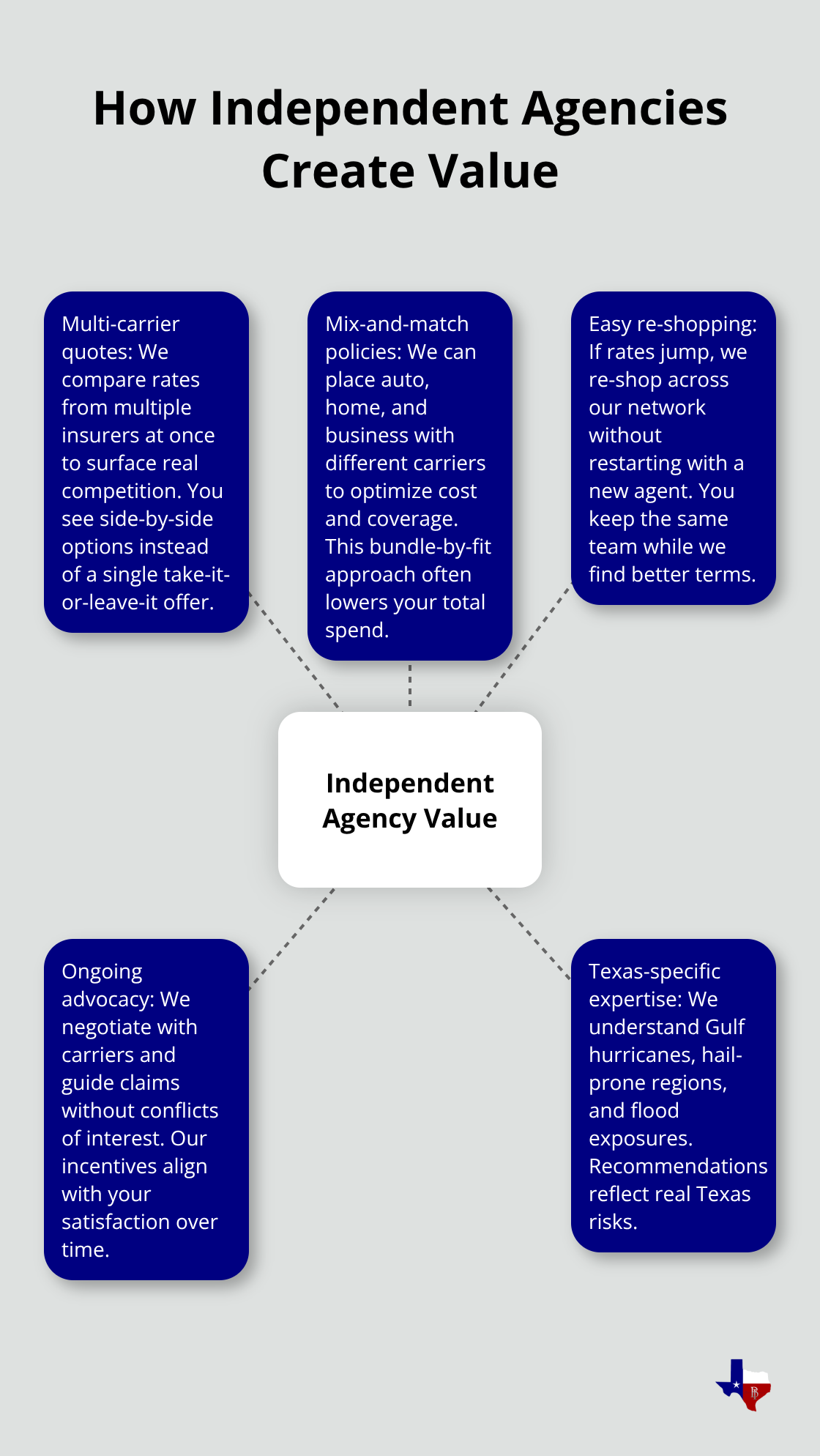

When you work with an independent agency, you gain access to quotes from numerous insurers simultaneously. A captive agent can only show you what one company offers, which means you’re comparing against nothing. We can place your auto policy with one carrier, your homeowners coverage with another, and your business insurance with a third if that combination saves you money and provides better coverage. This isn’t theoretical flexibility-it’s how we actually operate. If your rates spike with your current insurer, we can re-shop your entire policy across our carrier network without you having to start from scratch with a new agent.

You maintain your relationship with us while we find you better terms elsewhere. That’s impossible with a captive agent who works for one company.

Service Built Around Your Situation, Not Sales Quotas

Captive agents face pressure to meet sales targets for their employer’s products, which can influence what coverage they recommend. We earn commissions on the policies we place, but those commissions don’t push us toward more expensive options because we work with so many carriers. If a basic liability policy fits your needs better than comprehensive coverage, recommending that basic policy won’t cost us your business-you’ll still work with us for renewals and other insurance needs. This alignment matters in practice. We assess your actual risk profile, your budget constraints, and your coverage gaps. Then we match you with policies and carriers that fit those realities. Our local expertise in Texas means we understand regional risks like hurricane exposure on the Gulf Coast or hail damage in Central Texas, and we tailor recommendations accordingly.

Why Carrier Diversity Changes Everything

The ability to access multiple carriers (rather than one) transforms how we handle your coverage over time. When market conditions shift or your circumstances change, we don’t have to convince you to accept whatever your current insurer offers. We shop your policy across our network and present you with real alternatives. This flexibility protects you from rate increases that other consumers simply accept because they lack options. Independent agencies continue to grow their market share, reflecting growing consumer preference for this model. That growth tells you something important: Texas consumers increasingly recognize that working with an agency that represents multiple carriers produces better outcomes than working with a single-company agent.

How Captive Agencies Limit Your Options

One Company, One Set of Choices

A captive agent works exclusively for one insurance company and can only sell policies from that single carrier. When you sit down with a captive agent, you evaluate one company’s offerings against nothing. If State Farm’s auto rates don’t work for your situation, a captive agent cannot shop your policy to Allstate, USAA, or any other carrier. You either accept State Farm’s terms or walk away and start over with a different agent elsewhere.

This limitation directly impacts your wallet. An independent agency can place your auto insurance with one carrier, your homeowners policy with another, and your business coverage with a third if that combination delivers better rates and coverage. Independent agencies shop across dozens of carriers simultaneously, which means you see real competitive pricing instead of a single company’s take-it-or-leave-it offer.

The Growth Trend Toward Broader Options

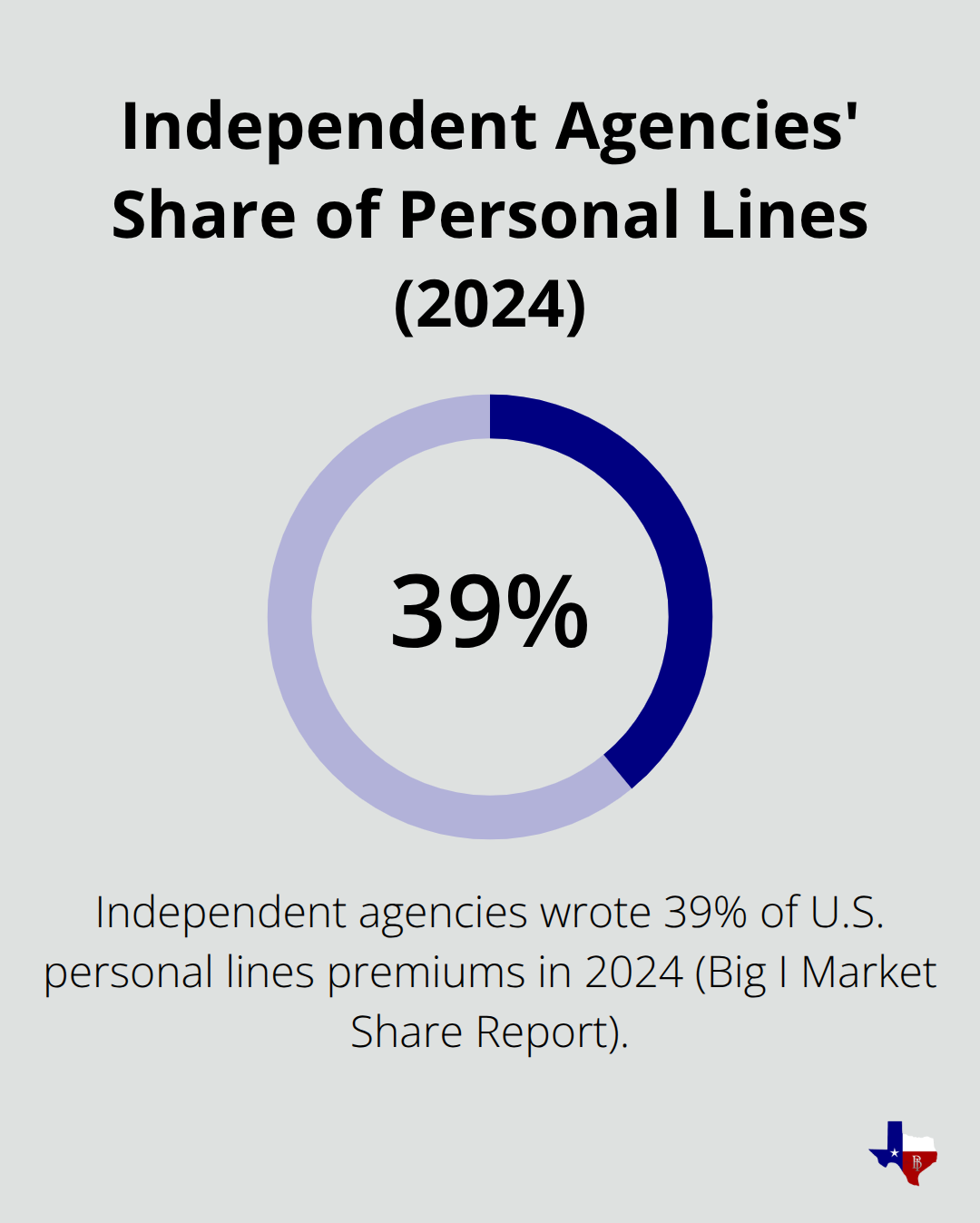

In 2024, independent agencies wrote 39 percent of all personal lines premiums, up from 35.7 percent in 2020 according to the Big I Market Share Report. That growth reflects consumers actively choosing broader options over limited ones. Texas consumers increasingly recognize that working with an agency representing multiple carriers produces better outcomes than working with a single-company agent.

Commission Incentives That Work Against You

The commission structure at captive agencies creates financial incentives that don’t align with your interests. Captive agents typically earn higher commissions when they sell more expensive policies because their employer benefits from larger premiums. This means a captive agent has a financial reason to recommend comprehensive coverage you might not need or permanent life insurance when term coverage fits your budget better.

Independent agencies operate differently. Because they represent multiple carriers with different pricing structures, recommending the wrong coverage type doesn’t protect income-it just loses business. The incentive becomes keeping you satisfied across renewals and additional insurance needs, not maximizing the premium on your first sale.

Limited Flexibility When Rates Rise

When market conditions shift or your rates spike, captive agents have limited flexibility to help you. They cannot re-shop your policy across competitors because they represent only one company. You either accept a rate increase or switch agencies entirely and rebuild your relationship with someone new.

Independent agencies can re-shop your entire policy across their carrier network without you changing agents. You maintain continuity while the agency finds you better terms. That practical difference matters most when rates are climbing-and in today’s insurance market, they often are.

This flexibility positions independent agencies as the better choice when you need coverage adjustments or rate relief, which leads directly to how independent agencies actually serve your needs through personalized solutions.

Why Independent Agencies Deliver Better Real-World Outcomes

Working with an independent agency means you stop accepting whatever one insurer decides to offer you. An independent agency places your auto policy with the carrier that actually competes for your business, your homeowners coverage with an insurer that understands Texas coastal risks, and your business insurance with a carrier specializing in your industry. This isn’t theory-it’s how independent agencies operate daily.

When your neighbor pays $200 more annually for identical auto coverage because they’re locked into a captive agent’s single carrier, that difference compounds over decades. Independent agencies wrote 39 percent of all personal lines premiums in 2024, up from 35.7 percent in 2020 because Texas consumers increasingly recognize that access to multiple carriers produces tangible savings and better coverage fits than single-carrier options.

Coverage That Actually Matches Your Needs

An independent agency assesses your situation independently rather than filtering recommendations through one company’s product lineup. If you own a contractor business and need commercial general liability coverage, the agency evaluates risk profiles across carriers that specialize in contractor exposures instead of forcing you into whatever one company offers. A captive agent selling for a major national carrier might not even have appetite for your specific contractor type. Independent agencies identify carriers with underwriting expertise in your industry, which means better rates and fewer coverage gaps. For homeowners in high-risk flood zones, an independent agency can place your dwelling fire coverage with one carrier while securing private flood insurance through another carrier that actually competes for coastal Texas business. This carrier diversity directly impacts your out-of-pocket costs and your protection level.

Advocacy That Continues After You Buy

When you file a claim, a captive agent’s loyalty flows to their employer first. An independent agency’s success depends entirely on your satisfaction because you can leave for another independent agency if you experience disappointment. This alignment matters when you’re stressed about property damage or facing coverage questions. The independent agency guides you through claims processes across different carriers without conflicts of interest. The agency negotiates with insurers on your behalf because its reputation depends on your outcome, not on protecting an insurance company’s claims department from payouts. Texas consumers increasingly choose independent agencies precisely for this reason-the agent’s incentives align with yours, not with an insurance company’s profit margins.

Real Flexibility When Market Conditions Shift

Rate increases hit every insurance consumer eventually, but your options differ dramatically based on your agency type. A captive agent cannot re-shop your policy across competitors because they represent only one company. You either accept a rate increase or switch agencies entirely and rebuild your relationship with someone new. An independent agency re-shops your entire policy across its carrier network without you changing agents. You maintain continuity while the agency finds you better terms. That practical difference matters most when rates are climbing-and in today’s insurance market, they often are. This flexibility positions independent agencies as the better choice when you need coverage adjustments or rate relief.

Why Carrier Diversity Protects Your Wallet

The ability to access multiple carriers (rather than one) transforms how an independent agency handles your coverage over time. When market conditions shift or your circumstances change, the agency doesn’t have to convince you to accept whatever your current insurer offers. The agency shops your policy across its network and presents you with real alternatives. This protection shields you from rate increases that other consumers simply accept because they lack options. Independent agencies continue to grow their market share, reflecting growing consumer preference for this model. That growth tells you something important: Texas consumers increasingly recognize that working with an agency representing multiple carriers produces better outcomes than working with a single-company agent.

Final Thoughts

Independent agencies serve Texas consumers better because they align your interests with theirs. When you work with an independent insurance agency, you avoid being locked into one company’s offerings or subject to a captive agent’s sales quotas. You gain access to competitive pricing across multiple carriers, objective recommendations tailored to your actual situation, and an agent who benefits when you stay satisfied long-term.

Evaluating an independent agency means asking practical questions about what is an independent insurance agency and how it operates for your benefit. Does the agency represent carriers that compete for your type of coverage? Can they explain why they recommend specific policies from specific insurers? Do they offer local expertise relevant to Texas risks like coastal exposure or hail damage? Will they re-shop your policy if rates spike, or do they expect you to accept whatever your current insurer charges?

At Brooks Insurance, we represent multiple top-rated insurance companies to serve Texas consumers with personal and commercial coverage solutions. Visit Brooks Insurance to get started with a quote or to speak with one of our agents about your coverage needs.

Disclaimer: The information provided in this blog is for general informational purposes only and does not constitute legal, financial, or insurance advice. Coverage options, terms, and availability may vary. Please consult with a licensed professional for advice specific to your situation