Running an independent insurance agency without a solid structure is like trying to manage client policies in a filing cabinet-chaos eventually wins.

At Brooks Insurance, we’ve seen firsthand how the right independent insurance agency organizational structure transforms operations. Clear roles, efficient systems, and strong team management separate thriving agencies from those constantly putting out fires.

This guide walks you through building an agency framework that scales with your growth.

Building Your Agency’s Operating Structure

Most independent agencies fail not because of market conditions but because their internal structure cannot handle growth. The difference between a $500,000 agency and a $2 million agency often comes down to one thing: how you organize people and processes. Your structure determines whether you spend time on client relationships or constantly fight operational problems.

Start by mapping every function that happens in your agency, then assign clear role ownership. Who handles new client onboarding? Who manages claims follow-up? Who owns renewal tracking? Agencies with defined role ownership see measurable improvements in operational efficiency. This isn’t about creating rigid hierarchies; it’s about eliminating confusion. When someone new joins your team, they know exactly what they own and what success looks like in that role.

Document these responsibilities in writing. A simple one-page role description prevents misunderstandings and protects you when turnover happens. Most agencies avoid this step because it feels bureaucratic, but it actually frees your team to work autonomously instead of constantly asking what comes next.

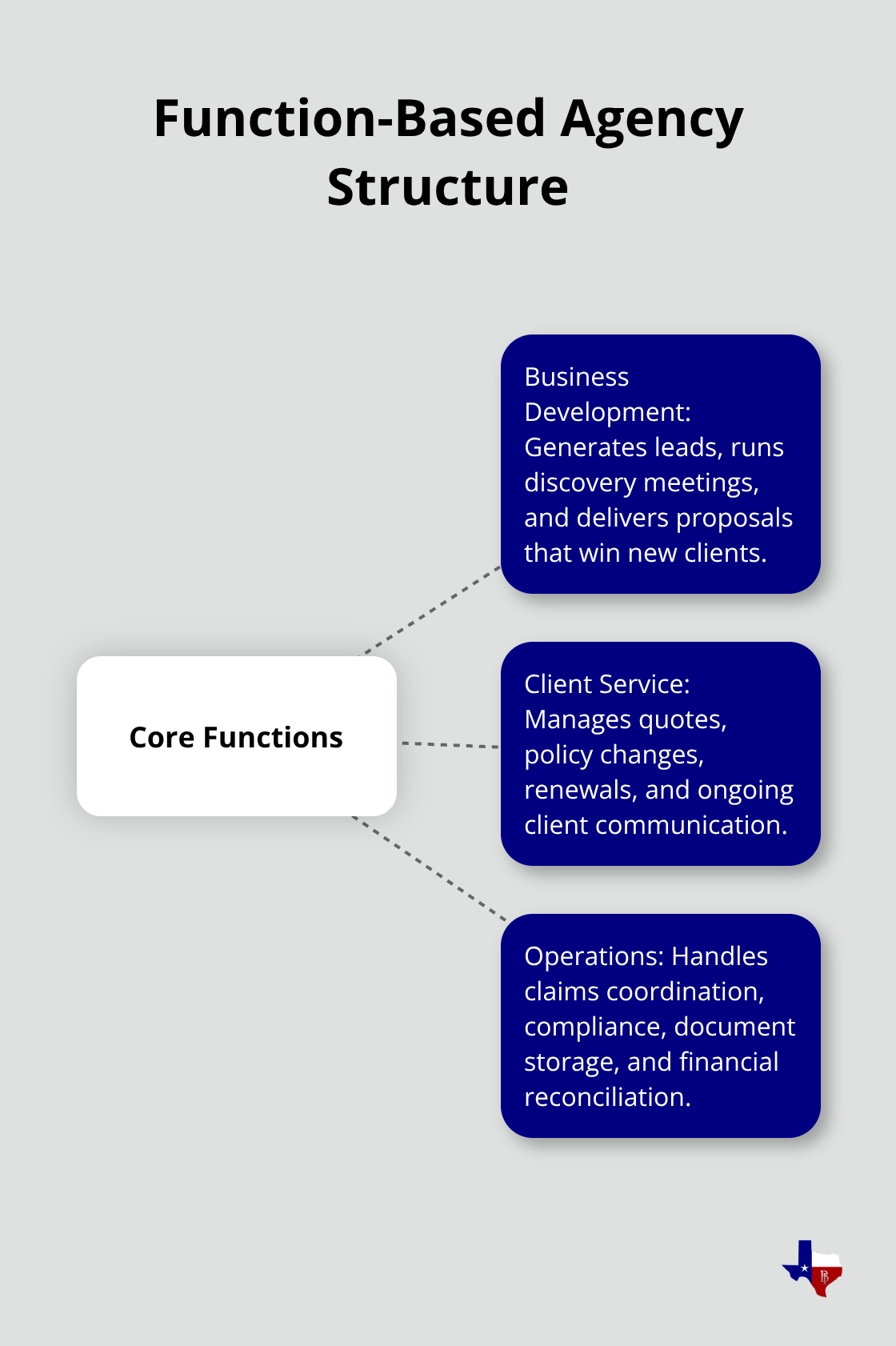

Organize by Function, Not by Insurance Lines

Don’t organize by insurance lines. That’s the mistake most agencies make.

Instead, organize by function: business development, client service, and operations. Your business development function owns lead generation, new client meetings, and proposals. Your client service function handles quotes, policy changes, renewals, and client communication. Your operations function manages claims coordination, compliance, document storage, and financial reconciliation.

This structure works whether you have three people or thirty. One person might wear multiple hats in a startup, but the functions stay separate. As you hire, you add specialists to each function rather than creating new departments. This approach scales smoothly because you don’t reorganize; you add capacity to existing functions.

When you hire your first producer, they focus on business development. When you hire your first dedicated service person, they join the client service function. The financial implications matter too-agencies structured this way typically spend 25-30% of revenue on salaries and commissions according to IIABA benchmarks, while poorly structured agencies drift toward 40-45% because of inefficiency and duplicate roles.

Build Systems That Support Your Structure

Your structure only matters if you build systems that support it. An AMS like EZLynx or Eclipse that handles comparative ratings, policy management, and workflow automation becomes the backbone of your organization. These tools cost under $1,000 to set up and $60-$600 monthly depending on your size, but they’re non-negotiable if you want your team to operate independently. Without them, every task requires supervision and every person becomes a bottleneck.

Your operations function should own the AMS and make sure data flows correctly. Set standards for how policies get entered, how renewals get flagged, and how client communications get logged. Most agencies lose money on renewals not because of competition but because they didn’t set up a system to track renewal dates and automatically generate renewal paperwork.

Document Your Procedures

Document your procedures in a Policy and Procedures Manual. This isn’t busywork-it’s what lets you hire people who can actually operate independently. When you need to onboard a new team member, they follow your manual instead of pestering experienced staff with endless questions. The Moberg Group works with IIAG to align procedures with industry best practices, and that framework costs nothing extra if you’re already an IIAG member.

Your structure succeeds or fails based on whether your team can execute consistently without constant direction from you. Once you establish these operational foundations, you’re ready to focus on the people who will drive your agency forward-which means investing in the right training and development practices that turn your structure into actual results.

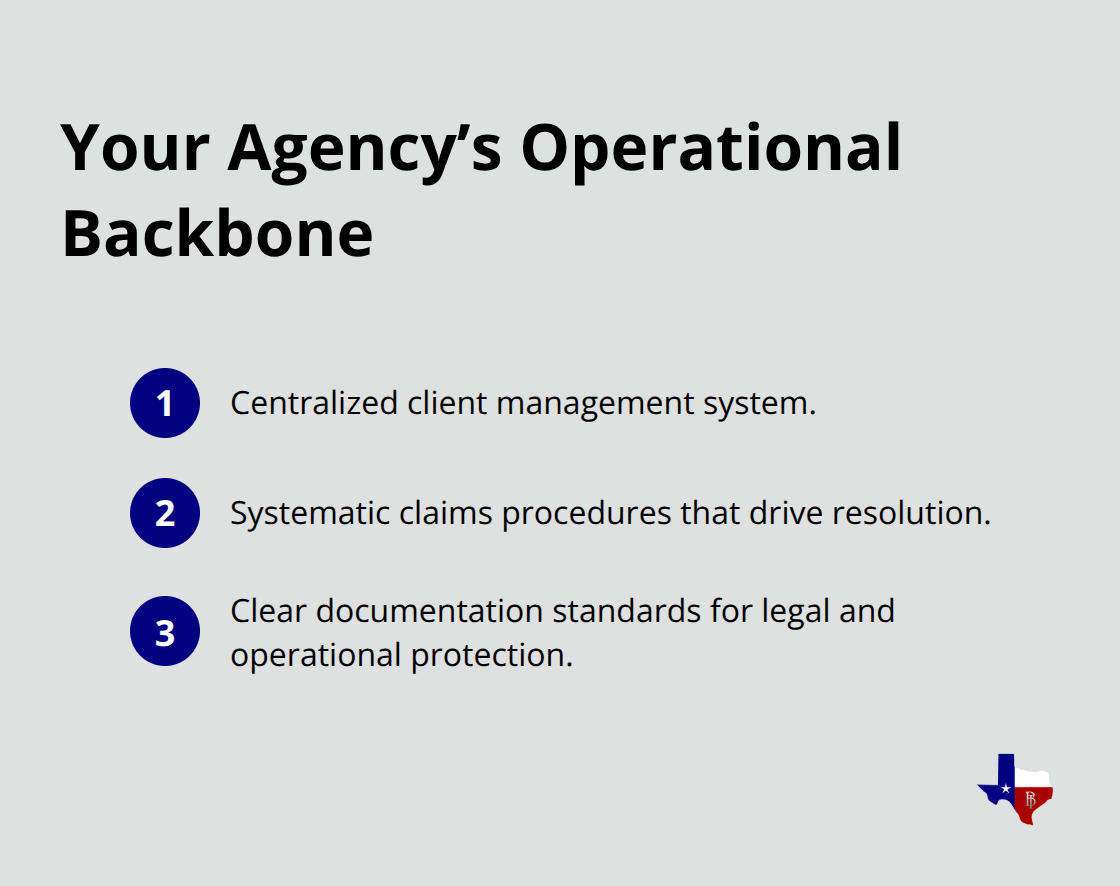

Key Operational Systems and Processes

Your structure means nothing without the right operational backbone. Most independent agencies waste money and client relationships because their systems don’t talk to each other. You need three things working together: a client management system that centralizes everything, claims procedures that actually get resolved instead of forgotten, and documentation standards that protect you legally and operationally.

Choose and Implement an Agency Management System

Start with your Agency Management System. EZLynx and Eclipse both handle comparative ratings, policy management, and workflow automation, costing under $1,000 to implement with monthly fees between $60 and $600 depending on your agency size. The critical decision isn’t which AMS you choose but whether it integrates with carrier live feeds and handles renewals automatically. If your AMS requires manual data entry for every renewal, you’ve bought an expensive filing cabinet.

Your operations team should own this system entirely and establish data entry standards that every team member follows. Set rules for how policies get classified, when renewal notices get generated, and which fields are mandatory before a policy closes in the system. Agencies that enforce these standards see renewal retention rates above 90 percent, while agencies with loose data practices drop to 75-80 percent because they miss renewal dates or send notices to wrong addresses.

Establish a Claims Coordination Process

Claims handling destroys client relationships when it’s reactive instead of systematic. Assign one person to own claims coordination as their primary responsibility. This person tracks every claim from first notification through settlement, sets calendar reminders for follow-ups, and communicates status to clients before they call asking for updates.

Create a simple claims log that captures the claim date, carrier, status, and expected resolution date. When a client calls about a claim, your team should know the answer within seconds instead of scrambling to find information. This single practice transforms how clients perceive your agency during their most stressful moments.

Build Documentation Standards for Compliance and Efficiency

Documentation standards matter equally for compliance and efficiency. Your Policy and Procedures Manual should specify how long you retain client files, what communications get documented, what disclosures you give at policy binding, and how you record and resolve complaints. Regulatory audits focus on documentation gaps, and agencies without clear standards face fines and license suspensions.

Your compliance function should audit files quarterly to verify you follow your own procedures. This catches problems before regulators do and demonstrates you take client protection seriously. When your team documents everything consistently, you build a record that protects both your clients and your agency during disputes or regulatory reviews. These operational foundations create the stability your team needs to focus on what matters most-building client relationships and growing your book of business.

How to Build a High-Performing Insurance Agency Team

Your structure and systems only work if your team executes them consistently. We know that hiring talented people and then leaving them to figure things out is expensive and slow. Your team needs three things to perform: specific skills training tied to their role, a culture where client outcomes drive decisions, and measurable accountability that shows them exactly how they’re contributing to agency success. Most independent agencies skip formal training because they’re bootstrapped and busy, but that decision costs them 15-20 percent in lost productivity and higher turnover. Agencies that invest in structured training see retention rates above 85 percent and faster ramp time for new hires, meaning new staff contribute to revenue within 60-90 days instead of six months.

Train Your Team on Actual Workflows

Start with role-specific training that goes beyond insurance basics. Your business development team needs training on discovery questions that uncover client needs, proposal writing that explains coverage in plain language, and objection handling specific to your target market. Your client service team needs deep knowledge of your AMS, policy change procedures, and how to communicate with carriers efficiently. Your operations team needs training on compliance requirements, document management, and claims coordination. Don’t use generic insurance education for this-that teaches compliance but not your actual workflow. Instead, have your most experienced team member document how they do their job, then use that documentation as your training material. When you hire someone new, they follow that documented process for their first 30 days while your experienced person reviews their work. This approach costs nothing but your time and produces consistent execution. After 30 days, measure their accuracy on key tasks like policy entries or renewal processing. If accuracy hits 95 percent, they’re ready for independence. If not, extend the training period.

This single practice eliminates the vague feedback that most agencies give and replaces it with objective performance data.

Create a Client-Focused Culture

Your culture determines whether your team treats clients as transactions or relationships. Agencies with strong client-focused cultures have one thing in common: leadership makes client outcomes visible to the entire team. Share client feedback in team meetings, not just the positive reviews but also complaints and service failures. When your team hears directly from a client about a bad experience, they understand why their role matters. Set a simple rule: no policy binds until the client confirms they understand their coverage. That means your client service team has permission to push back on producers who want to rush the binding process. When your operations team catches a compliance gap, they have authority to stop a renewal and fix it before it goes to the carrier. This isn’t bureaucracy-it’s empowerment. Agencies with this culture experience fewer errors, higher client retention, and lower staff turnover because people feel ownership of outcomes instead of just completing tasks.

Establish Measurable Performance Targets

Accountability requires specific, measurable targets tied to each role. Your business development team should have monthly targets for new client meetings, quotes generated, and policies written. Your client service team should have accuracy targets for policy entries, renewal notice generation, and client response time. Your operations team should track claims resolution time and compliance audit results. Post these metrics where your team sees them weekly, not as punishment but as progress tracking. When someone hits their target, acknowledge it publicly. When someone misses, discuss what got in the way and adjust support or resources. This practice takes 15 minutes per week in a team meeting and transforms how people think about their work. Agencies that use this approach see productivity increases of 20-30 percent because people focus on the right activities instead of staying busy with low-value work. The key is making targets achievable but ambitious-set them at 80-90 percent of what your best performer does, not at what your average performer does. This creates a culture of growth instead of comfort.

Final Thoughts

The independent insurance agency organizational structure you build today determines whether your agency survives the next five years or thrives through them. Structure creates clarity instead of bureaucracy. When your team knows their role, understands the systems they work within, and sees how their performance contributes to client outcomes, everything shifts. You stop managing people and start leading them. Clear roles and function-based organization create accountability, your AMS and documented procedures eliminate guesswork, and training plus measurable targets turn your structure into actual performance.

Proper organization delivers three long-term benefits that compound over time. Your team operates independently instead of constantly asking for direction, which frees you to focus on strategy and growth. Your client retention improves because your systems catch renewal dates, handle claims professionally, and maintain consistent communication. Your profitability increases because you eliminate waste and duplicate effort-agencies with strong organizational structures typically spend 25-30 percent of revenue on salaries and operations while poorly organized agencies drift toward 40-45 percent doing the same work less efficiently.

Start implementing immediately by mapping your current functions and assigning clear ownership. Choose your AMS this month and commit to data entry standards. Document your top performer’s workflow and use it as your training template. Set measurable targets for each role and review them weekly. These steps require no capital investment, only discipline and consistency. Brooks Insurance brings over 50 years of experience helping agencies build effective organizational structures that actually work.

Disclaimer: The information provided in this blog is for general informational purposes only and does not constitute legal, financial, or insurance advice. Coverage options, terms, and availability may vary. Please consult with a licensed professional for advice specific to your situation