Picking the right insurance agency can feel overwhelming when you’re faced with dozens of options across Texas. At Brooks Insurance, we’ve seen firsthand how the wrong choice can leave you underinsured or overpaying for coverage you don’t need.

Independent agencies operate differently than captive insurers-they work with multiple companies to find policies that actually fit your situation. This guide walks you through the key factors that separate a good agency from a great one.

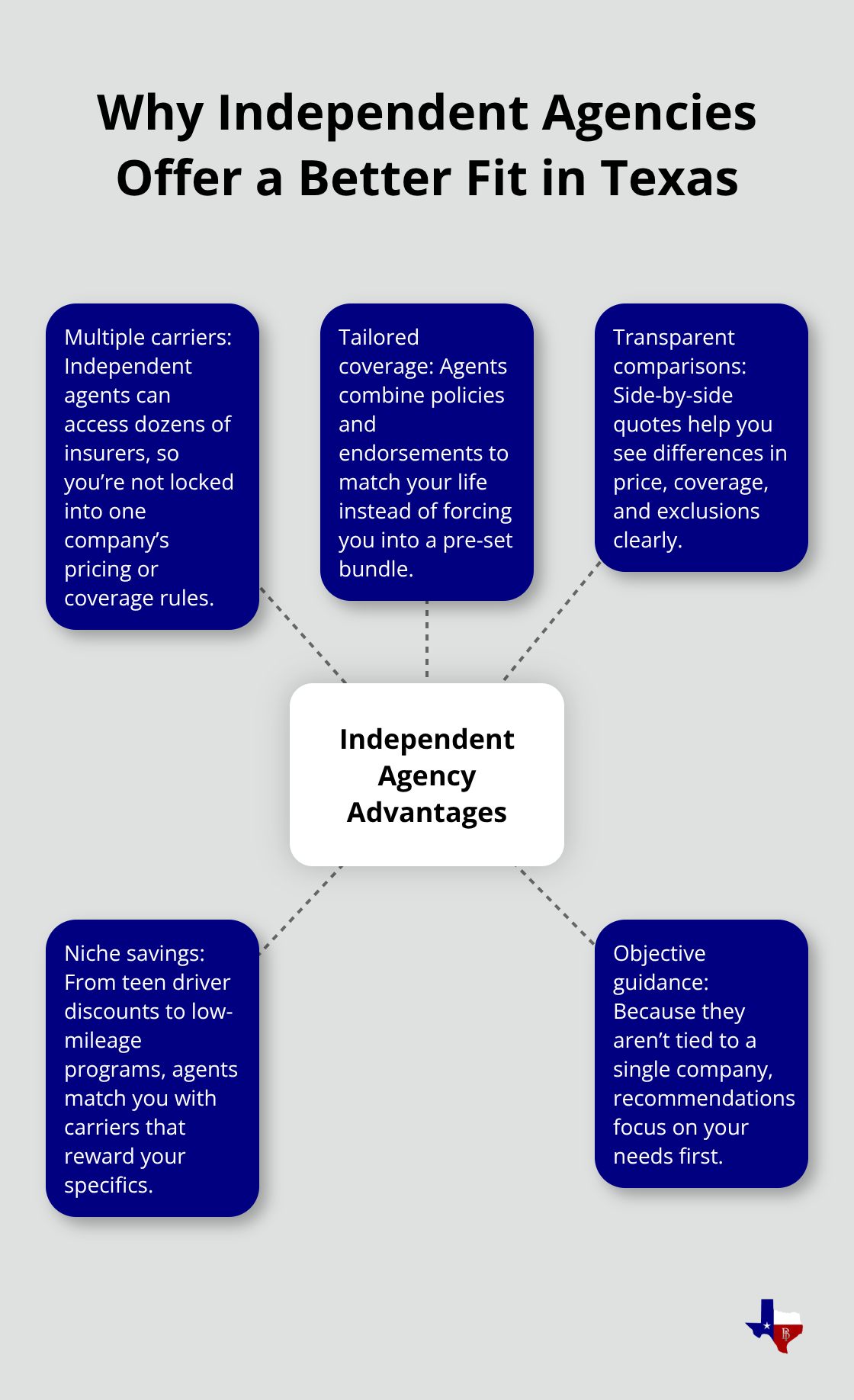

How Independent Agencies Give You More Options

Multiple Carriers Mean Real Choices

Independent agencies work with dozens of insurance carriers instead of just one, which means you avoid being locked into a single company’s pricing or coverage structure. When you work with an independent agent in Texas, you access carriers that may offer better rates for your specific situation. If you have a teenage driver, one carrier might offer substantial discounts for good grades while another focuses on low-mileage discounts. A captive agent tied to a single company cannot show you that comparison.

The real advantage appears in your coverage options. An independent agent pieces together a program that matches your life rather than forcing you into a pre-packaged bundle. If you own a rental property alongside your primary home, an independent agency quotes property coverage, landlord liability, and loss of rent protection from different carriers to find the best combination of price and protection.

Coverage Tailored to Your Situation

You might discover that one carrier excels at protecting against water damage while another offers stronger coverage for theft. An independent agent compares these specifics across carriers, whereas a captive agent presents only what their single employer offers. This flexibility matters most when your situation doesn’t fit the standard mold.

Whether you need auto, home, condo, renters, rental property, life, motorcycle, boat, umbrella, or business coverage, an independent agency searches across multiple carriers to find the right fit. When you evaluate an independent agency, ask how many carriers they represent and request quotes from at least three different companies for any major policy.

Transparency Reveals True Market Shopping

This transparency reveals whether an agency genuinely shops the market or simply gives you their preferred carrier’s quote with a different company name attached. An agency that represents multiple top-rated insurance companies can show you these differences side by side rather than pushing you toward whatever their assigned company offers.

The next step in your selection process involves understanding how an agency evaluates your specific needs and which carriers they prioritize for different situations.

What to Look For in a Licensed and Reputable Agency

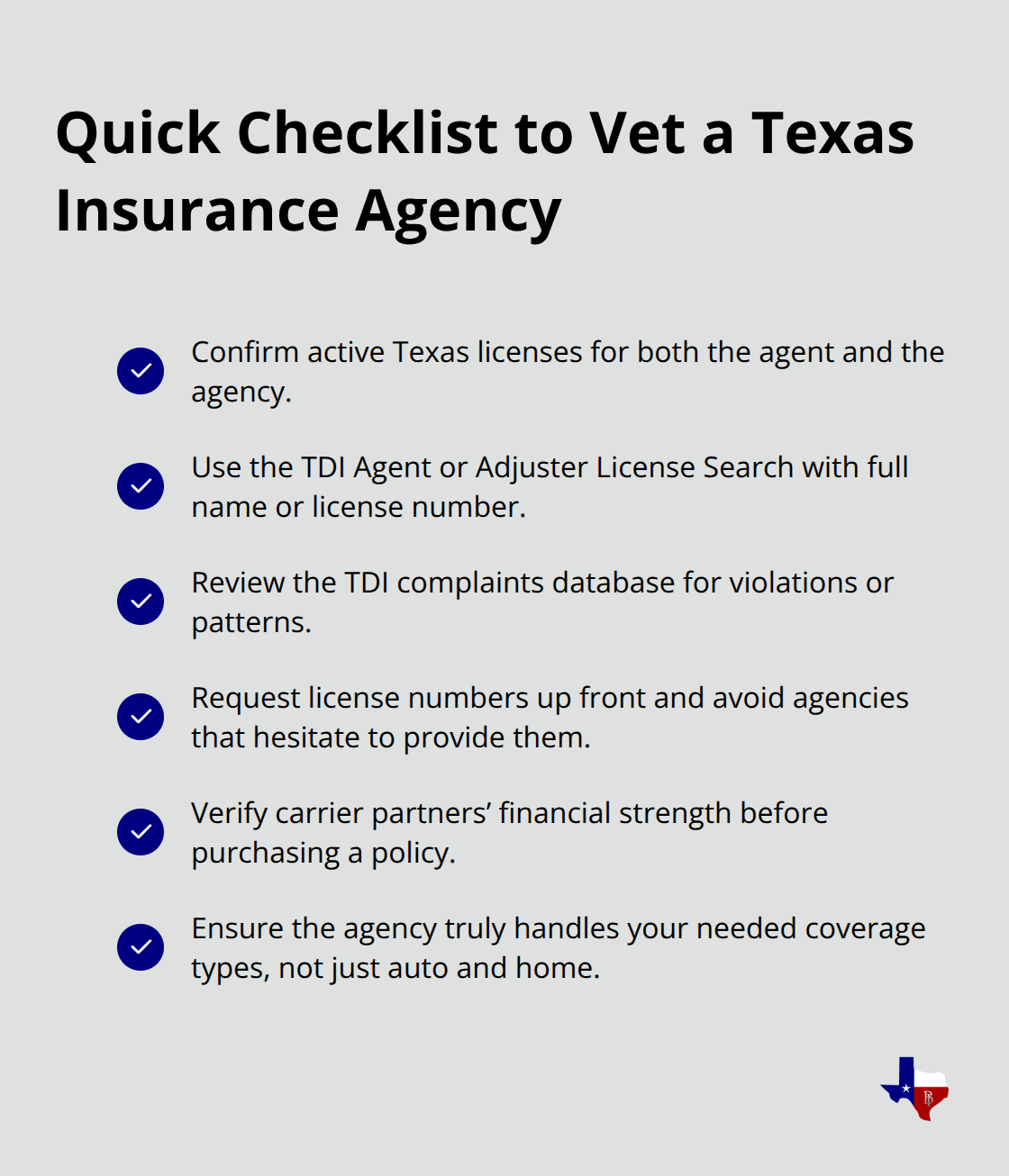

Verify Licensing Through Official State Records

Start your agency search by confirming that both the agent and agency hold current licenses in Texas. Visit the Texas Department of Insurance website and use their Agent or Adjuster License Search tool-you’ll need the agent’s full name or license number for the most accurate results. This five-minute step protects you from unlicensed operators who sometimes misrepresent themselves online. The TDI also maintains a searchable complaints database, so check whether the agency has filed market conduct violations or customer complaints.

If an agency hesitates to provide their license number or avoids answering questions about their licensing status, that’s a red flag worth taking seriously.

Confirm the Agency Handles Your Specific Coverage Types

Examine what products the agency actually handles beyond their marketing claims. Some independent agencies claim to represent dozens of carriers but only actively quote auto and home policies. If you need commercial coverage, workers’ compensation, or specialty lines like umbrella or boat insurance, confirm the agency has real relationships with carriers that offer those products. Call the agency directly and ask which carriers they work with for your specific coverage type-not a generic list, but the actual companies they’d quote for your situation. A strong independent agency should represent at least ten carriers across major product lines, giving you genuine options rather than a narrow selection.

Test Their Customer Service Before You Commit

Customer service responsiveness separates agencies that truly serve clients from those that simply process paperwork. When you call with a question about your policy, does someone answer within business hours, or do you get a voicemail that goes unreturned for days? Claims happen at inconvenient times, and you need an agency that treats your call as urgent. Send an email with a simple question and observe how long it takes to get a response. Agencies that prioritize quick responses typically handle claims better too, which matters far more than a slightly lower premium.

Check the Financial Strength of Their Carrier Partners

Verify the financial stability of the carriers the agency represents before you purchase a policy. The National Association of Insurance Commissioners provides ratings and complaint data for insurers, and you should check that any company quoting your policy has strong financial ratings. A cheap quote from an unstable insurer isn’t a bargain if they can’t pay your claim when you need them. This final verification step ensures that the coverage you purchase actually protects you when disaster strikes.

With licensing confirmed, products verified, service tested, and carrier stability checked, you’re ready to compare multiple agencies side by side to find the one that offers the best combination of options and support for your situation.

Comparing Agencies Side by Side

Request Standardized Quotes to Enable Real Comparison

Contact three independent agencies in your area and request identical coverage for the same property or vehicle from each one. This standardized approach prevents agencies from quoting different limits or deductibles that make comparison impossible. Ask each agency to provide written quotes that clearly show what’s included, what’s excluded, and the exact premium for each coverage type. After you receive these quotes, resist the urge to pick the cheapest option immediately. Comparing quotes based on price alone can lead to inadequate coverage, while examining coverage details alongside cost helps you save money without sacrificing protection.

Verify Coverage Details Match Across All Quotes

When comparing quotes, verify that each agency quoted the same deductibles, liability limits, and optional coverages. A quote that’s $200 cheaper annually might exclude water damage coverage or offer lower liability protection, which means it’s not actually comparable. Check whether each agency explained why they recommended specific carriers for your situation. A quality independent agency should explain that they chose Carrier A for your home because of superior water damage coverage in your area, while Carrier B makes more sense for your auto policy due to their excellent rates for bundled policies.

If an agency simply hands you a quote without explanation, that signals they’re not doing the comparative work that independent agencies should do.

Assess Service Quality Through Reviews and Complaint Records

Online reviews and complaint records tell you whether an agency’s service promises match their actual performance. Look for reviews on Google, the Better Business Bureau, and Trustpilot that specifically mention claims handling, response times, and how agents handled problems. Pay attention to patterns rather than individual reviews. If five reviews mention that an agency took two weeks to respond to emails while others praise quick responses, that’s a significant service difference. Check the Texas Department of Insurance complaint database to verify that the agencies you’re considering have no unresolved complaints or market conduct violations. This step takes ten minutes and eliminates agencies with serious compliance issues.

Evaluate Responsiveness and Long-Term Support

When you call an agency to verify their licensing status, use that conversation to assess their responsiveness and knowledge. Do they answer your questions directly, or do they seem evasive? Do they volunteer information about the carriers they work with, or do you have to extract every detail? An agency that eagerly discusses their carrier relationships and licensing credentials typically provides better service throughout your policy lifecycle. Finally, ask each agency what additional services they offer beyond policy issuance. Some agencies provide annual policy reviews to ensure your coverage keeps pace with your changing situation, while others only contact you at renewal. This difference matters when you experience life changes like purchasing a rental property, getting married, or starting a business. An agency committed to ongoing support costs you nothing extra since carriers pay them, but that service prevents costly coverage gaps down the road.

Final Thoughts

Choosing an independent insurance agency comes down to three core principles: verification, comparison, and service quality. Licensing confirmation through the Texas Department of Insurance protects you from unlicensed operators, comparing quotes across multiple carriers reveals genuine savings opportunities, and responsive customer service matters far more than a slightly lower premium. These evaluation criteria work together to separate agencies that truly serve your interests from those that simply process paperwork.

Independent agencies deliver better value for Texas consumers because they operate without the constraints that captive agents face. You avoid being locked into one company’s pricing structure or forced into coverage bundles that don’t match your situation. When you work with an independent agency, you access dozens of carriers, which means an agency can find better rates for your teenage driver, stronger water damage protection for your home, or specialized coverage for your rental property-all at no extra cost since carriers pay the agency commission regardless of which company you choose.

Contact three independent agencies in your area and request identical quotes for your specific coverage needs. Verify their licensing through official state records, check their complaint history, and assess their responsiveness by observing how quickly they answer your questions. When you’re ready to explore your options with an agency that prioritizes your interests, reach out to Brooks Insurance to discuss your insurance needs and receive personalized quotes from carriers that match your situation.

Disclaimer: The information provided in this blog is for general informational purposes only and does not constitute legal, financial, or insurance advice. Coverage options, terms, and availability may vary. Please consult with a licensed professional for advice specific to your situation