Flood insurance cost in Texas varies dramatically depending on where your home sits and how you protect it. At Brooks Insurance, we’ve helped hundreds of Texas homeowners understand why their premiums are what they are-and more importantly, how to bring those costs down.

Your flood zone, home elevation, and previous claims history all play a role. The good news is that several practical steps can meaningfully reduce what you pay each year.

What Determines Your Flood Insurance Premium

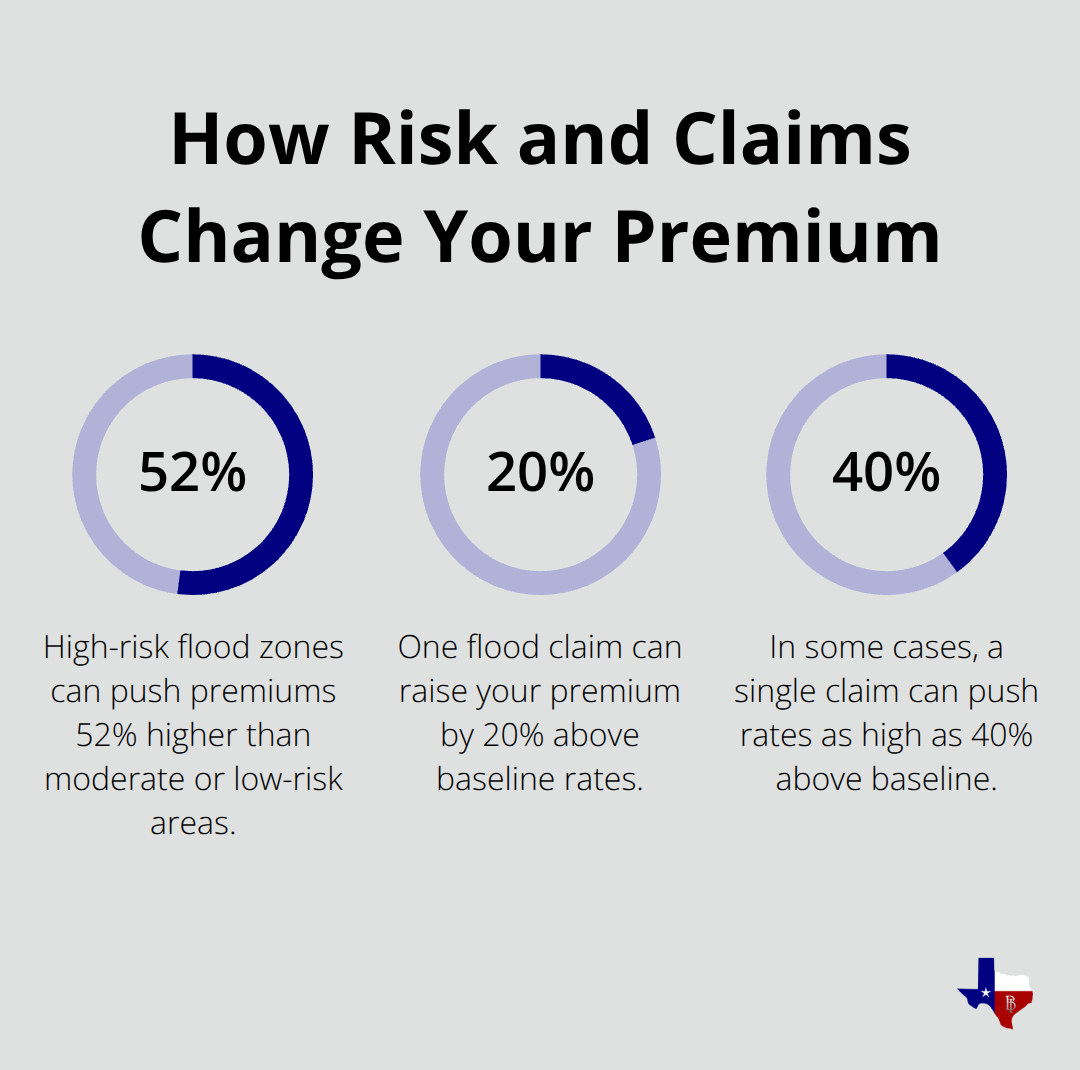

Your flood insurance premium in Texas depends on hard facts about your property and its surroundings. Risk Rating 2.0, implemented as of April 1, 2023, prices policies based on property-specific risk factors rather than relying solely on flood maps. This means two homes in the same flood zone pay vastly different premiums. Your location matters more than you think. In Houston, average NFIP premiums run about $1,200 to $1,500 per year, but in Austin they average around $601. Coastal Texas counties like Galveston average $992 annually, while inland Bexar County averages $794. High-risk flood zones in Texas can push premiums up to 52% higher than moderate or low-risk areas.

Distance from Water and Home Elevation

The distance your home sits from water sources directly impacts your rate. If your property sits further from a river, bayou, or coast, insurers view it as lower risk. Your home’s elevation relative to the expected flood level is equally critical. A property with its first floor elevated well above the base flood elevation pays substantially less than one built at or below that level.

Replacement Cost and Coverage Limits

The replacement cost value of your home and its contents drives your premium upward. A $400,000 home naturally costs more to insure than a $250,000 home. Your coverage limits matter too. NFIP policies cap dwelling coverage at $250,000 and contents at $100,000, but higher replacement values push you toward those limits and increase your annual cost.

How Your Home’s Physical Features Shape Cost

Your foundation type, first floor height, and whether machinery or equipment sits above flood level all factor into your premium calculation. Homes with elevated foundations or crawlspaces with proper flood openings qualify for NFIP mitigation discounts that can meaningfully reduce costs. A slab-on-grade foundation in a flood-prone area costs more to insure than an elevated structure. Age and construction quality matter as well. Older homes with outdated drainage systems or poor construction standards typically face higher premiums than well-maintained newer properties.

Loss History and Deductible Choices

If your home experienced flooding before, expect your premium to increase significantly. A previous flood claim creates a loss history that insurers view as predictive of future claims, and private insurers sometimes avoid or non-renew these properties altogether. Your deductible choice directly affects what you pay annually. Selecting a $5,000 deductible instead of $1,250 can lower your premium, but you’ll pay more out of pocket if a flood occurs. In Texas, shopping between NFIP and private flood insurance can reveal savings of 50 to 60 percent, though Houston’s high-risk market sometimes narrows that advantage. Understanding these cost drivers sets the stage for the practical steps that actually reduce what you owe each year.

Factors That Increase Your Flood Insurance Costs

Previous Flood Claims Raise Your Rates Significantly

Previous flood claims create a permanent mark on your property’s insurance record. If your home flooded once, insurers treat it as proof that flooding will happen again. Previous flood claims tracked by FEMA include properties in repetitive loss and severe repetitive loss categories. Private insurers often refuse to renew policies after a claim or charge rates so high they exceed NFIP pricing. One flood claim can raise your premium 20 to 40 percent above baseline rates. If your home has multiple claims within five years, private insurers may decline coverage entirely, leaving NFIP as your only option.

The NFIP doesn’t penalize you as harshly for loss history, but your rates still climb. Houston properties with repetitive loss history sometimes see premiums jump to $2,000 or higher annually. After a flood claim, you should document any mitigation work you complete-elevation improvements, new drainage systems, or flood vents can help offset future rate increases when you renew.

Your Home’s Age and Construction Standards Matter

Older homes cost more to insure because they typically lack modern drainage systems and may have foundation issues that increase flood vulnerability. A home built in 1975 with a slab-on-grade foundation in a flood-prone Houston neighborhood will pay substantially more than a 2015 home with an elevated foundation in the same area. Homes constructed to current building codes that account for flood risk have better structural protection. New construction with elevated first floors, reinforced foundations, and engineered flood vents qualifies for better mitigation discounts under NFIP pricing. The materials and quality of your home’s construction matter too. A home with poor drainage, deteriorating crawlspace walls, or inadequate ventilation presents higher risk. Cosmetic upgrades don’t reduce your premium, but structural improvements do. You can lower what you pay by upgrading your foundation type, raising your first floor height, or installing proper flood openings with engineering documentation.

Deductible Choices Control Your Annual Premium

Your deductible choice directly controls your annual premium. Selecting a $5,000 deductible instead of $1,250 cuts your premium by roughly 15 to 25 percent, depending on your flood zone and risk profile. Higher deductibles make sense if you have emergency savings to cover out-of-pocket costs after a flood. Lower deductibles protect you if your cash reserves are limited. In Texas high-risk zones, the difference between a $1,250 and $5,000 deductible might be $200 to $300 per year-savings worth evaluating against your financial situation. Your choice here directly affects what happens when water enters your home. The premium reduction you gain from a higher deductible must balance against the financial strain you’d face if a flood actually occurs. This trade-off sets the stage for the practical cost-reduction strategies that follow.

Ways to Lower Your Flood Insurance Premium

Elevation Improvements Deliver the Fastest Savings

Elevation work cuts your premium faster than any other single improvement. Raising your home’s first floor above the base flood elevation or installing flood vents in your crawlspace qualifies you for NFIP mitigation discount framework that reduces your annual cost, depending on your current foundation type and location. FEMA’s mitigation discount framework rewards homes with elevated foundations without enclosure, while those with solid foundation walls or properly engineered flood openings receive additional reductions. The machinery and equipment discount applies when all covered systems sit at least at the elevation of your first floor, so moving your HVAC unit, water heater, and electrical panel above flood level creates measurable savings. If your home sits in a high-risk Houston neighborhood, elevation work that qualifies you for multiple discounts could significantly reduce your annual premium. The Hazard Mitigation Grant Program covers up to 75 percent of eligible costs for qualifying homeowners, making structural improvements financially feasible even if your current budget is tight.

Drainage Improvements Strengthen Your Risk Profile

Drainage work reduces your flood risk score alongside elevation efforts. Proper grading around your foundation, sump pump installation, and gutter maintenance prevent water from pooling near your home’s structure. These improvements don’t always trigger the same discount percentages as elevation, but they improve your property’s risk profile when private insurers evaluate renewal decisions. After Hurricane Harvey, Houston homeowners who invested in drainage upgrades saw private insurers more willing to renew their policies rather than dropping them outright. Your foundation stays drier, and insurers recognize the reduced exposure.

Shop Between NFIP and Private Flood Insurance

Shopping between NFIP and private flood insurance is non-negotiable if you want the lowest premium. Private insurers often price competitively for properties outside the highest-risk zones, and even in coastal areas like Galveston, competitive quotes can provide meaningful savings.

Get quotes from at least three providers before you renew your policy, and compare deductible options alongside premium costs. A higher deductible with one insurer might save more than a lower deductible with another. Private flood policies also offer coverage NFIP doesn’t provide, including additional living expenses if you’re displaced by flooding and higher contents coverage limits beyond NFIP’s $100,000 cap.

Bundle Policies and Leverage Community Discounts

If you carry homeowners insurance with one company, bundling flood coverage with that same insurer often unlocks discounts. Texas communities participating in FEMA’s Community Rating System offer NFIP discounts to residents, so check whether your city qualifies. Your foundation type, first floor height, and distance to water sources affect what different insurers charge, so what works for your neighbor may not be your best option. Personalized quotes that account for your specific property features matter far more than relying on averages.

Final Thoughts

Your flood insurance cost in Texas reflects factors you control and factors you cannot. Location, home elevation, foundation type, and previous claims history shape what you pay annually, but elevation improvements, drainage work, and strategic deductible choices deliver measurable savings. Shopping between NFIP and private flood insurance reveals options that generic quotes miss entirely-a property in Houston might cost $1,500 with one insurer and $900 with another, depending on how each company weighs your specific risk factors.

An independent agency represents multiple insurers, not just one, which means you access competitive quotes and coverage options that online tools cannot provide. We at Brooks Insurance have spent over 50 years helping Texas homeowners navigate flood insurance decisions, and our licensed agents know which insurers price fairly for elevated homes, which ones offer the best additional living expenses coverage, and which ones actually renew policies after a claim rather than dropping you.

Your next step is straightforward: get personalized quotes from at least three providers, compare deductible options alongside premiums, and ask about mitigation discounts your property qualifies for. Contact Brooks Insurance to discuss your specific situation and receive quotes tailored to your property rather than relying on averages or assumptions.

Disclaimer: The information provided in this blog is for general informational purposes only and does not constitute legal, financial, or insurance advice. Coverage options, terms, and availability may vary. Please consult with a licensed professional for advice specific to your situation