Managing a fleet means protecting your business from unexpected costs. At Brooks Insurance, we help Texas business owners find fleet auto insurance options that match their actual needs and budget.

Whether you run two vehicles or twenty, the right coverage keeps your team safe and your finances secure. This guide walks you through the coverage types, cost-saving strategies, and how to pick the right provider for your fleet.

What Coverage Actually Protects Your Fleet

Liability Coverage Handles Third-Party Claims

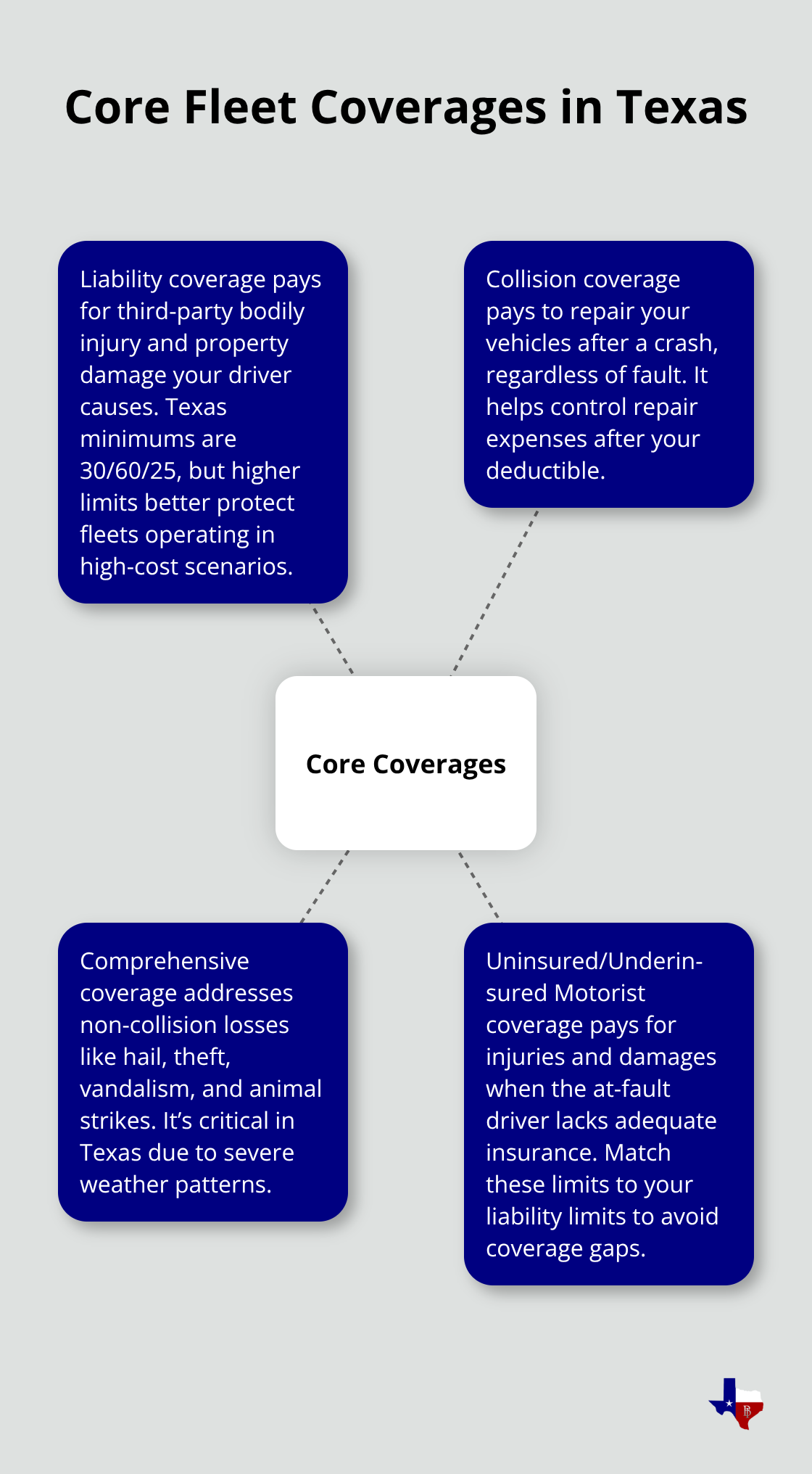

Fleet auto insurance in Texas requires three core protections that work together to handle different accident scenarios. Liability coverage is non-negotiable-Texas law mandates a minimum of 30/60/25, meaning $30,000 per person and $60,000 per accident for bodily injury, plus $25,000 for property damage. However, higher limits make sense for most fleets. If one of your drivers causes an accident that injures multiple people or damages expensive property, the state minimum disappears fast. A single serious injury claim can easily exceed $100,000, leaving your business exposed if you only carry the bare minimum. Fleets in construction, delivery, and service industries typically carry 100/300/100 limits or higher because their vehicles operate on busy roads where collision costs spike quickly.

Collision and Comprehensive Protection for Your Vehicles

Collision coverage handles damage to your own vehicles when you hit something or another vehicle hits you, regardless of fault. Comprehensive coverage takes everything else-weather damage from Texas hail storms, theft, vandalism, and animal strikes. In Texas, comprehensive becomes essential given severe weather patterns. The state experiences significant hail damage annually, particularly in spring months, and comprehensive policies cover these losses after you pay your deductible. Your deductible choice directly affects your premium; higher deductibles lower your premium costs but increase out-of-pocket expenses when a claim occurs.

Uninsured and Underinsured Motorist Protection

Uninsured and underinsured motorist coverage protects your drivers when the other party lacks adequate insurance or carries none at all. This coverage applies to medical expenses and vehicle damage caused by an uninsured or underinsured driver. About 12-15% of Texas drivers operate without insurance, making this protection critical for fleet safety. If an uninsured driver causes an accident involving your vehicle, uninsured motorist coverage steps in to cover your medical bills and lost wages without relying on the other driver’s policy. Underinsured motorist coverage fills the gap when the at-fault driver’s insurance limits are too low to cover your damages.

For fleets with multiple drivers, try carrying uninsured motorist limits that match your liability limits-so if you carry 100/300 liability, carry 100/300 uninsured motorist protection. This approach eliminates coverage gaps that leave your drivers vulnerable. Deductibles typically range from $250 to $1,000 per claim, and you should select deductibles based on your fleet’s cash flow and claims history rather than chasing the lowest premium. Once you understand these three core protections, the next step involves identifying which cost-saving strategies actually reduce your premiums without sacrificing the coverage your team needs.

How to Lower Fleet Insurance Costs Without Cutting Coverage

Reducing fleet insurance premiums requires a strategic approach that addresses the factors insurers actually use to calculate rates. The three most effective strategies involve bundling your policies, implementing measurable driver safety programs, and maintaining consistent vehicle upkeep.

Bundle Policies to Unlock Immediate Savings

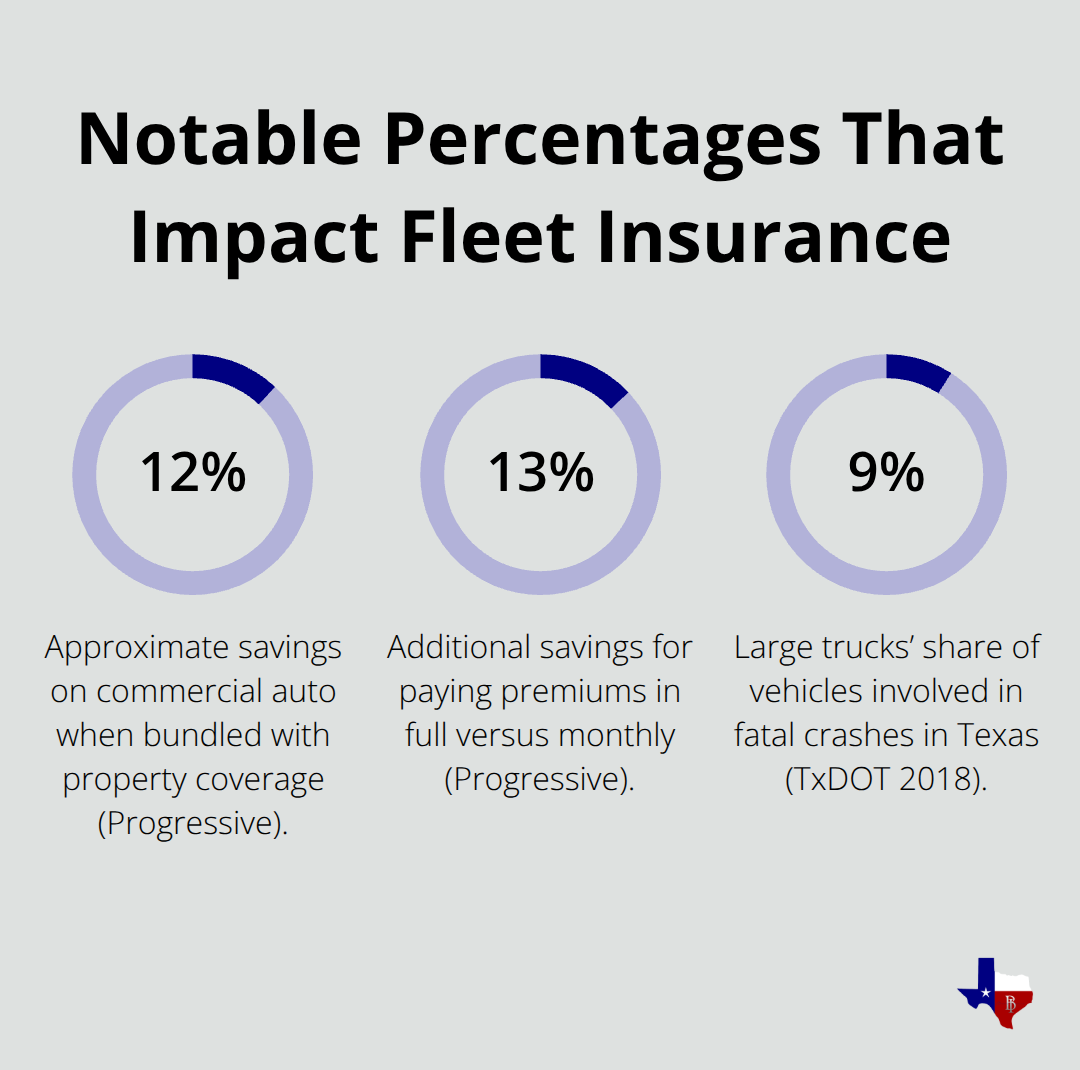

Bundling works because insurers reward businesses that consolidate coverage. Progressive reports saving approximately 12% on commercial auto when bundled with property coverage, plus additional incentives for multiple policies under one roof. If you carry general liability, workers compensation, or property insurance alongside fleet auto, combining them under one agent and insurer typically reduces your total premium.

Paying in full rather than monthly installments adds another 13% savings or more according to Progressive’s discount structure. For a fleet with five vehicles at an average $1,000 per vehicle annually, bundling and full payment could save $650 to $1,300 per year.

The key involves shopping with agents who represent multiple carriers, since different insurers weight bundling discounts differently. Some companies reward multi-policy customers aggressively while others offer modest discounts. Location matters significantly too-urban Texas fleets in Houston or Dallas pay higher premiums than rural operations due to traffic density and theft risk, but bundling can offset some of that geographic premium increase.

Implement Driver Safety Programs That Reduce Claims

Driver safety programs directly influence what insurers charge because they reduce claims frequency. Telematics systems track harsh braking, rapid acceleration, speeding, and distracted driving, providing insurers with concrete safety data. Fleets using telematics typically qualify for premium reductions because the data demonstrates lower risk. Dash cams serve a dual purpose: they reduce insurance costs by showing insurers you monitor driver behavior, and they provide evidence when claims occur, often resulting in faster claim resolution.

Formal driver training programs tied to actual performance metrics show insurers you take risk management seriously. Regular vehicle maintenance prevents breakdowns and mechanical failures that increase accident risk, which insurers recognize through lower premiums. Scheduling quarterly inspections, maintaining tire pressure, checking brakes, and documenting all maintenance creates a verifiable safety record. Fleets with documented maintenance schedules and clean driving records consistently pay 15-25% less than fleets with poor maintenance histories and frequent claims.

Combine Safety Data with Maintenance Records

The combination of telematics monitoring, driver training accountability, and documented maintenance transforms your fleet from a generic risk category into a demonstrably safer operation that insurers want to insure at competitive rates. This data-driven approach gives you leverage when shopping for quotes and negotiating rates with different carriers. Once you’ve optimized your internal operations and premium structure, the next critical decision involves selecting the right insurance provider who understands your fleet’s specific needs and can deliver responsive support when accidents happen.

Selecting the Right Fleet Auto Insurance Provider

Finding the right fleet insurance provider matters more than most business owners realize because the insurer you choose determines how quickly you get back on the road after an accident, what coverage gaps exist in your policy, and whether you pay fair rates for your actual risk profile. Evaluate three specific dimensions before signing any policy: how well the carrier’s coverage options match your fleet’s actual operations, whether their claims infrastructure can handle your team’s needs, and whether the agent understands fleet-specific risks in Texas rather than treating your business like a standard commercial account. Many fleets make the mistake of shopping solely on price, which typically means they discover coverage gaps only after an accident occurs.

Compare Coverage Options Across Multiple Carriers

Progressive insures commercial vehicles and maintains significant market share in the commercial insurance space, but market share doesn’t guarantee the best fit for your specific operation. A construction fleet operating in rural West Texas faces completely different risks than a delivery service operating across Houston’s dense urban corridors, yet generic quotes from large carriers often fail to account for these operational differences. Your insurer should ask detailed questions about your vehicles’ typical routes, annual mileage per vehicle, whether you transport cargo, which industries you serve, and your drivers’ experience levels before quoting. Carriers that rush through the quoting process without understanding these specifics typically underprice your risk, which means either inadequate coverage or surprise premium increases at renewal.

Evaluate Claims Support and Response Times

Claims support separates adequate insurance from genuinely useful insurance when your drivers actually need help. The Texas Department of Transportation’s 2018 Commercial Vehicle Crash Data shows that large trucks account for approximately 9% of vehicles involved in fatal crashes, highlighting why responsive claims handling matters urgently when incidents occur. Ask prospective carriers whether they employ in-house commercial claims adjusters who understand fleet operations rather than routing claims through generic call centers, whether they maintain a network of specialty repair shops in your operational areas, and whether they offer 24/7 support for roadside emergencies. An insurer with 24/7 access and local repair networks gets your vehicles operational faster, reducing downtime costs that often exceed the insurance premium itself.

Verify Self-Service Tools and Administrative Support

Additionally, verify whether the carrier offers self-serve tools for filing claims and making payments, as these capabilities simplify fleet administration when you manage multiple vehicles. Digital platforms that let you track claim status, upload documentation, and manage policy details reduce the time your team spends on administrative tasks. Some carriers provide mobile apps that connect drivers directly to claims support, which accelerates incident reporting and evidence collection at the scene of an accident.

Work with an Independent Agent Who Knows Fleet Operations

Work with an independent agent who represents multiple carriers and possesses genuine fleet experience in Texas rather than a captive agent representing a single company. Independent agents can compare coverage options across multiple top-rated insurers, identify which carrier best matches your specific fleet profile, and advocate on your behalf during renewals or claims disputes. A knowledgeable independent agent typically saves fleets 15-25% annually through proper coverage structure and negotiation that generic online quotes never capture. The agent’s relationships with multiple carriers also mean they can negotiate better terms, access carrier-specific discounts you wouldn’t find on your own, and adjust your coverage as your fleet evolves.

Final Thoughts

Fleet auto insurance protects your business from financial devastation when accidents happen, but only if you select the right coverage and provider. The three core protections-liability, collision and comprehensive, and uninsured motorist coverage-work together to handle the different ways your fleet faces risk on Texas roads. Liability coverage meets state minimums but should exceed them based on your actual operations, while collision and comprehensive protect your vehicles from damage and weather events. Uninsured motorist coverage fills gaps when other drivers lack adequate insurance, which happens frequently in Texas.

Reducing your premiums without sacrificing protection requires action on multiple fronts. Bundling your fleet auto insurance options with other business policies typically saves 12% or more on your commercial auto premium, and implementing driver safety programs with telematics and dash cams demonstrates lower risk to insurers, often qualifying your fleet for 15-25% premium reductions. Maintaining documented vehicle maintenance schedules reinforces your commitment to safety and further reduces your rates across the board.

Selecting the right insurance provider determines whether you receive fair pricing and responsive support when you need it most. At Brooks Insurance, we represent multiple top-rated carriers, which means we compare fleet auto insurance options across different companies rather than pushing you toward a single insurer, and our licensed agents understand fleet-specific risks in Texas to structure your policy without coverage gaps. Contact us today to receive a quote tailored to your fleet’s actual needs.

Disclaimer: The information provided in this blog is for general informational purposes only and does not constitute legal, financial, or insurance advice. Coverage options, terms, and availability may vary. Please consult with a licensed professional for advice specific to your situation