General liability insurance protects businesses from lawsuits and claims that could financially devastate them. This coverage handles bodily injury, property damage, and advertising injury claims from third parties.

We at Brooks Insurance see countless Texas business owners who underestimate their liability exposure. Understanding what general liability insurance covers helps you make informed decisions about protecting your business and personal assets.

What Does General Liability Insurance Actually Cover?

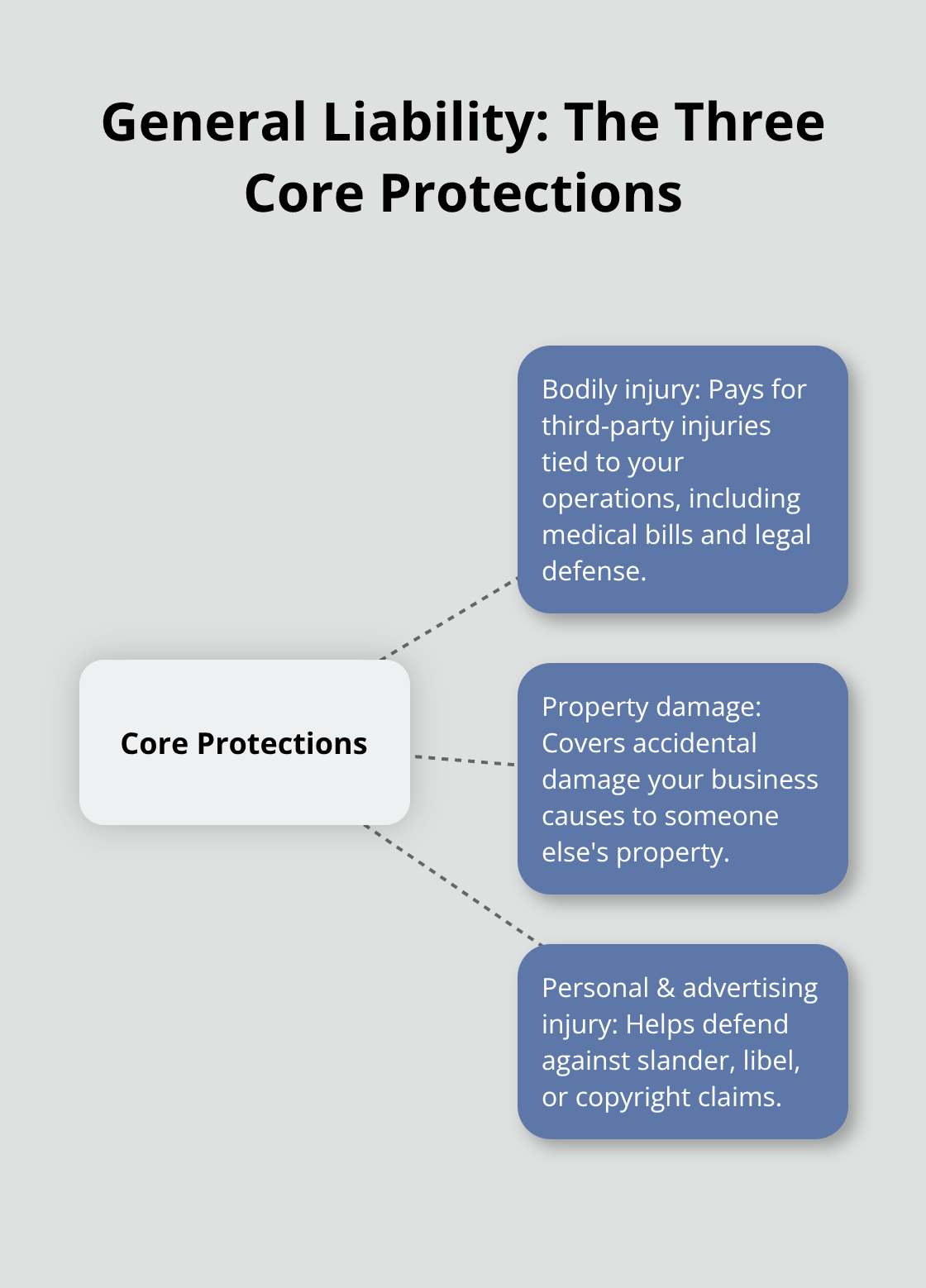

The Three Core Protection Areas

General liability insurance covers three primary areas that directly impact your business finances. Bodily injury coverage pays when someone gets hurt on your property or due to your business operations, with medical expenses that average $42,000 per workplace injury (National Safety Council data). Property damage protection handles situations where your business activities damage someone else’s property, like a contractor who accidentally breaks a client’s window. Personal and advertising injury coverage protects against claims of slander, libel, or copyright infringement, which cost businesses $15,000 to $50,000 in legal fees alone.

Who Actually Needs This Coverage

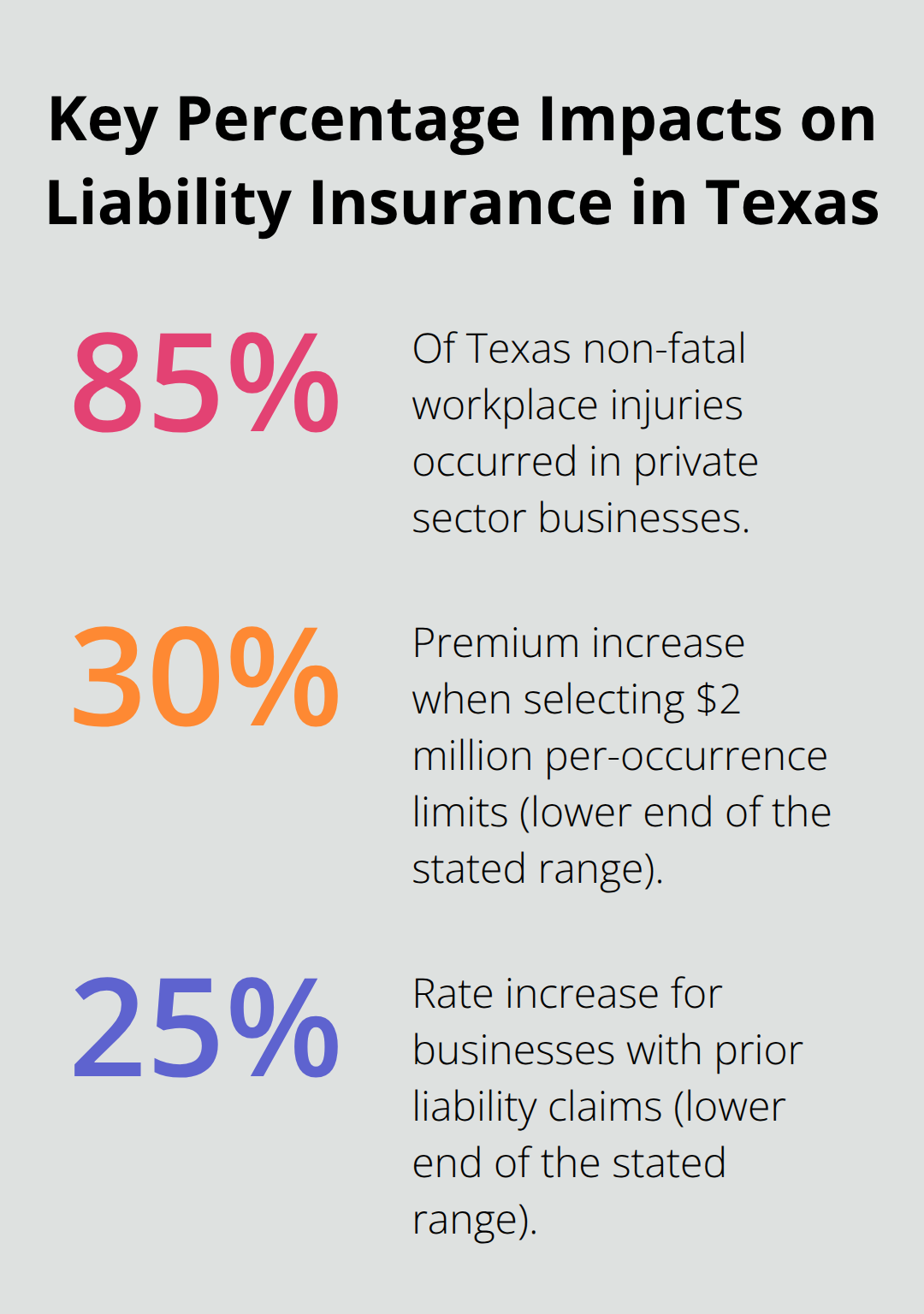

Every business that interacts with customers, vendors, or the public needs general liability insurance. Texas recorded 210,000 non-fatal workplace injuries in 2020, with over 85% that occurred in private sector businesses. Restaurants face slip-and-fall claims, contractors deal with property damage accusations, and service providers encounter advertising injury lawsuits. Even home-based businesses need protection when clients visit their premises or when they work at client locations.

Texas Legal Requirements and Industry Standards

Texas doesn’t legally mandate general liability insurance for most businesses, but many contracts and lease agreements require it. Commercial property landlords typically demand $1 million in coverage before they sign leases. Government contracts often require proof of liability insurance, and many clients won’t work with uninsured businesses. The median monthly cost for new customers is $60 (Progressive data), which makes it an affordable safeguard against lawsuits that could cost hundreds of thousands in legal fees and settlements.

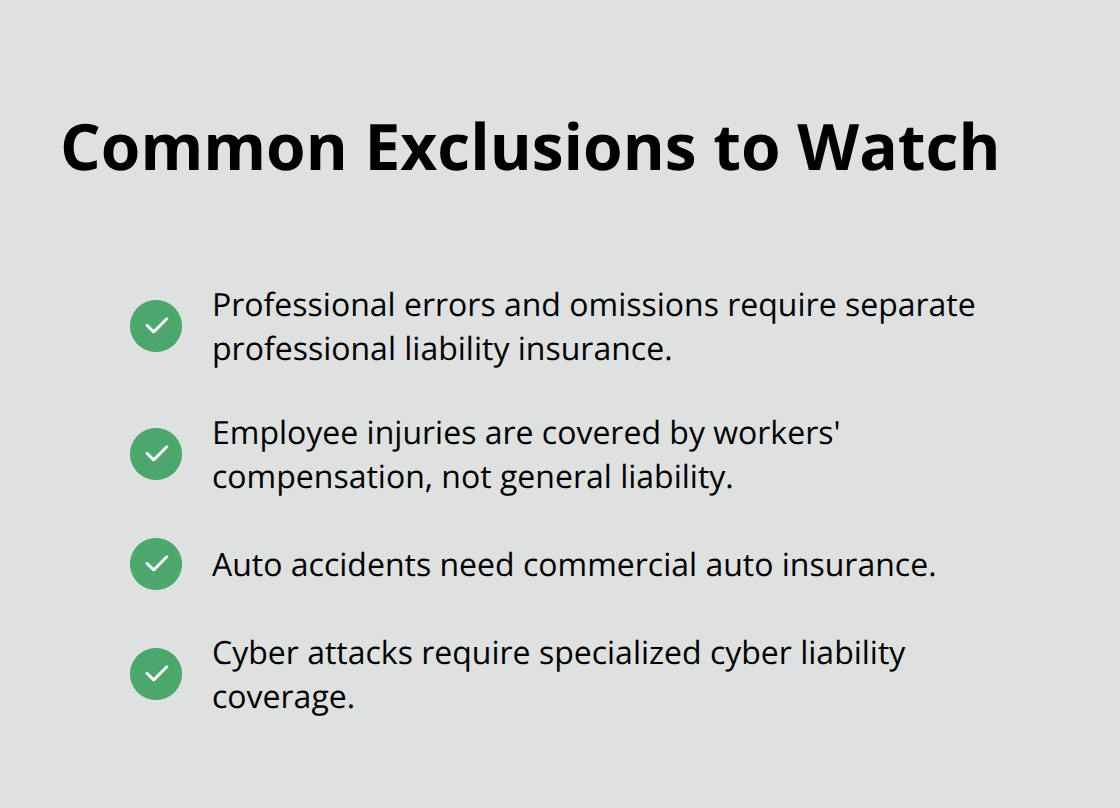

Common Exclusions You Should Know

Standard general liability policies exclude certain types of claims that catch business owners off guard. Professional errors and omissions fall outside general liability coverage, which means consultants and service providers need separate professional liability insurance. Employee injuries require workers’ compensation coverage instead of general liability protection. Auto accidents need commercial vehicle insurance, and cyber attacks require specialized cyber liability coverage to protect your business adequately.

The specific types of claims your policy covers depend on your industry and the exact policy language, which makes it important to understand what situations trigger coverage.

What Claims Will Your General Liability Policy Actually Pay?

Bodily Injury Claims Create Major Financial Exposure

Bodily injury claims represent the most expensive part of general liability coverage, with settlements that average $90,043 per incident according to National Safety Council data. These claims occur when customers slip on wet floors, trip over equipment, or sustain injuries during business operations. A restaurant customer who breaks their ankle on an uneven sidewalk creates medical bills, lost wages, and potential pain and suffering damages that quickly reach six figures.

Construction companies face even higher exposure, with bodily injury claims from job site accidents that often exceed $100,000. Texas businesses should carry at least $1 million in bodily injury coverage because legal fees alone cost between $100 to $500 per hour (according to Lawyers.com), and complex cases extend for months or years.

Property Damage Coverage Protects Against Costly Mistakes

Property damage coverage pays when your business operations damage someone else’s property. A landscaper who accidentally damages a client’s sprinkler system or a delivery driver who scratches a customer’s door both trigger this coverage. These incidents happen more frequently than most business owners expect, and repair costs add up quickly.

The coverage extends beyond simple accidents to include damage from your products or completed work. A contractor whose faulty installation causes water damage to a client’s home relies on this protection to cover repair costs and potential business interruption losses.

Personal Injury and Medical Payments Fill Coverage Gaps

Personal and advertising injury protection covers claims of slander, libel, copyright infringement, and false advertising, with legal defense costs that range from $15,000 to $50,000 per case. These claims often surprise business owners who focus only on physical accidents and property damage.

Medical payments coverage works differently from bodily injury protection by paying small medical bills immediately without determining fault. This coverage typically handles $5,000 to $10,000 per incident and helps maintain customer relationships by addressing minor injuries like cuts or bruises without lengthy legal proceedings.

Understanding these coverage areas helps you evaluate whether your current policy limits match your actual risk exposure and business operations.

How Much Does General Liability Insurance Cost

General liability insurance premiums depend on industry risk levels, business size, and claims history, with Texas businesses that pay between $400 to $1,500 annually for basic coverage. High-risk industries like construction and landscaping face premiums that reach $2,000 to $3,000 per year, while low-risk businesses such as consultants often pay under $600 annually. Insurance companies calculate rates with payroll figures, square footage, and revenue data, where each $100,000 in annual revenue typically adds $50 to $100 to your premium. Your claims history directly impacts rates, as businesses with previous liability claims pay 25% to 40% higher rates than those with clean records.

Coverage Limits Directly Affect Your Protection and Costs

Most Texas businesses choose $1 million per occurrence and $2 million aggregate limits, which costs approximately $60 per month. Higher limits of $2 million per occurrence increase premiums by 30% to 50%, but provide better protection against large claims. Deductibles range from $250 to $2,500, with higher deductibles that reduce premiums by 10% to 20%. Businesses that face contract requirements or higher risk exposure should select $2 million limits, while low-risk service businesses often find $1 million adequate for their operations.

Industry Type Determines Your Base Premium Rate

Construction companies and landscapers pay the highest rates because they work with heavy equipment and face constant injury risks. Restaurants and retail stores pay moderate premiums due to customer interaction and slip-and-fall exposure. Professional service businesses like accountants and consultants pay the lowest rates because they operate in office environments with minimal physical risks. Manufacturing businesses fall into the high-risk category when they produce products that could cause harm or damage.

Smart Strategies Cut Insurance Costs Without Sacrifice

Safety programs reduce premiums by 5% to 15%, as insurers reward businesses that actively prevent accidents through employee training and hazard identification. Bundled policies with commercial property or workers compensation create package discounts of 10% to 25%. Annual payment schedules eliminate monthly fees that add $50 to $100 yearly. Independent agencies provide access to multiple carriers and competitive rates, while strong relationships with single carriers often result in loyalty discounts after three claim-free years.

Final Thoughts

General liability insurance protects your business from lawsuits that could destroy your operations, with bodily injury claims that average $90,043 per incident and property damage costs that escalate rapidly. This coverage shields your personal assets and business operations from third-party claims while it maintains customer relationships through immediate medical payments for minor injuries. Texas businesses face significant financial exposure without proper protection against these common risks.

Your industry risk level and contract requirements determine the right coverage amount for your specific situation. Most Texas businesses need $1 million per occurrence limits, while high-risk operations like construction require $2 million for adequate protection. Annual revenue, employee count, and customer interaction levels all influence the coverage limits that match your actual exposure (with higher-risk businesses needing more comprehensive protection).

Understanding what is general liability insurance helps you make informed decisions about protecting your business from costly lawsuits and claims. We at Brooks Insurance represent multiple top-rated carriers and provide personalized quotes that match your specific risk exposure and budget requirements. Brooks Insurance offers competitive rates and expert guidance to help you secure the right coverage for your business operations.