General liability insurance cost varies dramatically based on your business type, size, and risk factors. Most Texas businesses pay between $400 and $3,000 annually for coverage.

We at Brooks Insurance see how these premiums can impact your bottom line. Understanding the key factors that drive pricing helps you make smarter coverage decisions and find better rates.

What Affects General Liability Insurance Costs

Business Size and Revenue Impact on Premiums

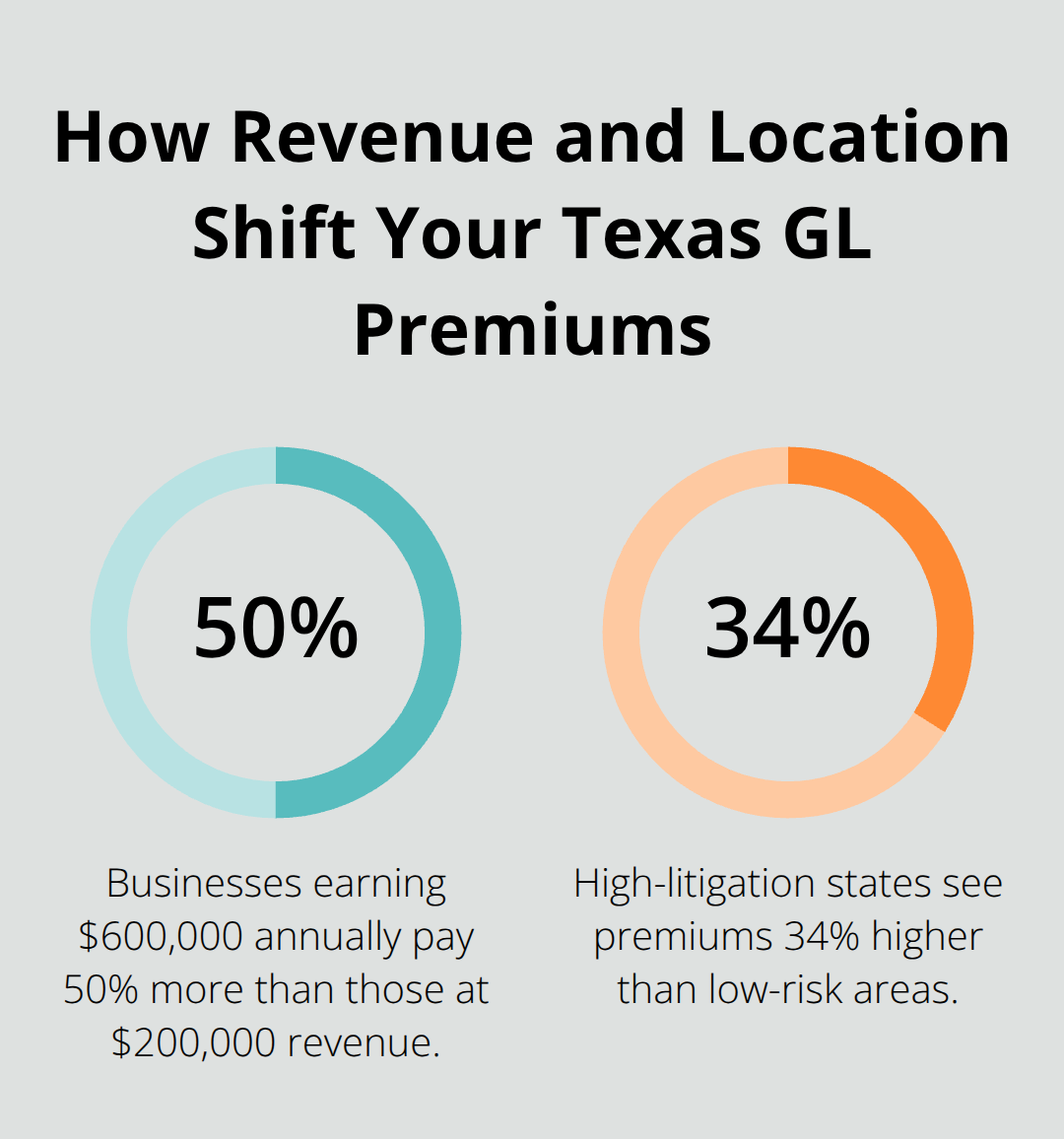

Your annual revenue forms the foundation for premium calculations. Progressive data shows businesses that earn $600,000 annually pay 50% more than companies with $200,000 in revenue. Insurance companies view higher revenue as increased exposure to potential claims and larger settlement amounts.

A consulting firm with $100,000 in annual sales might pay $780 yearly, while the same business type that earns $500,000 could face premiums that exceed $1,200. This revenue-based approach reflects the reality that larger operations handle more customers, transactions, and potential liability situations daily.

Industry Risk Level and Claims History

Construction companies pay nearly 12 times more than consulting firms due to inherent injury risks. Pressure washing businesses face monthly premiums of $918 because of slip hazards, while drone operators pay just $17 monthly. The Hartford research reveals accountants average $22 monthly premiums, contractors pay around $256, and retail businesses settle at approximately $696 annually.

Your industry classification code directly correlates with claim frequency data that insurance companies maintain. High-risk sectors like roofing, landscaping, and installation work consistently generate more bodily injury and property damage claims than office-based businesses.

Coverage Limits and Deductible Choices

Coverage limits that double increase premiums by 15% to 25%, but claims can significantly impact your rates for extended periods. The frequency in 2024 was 6.9 claims per $100 million GDP, compared to 9.8 per $100 million before the pandemic. Companies that maintain clean claims records receive 10% to 20% discounts over time (a significant long-term savings opportunity).

Most Texas businesses select $1 million per occurrence limits with $2 million aggregate coverage for adequate protection without excessive premium costs. Higher deductibles reduce monthly payments but increase your out-of-pocket exposure when claims occur. Geographic location adds another layer, with high-litigation states that see premiums 34% higher than low-risk areas (making Texas location selection important for cost management).

These cost factors work together to create your final premium, but specific business types show dramatically different average costs across industries.

Average General Liability Insurance Costs by Business Type

Small businesses across Texas face dramatically different premium costs based on their specific operations and risk exposure. MoneyGeek data shows The Hartford offers the most competitive rates at $83 monthly, while Simply Business and Nationwide follow at $97 and $98 respectively. These baseline figures shift dramatically when you examine actual business categories and their real-world premium ranges.

Small Business Premium Benchmarks

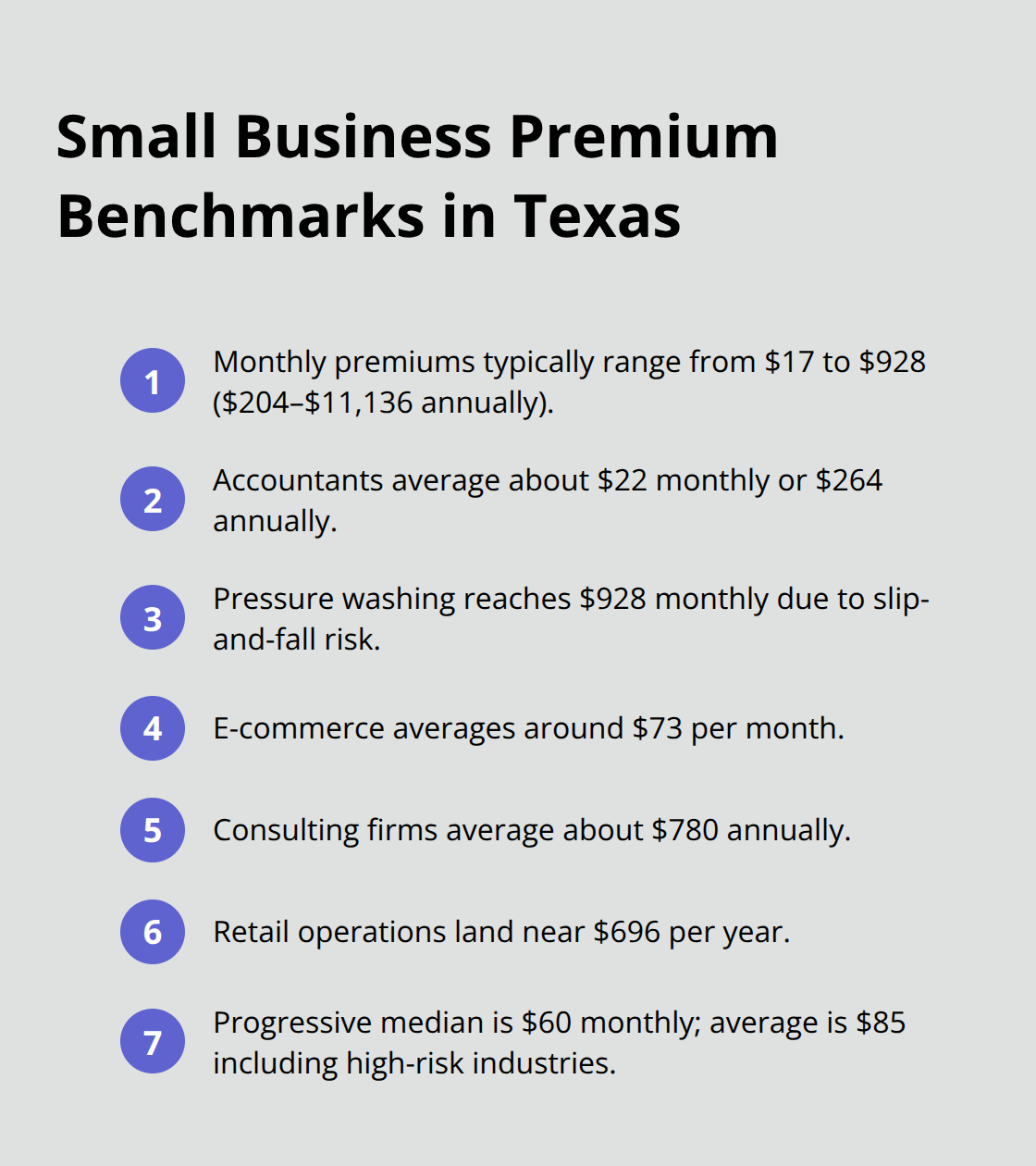

Most Texas small businesses pay between $17 and $928 monthly for general liability coverage (an annual range from $204 to $11,136). Accountants represent the lowest-cost category at approximately $22 monthly or $264 annually, while pressure washing operations hit the premium ceiling at $928 monthly due to slip and fall hazards. E-commerce businesses typically settle around $73 monthly, and consulting firms average $780 annually.

Retail operations land near $696 per year. Progressive research indicates their median monthly cost sits at $60 for new customers, though the average reaches $85 monthly when you factor in high-risk industries.

High-Risk Industries Pay Premium Prices

Construction businesses face the steepest premiums at roughly $2,125 annually, nearly 12 times higher than consulting firms due to constant injury exposure and property damage risks. Contractors face significant claim exposure, with general liability claims averaging $51,500 in 2025. Roofing contractors, landscapers, and installation companies consistently generate more claims than office-based operations. This drives their premiums into the $200-300 monthly range. Drone operators pay minimal premiums at $17 monthly because their operations present limited physical interaction risks.

Texas Regional Cost Variations

Major Texas metropolitan areas like Houston and Dallas command higher premiums due to increased litigation activity and elevated costs. Businesses that operate in these high-density markets face greater claim frequency and larger settlement amounts. This pushes their premiums 15-25% above rural Texas averages. Weather-prone regions across the state also see elevated premises liability costs, as severe storms and events increase property damage exposure for businesses that maintain physical locations.

These cost variations highlight why smart business owners focus on strategies to reduce their premiums without sacrificing essential protection.

Ways to Reduce General Liability Insurance Premiums

Safety Programs Deliver Measurable Premium Reductions

Companies with documented safety programs can earn premium discounts, particularly for high-risk industries like roofing and construction. Companies that maintain robust safety protocols demonstrate reduced claim likelihood to insurers, which translates directly into lower premiums over time. The Hartford data shows businesses with established safety records maintain consistently lower rates compared to operations without formal risk management procedures.

Workplace safety courses, regular equipment maintenance schedules, and incident reports create a paper trail that insurance companies reward with premium discounts. These programs require upfront investment but generate long-term savings that often exceed the initial costs within 24 months.

Policy Bundling Creates Substantial Savings

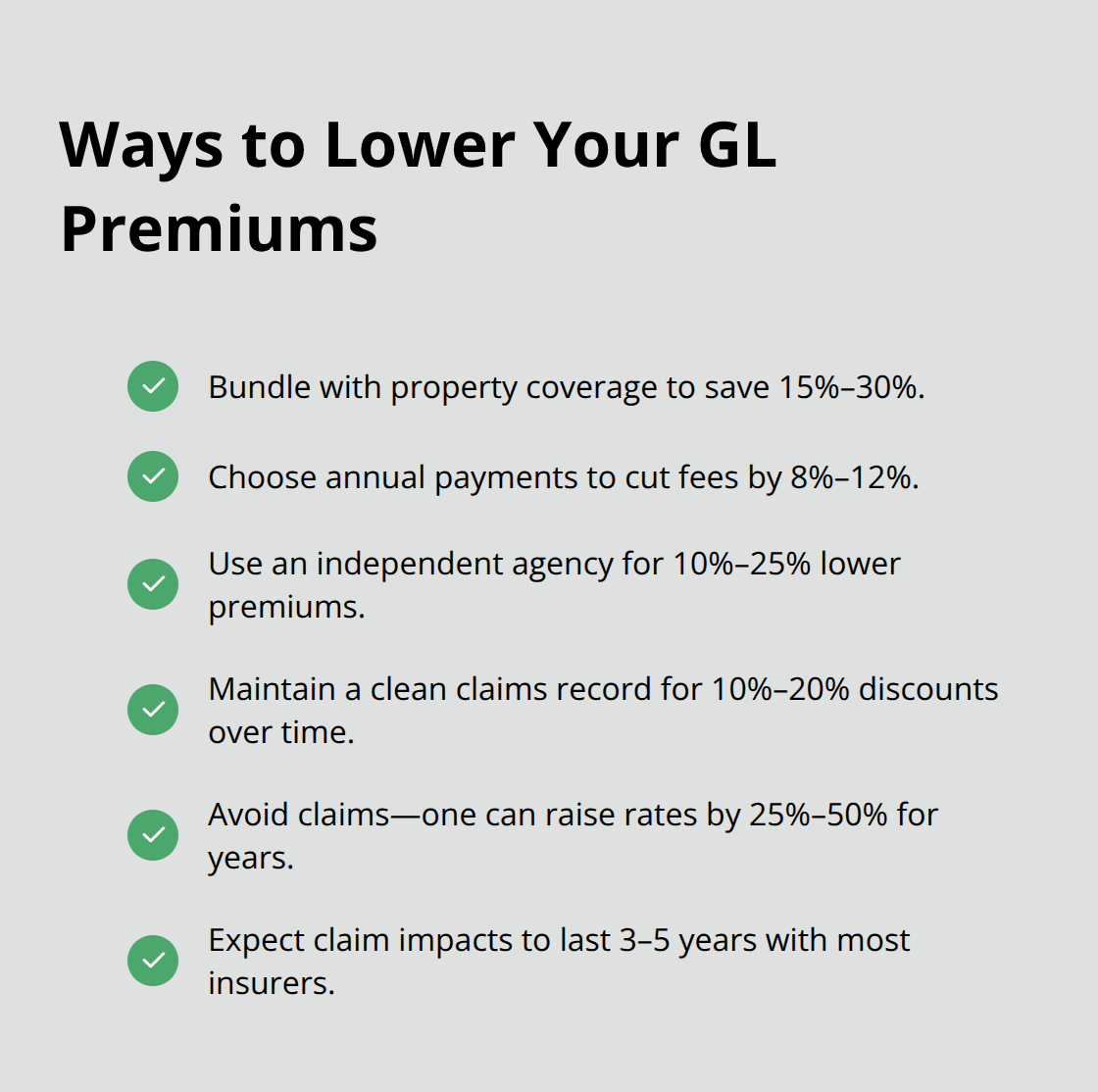

Bundled general liability with property coverage results in savings of 15% to 30% compared to separate policies from different insurers. Most Texas businesses save between $200 and $800 annually through multi-policy discounts when they combine commercial auto, workers compensation, and general liability coverage.

Annual payment options reduce fees by 8% to 12%, which creates additional savings of up to $156 yearly compared to monthly payment plans. Independent agencies access wholesale rates that direct insurers cannot match (often resulting in 10% to 25% lower premiums for identical coverage limits and deductibles).

Claims History Management Protects Future Rates

Clean claims records receive 10% to 20% discounts over time, while one claim can increase premiums by 25% to 50%. Claims impact rates for three to five years post-incident, with insurers that assess risk differently based on your track record.

Companies that invest in preventive measures and proper documentation avoid costly claims that damage their insurance profile. Regular property maintenance, employee safety courses, and proper customer interaction protocols reduce the likelihood of incidents that trigger premium increases. Contractors can reduce general liability premiums through strategic policy selection and risk management approaches.

Final Thoughts

General liability insurance cost depends on three primary factors: your business type and revenue, industry risk level, and coverage choices. Texas businesses pay between $17 and $928 monthly, with construction companies that face premiums nearly 12 times higher than consulting firms. Your claims history impacts rates for three to five years, which makes risk management programs worth the investment.

Multiple quote comparisons remain the most effective strategy for competitive rates. Independent agencies access wholesale prices that direct insurers cannot match, often delivering 10% to 25% lower premiums for identical coverage (a significant advantage for cost-conscious business owners). We at Brooks Insurance represent multiple top-rated insurance companies, which gives you access to a larger selection of coverage options and prices.

Gather your annual revenue figures, employee count, and industry classification code before you request quotes. Contact at least three providers to identify the best combination of coverage and cost for your specific business needs. Smart business owners who compare options save hundreds of dollars annually on their general liability insurance cost.