Flooding is one of the most destructive natural disasters in Texas, and standard homeowners insurance won’t protect you from it. Understanding what flood insurance covers is the first step toward protecting your property and finances.

At Brooks Insurance, we help Texas homeowners navigate their flood insurance options so they’re not caught off guard when water damage strikes. This guide breaks down exactly what’s covered, what isn’t, and how to choose the right policy for your situation.

What Flood Insurance Actually Covers

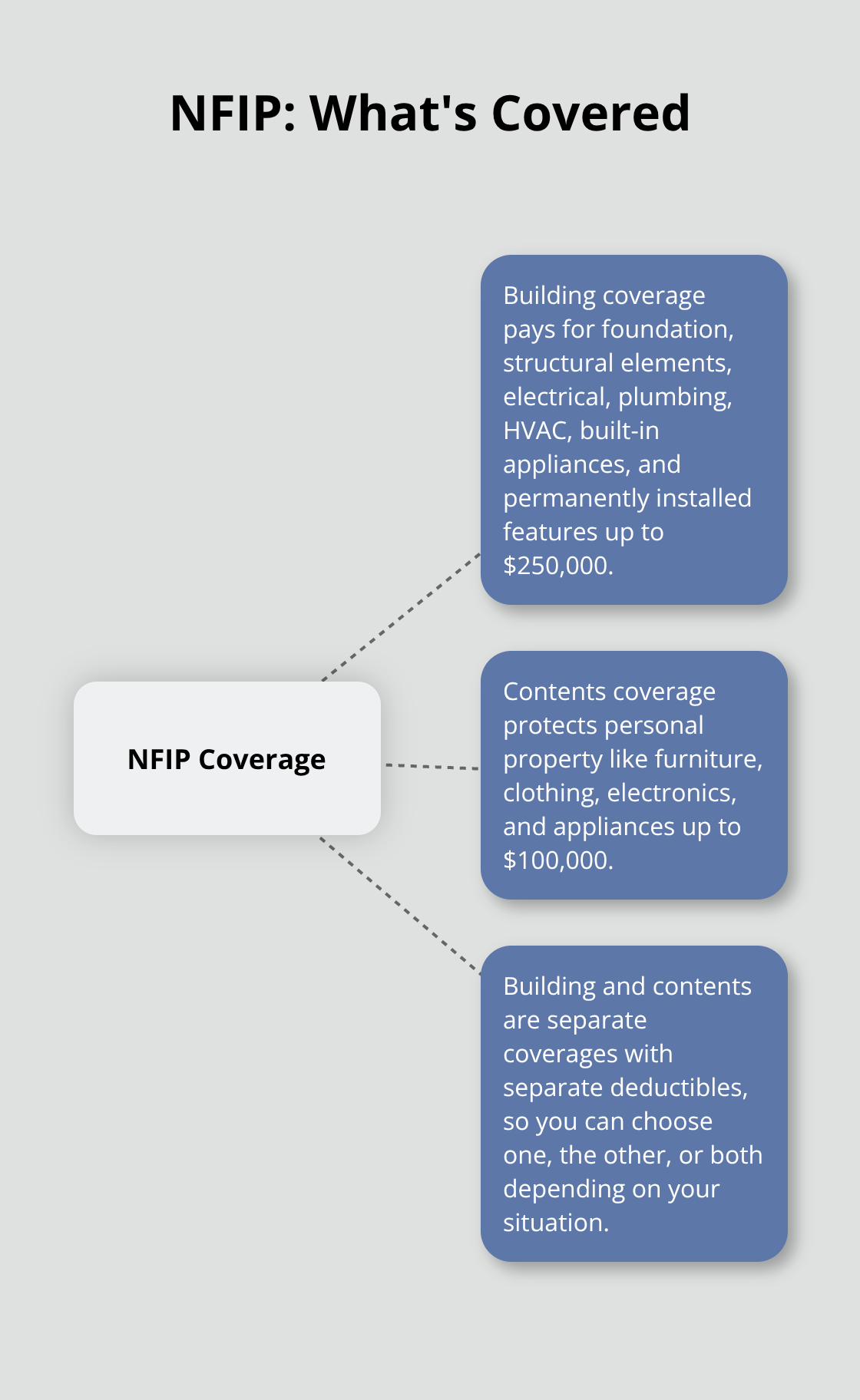

Flood insurance from the National Flood Insurance Program covers direct physical damage to your home’s structure and the belongings inside it, but the protection has real limits you need to understand. Building coverage pays for damage to your foundation, walls, electrical systems, plumbing, HVAC equipment, built-in appliances, and permanently installed features like cabinets and flooring, up to $250,000 for homeowners. Contents coverage protects your personal property-furniture, clothing, electronics, appliances, and other movable items-up to $100,000.

These are separate coverages with separate deductibles, so you might choose one, the other, or both depending on whether you own or rent your home and what protection matters most to your situation.

Understanding Your Coverage Limits

The $250,000 building cap and $100,000 contents limit sound substantial until a major flood hits. During Hurricane Katrina in 2005, the NFIP paid across 168,200 paid losses, showing how quickly flood damage exhausts standard coverage limits. If your home’s replacement cost exceeds $250,000 or your belongings are worth more than $100,000, you face a significant gap. Texas homeowners in high-value properties often discover their flood coverage falls short after damage occurs, which is why some choose private flood insurance that can offer higher limits-up to $2 million for structure coverage and contents coverage exceeding $500,000 in many cases. Your agent can help you calculate your actual replacement costs and determine whether standard NFIP limits work for your property.

What Else Flood Insurance Includes

Beyond structure and contents, NFIP policies cover some additional protections that matter when water invades your home. Valuable items like original artwork or furs receive coverage up to $2,500 under contents coverage, which helps if you own collectibles. However, flood insurance does not cover temporary housing costs, business interruption, or loss of use-expenses that can quickly drain savings after displacement. Some private flood policies do include loss of use coverage, covering additional living expenses if flooding forces you from your home, making them worth comparing if you’re concerned about relocation costs during recovery.

Comparing NFIP and Private Flood Insurance

Private flood insurance offers higher limits and broader protections than the NFIP standard policy. While NFIP caps building coverage at $250,000 and contents at $100,000, private insurers can provide up to $2 million for structure coverage and contents coverage exceeding $500,000. Private policies also may include loss of use coverage (additional living expenses), a feature NFIP policies generally do not offer. The trade-off involves potentially higher premiums, though advanced risk modeling and data analytics have helped some private insurers reduce rates over time. Your specific situation-property value, location, and budget-determines which option makes the most sense.

Next Steps for Your Coverage Decision

Now that you understand what flood insurance covers and where the gaps exist, the next step involves assessing your own property’s flood risk and calculating what replacement costs would actually be. Your location in Texas, proximity to water, elevation, and the age of your home all affect both your flood risk and the coverage limits you should carry.

What Flood Insurance Leaves Unprotected

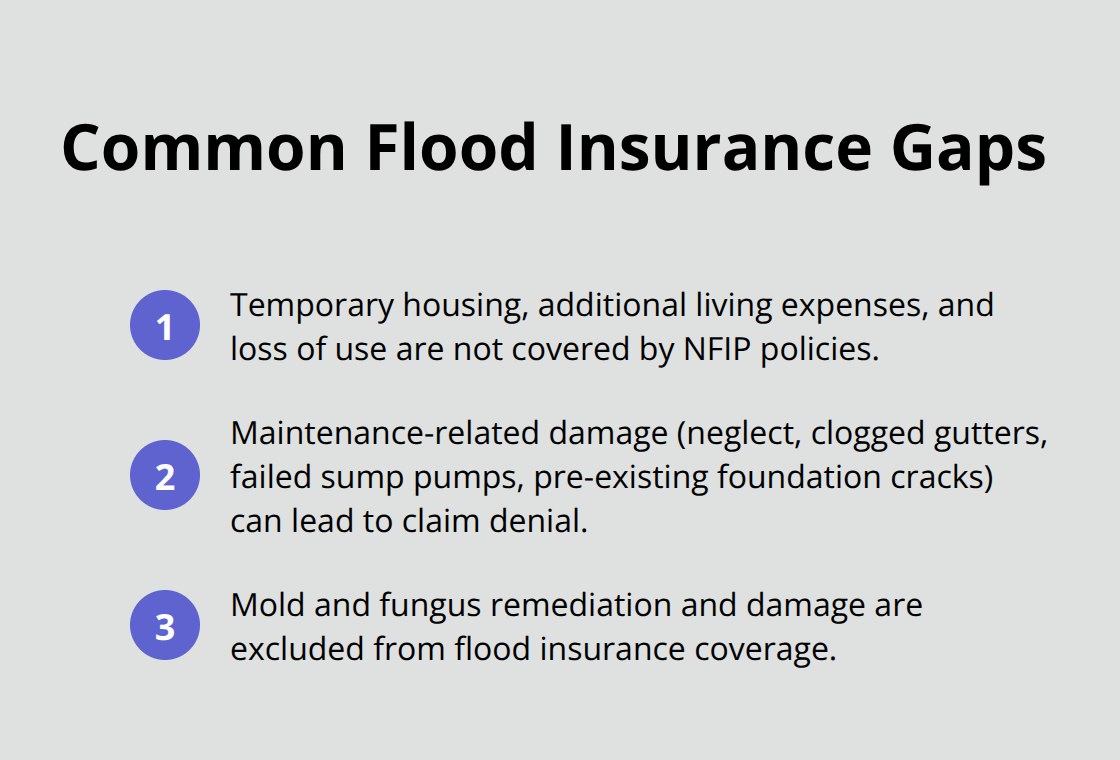

Flood insurance fills a gap that standard homeowners policies ignore, but it has substantial exclusions that catch many Texas property owners off guard. The NFIP explicitly does not cover temporary housing, additional living expenses, or loss of use-meaning if flooding forces you from your home, you pay hotel bills, rental costs, and meals while repairs happen.

This omission matters more than it sounds; after Hurricane Harvey in 2017, thousands of Texas families faced weeks or months of displacement while waiting for repairs, and their flood policies paid zero dollars toward those relocation expenses. Some private flood insurers address this gap by offering loss of use coverage, which reimburses additional living expenses during recovery, making it worth discussing with your agent if extended displacement concerns you.

Maintenance Issues and Claim Denials

Maintenance-related damage falls outside flood insurance coverage-if your gutters were clogged, your sump pump failed, or your foundation had existing cracks that water exploited, the insurer will deny your claim. Insurers investigate whether poor maintenance contributed to water entry, and they will not pay if they find evidence of neglect. This distinction matters because it shifts responsibility to you for upkeep that could have prevented or reduced water intrusion. Texas homeowners often discover too late that deferred maintenance becomes a reason for claim rejection.

Mold and Fungus Exclusions

Mold and fungus damage represents another major exclusion that surprises homeowners after water damage occurs. Flood insurance does not cover mold remediation, mold damage to walls or contents, or fungal growth that develops after water intrusion, regardless of how the flooding happened. Texas’s humid climate makes mold growth almost inevitable after flooding, yet policies specifically exclude it, leaving you responsible for potentially expensive mold removal and structural repairs. If mold remediation costs exceed $10,000-a realistic figure for significant contamination-you absorb the entire expense yourself.

Addressing the Coverage Gaps

Understanding these exclusions before disaster strikes allows you to plan accordingly. Private flood insurance with broader coverage, separate mold coverage, or financial reserves for these predictable gaps all represent ways to protect yourself beyond standard NFIP limits. Your agent can help you evaluate which gaps pose the greatest risk to your specific property and finances. With these exclusions in mind, the next step involves assessing your actual flood risk and determining which coverage limits and policy type align with your property’s needs.

How to Choose the Right Flood Insurance Policy

Determine Your Flood Risk and Location

Your flood risk varies dramatically across Texas depending on where your property sits. The NFIP provides free flood maps that show whether your home falls in a high-risk zone, moderate-risk zone, or low-risk area, and this classification directly affects your premium and whether your lender requires flood insurance in Texas. If you have a mortgage from a government-backed lender in a high-risk flood zone, flood insurance becomes mandatory, not optional. Texas homeowners often assume their location is safe until they check the flood map and discover they sit in an area that experienced flooding during Hurricane Harvey in 2017 or the 2016 Louisiana severe storms. Your elevation, proximity to water, and property age all influence both your flood risk and the coverage limits you should carry.

Calculate Your Actual Replacement Costs

Calculate your home’s replacement cost to determine whether standard NFIP limits will actually protect you. Research construction costs in your area and your belongings’ actual value, not what you think they’re worth. This number determines whether standard NFIP limits of $250,000 for structure and $100,000 for contents will leave you facing a substantial shortfall. Homes in Houston, Dallas, and Austin suburbs often exceed these limits, making private flood insurance worth evaluating for the higher coverage available. Properties valued above $250,000 face significant gaps under NFIP building coverage alone.

Compare Coverage Options Across Policies

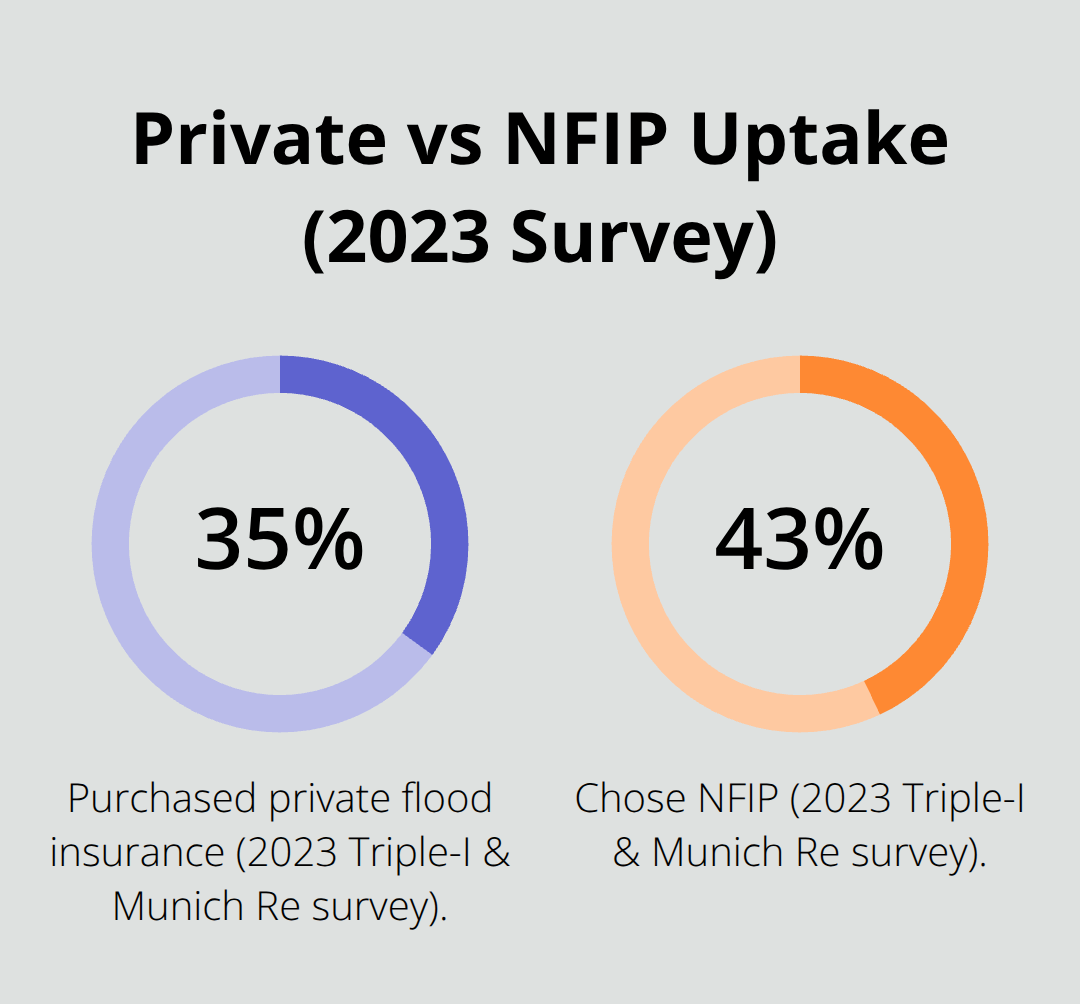

Compare what different policies actually cover rather than focusing solely on premium price. NFIP policies exclude loss of use and mold coverage, while some private insurers include loss of use coverage that reimburses additional living expenses during recovery. The 2023 Triple-I and Munich Re Consumer Survey found that 35 percent of homeowners at flood risk purchased private flood insurance while 43 percent chose NFIP, indicating both options serve legitimate needs depending on your circumstances.

Request quotes from multiple providers through an independent insurance agency, who can access NFIP pricing alongside private flood insurance options from companies like AXA, Liberty Mutual, Assurant, and others. An independent agent can help you compare deductible options, coverage limits, and specific exclusions across policies, saving you the time of contacting multiple insurers separately.

Evaluate Pricing and Advanced Risk Models

Don’t assume NFIP is cheaper-private insurers using advanced risk modeling have reduced rates considerably since 2012, and you may find competitive pricing with substantially better coverage. Private residential flood insurance has grown significantly, with policies nearly doubling from 277,000 in 2020 to approximately 569,000 by 2024, reflecting growing consumer interest in these alternatives. As insurers gain experience and use advanced data analytics and machine learning, private flood insurance rates may decrease further over time. Your specific situation-property value, location, and budget-determines which option makes the most sense for your finances.

Review Your Policy Annually

Review your policy annually because Texas property values and flood maps change, and your coverage should reflect your current situation, not what protected you five years ago. Flood map updates can shift your property into a higher-risk zone, triggering new lender requirements or premium increases. Property improvements that increase your home’s value may also require higher coverage limits to maintain adequate protection.

Final Thoughts

Flood insurance protects your Texas home and belongings from one of the most destructive natural disasters you’ll face, but only if you understand what coverage actually means for your situation. Standard homeowners policies leave you completely exposed to water damage, making flood insurance essential whether you own your home outright or carry a mortgage in a high-risk zone. The NFIP provides affordable baseline protection with building coverage up to $250,000 and contents coverage up to $100,000, while private insurers offer higher limits and additional protections like loss of use coverage that reimburse your living expenses during recovery.

What flood insurance covers ultimately depends on which policy you choose and how thoroughly you assess your property’s actual replacement costs. Many Texas homeowners discover their coverage falls short only after water damage occurs, leaving them responsible for gaps between their policy limits and their real losses. Hurricane Katrina demonstrated this reality when the NFIP paid an average of approximately $156,046 per claim across 168,200 losses, yet many homeowners faced replacement costs far exceeding those amounts.

Start by checking your property’s flood zone on the NFIP flood maps, then calculate your home’s replacement cost and your belongings’ actual value. Compare what standard NFIP policies cover against what private flood insurance offers in your area, paying attention to exclusions like mold coverage and loss of use protection. We at Brooks Insurance represent multiple top-rated insurance companies, giving you access to both NFIP options and private flood insurance alternatives so you can choose coverage that matches your needs and budget-contact us today to discuss your flood insurance options and protect your property before the next storm arrives.