Texas faces significant flood risks, with Hurricane Harvey causing $125 billion in damages across the state in 2017. Many homeowners mistakenly believe their standard property insurance covers flood damage.

We at Brooks Insurance help Texas residents navigate the complex world of flood insurance requirements and coverage options. Understanding your flood protection needs can save you thousands when disaster strikes.

When Must Texas Property Owners Buy Flood Insurance?

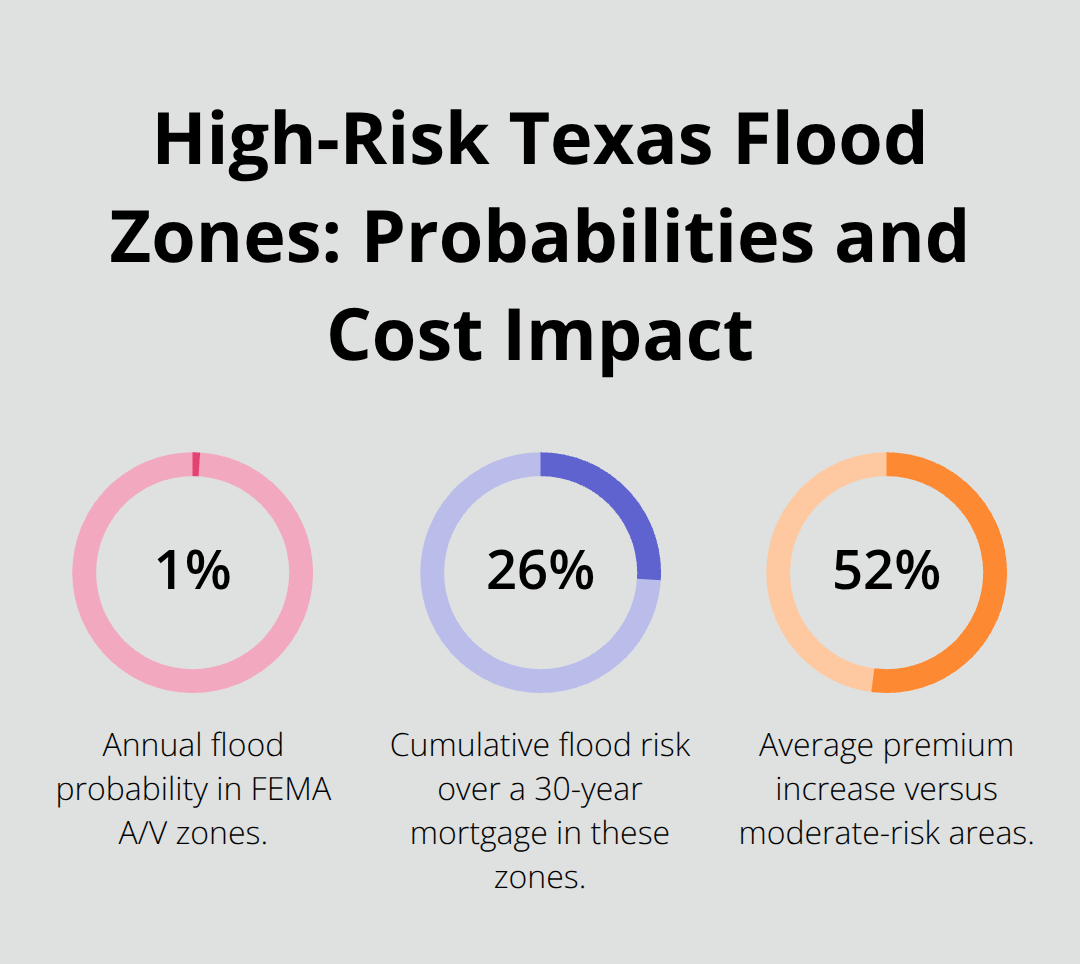

The Federal Emergency Management Agency mandates flood insurance for all mortgaged properties in Special Flood Hazard Areas, which include flood zones that start with A or V. These high-risk zones face a 1% annual chance of floods, which creates a 26% chance over a 30-year mortgage period. Lenders refuse to close your loan without proof of flood insurance coverage. Texas properties in these zones pay an average of $1,021 annually (52% higher than moderate-risk areas).

High-Risk Zone Requirements

Properties in FEMA-designated flood zones A and V face mandatory coverage requirements. Galveston County residents pay an average of $992 per year, while Hidalgo County averages $531 annually. The National Flood Insurance Program caps coverage at $250,000 for structures and $100,000 for contents. Your lender will verify coverage through an elevation certificate that compares your property’s height to the Base Flood Elevation.

Optional Coverage for Low-Risk Areas

FEMA data reveals 40% of flood claims occur outside high-risk zones between 2016 and 2022. These moderate- and low-risk properties average $66,000 in claim payouts. Travis County homeowners pay $644 annually while Montgomery County averages $692. The 30-day wait period prevents you from purchasing coverage after storm warnings are issued.

Texas-Specific Regulations

Texas Windstorm Insurance Association requires flood coverage for properties built or altered after September 1, 2009, to obtain windstorm policies. The Texas Department of Insurance considers the entire state within flood zones due to Flash Flood Alley that covers Central and North Texas. Major cities like Houston, Austin, and San Antonio sit in high-risk areas despite their inland locations.

Understanding these requirements helps you determine when coverage becomes mandatory versus optional. The next step involves exploring the different types of flood coverage available to Texas residents and what each policy type actually protects.

What Coverage Options Exist for Texas Flood Insurance?

Texas residents choose between two primary flood insurance sources: the National Flood Insurance Program managed by FEMA and private insurance companies. The NFIP covers 5.1 million policies nationwide with standardized rates and coverage limits, while private insurers offer customized policies with higher limits and additional benefits. Private flood insurance grew 15% annually from 2018 to 2023 as more Texans seek alternatives to federal programs.

NFIP Standard Coverage Limitations

The National Flood Insurance Program caps structure coverage at $250,000 and contents at $100,000, which falls short for many Texas properties. NFIP policies exclude Additional Living Expenses, basement improvements, and outdoor property like decks and pools. Deductibles range from $1,000 to $10,000, and the program requires separate contents coverage for personal belongings. The average NFIP claim payout between 2016 and 2022 reached $66,000 (which highlights the importance of adequate coverage limits).

Private Insurance Advantages

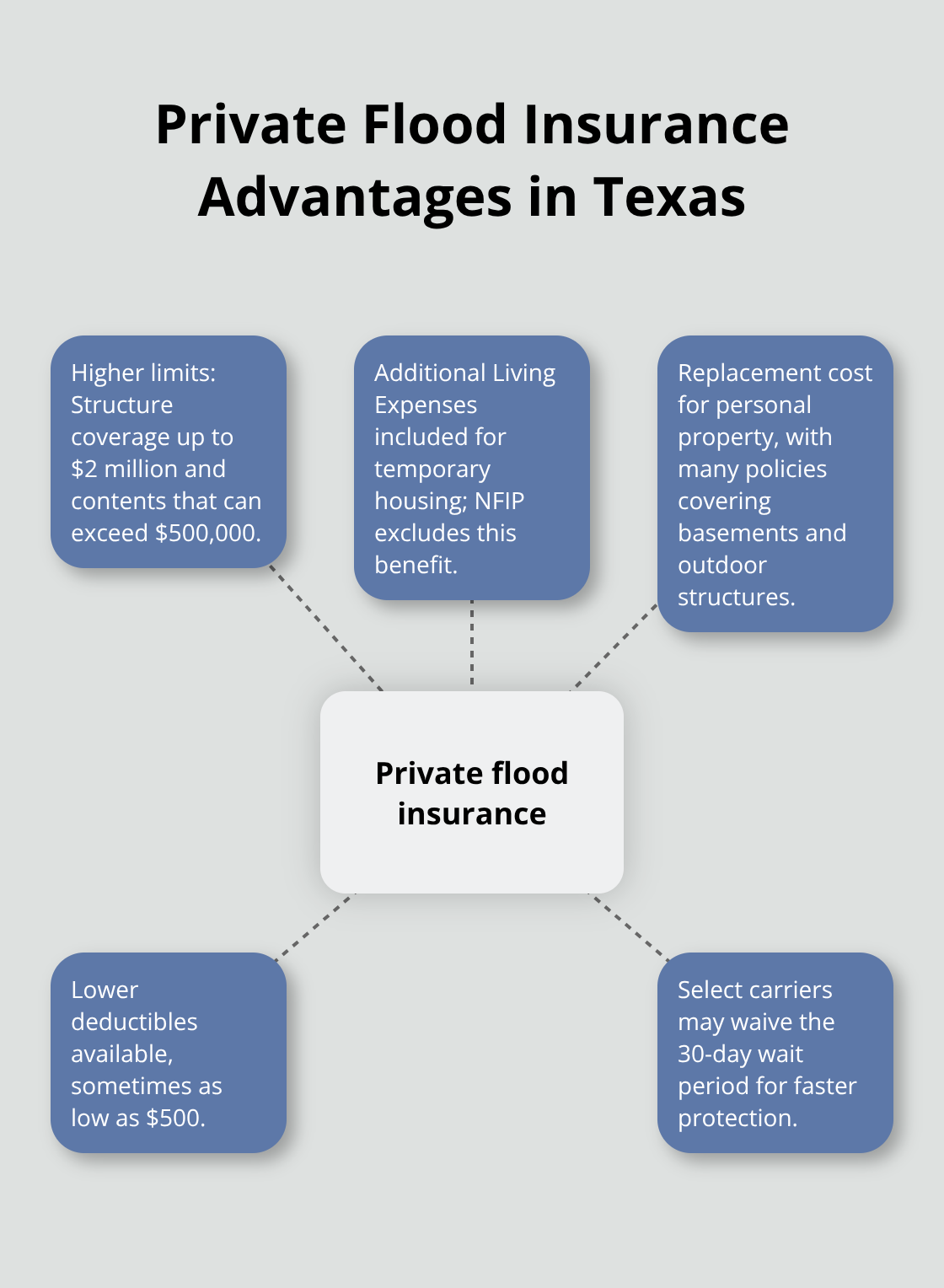

Private flood insurers provide structure coverage up to $2 million and contents coverage that exceeds $500,000 in many cases. These policies include Additional Living Expenses for temporary housing, which NFIP excludes completely. Private insurers offer replacement cost coverage for personal property instead of actual cash value, and many policies cover basement improvements and outdoor structures. Deductibles can be as low as $500, and some carriers waive the 30-day wait period for immediate coverage needs.

Coverage Exclusions Apply Universally

Both NFIP and private policies exclude damage from earth movement, power outages, currency and precious metals, and vehicles. Neither option covers sewer backup unless water enters through recognized flood sources first. Swimming pools, hot tubs, and landscaping remain excluded under standard policies (though some private insurers offer endorsements for these items). These exclusions affect claim outcomes regardless of which coverage type you select.

The next step involves understanding how insurers calculate your premiums and what factors influence your annual flood insurance costs in Texas.

How Much Will Your Texas Flood Insurance Cost?

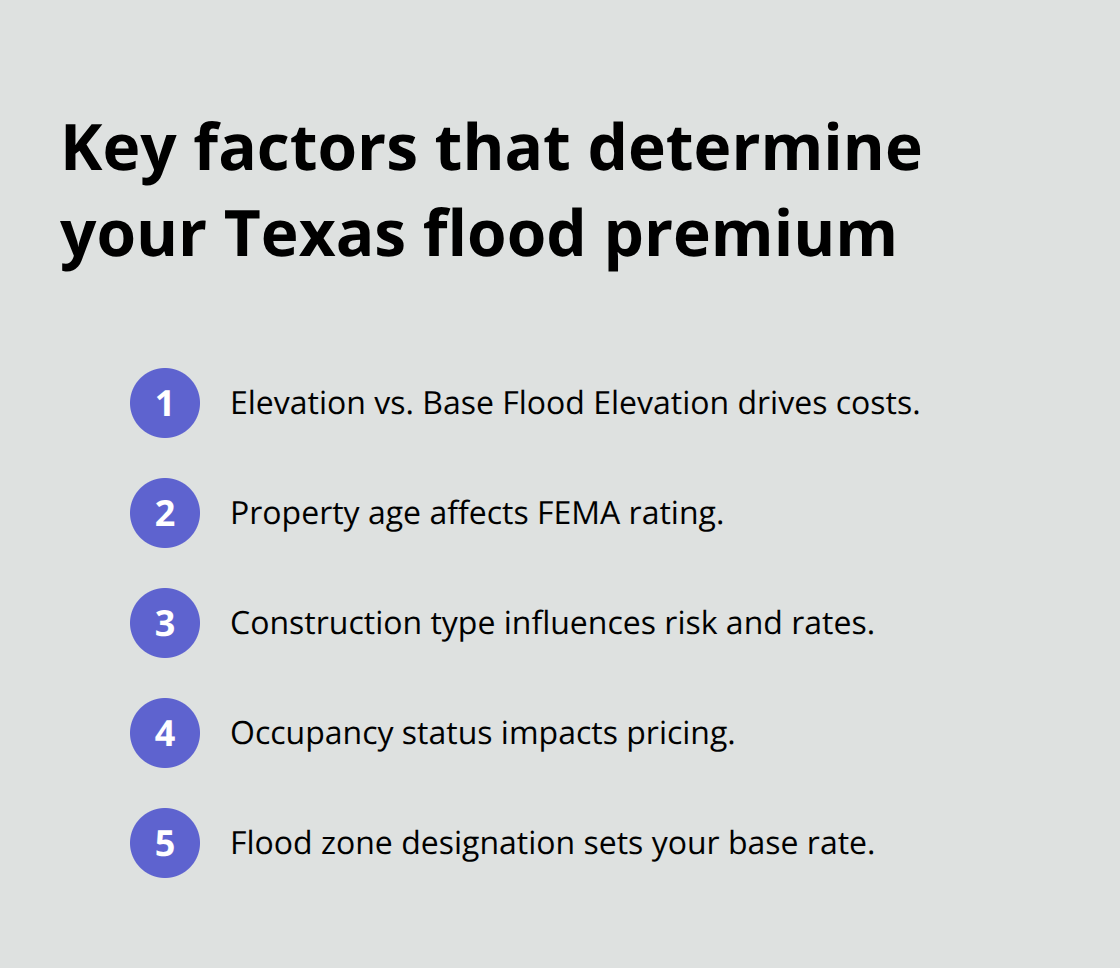

Flood insurance premiums in Texas depend on five primary factors that insurers analyze when they calculate your annual rate. Your property’s elevation certificate determines the most significant cost component, as homes below Base Flood Elevation pay substantially higher premiums than elevated structures. FEMA uses your property’s age, construction type, and occupancy status alongside flood zone designation to establish base rates.

The average Texas homeowner pays $783 annually for NFIP coverage, but costs range from $531 in Hidalgo County to $992 in Galveston County based on local flood frequency and severity data.

Premium Reduction Through Property Modifications

Property owners who elevate utilities above potential flood levels reduce premiums by 10-25% (depending on your flood zone classification). Homeowners who install flood vents in enclosed areas below the lowest floor qualify properties for substantial discounts under FEMA guidelines. Updated elevation certificates after home improvements help many property owners reduce their annual costs by $200-400 through documented modifications. Community Rating System participation offers additional savings through premium discounts for policyholders in communities that implement proactive flood mitigation measures.

Smart Comparison Strategies Beat Standard Rates

Private insurers consistently offer lower rates for properties in moderate-risk zones, with savings that average 15-30% compared to NFIP policies. Property owners should request quotes from both NFIP agents and private carriers within 60 days of their renewal date to capture the best available rates. Texas residents should compare actual cash value versus replacement cost coverage options, as the premium difference often justifies the enhanced protection. Multi-policy discounts through your current homeowners carrier frequently produce unexpected savings that offset higher base flood insurance rates (especially when you bundle multiple policies with the same company).

Geographic Rate Variations Across Texas

Counties across Texas show dramatic premium differences based on historical flood patterns and risk assessments. Bexar County residents pay an average of $794 annually, while Montgomery County averages $692 per year. These variations reflect local flood frequency, drainage infrastructure quality, and proximity to major water sources. Properties near the Gulf Coast face higher premiums due to hurricane surge risks, while inland areas benefit from lower base rates despite Flash Flood Alley concerns.

Final Thoughts

Texas property owners face complex flood insurance decisions that directly impact their financial security during natural disasters. The state’s diverse geography creates different risk levels, from Gulf Coast hurricane zones to Flash Flood Alley in Central Texas. Property owners who understand mandatory coverage requirements, compare NFIP versus private insurance options, and implement cost-reduction strategies through property modifications can save thousands annually while they maintain adequate protection.

Proper flood protection starts when you assess your property’s specific risk through FEMA flood maps and elevation certificates. You should request quotes from both federal and private insurers within 60 days of your renewal date to capture the best available rates. Property modifications like elevated utilities and flood vents reduce premiums while they improve your home’s flood resistance (and provide long-term value for your investment).

Professional guidance makes the difference between adequate coverage and costly gaps in protection. We at Brooks Insurance represent multiple insurance companies and provide you access to comprehensive flood insurance in Texas options with competitive rates. Our licensed agents help you navigate complex coverage decisions and find the right protection for your specific situation.