Your business vehicles are on the road every day. Without proper commercial auto insurance for small business, one accident could drain your finances and expose you to serious legal liability.

At Brooks Insurance, we help Texas small business owners understand what coverage they actually need. This guide walks you through the types of protection available, how to cut costs without sacrificing coverage, and why working with an independent agent makes a real difference.

Why Your Small Business Needs Commercial Auto Insurance

Texas has over 3 million small businesses, and most operate vehicles for daily operations. Personal auto insurance simply will not cover business use, which means your business faces massive exposure without proper commercial auto coverage. One accident involving a company vehicle can trigger lawsuits, medical claims, and property damage bills that exceed $100,000. Many business owners discover their personal policy excludes work-related driving only after an accident occurs. The Texas minimum liability requirement of 30/60/25 ($30,000 bodily injury per person, $60,000 per accident, $25,000 property damage) exists precisely because accidents happen, and without coverage, small businesses collapse under the financial weight.

State Law Mandates Coverage for Business Vehicles

Texas law requires commercial auto liability coverage for any vehicle used for business purposes. Operating without it exposes your business to fines, license suspension, and personal liability that pierces your business structure. If your employee causes an accident while making a client delivery, your business becomes responsible for damages. Your personal assets become fair game in lawsuits. The minimum limits sound adequate until you calculate actual accident costs: a serious injury claim easily reaches $150,000 to $500,000, far exceeding the state minimum. Higher limits protect your business assets and provide the cushion you need when accidents occur. Many industries face even greater risk exposure based on vehicle type and operations.

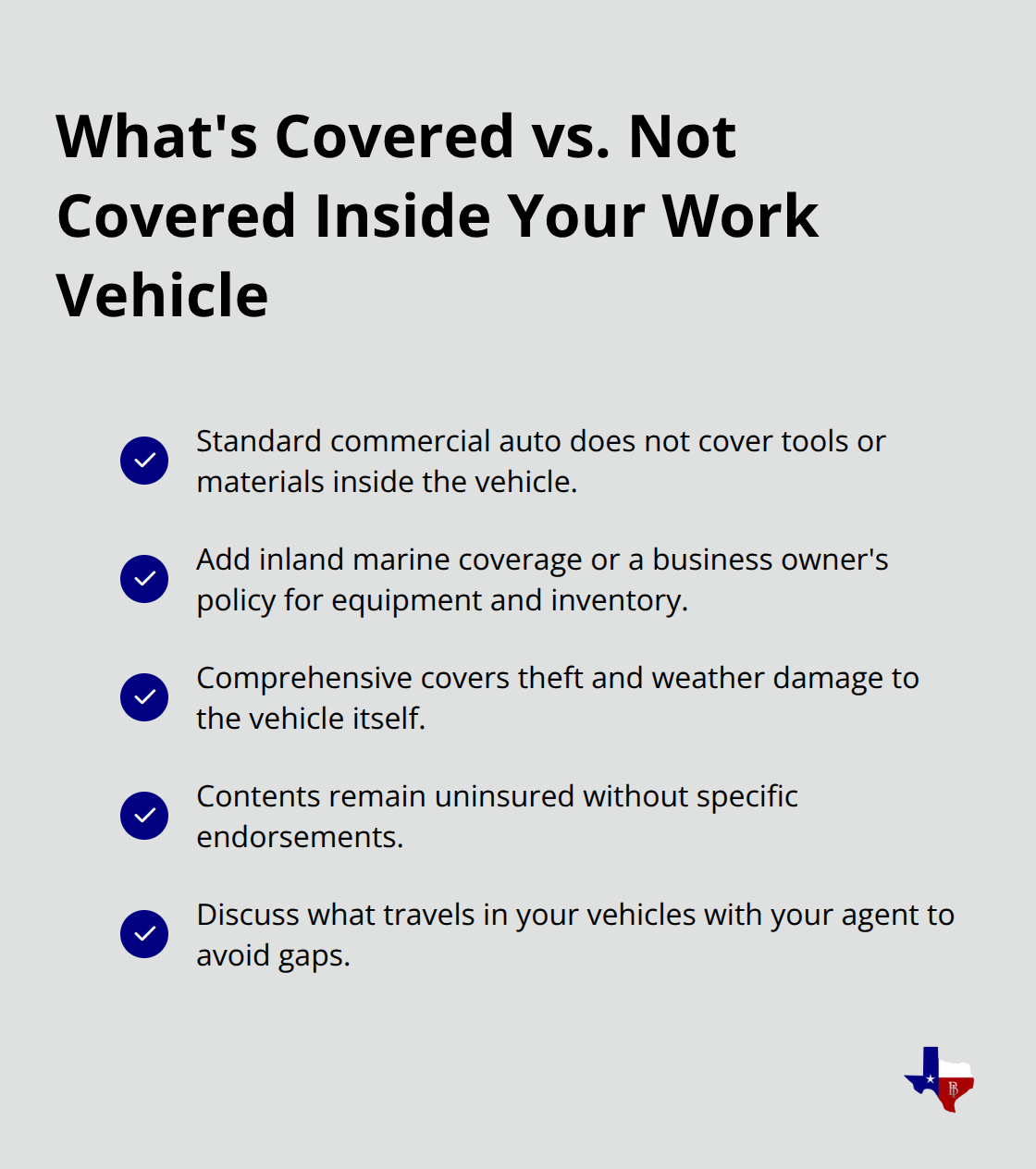

Equipment and Tools Require Separate Protection

Your work vehicle likely carries valuable equipment, tools, or inventory inside. Standard commercial auto policies do not cover tools and materials stored in the vehicle.

A box truck carrying contractor equipment worth $15,000 remains unprotected unless you add inland marine coverage or a business owner’s policy. This gap catches business owners off guard after theft or damage. Comprehensive coverage handles theft and weather damage to the vehicle itself, but the contents remain uninsured. You must specifically discuss what travels inside your vehicles with your agent to avoid discovering coverage gaps after a loss.

Medical Expenses Coverage Protects Your Team

Medical payments coverage protects your employees and passengers if someone gets injured during a work-related accident. This coverage pays medical expenses regardless of fault, which means your team receives treatment without delay. When an accident happens, your employees need immediate medical attention-not a lengthy dispute over who caused the crash. Medical payments coverage removes that barrier and demonstrates to your team that you prioritize their safety and wellbeing. Understanding these protection layers helps you move forward with confidence toward selecting the right coverage options for your specific business needs.

Types of Commercial Auto Coverage for Small Businesses

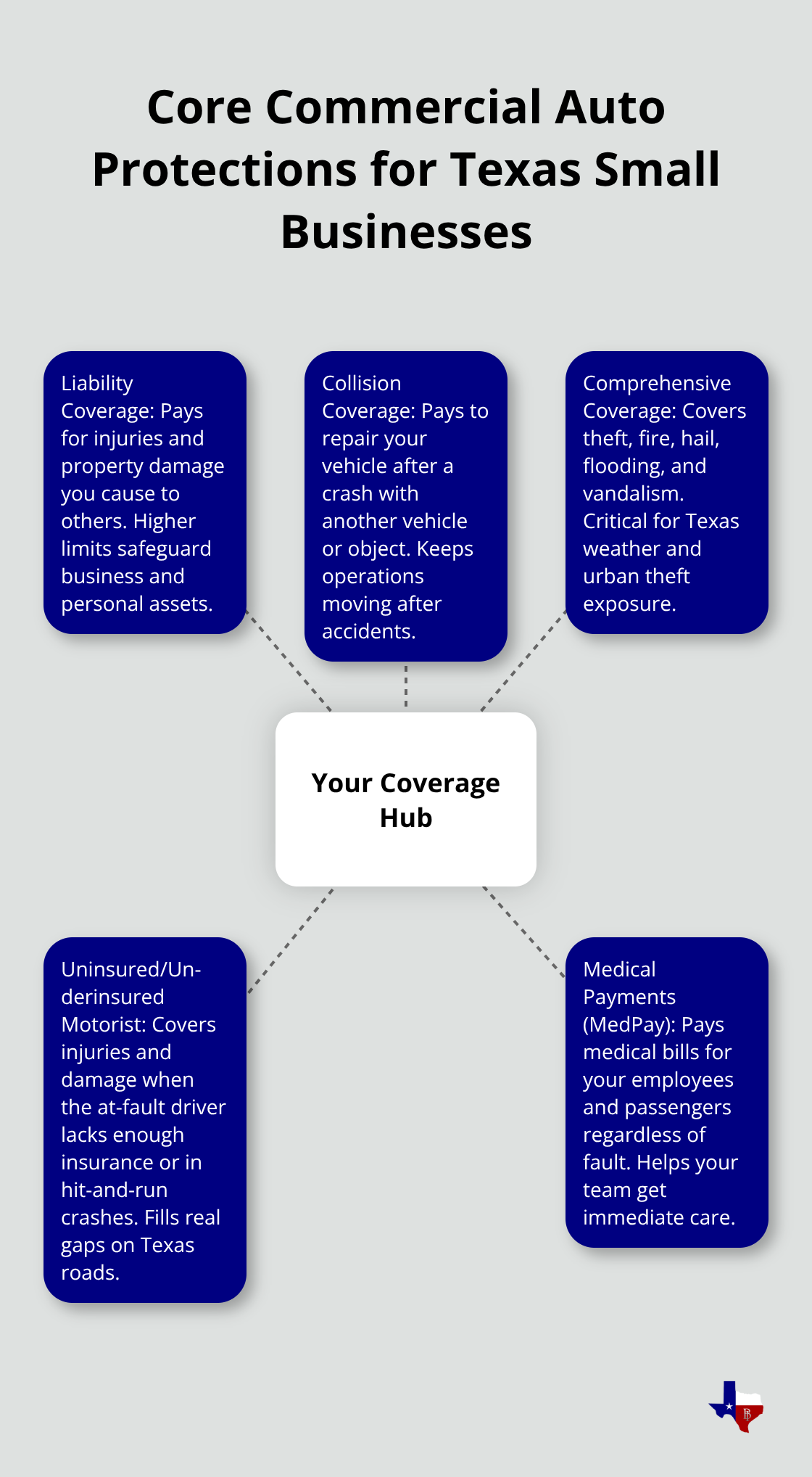

Liability Coverage Forms Your Foundation

Liability coverage forms the foundation of commercial auto insurance, and Texas law requires it for good reason. This coverage pays for bodily injury and property damage your business causes to other people and their property when your company vehicle is involved in an accident. The state minimum of 30/60/25 means $30,000 per person and $60,000 per accident for injuries, plus $25,000 for property damage.

However, these minimums are dangerously low for most small businesses. A single serious injury claim easily exceeds $150,000, which means the state minimum leaves your business vulnerable to lawsuits that drain your personal assets. Higher limits based on your actual operations and vehicle types protect your business from catastrophic losses. If your company vehicle regularly carries valuable equipment or operates in high-traffic areas, limits of at least 100/300/100 shield your business from devastating financial exposure.

Collision and Comprehensive Coverage Keep Operations Running

Collision coverage handles damage to your own vehicles when they hit another car or object, while comprehensive coverage protects against theft, fire, weather damage, and vandalism. These two coverages work together to keep your vehicles operational after accidents or incidents. Comprehensive coverage proves especially important in Texas given the state’s exposure to hail, flooding, and theft in urban areas like Houston and Dallas. Weather events and vehicle theft occur regularly across Texas, and comprehensive coverage restores your ability to serve clients without interruption. Collision coverage ensures that accidents with other vehicles do not sideline your business operations for weeks while repairs happen.

Uninsured Motorist Protection Covers Real Gaps

Uninsured and underinsured motorist coverage protects your business when another driver causes an accident but lacks sufficient insurance to cover damages. Texas does not require this coverage, yet it remains one of the smartest purchases for small business owners. Texas maintains a 14.5% uninsured motorist rate, with millions of uninsured vehicles operating on Texas roads. If an uninsured driver hits your company vehicle and injures your employee, your uninsured motorist coverage pays medical bills and vehicle repairs without relying on the other driver’s insurance. This coverage also applies to hit-and-run accidents where the other driver flees the scene. Many business owners skip this protection to save money, then face thousands in out-of-pocket expenses when accidents happen with uninsured drivers. The cost difference between policies with and without uninsured motorist protection is minimal, making the decision straightforward for smart business operators.

Now that you understand which coverage types protect your vehicles and team, the next step involves identifying which specific coverages fit your business operations and how to control costs without sacrificing protection.

How to Cut Your Commercial Auto Insurance Costs

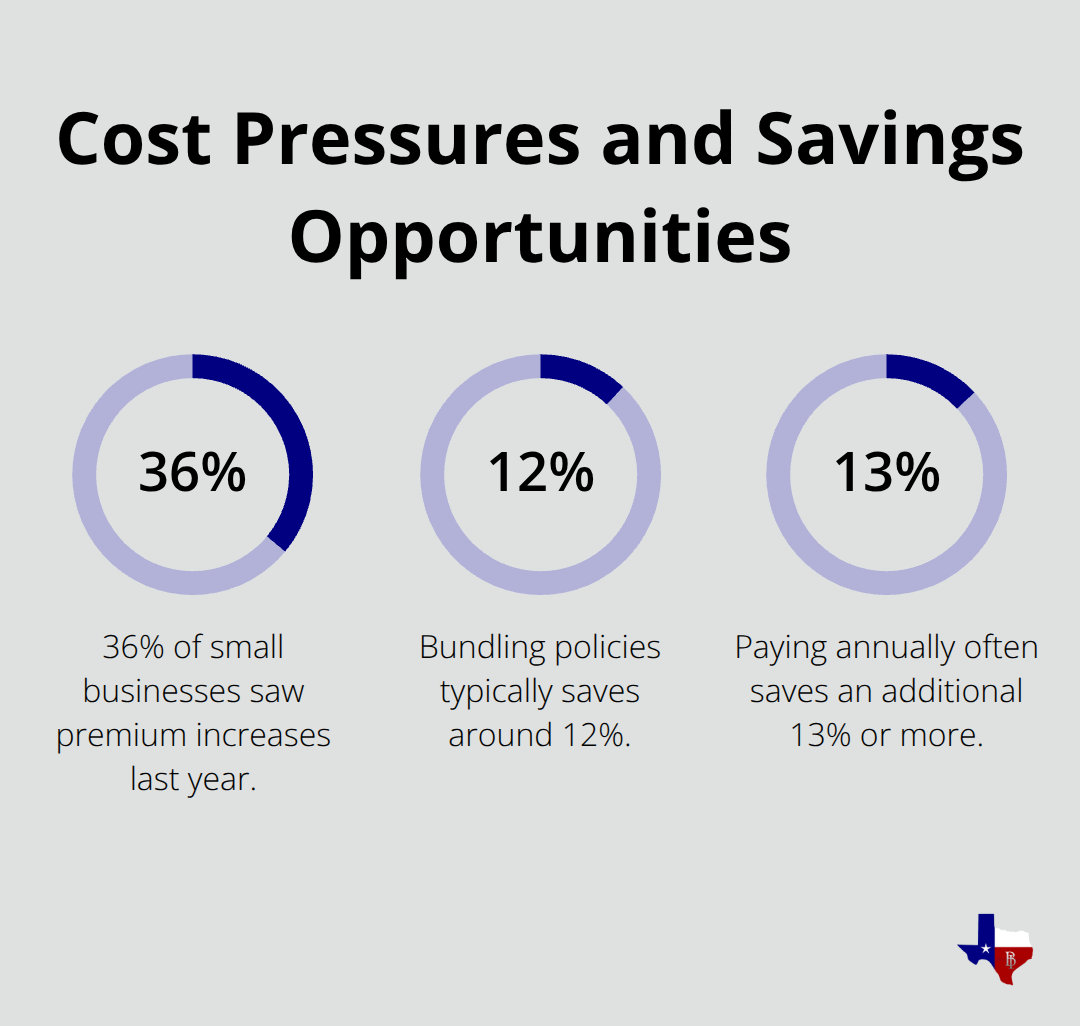

Reducing your commercial auto insurance premium does not mean accepting weaker coverage or gambling with your business protection. The J.D. Power 2024 U.S. Small Commercial Insurance Study found that 36% of small businesses experienced premium increases in the past year, making cost management a real priority for business owners. Most businesses overlook three concrete strategies that generate substantial savings without sacrificing protection.

Bundle Your Policies for Immediate Savings

Adding commercial auto coverage to an existing business owner’s policy, commercial property, or general liability policy generates bundling discounts that typically save around 12% on your auto insurance. If you carry multiple policies across different insurers, consolidating with one agent creates immediate savings. A contractor carrying a commercial auto policy with one insurer and a general liability policy with another leaves money on the table every month. Consolidating these policies with a single independent agency eliminates that waste and often reduces your total business insurance cost beyond the 12% baseline. Many small business owners assume they already bundle their coverage when they actually split policies across multiple insurers because they never asked an agent about consolidation.

Paying your entire annual premium upfront rather than monthly installments generates an additional 13% or more in savings with most carriers. For a business paying $2,000 annually in commercial auto premiums, bundling and annual payment combined could reduce your costs by $400 to $500 per year with no reduction in coverage limits or protection levels.

Align Your Coverage Limits with Actual Operations

Texas businesses commonly overpay for coverage that exceeds their actual risk exposure. A service business operating a single passenger van in Austin does not need the same liability limits as a contractor running a fleet of box trucks across multiple cities. Your vehicle types, where you operate, and what equipment travels in your vehicles determine the right coverage levels for your situation. An agent can right-size your coverage and eliminate unnecessary costs once you provide these details.

Increasing your collision and comprehensive deductibles from $500 to $1,000 lowers your premium significantly if your business maintains adequate cash reserves to cover that higher out-of-pocket amount during a claim. This strategy only works if your business can genuinely afford the higher deductible without financial strain. If your business operates primarily within a single city like Houston or San Antonio with lower travel radius exposure, your agent can adjust coverage to reflect that lower risk and reduce your rates accordingly. The opposite mistake happens when businesses purchase coverage designed for high-risk operations when their actual driving patterns are far less risky.

Match Vehicle Types to Coverage Needs

Different vehicles require different protection levels based on their use and value. A food truck carrying expensive equipment and inventory needs more comprehensive protection than a sales representative’s sedan. Your agent should understand exactly what each vehicle does, where it travels, and what it carries. This information allows your agent to recommend appropriate limits and coverages rather than applying a one-size-fits-all approach that wastes your money.

Final Thoughts

Commercial auto insurance for small business protects far more than just your vehicles-it protects your employees, your clients, your business assets, and your personal finances from the real consequences of accidents on Texas roads. Start by reviewing your current coverage with honest answers to three questions: What vehicles does your business operate? What do those vehicles carry? Where do they travel? Your answers determine whether your current limits and coverages actually match your real risk exposure.

The cost-saving strategies we discussed-bundling policies, adjusting deductibles, and aligning coverage to actual operations-generate real savings without gambling with your business protection. A 12% bundling discount combined with annual payment savings can reduce your annual premium by several hundred dollars while maintaining the protection your business needs. Many business owners discover they’re either overpaying for unnecessary protection or dangerously underinsured after reviewing these details with an agent.

Working with an independent agent makes this process straightforward. At Brooks Insurance, we represent multiple top-rated insurance companies, which means you get access to genuine options rather than being locked into one carrier’s offerings. Contact Brooks Insurance today to evaluate your current commercial auto insurance for small business and identify opportunities to strengthen your protection or reduce unnecessary costs.

Disclaimer: The information provided in this blog is for general informational purposes only and does not constitute legal, financial, or insurance advice. Coverage options, terms, and availability may vary. Please consult with a licensed professional for advice specific to your situation