Roofing contractors in Texas face real liability risks on every job site. One accident or property damage claim can cost thousands-or worse, put your business under.

At Brooks Insurance, we help roofing companies protect themselves with the right general liability coverage. This guide walks you through what you need to know to get properly protected.

What Roofing General Liability Insurance Actually Protects

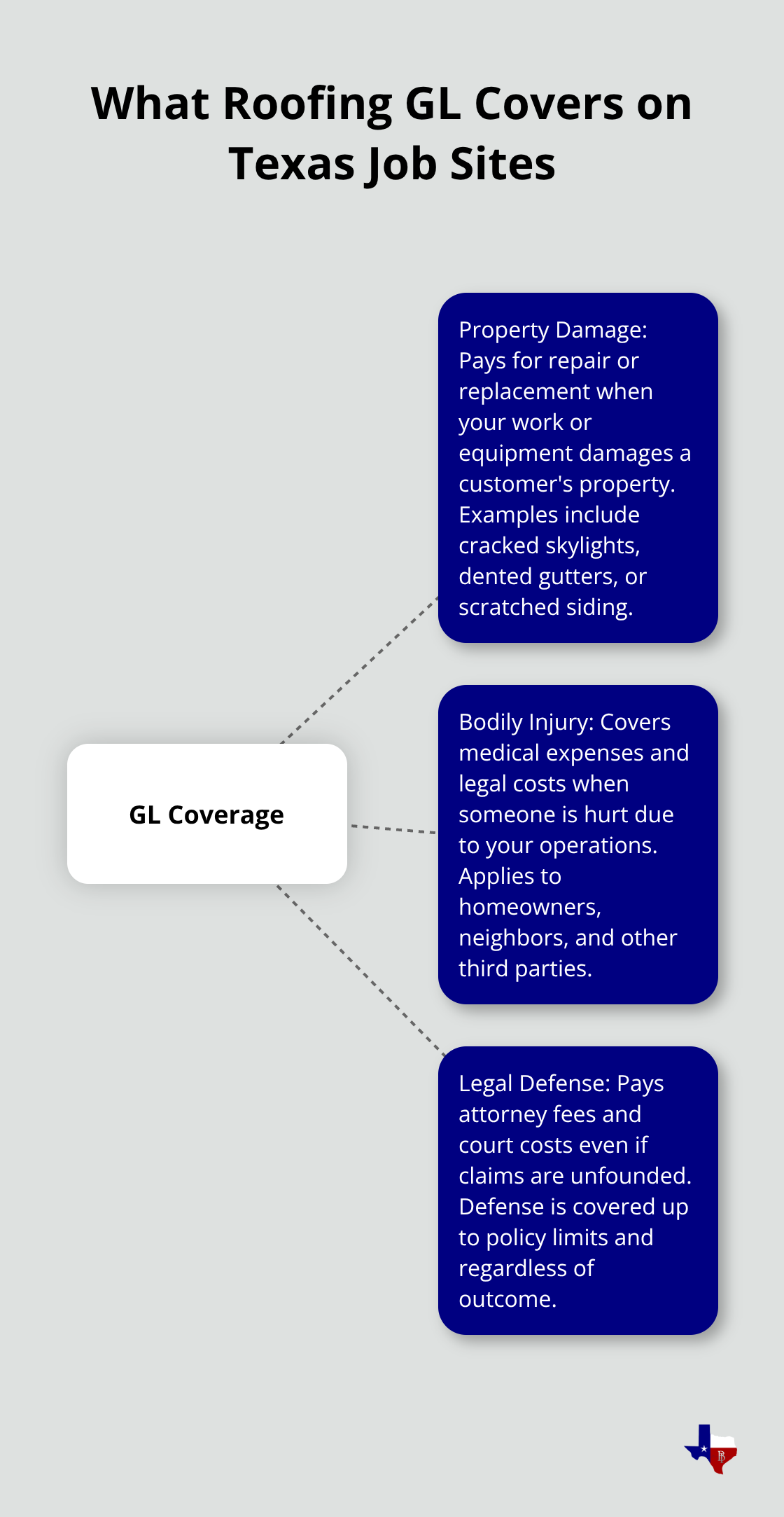

General liability insurance for roofing contractors covers three main categories of claims that show up regularly on Texas job sites. Property damage claims occur when your work or equipment damages a customer’s home or belongings. A falling roof tile that cracks a skylight, a ladder that dents guttering, or materials that scratch siding all trigger this coverage. The insurance pays for repairs or replacement up to your coverage limit. Bodily injury protection covers medical expenses and legal costs when someone gets hurt because of your work. A homeowner slipping on wet roofing materials or a neighbor hit by debris qualifies here. The policy also covers your legal defense costs, including attorney fees and court expenses, even if a claim turns out to be unfounded. This matters because defending yourself against a lawsuit costs money whether you win or lose.

The Real Limits You Actually Need

Most Texas roofers carry a minimum of $1,000,000 per occurrence and $2,000,000 aggregate coverage. Per occurrence means the policy pays up to $1 million for each separate incident. Aggregate means the policy pays a maximum of $2 million across all claims in one year. If you work on high-value homes or handle larger projects, these minimums might not be enough. A kitchen remodel that gets damaged during roofing work could easily exceed $100,000. Major contractors often require roofing subcontractors to carry these minimums before allowing them on job sites, which means you need this coverage to bid jobs competitively. When you request a quote, specify the types of projects you handle and the property values you typically work on so your coverage limits match your actual exposure.

What Gets Excluded From Coverage

Standard roofing general liability policies exclude certain work and situations. Open roof work exclusions prevent coverage when trusses or structural elements are exposed during installation or repair. Exclusions also apply to work involving heating equipment or heating processes. Buildings over three stories tall often face exclusions or require additional endorsements. High-risk property types like condos, churches, medical facilities, and large commercial buildings may be excluded from standard policies or require specialty coverage through excess and surplus markets. When you get a quote, ask specifically about these exclusions and whether any apply to your typical projects. If exclusions would prevent you from working on jobs you want, discuss endorsements or alternative coverage options with your agent before committing to a policy.

Moving Forward With Your Coverage Decision

Understanding what your policy covers and what it excludes puts you in position to make an informed choice about your protection level. The next step involves assessing how much coverage your specific business actually needs based on your project types and revenue.

Getting Your Roofing General Liability Quote

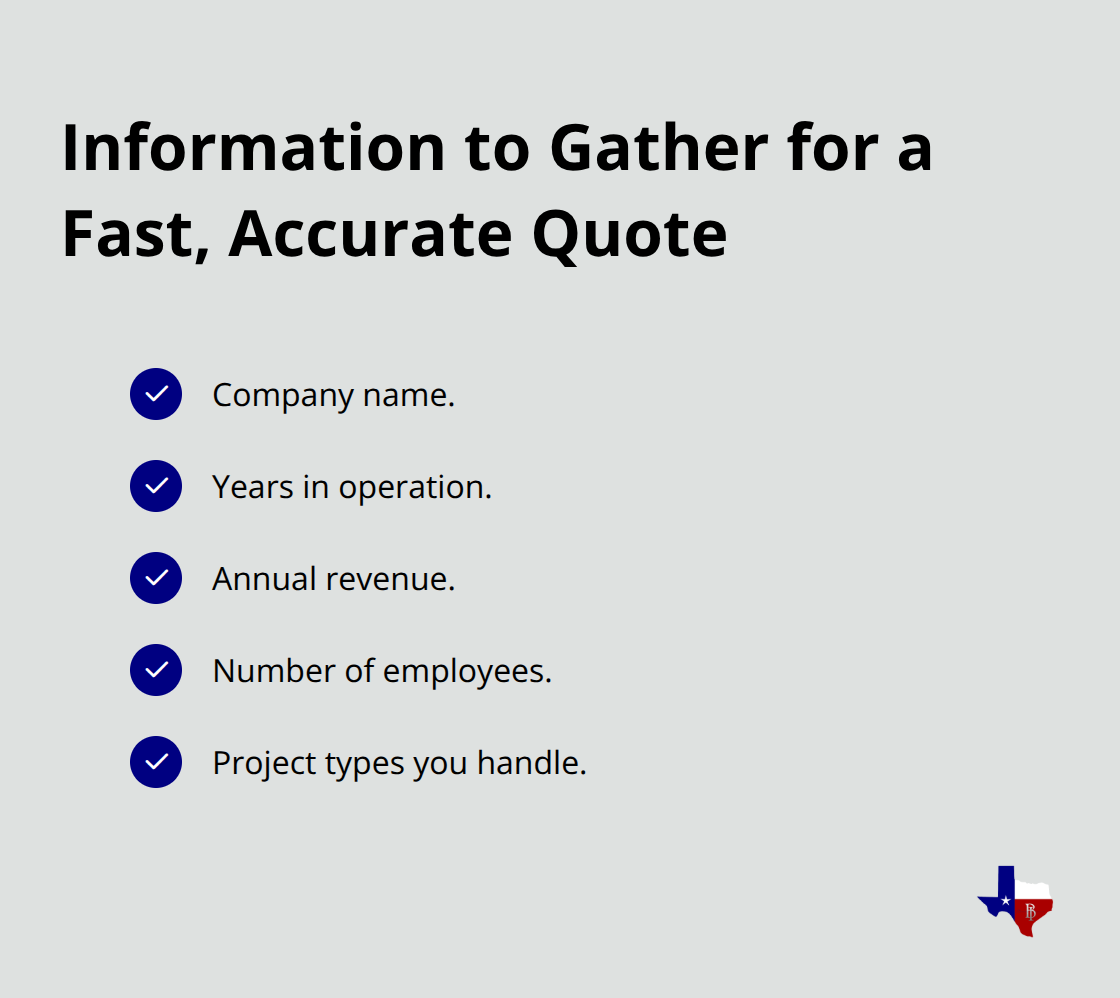

Roofing general liability quotes come together faster than most contractors expect, but accuracy in your application matters significantly. Gather basic information about your business before contacting insurers: company name, years in operation, annual revenue, number of employees, and project types you handle. Insurance companies assess your risk profile using this data.

When you reach out to an insurance provider, specify your work clearly. Describe whether you handle residential roofs, commercial buildings, steep-slope work, or a combination. Mention the property values you typically work on and whether you ever work on buildings over three stories tall, since these factors affect both pricing and exclusions. Most providers generate an initial quote within hours. The average roofing general liability policy in Texas costs around $2,800 per year, though this varies based on company size, claims history, and coverage limits. Premiums typically run 2 to 3 percent of your annual revenue, so a $500,000 revenue business might expect to pay $10,000 to $15,000 annually for a complete insurance package that includes general liability, workers compensation, and commercial auto.

Compare Multiple Quotes Side by Side

Contact at least three different insurance companies and compare their offers at identical coverage limits. Pricing varies significantly between carriers, and some specialize in roofing while others treat it as a secondary market. When comparing quotes, verify that each one includes the same per-occurrence and aggregate limits so you’re truly comparing apples to apples. This step prevents you from accidentally selecting cheaper coverage that provides less protection than you actually need.

Select Coverage Limits That Match Your Work

The $1,000,000 per occurrence and $2,000,000 aggregate baseline works for many roofing contractors, but your actual needs depend on your project scope. If you primarily handle residential roof replacements on homes valued under $300,000, these minimums provide adequate protection. However, if you work on commercial properties, high-end residential projects, or handle multiple jobs simultaneously, higher limits make sense. Major general contractors often require their roofing subcontractors to carry these minimums before allowing them on job sites, which means you need at least this much to stay competitive.

Evaluate Deductibles and Endorsements

When reviewing policy terms, check for deductible options. A higher deductible lowers your premium but increases your out-of-pocket cost when you file a claim. A $2,500 deductible typically costs less than a $1,000 deductible, but you need to decide what amount your business can actually afford to pay if something goes wrong. Ask your agent about endorsements that add coverage for the exclusions discussed earlier, like open roof work or buildings over three stories. These endorsements cost extra but eliminate coverage gaps.

Verify Coverage and Obtain Documentation

Once you’ve selected your limits and reviewed the exclusions, verify that the policy explicitly covers on-site property damage and third-party bodily injury claims arising from roofing operations. Request a Certificate of Insurance once your policy is active so you have documentation ready for clients and general contractors who require proof before you start work. This certificate provides a one-page summary of your policy number, coverage, limits, and policy dates-exactly what most clients need to see before you arrive on their job site.

With your coverage limits selected and your policy details confirmed, the next step involves understanding the actual costs involved and what factors influence your premiums.

What Actually Drives Your Roofing Insurance Cost

Your insurance premium isn’t random. It reflects exactly how much risk you represent to the insurance company, and Texas roofing contractors have significant control over several cost factors. Years in business matter tremendously. A roofing contractor with ten years of operation and a clean claims history pays substantially less than someone starting their first year. Insurance companies view experience as proof you know how to manage risk on job sites. Your safety record directly influences your rate because claims history shows whether accidents actually happen under your management. A contractor who has filed three claims in five years will pay more than an identical business with zero claims. When you apply for coverage, be honest about your claims history because insurers verify this information anyway, and hiding claims creates problems later when they discover the truth during underwriting. The specific coverage limits you select also shift your premium significantly. Coverage limits, such as $2 million in general liability, increase costs compared to lower limits because the insurance company faces greater exposure. Your deductible works the same way. Choosing a higher deductible instead of a lower one lowers your annual premium noticeably because you accept more financial responsibility when claims occur. The tradeoff requires honest assessment of what your business can actually afford to pay out of pocket if something goes wrong.

Finding the Right Deductible for Your Situation

Don’t automatically choose the lowest deductible just because you want maximum protection. A lower deductible might cost more annually while a higher deductible costs less for identical coverage limits. That savings can be significant over time. If your business has healthy cash reserves and you rarely file claims, the higher deductible saves money over time. However, if you operate with tight margins and a single claim would strain your finances, the lower deductible provides peace of mind that justifies the extra cost. The math changes based on your specific situation, so calculate both scenarios before deciding. Some Texas roofing contractors intentionally choose higher deductibles to lower their annual premiums, then set aside the deductible amount in a separate business account. This approach reduces your insurance costs while guaranteeing you can cover your deductible if needed. Talk with your insurance agent to confirm this strategy makes sense for your operation.

The Real Value of Safety Programs and Training

Insurance companies offer premium discounts to contractors who complete safety training or implement documented safety programs on job sites. These discounts typically range from five to fifteen percent (depending on the insurer and the specific program). OSHA-related training, fall protection certification, and documented safety protocols all qualify for consideration.

The investment in safety training costs money upfront, but a discount on your annual premium saves money yearly. Over a multi-year policy period, those savings can cover the cost of most safety training programs. Beyond the financial savings, contractors with strong safety records experience fewer actual claims, which keeps future premiums lower. This creates a compounding benefit where safety investments pay dividends year after year through reduced premiums and fewer interruptions from claims handling.

Final Thoughts

Roofing general liability insurance protects your Texas business from the financial devastation that follows a single accident or property damage claim. Your claims history and years in business shape your premiums more than anything else, which means your best long-term strategy involves investing in documented safety programs that reduce claims while simultaneously lowering your insurance costs. The five to fifteen percent discounts available through safety initiatives pay for themselves through annual premium savings.

Working with an insurance professional makes this process faster and more accurate than trying to navigate coverage options alone. At Brooks Insurance, our licensed agents understand Texas roofing operations and the specific risks you face on job sites, and we represent multiple top-rated insurance companies so you access a larger selection of coverage options and competitive pricing. Our team helps you identify coverage gaps, understand exclusions that might affect your work, and select limits that actually match your project scope and revenue.

Contact Brooks Insurance with your basic business information and project details, and our agents will generate quotes from multiple carriers and walk you through the options so you understand exactly what you’re buying. Roofing general liability insurance takes hours to secure, not weeks, and the protection it provides is worth far more than the annual premium you’ll pay.

Disclaimer: The information provided in this blog is for general informational purposes only and does not constitute legal, financial, or insurance advice. Coverage options, terms, and availability may vary. Please consult with a licensed professional for advice specific to your situation