Your business is growing, and so are your transportation needs. A personal auto policy won’t cut it anymore-you need a small business auto policy designed for commercial use.

At Brooks Insurance, we help Texas business owners find coverage that matches their fleet size and operational demands. The right policy protects your vehicles, your drivers, and your bottom line.

Why Personal Auto Policies Leave Your Business Exposed

Personal Policies Exclude Business Use

Personal auto policies explicitly exclude business use, which means your insurer will not cover accidents that occur while you conduct company business. Most personal policies deny claims outright if a vehicle transports goods, makes deliveries, or carries clients. We at Brooks Insurance have seen too many business owners face this exclusion after an accident leaves them personally liable for thousands in damages. Texas law requires commercial vehicles to carry specific liability coverage, and operating a business vehicle on a personal policy violates that requirement. If authorities catch you without proper coverage, you face fines from the Texas Department of Insurance, potential license suspension, and civil liability for any injuries or property damage you cause.

Minimum Coverage Requirements in Texas

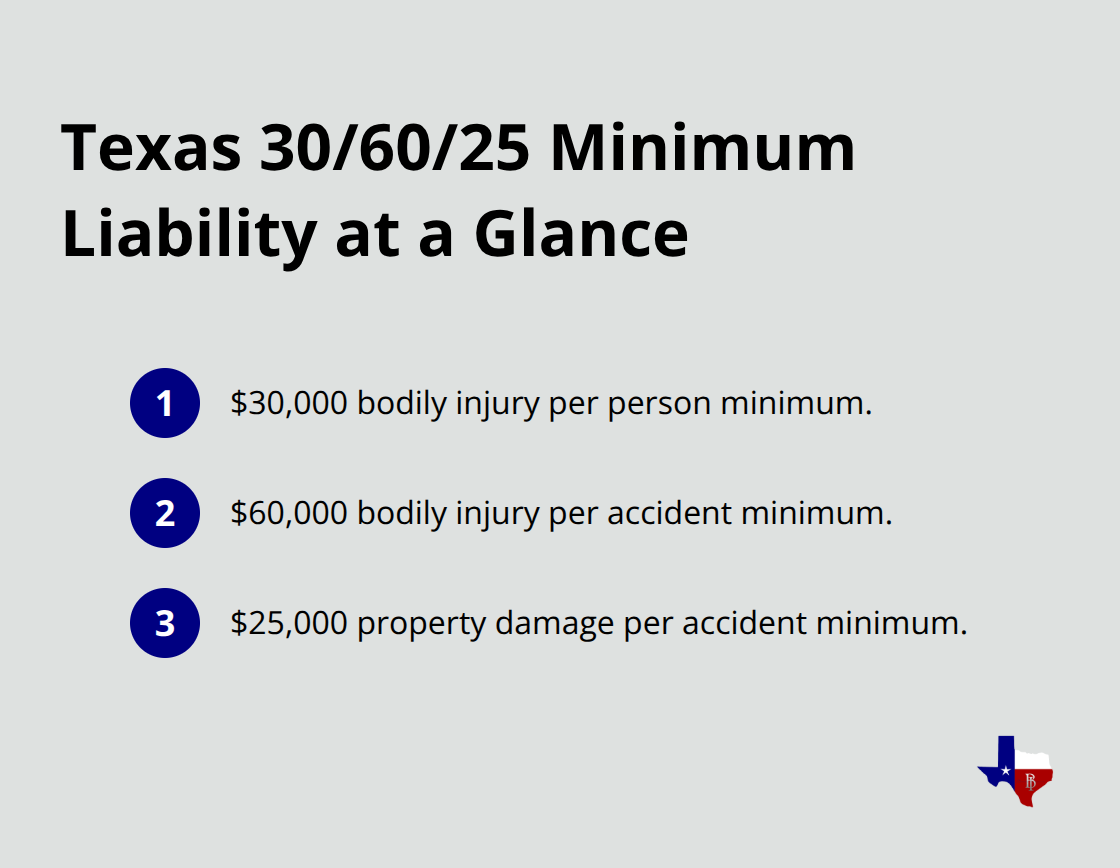

The minimum liability limits in Texas are 30 per person and 60 per accident for bodily injury, plus 25 for property damage.

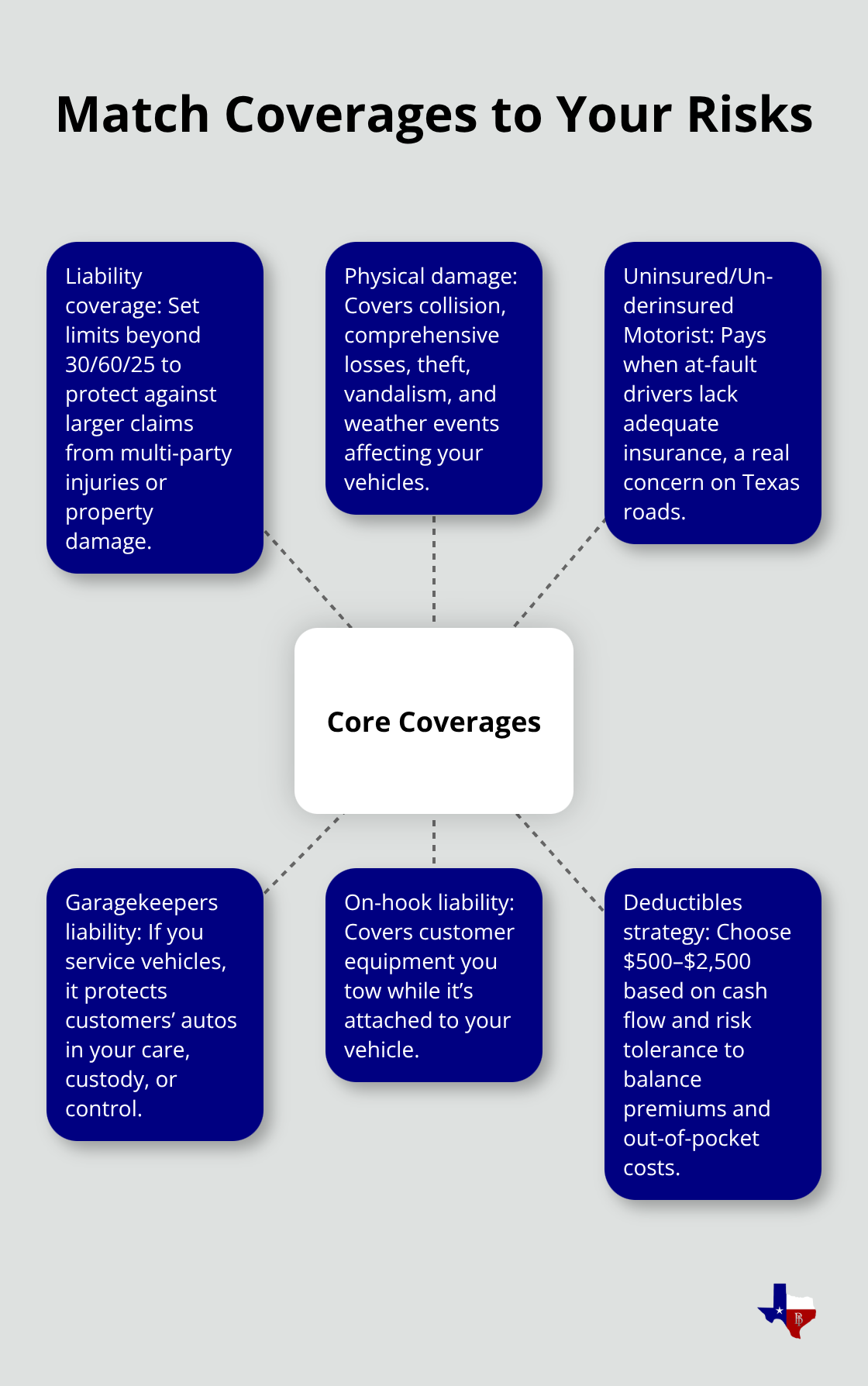

These minimums apply only if you carry the right policy type. A commercial auto policies covers bodily injury and property damage liability when your vehicle injures someone or damages their property during business operations. Physical damage coverage protects your own vehicles against collision, comprehensive losses, and weather damage. Uninsured and underinsured motorist coverage safeguards your drivers if they are hit by someone without adequate insurance-a real risk in Texas, where roughly 15% of drivers remain uninsured according to Texas Department of Insurance data.

Scaling Coverage for Your Fleet

If you operate multiple vehicles, commercial auto policies scale to your fleet size and allow you to add coverage for specific business risks. Garagekeepers liability applies if you service vehicles, while on-hook liability covers customer equipment you tow. The cost difference between operating without proper coverage and paying for a business policy proves stark: one serious accident on a personal policy can bankrupt a growing company, while a commercial policy costs a fraction of that potential loss. Commercial auto policies protect your business in ways personal policies simply cannot.

Essential Coverage for Your Growing Fleet

Liability Coverage Forms Your Foundation

Liability coverage forms the foundation of any commercial auto policy, and in Texas, the 30/60/25 minimums barely scratch the surface for most growing businesses. These limits mean $30,000 per person and $60,000 per accident for bodily injury, plus $25,000 for property damage-numbers that evaporate quickly when a serious accident occurs. We recommend moving beyond minimums to combined single limits of at least $500,000 or $1 million, depending on your industry and vehicle types. Food trucks, landscaping services, and contractor vans face higher exposure because they operate near customers, equipment, and pedestrians daily. A single accident involving a delivery vehicle that injures multiple people or damages commercial property can exceed minimums by tenfold. Texas data shows that larger settlements in urban areas like Dallas and Houston routinely exceed the state minimums, making higher limits a practical necessity rather than optional protection.

Physical Damage Coverage Protects Your Assets

Physical damage coverage protects the vehicles themselves against collision, theft, vandalism, and weather events-risks that matter more as your fleet grows. Deductibles of $500 or $1,000 balance affordability with meaningful protection, though businesses with older vehicles sometimes accept $2,500 deductibles to lower premiums. This coverage applies to vehicles you own outright or finance, and it covers repair or replacement costs after a covered loss. Weather events (hail, flooding, wind) and theft represent significant risks in Texas, particularly in areas prone to severe storms or high-crime zones. Selecting the right deductible depends on your cash flow and risk tolerance-lower deductibles cost more upfront but reduce out-of-pocket expenses after a loss.

Uninsured and Underinsured Motorist Protection Fills Critical Gaps

Uninsured and underinsured motorist coverage shields your drivers when at-fault third parties lack adequate insurance, a genuine concern given that approximately 12% of Texas car owners are uninsured. This coverage pays medical expenses, lost wages, and pain and suffering for your drivers-protection your personal policy never offered. If a driver works in a high-traffic area, underinsured motorist coverage becomes even more valuable because it covers the gap when someone carries only minimum liability limits. Growing businesses with multiple vehicles should confirm that underinsured motorist coverage applies per vehicle rather than per accident, maximizing protection across your fleet. Texas law requires you to offer this coverage unless you reject it in writing, making it an important decision point when you structure your policy.

Additional Coverages Match Your Business Risks

Garagekeepers liability applies if you service vehicles, while on-hook liability covers customer equipment you tow. These specialized endorsements address specific operational risks that standard commercial auto policies do not cover. The cost difference between operating without proper coverage and paying for a business policy proves stark: one serious accident on a personal policy can bankrupt a growing company, while a commercial policy costs a fraction of that potential loss. As your fleet expands and your operations become more complex, your coverage needs shift-what protects a single service van differs significantly from what protects a five-vehicle contractor fleet.

Understanding which additional coverages match your specific business activities helps you avoid gaps that could expose your company to unexpected liability.

Choosing Coverage That Actually Fits Your Operations

Match Fleet Size to Your Real Exposure

Fleet size determines everything about your commercial auto policy. Start by counting vehicles and categorizing them by function. A food truck operation runs different risks than a contractor fleet, which runs different risks than a delivery service. Document what each vehicle does: Does it carry equipment worth thousands? Does it transport clients or just materials? Does it operate within a five-mile radius or across multiple counties?

Travel radius significantly affects your premium because local routes present lower risk than statewide operations. Once you know your fleet composition, you can stop guessing at coverage needs and instead match protection to actual exposure. Texas commercial auto policy pricing factors include the type of vehicle being insured. A contractor with three vans operating in Austin faces different pricing than the same contractor operating across Dallas, Houston, and San Antonio, even though the vehicles are identical. This specificity matters: vague descriptions lead to incorrect quotes and coverage gaps that appear only after an accident occurs.

Set Liability Limits Above Minimums

Coverage limits should reflect your actual liability exposure, not just Texas minimums. The 30/60/25 baseline protects almost nothing in real-world scenarios. A single accident involving a client vehicle or pedestrian in an urban area like Dallas or Houston routinely generates settlements exceeding $100,000, meaning minimums leave your business personally liable for the difference.

We recommend combined single limits of at least $500,000 for most growing businesses, with $1 million limits for operations involving multiple vehicles or high-value client interactions. Food trucks operating near pedestrians, landscaping services using heavy equipment, and contractor fleets working on active job sites should lean toward higher limits because their daily operations create genuine exposure.

Choose Deductibles That Match Your Cash Flow

Deductibles demand attention when you structure your policy. A $500 deductible costs more upfront but reduces your out-of-pocket expense after a collision, while a $2,500 deductible lowers premiums significantly if your business maintains a strong safety record. The right choice depends on your cash reserves and risk tolerance rather than on industry averages.

Leverage Multiline Discounts and Payment Options

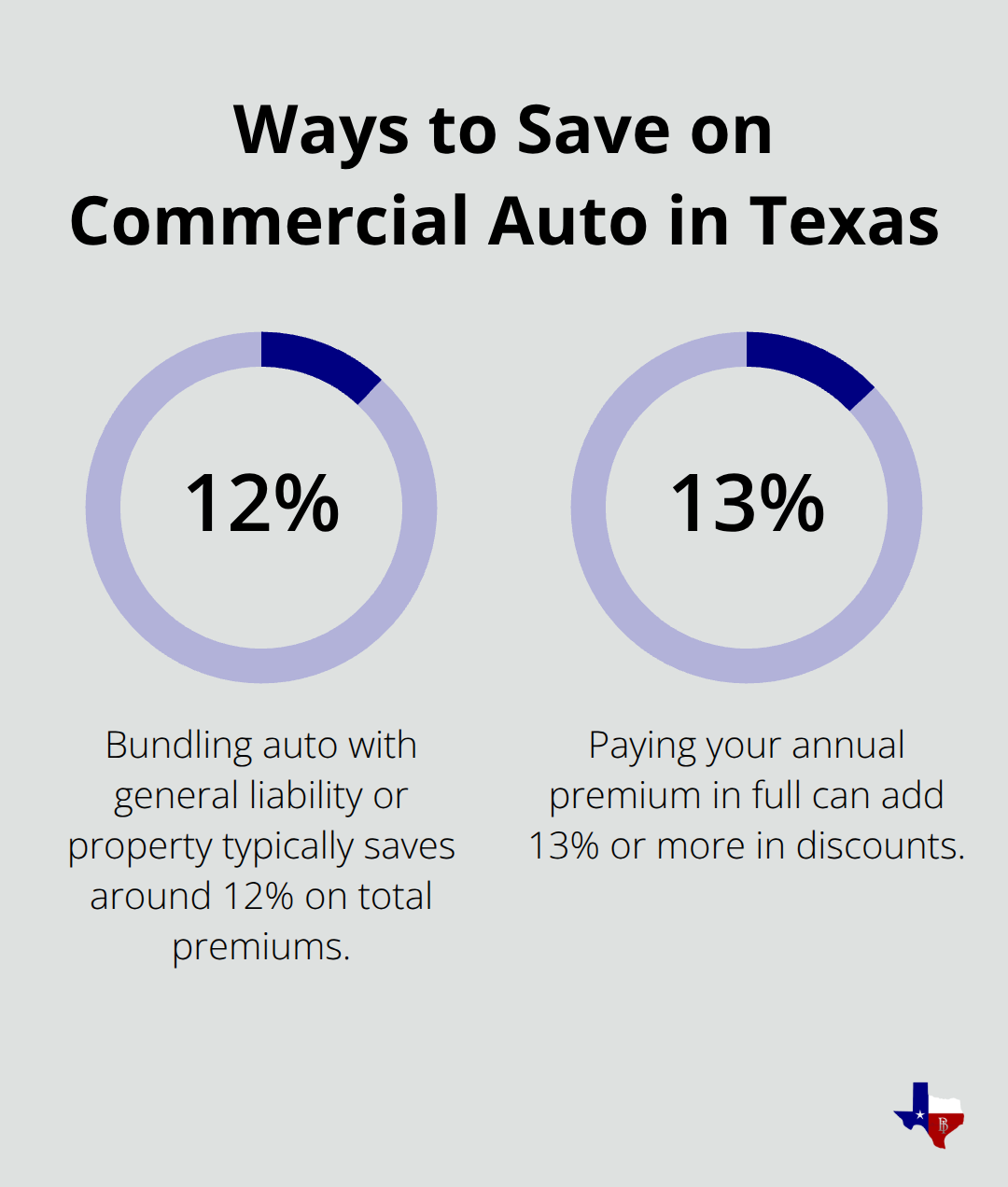

Bundling your commercial auto policy with other business coverages like general liability or property insurance typically saves around 12% on total premiums according to industry data. Paying your annual premium in full rather than monthly can yield additional discounts of 13% or more, helping growing businesses stretch insurance budgets further.

Work with an Independent Agent for Competitive Quotes

An independent agent who represents multiple insurers can compare quotes across carriers in minutes, revealing which companies price your specific operation most competitively rather than forcing you into one carrier’s standard rates. This approach uncovers savings and coverage options that single-carrier agents cannot match.

Final Thoughts

Small business auto insurance protects your growing company in ways personal policies never can. A small business auto policy covers your vehicles during business operations, meets Texas legal requirements, and shields your drivers and assets from real-world liability exposure. The right coverage transforms insurance from a compliance checkbox into genuine business protection that matches your fleet size and operational demands.

We at Brooks Insurance understand that growing businesses need flexibility and competitive pricing. As an independent agency, we represent multiple top-rated insurance companies, which means you access a larger selection of coverage options and pricing than single-carrier agents can offer. Our licensed agents compare quotes across carriers to find the most competitive rates for your specific operation, whether you operate a single service vehicle or a multi-vehicle fleet.

Contact us at brooksinstx.com to request a quote tailored to your fleet size, vehicle types, and operational needs. Our agents answer questions about coverage limits, deductibles, and multiline discounts that could lower your total insurance costs. We’re just a phone call or email away whenever you need clarification about your policy or want to adjust coverage as your business expands.

Disclaimer: The information provided in this blog is for general informational purposes only and does not constitute legal, financial, or insurance advice. Coverage options, terms, and availability may vary. Please consult with a licensed professional for advice specific to your situation