General liability insurance protects your small business from costly lawsuits and medical claims. But understanding small business general liability insurance costs can feel overwhelming when you’re juggling a dozen other priorities.

We at Brooks Insurance help Texas business owners find coverage that fits their budget and protects what they’ve built. This guide breaks down exactly what you’ll pay and how to reduce those premiums.

What Drives Your General Liability Insurance Premium

Industry Type Sets Your Cost Foundation

Your industry type is the single biggest factor determining what you’ll pay for general liability coverage, and it’s not close. Construction contractors in Texas typically pay $1,200–$3,500 annually, while consultants working from home might pay just $480–$720. According to Simply Business data from mid-2024, premiums vary dramatically by risk level. Roofers face $1,500–$4,500 per year, electricians $1,000–$2,500, and painters $800–$1,800. Coffee shops and restaurants run $1,200–$2,000 annually because food service involves higher exposure to customer injuries and property damage. Photographers and graphic designers pay $500–$900 because their risk profile differs fundamentally.

Revenue and Business Size Matter More Than Structure

Your actual revenue and business size matter more than your business structure. An LLC doesn’t automatically lower your premium-what matters is how much money flows through your business and how many employees you have. A home-based consultant earning $50,000 annually pays substantially less than a retail store doing $500,000 in revenue. Texas small businesses with one to four employees typically pay around $69 per month for standard $1 million per occurrence coverage, but this assumes low-risk operations with clean claims histories.

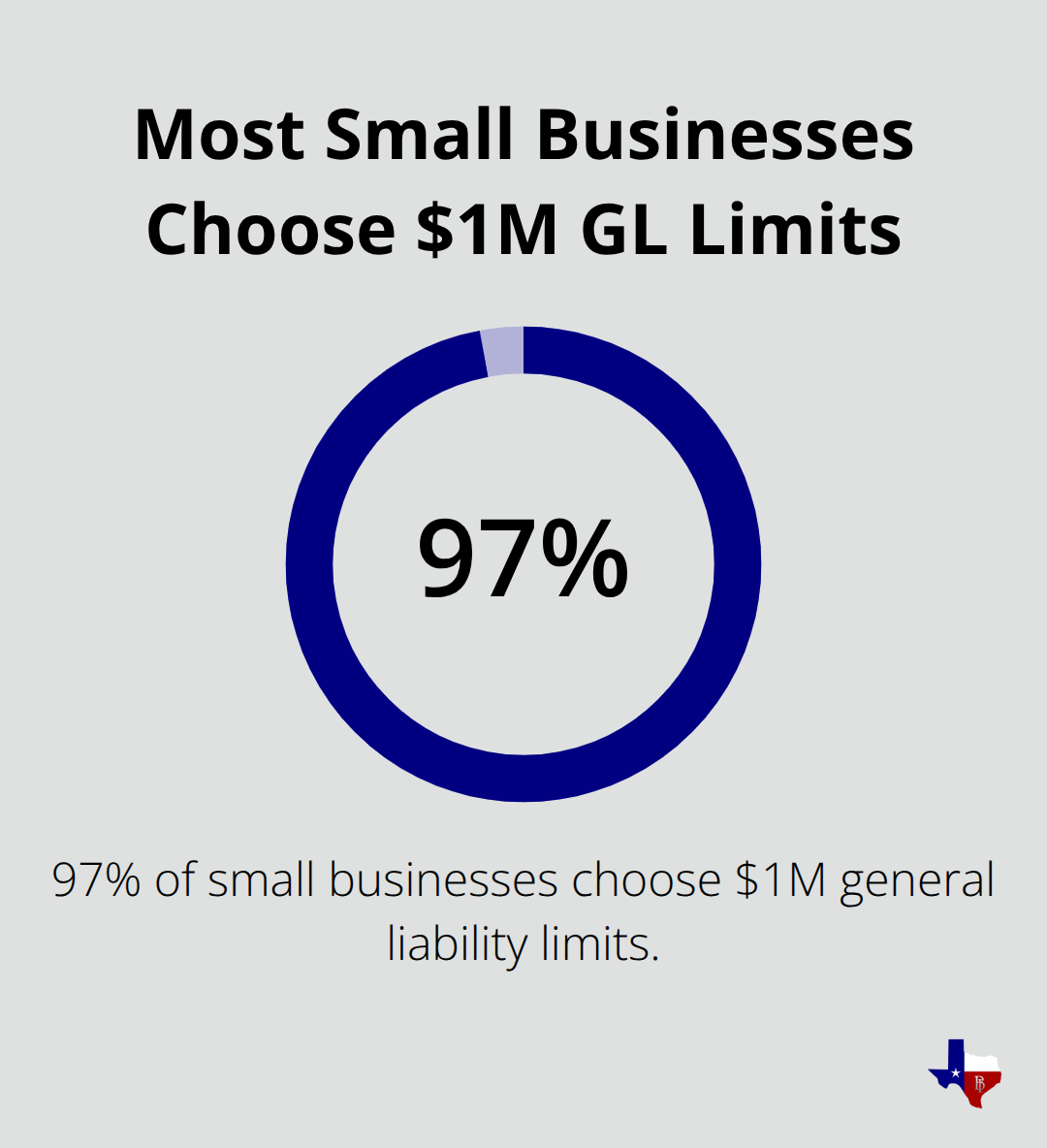

Coverage Limits and Deductibles Shape Your Bottom Line

Most Texas small businesses choose $1 million in coverage limits because that’s the minimum many clients and landlords require. Simply Business found that 97 percent of their customers select $1 million limits rather than higher amounts. Jumping to $2 million in limits increases your cost by roughly 15–25 percent, making it a meaningful decision.

Your deductible directly controls what you pay monthly-raising your deductible from $500 to $1,000 or $2,500 noticeably reduces premiums, but only if you can actually cover that amount from your operating cash if a claim occurs.

Location and Claims History Drive Regional Differences

Location within Texas substantially affects pricing because Dallas and DFW metro areas run 5–15 percent higher than statewide averages due to property values and traffic patterns. Houston carries similar costs, while San Antonio runs 5–10 percent cheaper, and smaller Texas towns can be 10–20 percent below Dallas rates. A clean claims history is your most valuable asset-businesses with prior claims pay significantly more, while those with five-plus years of no claims qualify for better rates. Years in operation matter too; startups often face higher premiums than established businesses because insurers view longevity as proof of stability. Understanding these regional and historical factors helps you anticipate what your specific quote will look like when you move forward with coverage options.

What You’ll Actually Pay for General Liability Insurance

Industry Type Determines Your Premium Range

Your actual premium depends on which industry you operate in, and the numbers show stark differences. A home-based consultant pays roughly $480–$720 annually for $1 million in coverage, while a restaurant owner in Dallas pays $1,200–$2,000, and a roofer can expect $1,500–$4,500. According to Simply Business data, most small business owners pay less than $95 per month, but that median masks the reality that your industry determines whether you sit at the low or high end of that range. Mobile service businesses like auto repair or window tinting run $600–$1,800 annually depending on your specific operations and location. Specialty trades show even wider variation: electricians typically pay $1,000–$2,500, plumbers $900–$2,200, HVAC contractors $1,000–$2,400, and painters $800–$1,800. Insurers price based on actual claims data from your industry. A photographer with zero injury claims over five years costs less to insure than a contractor working at heights with machinery involved. Retail stores with foot traffic typically cost $600–$1,000 annually, while creative professionals like graphic designers pay $500–$900.

How Texas Stacks Up Against National Rates

Texas premiums run lower than the national average in most cases, which works in your favor. Location within Texas matters significantly, however. Dallas and the DFW area run 5–15 percent higher than statewide averages, Houston tracks similarly, San Antonio runs 5–10 percent cheaper, and smaller Texas towns can be 10–20 percent below Dallas rates. These regional differences reflect property values, traffic patterns, and local market conditions that insurers factor into their pricing models.

Coverage Limits Control Your Monthly Cost

Standard $1 million per occurrence limits cost substantially less than $2 million limits, which add roughly 15–25 percent to your premium. Liability coverage provides you with bodily injury and property damage protection, and since 97 percent of small businesses choose $1 million coverage anyway, that’s typically your starting point unless you operate in high-risk industries or have significant revenue. This decision alone shapes whether you pay $40 per month or $60 per month for the same basic protection.

Deductibles Offer Your Second Cost Lever

Your deductible directly controls your monthly premium. Raising your deductible from $500 to $1,000 or $2,500 noticeably reduces your monthly cost, but only increase your deductible if you can actually cover that amount from cash on hand when a claim occurs. Many business owners lower their deductibles just to save money on premiums, then face financial strain when they must pay out-of-pocket on a claim. The math only works if you have the reserves to back it up.

What Comes Next in Your Cost Strategy

Understanding these baseline costs sets the stage for the real opportunity: reducing what you actually pay through smart policy choices and risk management. The next section shows you exactly how to lower your premiums without sacrificing the protection your business needs.

How to Cut Your General Liability Premiums Without Cutting Corners

Safety Protocols Lower Your Premiums Directly

Safety protocols and risk management practices reduce what insurers charge you each month. Businesses that document employee training, maintain organized workspaces, install security systems, and weatherproof their premises qualify for measurable discounts. Implementing these concrete safety measures lowers your GL costs because insurers reward risk reduction with better rates. If you operate a retail storefront, better lighting and clear sightlines reduce trip-and-fall claims, which translates to lower premiums at renewal. Construction companies that maintain documented safety protocols and equipment maintenance records pay substantially less than those without formal procedures. The key is making these practices visible to your insurer through documentation and then telling your agent about them during renewal conversations. Many business owners implement safety improvements but never mention them to their carrier, missing out on the discounts they’ve earned.

Bundle Policies to Save 10–30 Percent

Bundling general liability with commercial property into a Business Owner’s Policy saves 10–30 percent compared to buying coverages separately. A standalone general liability policy costs roughly $69 per month for standard $1 million coverage, but adding commercial property separately runs another $67 monthly according to industry data. Bundling both into a BOP reduces your total cost significantly while simplifying your policy management. If you need workers’ compensation for employees, professional liability for services you provide, or cyber insurance for data protection, each additional policy bundled with your GL coverage yields additional discounts. Independent agents can access 80+ carriers and quote multiple bundle options in minutes, showing you exactly how much you save by combining coverages versus keeping them separate. Most small business owners discover they’re overpaying because they’ve collected policies from different carriers over years without comparing bundled rates. Consolidating with one carrier through a BOP or similar bundle is the fastest way to lower your overall insurance costs.

Review Your Coverage Annually to Catch Savings

Your claims history, revenue changes, and business operations shift annually, which means your coverage needs and pricing change too. Scheduling a coverage review conversation with your agent every 12 months catches opportunities to adjust deductibles, remove unnecessary limits, or add protections you’ve outgrown. If you’ve maintained a clean claims record for two years, mention it at renewal because many carriers reward consecutive claim-free years with rate reductions. Conversely, if your revenue dropped, lowering your coverage limits slightly can reduce premiums without leaving you exposed. An independent agent who represents multiple carriers can shop your updated profile across their entire panel rather than asking your current carrier for a quote and accepting whatever they offer. This annual review and shopping process often uncovers savings of $20–$40 per month simply because your risk profile has improved or market conditions have shifted in your favor.

Final Thoughts

General liability insurance protects your business from financial devastation, but the cost doesn’t have to drain your operating budget. Your small business general liability insurance cost depends on your industry, location, coverage limits, and claims history-factors you now understand clearly. A home-based consultant pays $480–$720 annually while a restaurant owner pays $1,200–$2,000, and that difference reflects real risk differences, not arbitrary pricing.

The real opportunity lies in the actions you control right now. Documented safety protocols, bundled policies for 10–30 percent savings, and annual coverage reviews catch premium reductions most business owners miss. Raising your deductible, maintaining a clean claims record, and working with an independent agent who accesses 80+ carriers puts you in position to pay substantially less than businesses that accept their first quote without shopping.

An independent agent can show you multiple bundle options, compare rates across carriers, and explain exactly what each coverage level protects in minutes rather than hours. You’ll see concrete numbers for your specific business rather than guessing based on industry averages. Contact Brooks Insurance today to get your quote and start paying what your business actually deserves.

Disclaimer: The information provided in this blog is for general informational purposes only and does not constitute legal, financial, or insurance advice. Coverage options, terms, and availability may vary. Please consult with a licensed professional for advice specific to your situation