Flood damage can wipe out your savings in seconds. When a storm hits Texas, your flood policy deductible becomes the difference between recovering quickly and facing financial hardship.

We at Brooks Insurance know that most homeowners don’t understand how deductibles actually work or what they’ll really pay out of pocket after a flood. This guide breaks down the numbers so you can make a smart choice.

How Flood Deductibles Actually Work in Texas

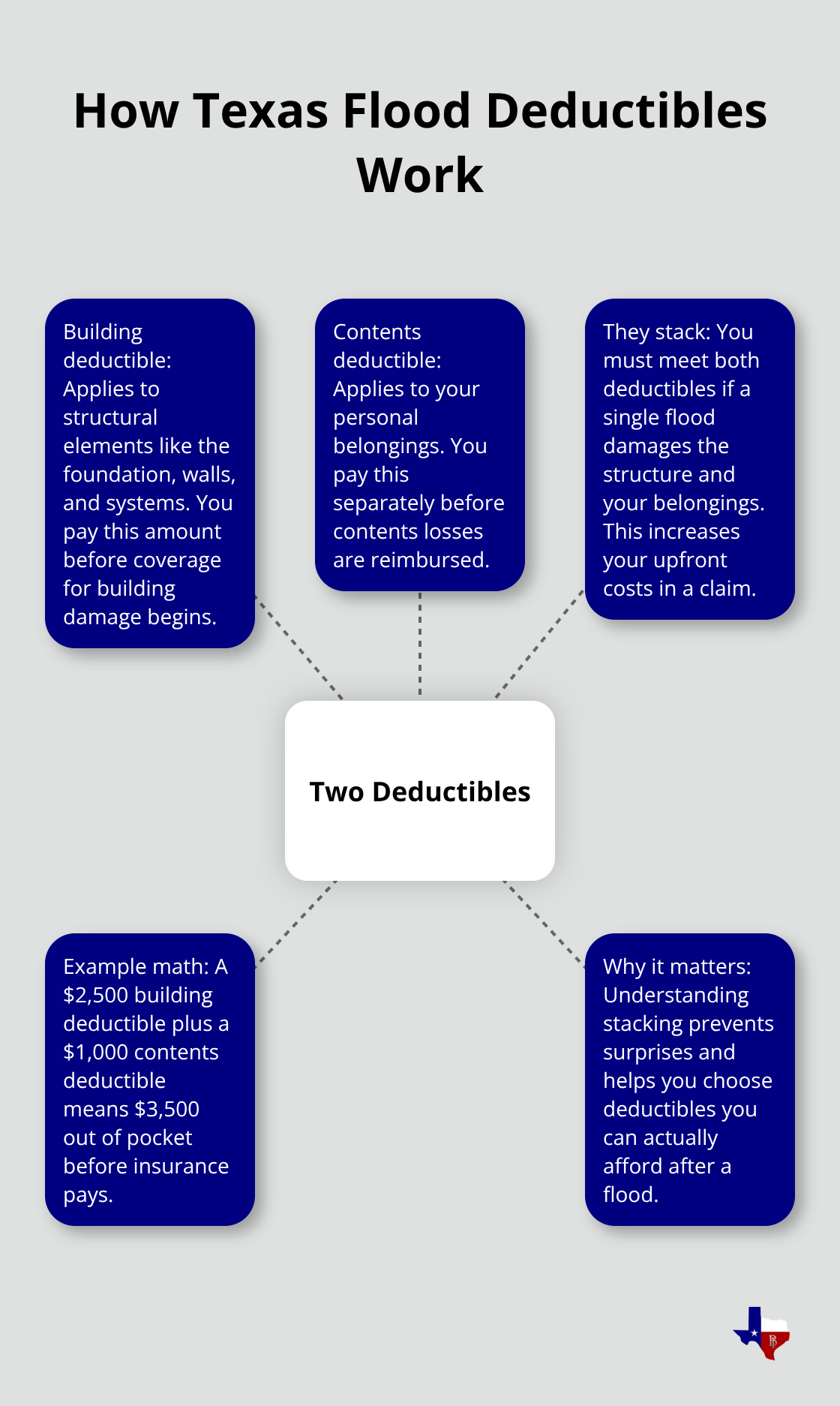

A flood insurance deductible is the amount you pay out of your own pocket before your insurance company covers the rest of the damage. Here’s what matters for Texas homeowners: flood policies use two separate deductibles, not one. You have a building deductible that applies to structural damage and a contents deductible that applies to your personal belongings. These deductibles stack, meaning you pay both before receiving any reimbursement. If your building deductible is $2,500 and your contents deductible is $1,000, a flood that damages both your home’s foundation and your furniture means you’ll pay $3,500 out of pocket before insurance kicks in.

This two-deductible structure surprises most homeowners, so understanding it upfront prevents nasty surprises when you file a claim.

What Deductible Options Actually Cost You

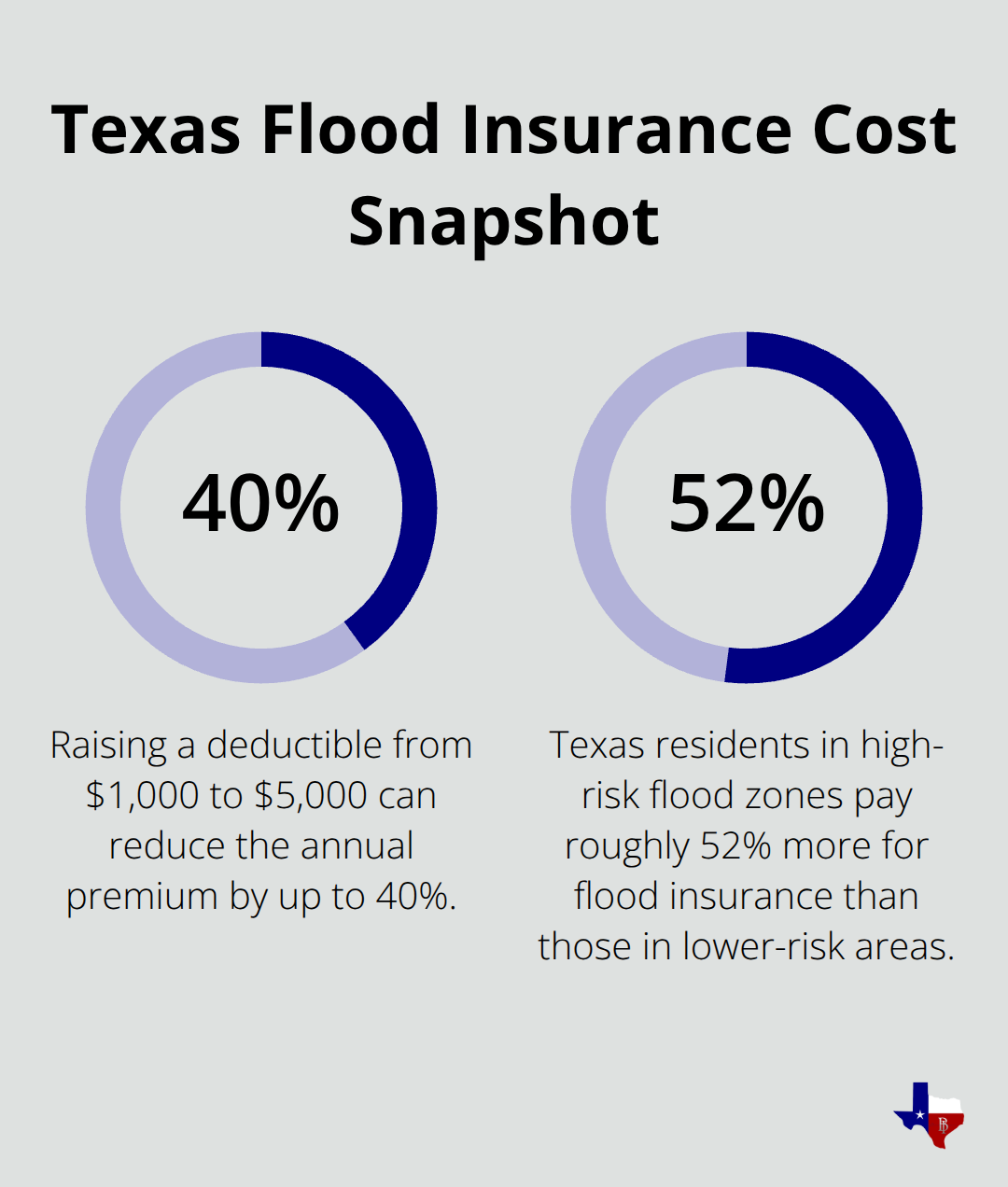

In Texas, NFIP deductibles range from $1,000 to $10,000, and the choice you make directly impacts your monthly premium. Here’s the financial reality: raising your deductible from $1,000 to $5,000 can reduce your annual premium by up to 40 percent. That sounds attractive until a flood hits and you need to cover that $5,000 before insurance pays anything. The average NFIP claim payout in Texas from 2016 to 2022 was about $66,000, so most claims exceed typical deductibles significantly.

However, Texas residents in high-risk zones pay roughly 52 percent more for flood insurance than those in lower-risk areas, with high-risk homeowners paying around $1,021 annually compared to $671 in lower-risk zones. This premium difference makes deductible selection genuinely consequential. Your mortgage lender may also cap your deductible choices, particularly in high-risk flood zones, to protect their investment in your property. Private flood insurance providers often offer more flexible deductible options than NFIP, which can be valuable if you want customization beyond what federal programs allow.

Balancing Cost and Your Real Financial Readiness

The right deductible depends on three concrete factors: your location’s flood risk, your lender’s requirements, and how much cash you actually have available for an emergency. About 25 percent of all flood insurance claims come from areas with low-to-moderate flood risk, which means flood risk remains unpredictable regardless of where you live in Texas. If you live in a moderate-risk area with lower baseline premiums, you can afford a higher deductible while still keeping your total annual cost reasonable. If you’re in a high-risk coastal county like Galveston, where the average NFIP premium reaches $992 annually, you might need to push your deductible higher to keep premiums manageable. The critical question isn’t whether a higher deductible saves money on premiums-it does-but whether you have $5,000 or $10,000 sitting in savings when a flood destroys your home. Most people don’t, which is why choosing a deductible that aligns with your actual emergency fund matters more than your premium budget alone.

How Your Flood Risk Zone Shapes Deductible Decisions

Your location in Texas determines both your baseline premium and the deductible options available to you. High-risk zones (designated with FEMA codes starting with A or V) often come with stricter deductible caps or fewer customization options through NFIP. A homeowner in Harris County pays an average of $786 annually, while someone in Hidalgo County pays $531-a significant difference that affects how much you can realistically raise your deductible. Low- and moderate-risk zones (codes B, C, or X) typically offer more flexibility and lower baseline costs, making higher deductibles more affordable. Private flood insurance providers can sometimes offer more options in these lower-risk areas, giving you additional choices beyond federal programs. Understanding your specific zone helps you calculate whether a $5,000 deductible actually saves you money or simply shifts risk to your emergency fund.

Moving Forward With Your Deductible Choice

The deductible you select today determines what you’ll pay tomorrow when water enters your home. Your next step involves comparing what NFIP offers against private flood insurance options available in your area, then matching those choices to your financial situation and lender requirements. This comparison reveals whether you can truly afford that higher deductible or whether a lower one protects both your home and your finances better.

How Deductibles Impact Your Payout

What You’ll Actually Pay When Floodwater Hits

When floodwater damages your Texas home, the math becomes immediate and unforgiving. Your insurance payout equals the total damage cost minus your deductibles, and this calculation determines whether you recover financially or struggle for months. If a flood causes $75,000 in combined structural and contents damage, and you selected a $2,500 building deductible plus a $1,000 contents deductible, you pay $3,500 out of pocket before the insurer covers the remaining $71,500. The NFIP’s average claim payout in Texas from 2016 to 2022 was approximately $66,000, which means most homeowners who file claims receive substantial reimbursement after meeting their deductibles. However, this average masks a critical reality: deductible selection directly affects your immediate financial burden.

A homeowner in a high-risk zone like Galveston County paying $992 annually might rationalize a $5,000 deductible to save on premiums, but that same homeowner needs $5,000 in accessible cash immediately after a flood to start repairs while waiting for insurance processing, which typically takes four to eight weeks. Private flood insurance providers sometimes offer lower deductibles than NFIP allows in high-risk areas, which can reduce your out-of-pocket exposure during a claim, though you’ll pay higher premiums for this flexibility.

Why Homeowners Make Costly Deductible Mistakes

The mistakes homeowners make when selecting deductibles stem from focusing only on annual premium savings rather than actual financial readiness. Many Texas residents choose $5,000 or $10,000 deductibles because the premium reduction looks attractive on paper, then panic when a flood occurs and they cannot access that cash without depleting their emergency fund or taking loans. A homeowner in Harris County with a $786 annual NFIP premium might save $200 to $300 yearly by increasing their deductible from $1,000 to $5,000, but this savings evaporates instantly if they lack $5,000 in liquid savings when disaster strikes.

Your mortgage lender may also impose deductible caps in high-risk zones, limiting your ability to raise deductibles regardless of premium savings, so confirming these requirements before policy selection prevents wasted time comparing options your lender won’t accept. The strongest deductible strategy aligns your premium budget with your actual emergency savings, not just the numbers that look good on a quote comparison.

Matching Your Deductible to Your Real Financial Situation

If you have $3,000 in accessible savings, a $2,500 building deductible paired with a $500 contents deductible makes financial sense, even if a slightly higher deductible would lower your premium by another $50 annually. This approach means you can cover your deductible obligation without financial strain when a claim happens, allowing you to focus on repairs rather than scrambling for funds. The deductible you select today determines what you’ll pay tomorrow when water enters your home, so your next step involves comparing what NFIP offers against private flood insurance options available in your area, then matching those choices to your financial situation and lender requirements.

What Deductible Actually Fits Your Budget

Start With Your Emergency Savings, Not Your Premium

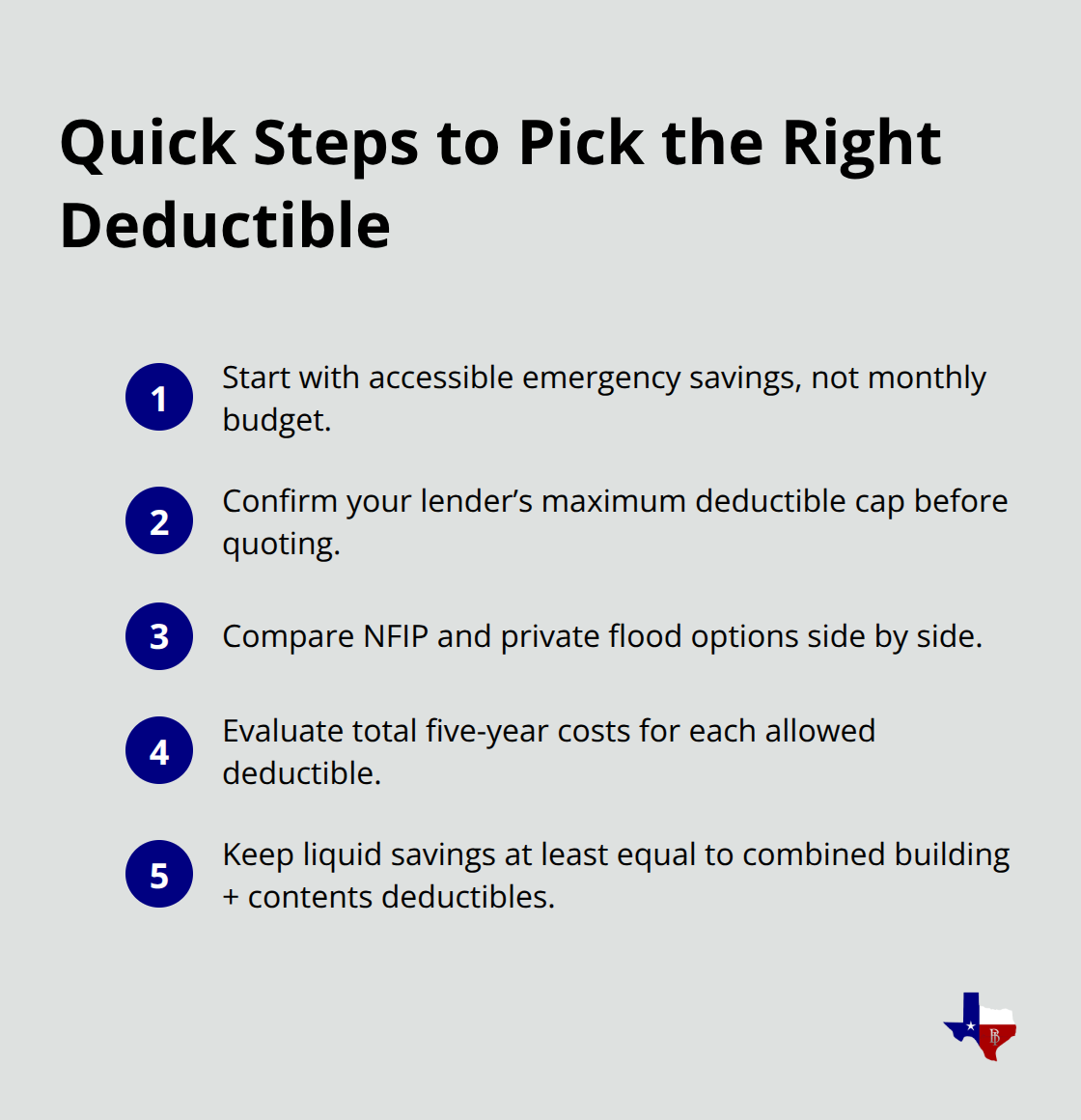

Your emergency fund, not your monthly budget, should determine your deductible. We see this mistake constantly: homeowners pick a $5,000 deductible because it saves $200 annually, then face financial collapse when that deductible comes due. The math looks simple on a quote, but the reality hits differently when you’re standing in floodwater. Start by calculating how much liquid cash you can access within 48 hours without borrowing. If you have $2,000 in savings, a $1,000 building deductible plus a $500 contents deductible aligns with reality. If you have $8,000 available, you can comfortably handle a $5,000 building deductible.

The NFIP average claim payout in Texas from 2016 to 2021 was about $66,000, which means your deductible is just the first payment before substantial insurance money flows in. However, that money takes four to eight weeks to arrive, and you need immediate cash for emergency repairs, temporary housing, and contractor deposits. This timing gap makes accessible savings the true constraint, not premium savings.

Confirm Your Lender’s Deductible Limits First

Your mortgage lender imposes hard limits on deductible choices, particularly in high-risk zones designated with FEMA codes starting A or V. Contact your lender before shopping for quotes and confirm their maximum deductible cap. High-risk borrowers in coastal areas like Galveston County, where average NFIP premiums reach $992 annually, often face stricter caps than borrowers in moderate-risk zones. This constraint eliminates the guesswork from deductible selection because your lender removes options you cannot legally choose.

Private flood insurance providers frequently offer deductible flexibility that NFIP cannot match, especially in moderate-risk areas where baseline premiums run lower. A homeowner in Harris County with a $786 average premium might find private options that allow a $1,500 deductible instead of NFIP’s $1,000 minimum, or conversely, that reduce the minimum to $500 in some cases. Comparing NFIP quotes directly against private providers reveals which option actually fits your financial situation and lender requirements.

How Your Flood Zone Affects Deductible Costs

Your flood risk zone shapes what deductibles cost you in real dollars. Hidalgo County homeowners paying $531 annually can afford higher deductibles more easily than Galveston County residents paying $992. A $4,000 annual premium difference between zones means a $200 premium savings in Hidalgo from raising your deductible might represent only 38 percent savings, while the same $200 savings in Galveston represents just 20 percent savings.

The practical action is this: obtain quotes from at least two NFIP-licensed agents and one private provider, then compare total five-year costs across all deductible options your lender permits. Five-year totals reveal whether premium savings compound into meaningful money or disappear against your out-of-pocket risk. Try to choose the deductible that keeps your annual premium affordable while maintaining emergency savings at least equal to your combined deductibles. This approach protects your finances today and your recovery tomorrow.

Final Thoughts

Your flood policy deductible in Texas determines whether you recover financially or struggle after a flood. The deductible you select today directly affects your monthly premium and your out-of-pocket costs when disaster strikes. Match your deductible to your actual financial readiness, not just the numbers that look attractive on a quote-if you have $3,000 in accessible savings, a $2,500 building deductible makes sense, while $8,000 in savings allows you to handle a $5,000 deductible comfortably.

Your mortgage lender’s requirements and your flood risk zone shape what options you can actually choose, so confirm these constraints before shopping to avoid wasted time comparing policies you cannot legally select. We at Brooks Insurance understand that deductible selection feels overwhelming when you compare NFIP quotes against private flood insurance options, and our licensed agents represent multiple top-rated insurance companies to give you access to a larger selection of coverage, pricing, and payment options than you would find with a single carrier.

Contact us at brooksinstx.com to review your current flood insurance or to get quotes that compare NFIP and private options side by side. Our agents will confirm your lender’s deductible limits, calculate what different deductible choices actually cost you over five years, and help you select coverage that matches your real financial situation.

Disclaimer: The information provided in this blog is for general informational purposes only and does not constitute legal, financial, or insurance advice. Coverage options, terms, and availability may vary. Please consult with a licensed professional for advice specific to your situation