Finding the right insurance agent in Texas shouldn’t feel overwhelming. Local independent agents offer something big national companies can’t: they know your community, your risks, and your specific needs.

At Brooks Insurance, we believe that working with local independent agents in Texas gives you real advantages-from personalized service to access to multiple carriers that fit your situation. This guide walks you through exactly how to find and choose an agent who’ll have your back.

Why Local Independent Agents Make a Real Difference

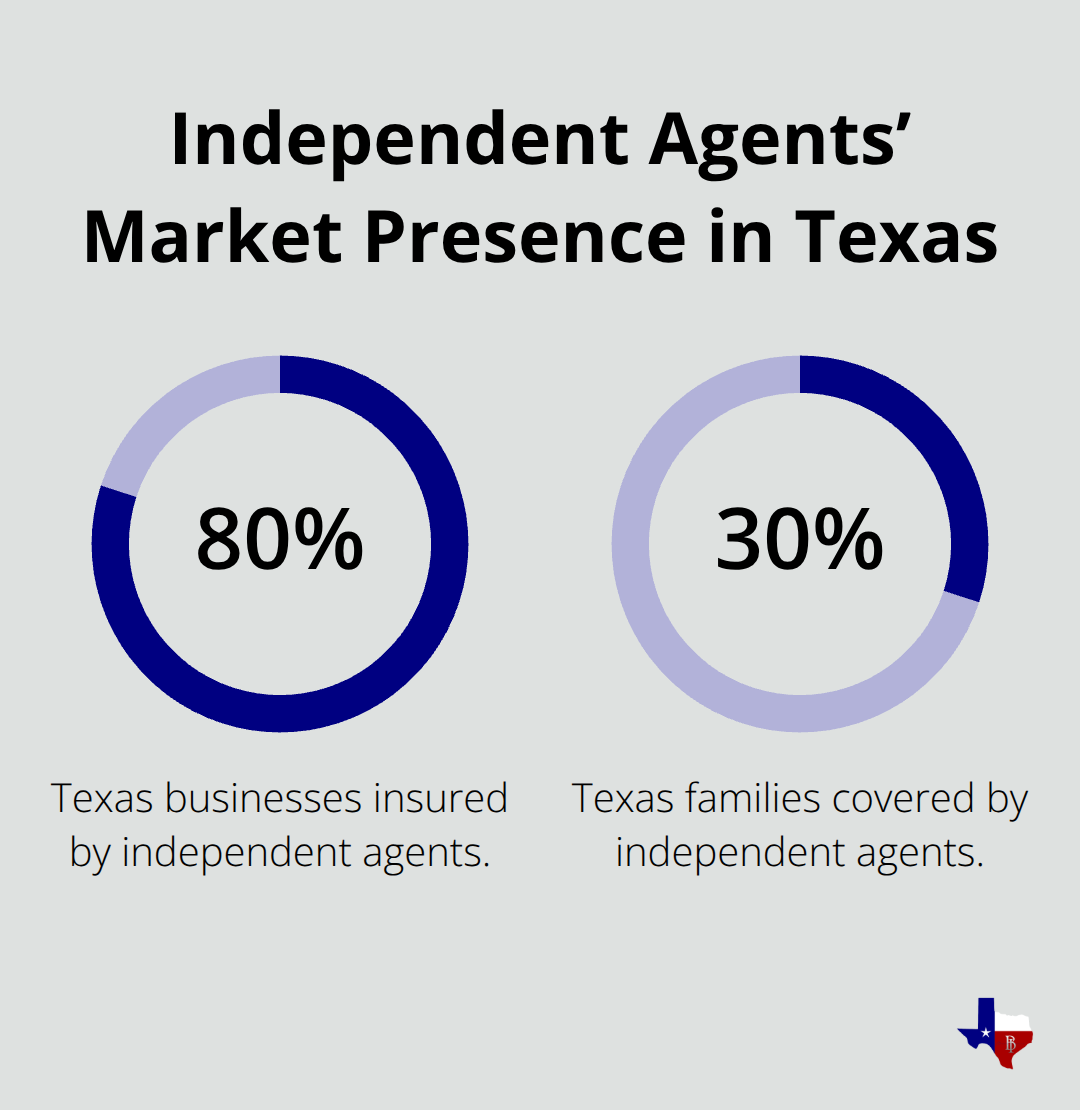

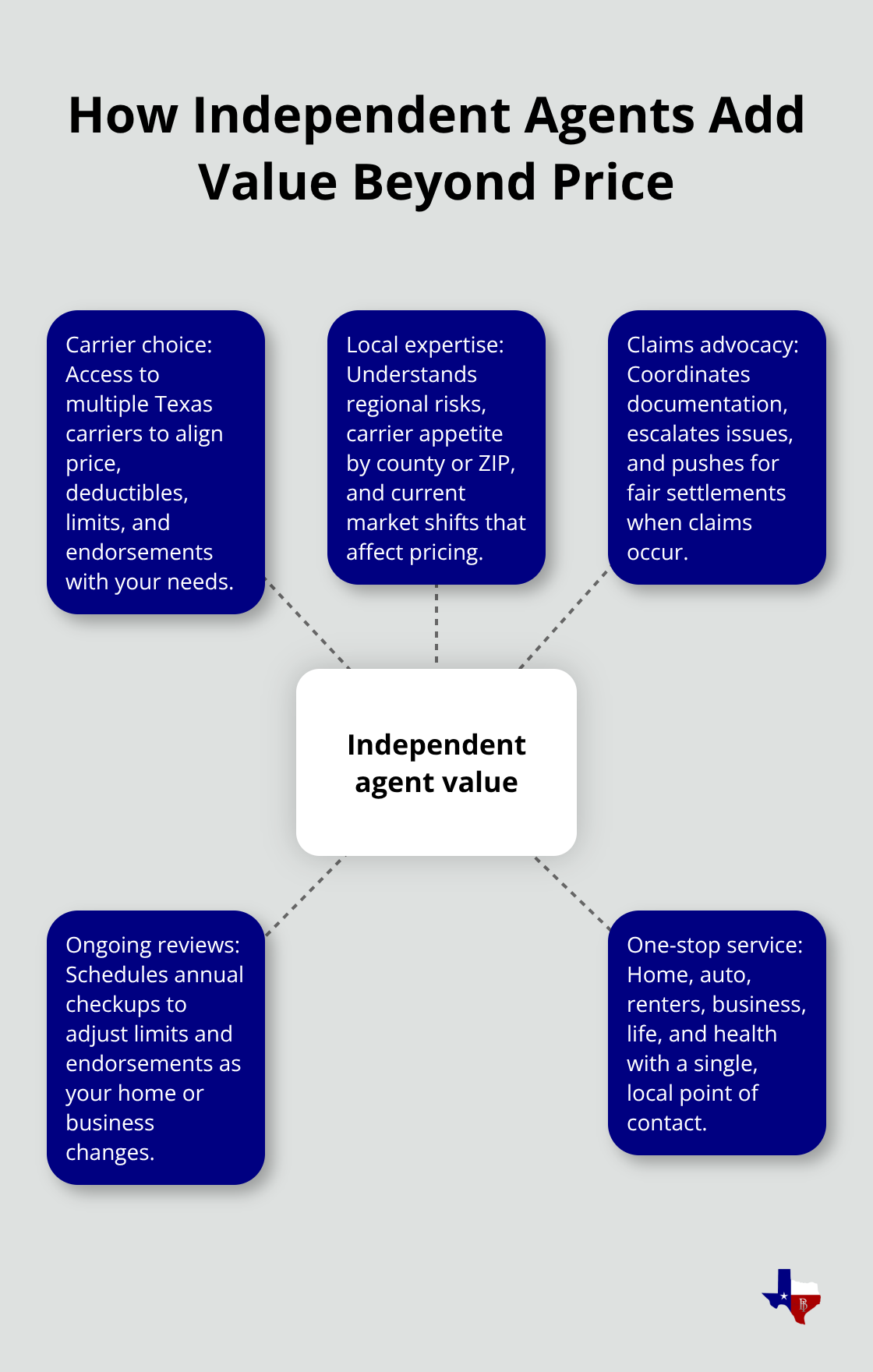

Local independent agents in Texas control access to something national companies simply cannot replicate: direct relationships with a dozen or more insurance carriers operating in your state. Independent agents insure about 80% of Texas businesses and provide coverage for nearly 30% of Texas families, representing roughly $9.6 billion in premiums annually. This market presence reflects a fundamental truth: when you work with a local independent agent, you’re not locked into one insurer’s rates or coverage options. Instead, you gain genuine choice.

An independent agent pulls quotes from multiple carriers in minutes, comparing not just price but deductibles, coverage limits, and endorsements specific to your situation. National direct-buy platforms and captive agents representing a single insurer cannot do this. The Texas homeowners insurance market alone includes nearly 160 carriers competing for your business, yet most consumers never see more than one or two quotes before purchasing. Working with an independent agent changes that equation entirely.

Local Knowledge Cuts Through Market Complexity

Texas presents unique insurance challenges that vary dramatically by region. The 14 coastal counties served by the Texas Windstorm Insurance Association face different wind and hail risks than inland areas, and premium structures reflect this reality. A local independent agent understands which carriers offer the best terms in your specific county, which ones have pulled out of certain zip codes, and which ones actively write new business in your area. This matters because the Texas homeowners insurance market shifted substantially in recent years, with the combined ratio hitting 105.1% in 2023 before improving to 98.3% in 2024, according to the Texas Department of Insurance. These swings affect carrier appetite and pricing. An agent embedded in your community knows exactly how these market movements affect you today, not six months from now when national information becomes outdated. They also know local contractors, understand regional property values, and spot coverage gaps that someone reading from a national script would miss entirely.

Advocacy That Works When Claims Happen

When you file a claim, most direct-buy insurers hand you a phone number and a claims adjuster you’ve never met. Independent agents do something different: they advocate on your behalf throughout the process. They guide you through documentation requirements, follow up with the carrier, and push back if the initial settlement offer seems low. This matters because claims disputes are where insurance relationships prove their actual value. An independent agent who has worked with a carrier for years and sends them steady business has leverage that a one-time customer does not.

They make calls, escalate issues, and get answers faster than you can alone. This ongoing relationship also means your agent reviews your coverage annually, adjusts limits as your home value changes, and catches gaps before you need them.

What Sets Independent Agents Apart From National Options

Independent agents operate differently than captive agents or direct-buy channels. A captive agent represents a single insurer and cannot show you options from competitors. A direct-buy platform offers convenience but provides no human advocate when problems arise. Independent agents give you both choice and personal support. You access multiple quotes without switching agencies as your needs change. You receive one-stop shopping for home, renters, auto, business, life, and health insurance. Most importantly, you work with a licensed professional embedded in your community who treats you like a person, not just another policy number. These agents are small business owners themselves-about 60% employ four or fewer people-and they depend on your satisfaction and referrals to succeed. That alignment of interests matters when you need help most.

The next step involves understanding exactly how to evaluate and select the right agent for your situation, which requires knowing what credentials to verify and what questions to ask.

How to Evaluate and Choose the Right Independent Agent

Verify Licensing and Credentials First

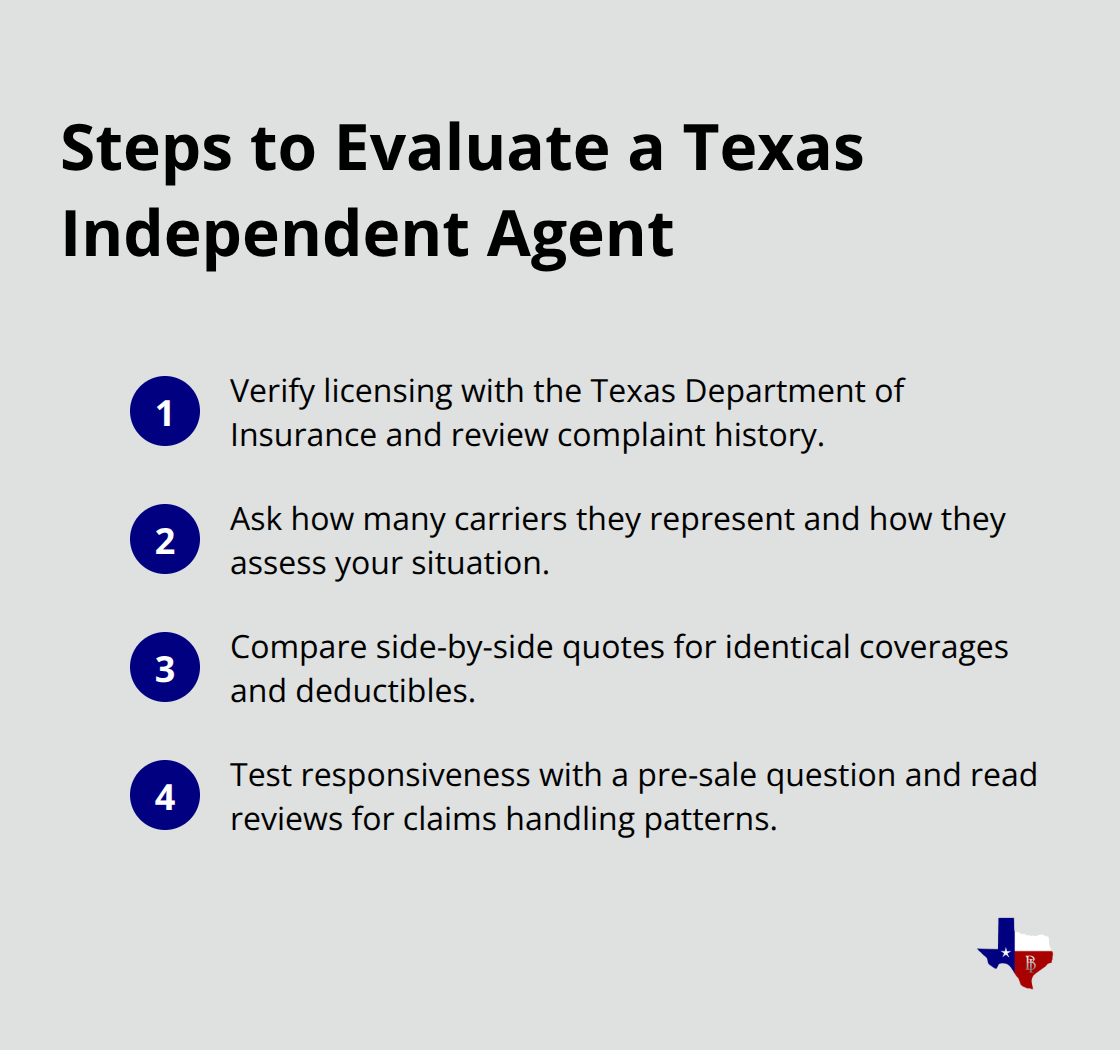

Verifying licensing is your first and non-negotiable step. Call the Texas Department of Insurance Help Line at 800-252-3439 and confirm that any agent or agency you’re considering holds a current license. This matters because selling insurance without a license is illegal in Texas, and an unlicensed seller might refuse to pay your claim when it matters most. Use the TDI’s Search for a Company or an Agent tool on their website to check not just licensing status but also complaint history and any disciplinary actions the department has taken. An agent with zero complaints does not exist, but one with a pattern of unresolved complaints is a red flag you cannot ignore.

Ask About Carrier Access and Coverage Options

Ask the agent directly how many carriers they represent. IIAD member agencies typically represent more than a dozen insurance carriers, which gives you genuine choice. If an agent represents only three or four carriers, you miss the full benefit of the independent model. During your initial conversation, ask the agent how they evaluate your specific situation. Do they ask detailed questions about your home, business operations, or family circumstances? Or do they jump straight to quoting rates? The ones who ask questions first understand that insurance is not one-size-fits-all. A good agent spends time learning your actual risks before recommending coverage.

Compare Quotes Across Multiple Carriers

Comparing quotes across multiple carriers through your agent is where real savings happen. Request quotes from at least three different carriers for the same coverage levels and deductibles so you can see how pricing varies. Pay attention to what changes between quotes: some carriers charge more for higher deductibles, others offer bigger discounts for bundling home and auto, and some provide credits for safety features you already have.

The Texas Department of Insurance reports that discounts can meaningfully lower your premiums, so ask your agent specifically what discounts apply to your situation rather than accepting the first number quoted.

Assess Responsiveness and Customer Service Quality

When evaluating responsiveness, contact the agent with a question before you commit to working with them. How quickly do they respond? Do they answer your question directly or make you call back? During claims, speed matters enormously. An agent who takes two days to return a call during shopping will take two days during a claim. Check online reviews on Google and the Better Business Bureau, but read critically. Look for patterns in what customers say about claims handling and responsiveness, not just overall star ratings. Trust an agent who acknowledges that they cannot control claim outcomes but promises to advocate for you throughout the process. That honesty signals someone who understands the actual relationship between agent and insurer.

The next step involves understanding what happens after you select an agent and how that partnership actually works when you need coverage adjustments or file a claim.

What Happens After You Choose Your Agent

Selecting an independent agent marks the start of a partnership that delivers real value over time. The true benefit emerges in how that agent structures your coverage, stays involved as your circumstances shift, and supports you when claims arise. When you first meet with your agent, expect a detailed conversation about your home, family, or business operations. A competent agent asks about square footage, year built, roof condition, security systems, recent renovations, and claims history. For business owners, they ask about operations, inventory levels, and the specific risks you face daily. This information determines whether you need standard homeowners coverage, additional endorsements for high-value items, or specialized business policies.

How Agents Present Your Coverage Options

Your agent then presents options from multiple carriers with clear explanations of what each quote includes. They show you how deductible choices affect premiums and explain why one carrier costs more than another. They identify specific discounts you qualify for-information that matters significantly since discounts can meaningfully lower premiums, yet many customers never learn what discounts actually apply to them. This transparency separates independent agents from direct-buy platforms that simply hand you a single quote and expect you to accept it.

Annual Reviews Keep Your Coverage Current

After you purchase a policy, the partnership continues through regular reviews. A serious independent agent schedules annual conversations to reassess your coverage against life changes. If you renovated your kitchen, added a pool, or purchased expensive jewelry, your agent adjusts limits accordingly. If you started a home-based business, they add commercial coverage. These reviews prevent the common problem of outgrowing your policy without realizing it.

Claims Advocacy Makes the Difference

When you file a claim, your agent becomes your advocate with the insurance company. They help you document damages, submit required paperwork, and follow up on settlement timelines. They push back if an initial offer seems unfair and escalate issues when needed. This ongoing relationship means your agent knows your situation intimately, making them far more effective at fighting for fair treatment than you could be alone. An agent who has worked with a carrier for years and sends them steady business has leverage that a one-time customer does not possess.

Accessibility That Matters

Your agent remains available throughout the policy lifecycle. Licensed agents and staff answer questions about coverage through phone calls or emails, providing the accessibility that separates independent agents from faceless national companies. This consistent contact point means you never navigate policy changes or claim disputes alone.

Final Thoughts

Choosing a local independent agent in Texas means gaining access to something that national companies cannot match: genuine choice combined with personal advocacy. These agents control relationships with multiple carriers, understand your specific regional risks, and fight for you when claims arise. Their interests align with yours because they depend on your satisfaction and referrals to succeed, creating a partnership that captive agents or direct-buy platforms simply cannot replicate.

When you evaluate agents, verify licensing through the Texas Department of Insurance, ask directly about carrier access and how they assess your situation, and test their responsiveness before committing. The agent who asks detailed questions about your home or business before quoting rates understands that insurance requires customization, not templates. The real value of working with local independent agents Texas emerges over time through annual policy reviews that catch coverage gaps, claims advocacy that gets you fair settlements faster, and accessibility to a real person when questions arise.

Contact Brooks Insurance today to connect with an independent agent who takes time to understand your actual needs rather than rushing to close a sale. Prepare to answer detailed questions about your home or business, request quotes from multiple carriers, and compare not just price but coverage and service quality. The agent worth working with long-term is the one who delivers better coverage and genuine peace of mind.

Disclaimer: The information provided in this blog is for general informational purposes only and does not constitute legal, financial, or insurance advice. Coverage options, terms, and availability may vary. Please consult with a licensed professional for advice specific to your situation