Your fleet is your business. When vehicles break down or accidents happen, unplanned downtime costs money-and inadequate Texas commercial auto coverage can cost even more.

We at Brooks Insurance know that fleet owners face unique risks that standard policies often miss. This guide walks you through the coverage types you need, the gaps you should watch for, and how to build a policy that actually protects your operation.

What Your Texas Commercial Auto Policy Actually Covers

Liability Coverage: The Foundation of Fleet Protection

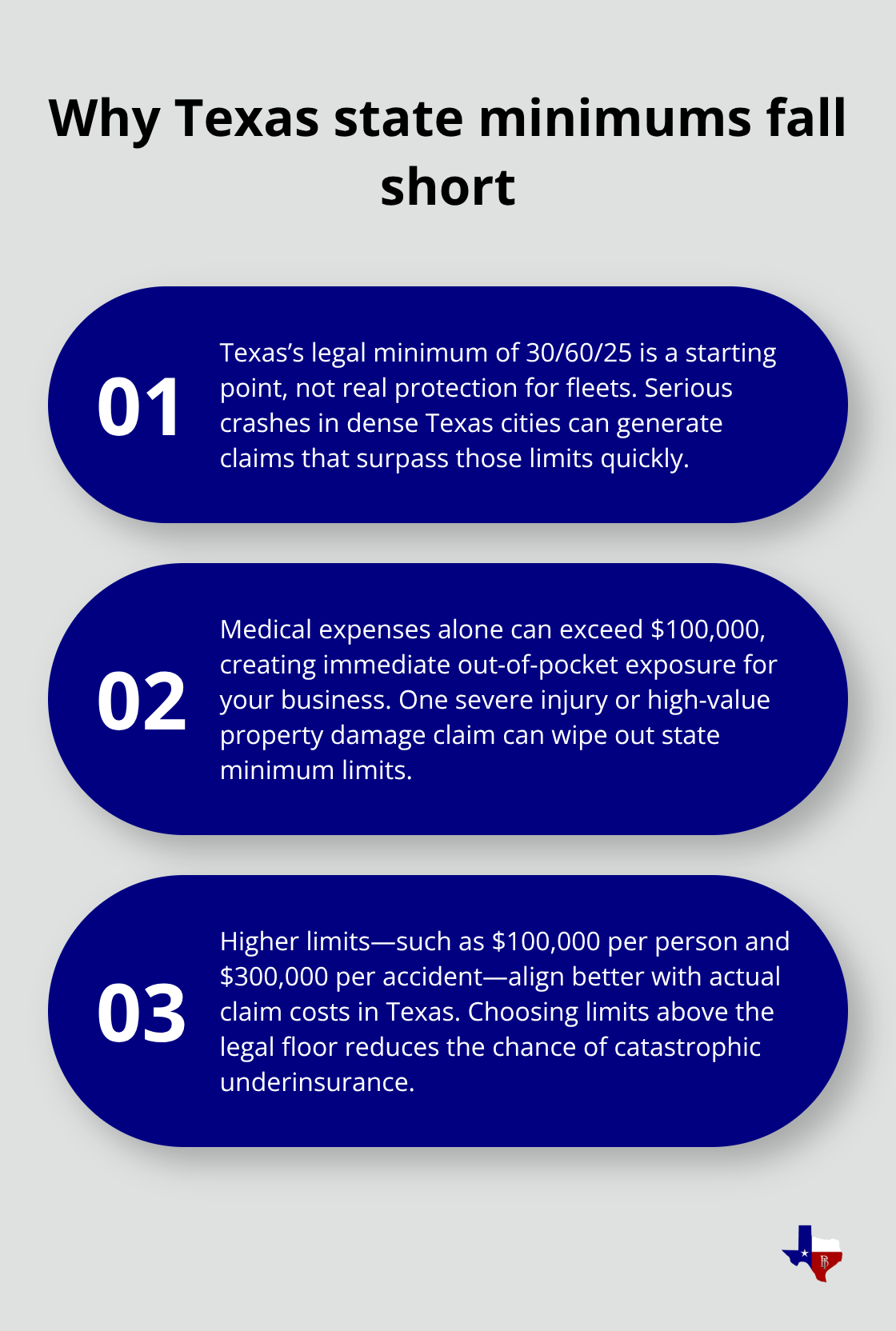

Texas commercial auto insurance protects your fleet against three major categories of loss. Liability coverage handles bodily injury and property damage you cause to others-this is mandatory under Texas law, which requires minimum limits of 30/60/25 ($30,000 per person, $60,000 per accident, and $25,000 property damage). That legal floor is dangerously low for most fleet operations. If one of your drivers injures someone seriously or damages expensive property, those state minimums evaporate quickly. A single medical claim can easily exceed $100,000, leaving your business responsible for the overage.

We recommend carrying at least $100,000 per person and $300,000 per accident for liability-significantly higher than the Texas minimum-because that’s what actually matches the real-world cost of claims in Texas cities. The Texas Department of Insurance data shows that liability settlements in urban areas like Dallas and Houston regularly exceed state minimums, so defaulting to the legal floor is essentially gambling with your company’s future.

Collision and Comprehensive: Protecting Your Vehicles

Collision and comprehensive coverage pay to repair or replace your vehicles after covered accidents or non-accident damage like theft, weather, or vandalism. Collision covers accidents with other vehicles or objects; comprehensive covers everything else. These are optional but required if you finance or lease vehicles, and they’re smart regardless.

Set your deductible based on each vehicle’s age and value-a $1,000 deductible makes sense for a newer truck worth $40,000, but a $500 deductible on a used van worth $8,000 wastes money on higher premiums. This approach keeps your costs aligned with actual risk.

Uninsured and Underinsured Motorist Coverage

Uninsured and underinsured motorist coverage protects you and your drivers when someone else causes an accident but lacks sufficient insurance. Texas law requires this coverage unless you formally reject it in writing, and rejecting it is a mistake. Texas roads carry significant uninsured motorist exposure; many drivers carry minimal coverage or none at all.

Your underinsured motorist limit should match or exceed your liability limit so your drivers aren’t left paying out of pocket when hit by an underinsured driver. This protection closes a critical gap that liability coverage alone cannot address.

What Lies Beyond the Basics

These three categories form the foundation of fleet protection, but they’re only the beginning. Most fleet owners operate with gaps in coverage that emerge only when accidents happen-and that’s when the real costs surface.

Common Coverage Gaps Fleet Owners Miss

Non-Owned Vehicle Coverage Limitations

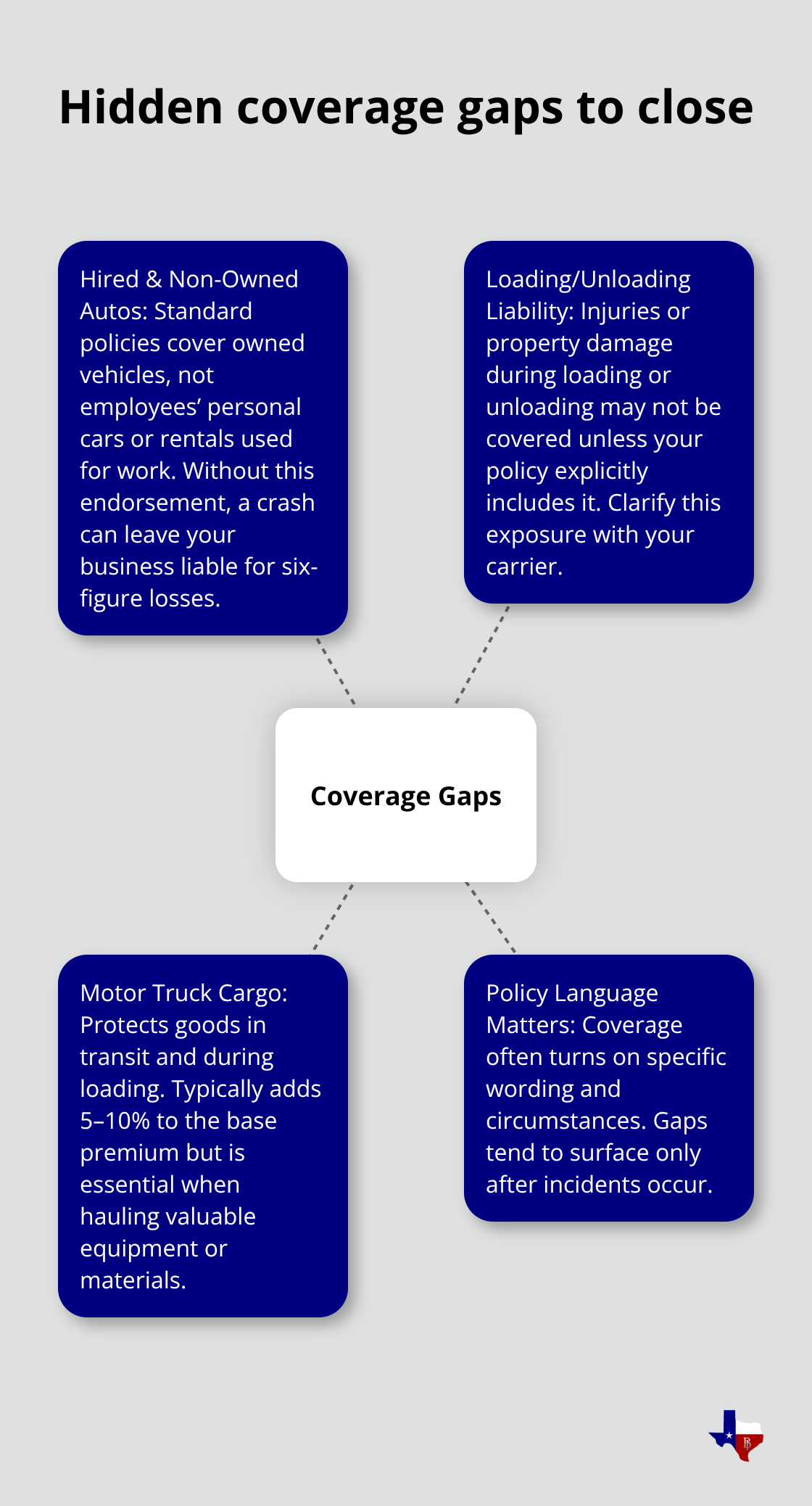

Most fleet owners assume their standard commercial auto policy covers all vehicles used for business. It doesn’t. The policy you purchased protects vehicles your business owns, but the moment an employee uses a personal vehicle for a work errand or you rent a vehicle for a temporary job, your coverage either vanishes or becomes severely limited. A delivery driver uses their personal car to pick up supplies and crashes, injuring someone. Your policy won’t pay because personal auto policies explicitly exclude business use. Your business becomes liable for damages that could reach $150,000 or more, and you pay directly out of pocket.

Hired and non-owned auto coverage closes this exact gap by protecting you when employees use rental vehicles or their own cars for business purposes. Without it, you operate with a coverage hole that will eventually cost your company significant money. The Texas Department of Insurance data shows that claims involving non-owned vehicles represent a growing portion of commercial auto losses, yet most small fleet operators simply don’t purchase this protection.

Loading and Unloading Exposure Risks

Loading and unloading operations present another hidden gap that catches fleet owners off guard. When your driver parks a delivery truck and walks into a building, cargo theft or weather damage can occur. More critically, if loading or unloading operations cause injury to a customer or damage to their property, your standard commercial auto policy may not cover it (depending on how the incident occurs and what your policy language actually states).

A loader drops a pallet on a customer’s foot while unloading at their dock. Your liability coverage might apply, but only if the policy explicitly includes loading and unloading exposure.

Many policies don’t. Motor truck cargo coverage is a specialized endorsement that protects goods in transit and during loading operations, and it becomes essential if your fleet carries valuable equipment, merchandise, or materials. The cost is modest compared to the exposure, typically adding 5 to 10 percent to your base premium (depending on cargo type and value).

If your drivers handle goods worth more than a few thousand dollars per load, this coverage isn’t optional. The gap between what you think you’re covered for and what your policy actually covers can cost thousands when an incident occurs. Understanding these specific exposures helps you build a policy that actually matches your operation.

Building Your Fleet Policy: What Actually Matters

Document Your Fleet and Operations

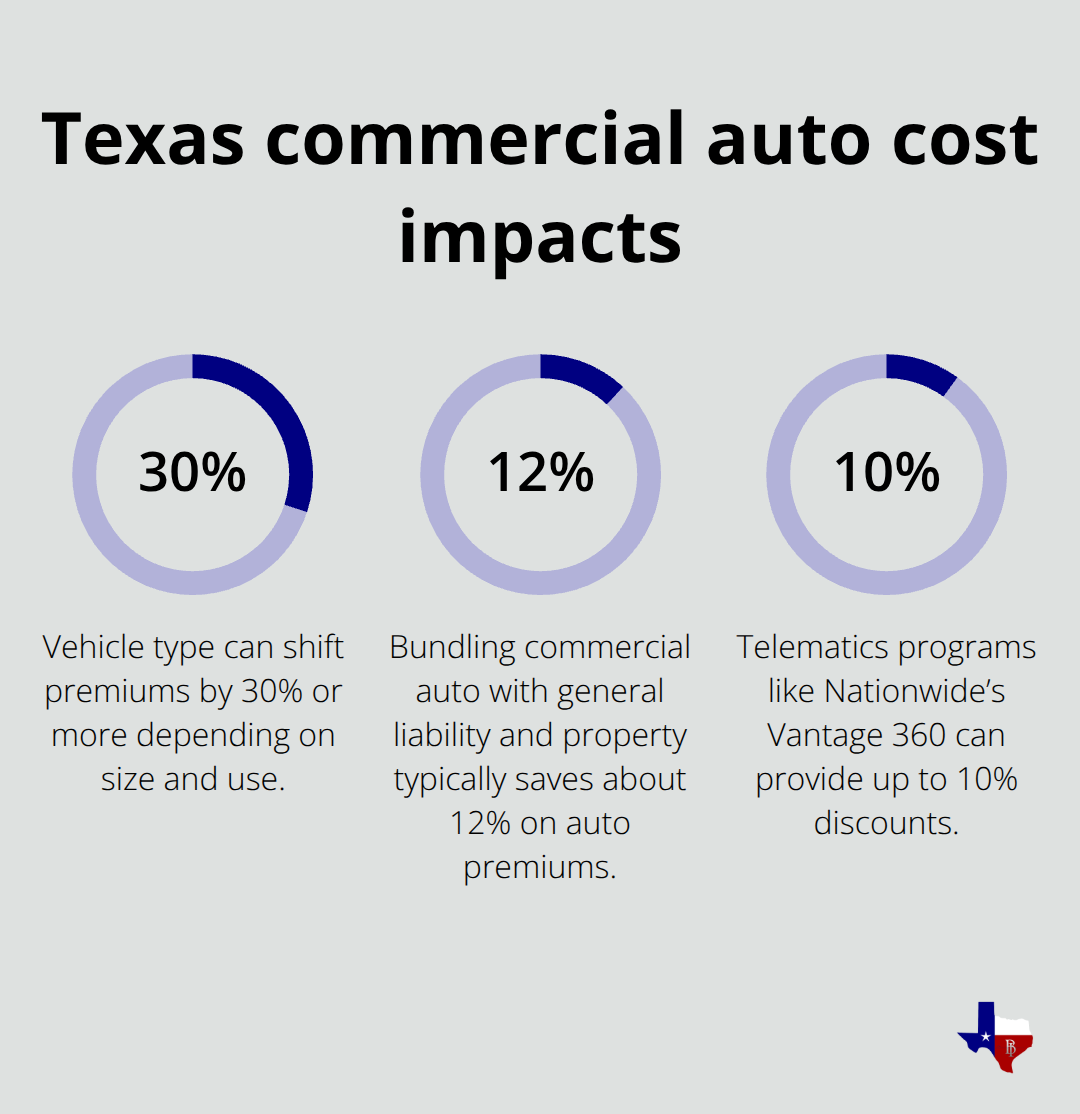

Start with your specific operation, not industry averages. You need to document exactly how many vehicles you own, what type each one is (pickup trucks, vans, box trucks, specialty rigs), and what work they perform. A contractor with three service vans doing local HVAC jobs faces completely different risk than a courier operating a mixed fleet across multiple Texas cities. Vehicle type alone creates pricing swings of 30 percent or more. Larger vehicles, such as trucks and vans, typically incur higher insurance costs compared to smaller vehicles like sedans.

Your premium depends on the number and type of vehicles, annual mileage, driver histories, garage locations, claims history, and chosen coverages. You should measure your actual routes and mileage too. Travel radius matters significantly for pricing; local operations within a single city typically cost less than regional routes spanning multiple counties.

Evaluate Your Drivers and Driving Records

You need to document which employees drive regularly, pull their three-year driving records, and be honest about violations and accidents. Insurance carriers review this data closely, and accuracy prevents quote rejections or policy cancellations later. This step takes time but protects you from surprises when your policy renews or when you file a claim.

Compare Quotes from Multiple Carriers

You should request quotes from at least three carriers and compare policy terms, not just premiums. Progressive leads across most vehicle types in Texas, with particularly strong rates for specialty operations like taxi fleets and food trucks. GEICO often provides better affordability on sedans and SUVs, typically 14 to 19 percent below Texas averages depending on vehicle type. The Hartford offers the deepest coverage customization and 24/7 claims support, though premiums run higher. Nationwide excels for upfitted vehicles and agricultural operations, with Vantage 360 telematics offering up to 10 percent potential discounts.

When you compare quotes, specify your actual coverage needs beyond state minimums: hired and non-owned auto coverage, uninsured motorist limits matching your liability limits, motor truck cargo if applicable, and collision deductibles that match each vehicle’s value. You should request certificates of insurance from each carrier to confirm they can issue them quickly with additional insured wording, since clients frequently require them.

Maximize Savings Through Bundling and Coverage Alignment

Bundling commercial auto with general liability and property coverage typically saves about 12 percent on auto premiums alone. This approach reduces your overall costs while simplifying your insurance management.

An independent agency like Brooks Insurance can help you evaluate these options and connect you with carriers that align with your operation’s specific risk profile and budget.

Final Thoughts

Your Texas commercial auto coverage strategy should reflect your actual operation, not industry defaults or what you think you need. The foundation starts with liability limits that exceed the state minimum of 30/60/25, uninsured motorist protection matching your liability limits, and collision and comprehensive coverage aligned to each vehicle’s value. Beyond these basics, hired and non-owned auto coverage and motor truck cargo protection close the gaps that catch most fleet owners off guard.

Pull your declarations page and verify that your liability limits actually match your business risk, not just the legal floor. Confirm that your uninsured motorist coverage equals your liability limits, and check whether your policy includes hired and non-owned auto coverage if your drivers ever use rental vehicles or personal cars for work. If you transport goods, verify that motor truck cargo coverage is included (and compare your deductibles against each vehicle’s current value to eliminate overpaying for coverage on older units).

We at Brooks Insurance have spent over 50 years helping Texas fleet owners build policies that work. As an independent agency, we represent multiple top-rated carriers, which means you get access to a larger selection of coverage options and pricing than you would working with a single insurer. Contact us at brooksinstx.com to request a quote and have a conversation about what your fleet actually needs to stay protected and moving.

Disclaimer: The information provided in this blog is for general informational purposes only and does not constitute legal, financial, or insurance advice. Coverage options, terms, and availability may vary. Please consult with a licensed professional for advice specific to your situation