Getting accurate Texas commercial auto quotes requires more than just a quick online search. The difference between a low quote and one that actually reflects your business needs can save you thousands annually.

At Brooks Insurance, we’ve helped countless Texas business owners navigate the quote process and find coverage that fits their operations. This guide walks you through the key factors insurers consider, how to prepare your information, and how to compare quotes effectively.

What Determines Your Texas Commercial Auto Rates

Vehicle Type and Usage Patterns

Insurance companies in Texas examine specific factors when calculating your commercial auto premium, and understanding these drivers helps you anticipate costs and identify where you can reduce them. Vehicle type matters significantly because heavy trucks and specialized equipment common in Texas oil and gas and construction sectors command higher premiums due to repair costs and exposure risk. A box truck will cost more to insure than a sedan, and a fleet of dump trucks will cost substantially more than delivery vans. Usage patterns directly impact your rate as well, since vehicles with heavy usage of 50,000 or more miles annually push costs higher than those with moderate mileage.

Weather, Accidents, and Location Risk

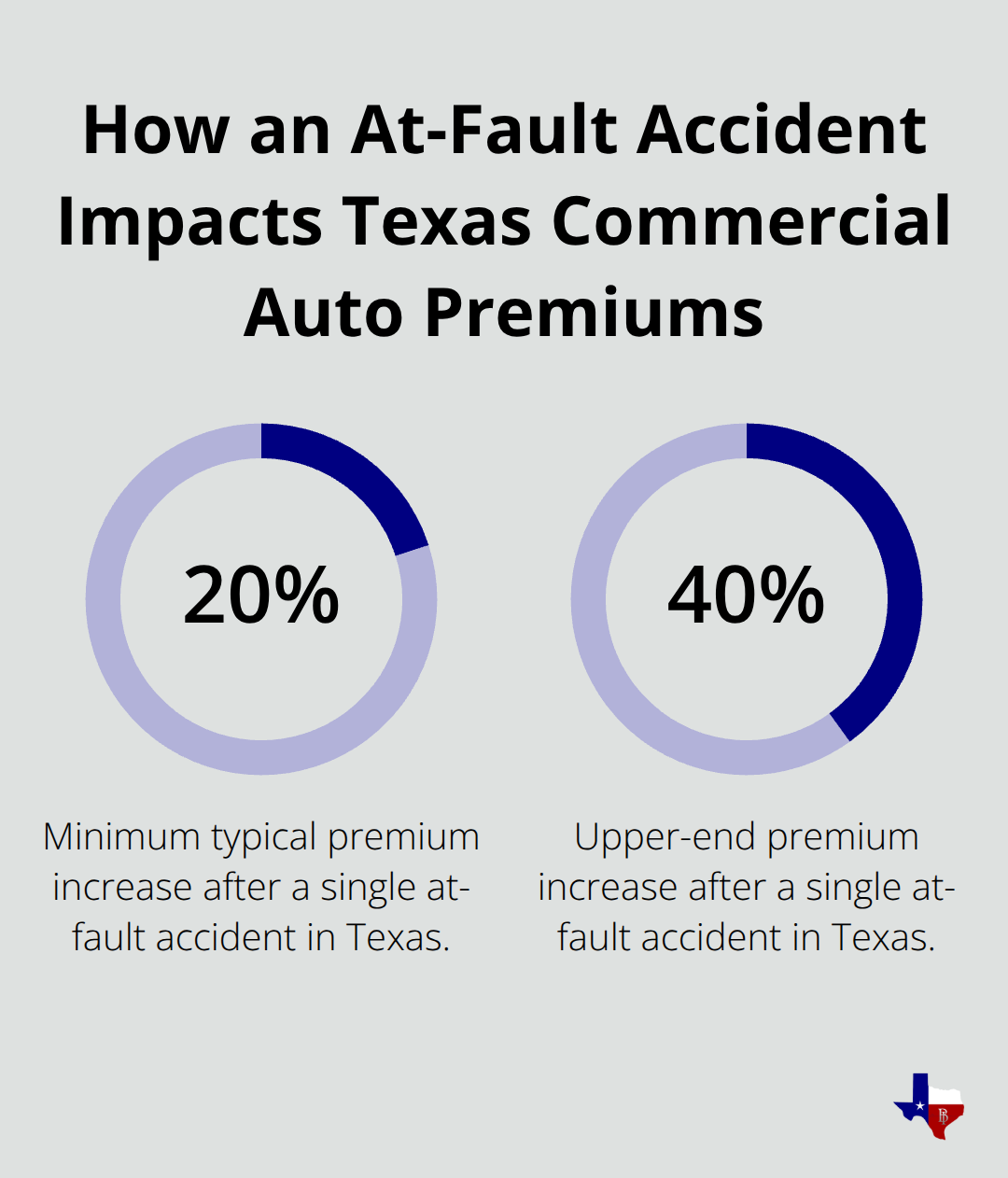

Commercial auto premiums in Texas have been subject to rate adjustments, and a single at-fault accident can increase your premiums by 20 to 40 percent, making your driving history one of the most influential pricing factors. Your location in Texas plays a role that many business owners overlook but shouldn’t. Vehicles based in high-traffic urban areas like Dallas or Houston face elevated accident risk, with I-35E in Dallas reporting more than 500 crashes per month and Houston’s I-610 loop seeing about 600 crashes monthly according to Texas DMV data.

A San Antonio contractor reduced premiums by moving operations from an urban to a safer rural location, demonstrating that geography directly affects what you pay.

Driver Records and Coverage Choices

Driver records and experience are primary pricing considerations, which is why a team member with multiple violations costs significantly more to insure than one with a clean record. Coverage limits you select have substantial impact on your bottom line, since higher liability limits raise premiums noticeably, while higher deductibles can reduce them. For example, moving from standard limits to 2 million dollars in liability coverage can add 15 to 25 percent to your annual premium. Telematics and driver risk programs help insurers price coverage more accurately and can support discounts when you implement anti-theft systems and collision-avoidance technology, signaling lower risk and reducing your pricing.

Industry Type and Claims History

Installation contractors average about 299 dollars monthly for commercial auto coverage compared to nonprofits at around 168 dollars monthly, based on Insureon data covering approximately 100,000 small business owners. Industry and business type shape your costs substantially, since trucking and construction businesses typically pay higher rates than office-based or retail operations. Claims history heavily affects what insurers charge you going forward, since frequent or costly claims raise premiums while a clean claims record helps lower rates. Once you understand these rate factors, the next step involves preparing the specific information insurers need to generate accurate quotes for your business.

What Information You Need Before Requesting Quotes

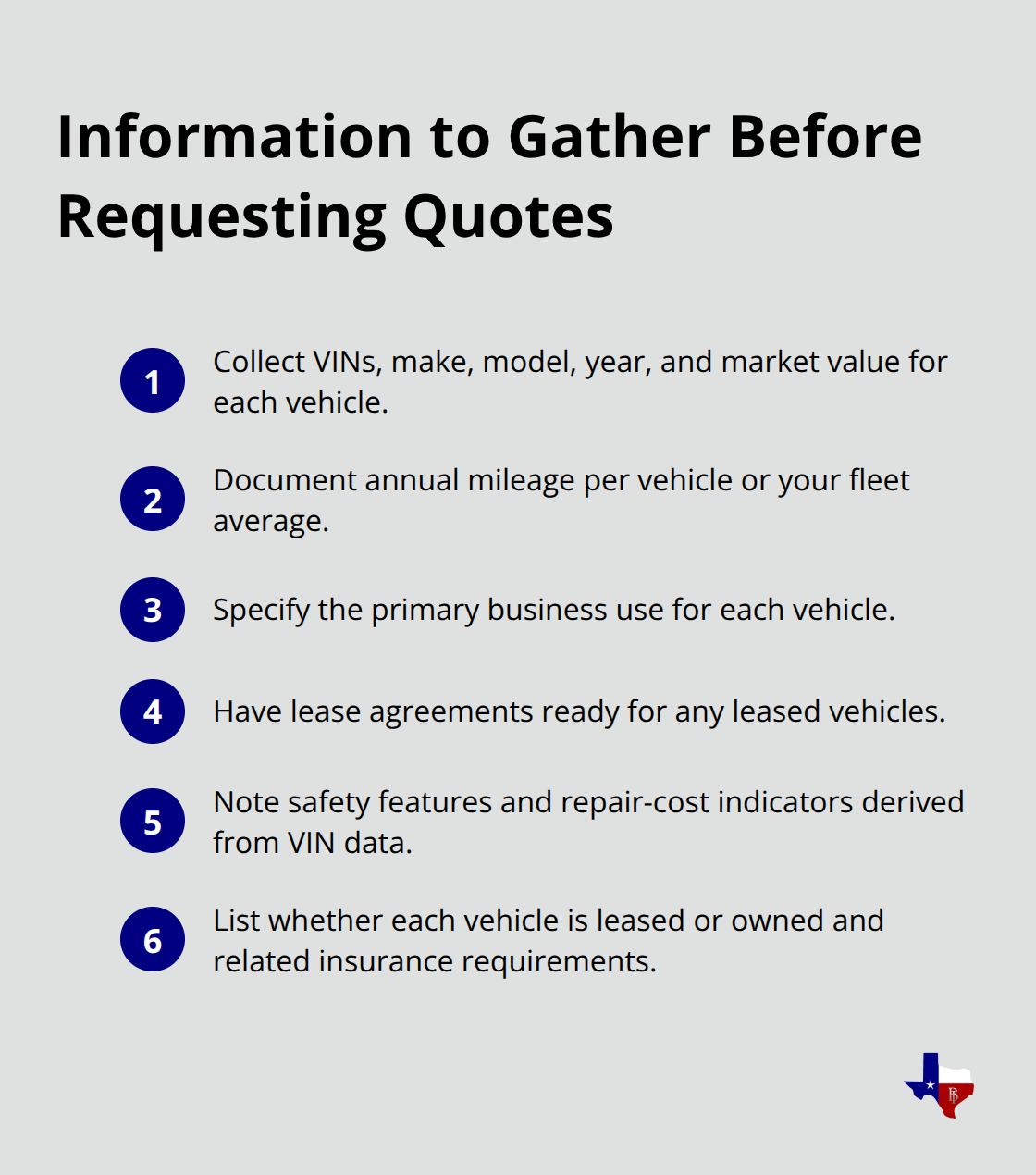

Insurers require specific details to generate accurate quotes, and missing information often results in estimates that don’t reflect your actual risk. Gather your vehicle identification numbers (VINs) for every vehicle you want to insure, along with the make, model, year, and current market value of each. Insurance companies use VIN data to assess repair costs and safety features, so having this ready prevents delays and ensures quotes account for the actual vehicles in your fleet.

Document annual mileage for each vehicle or your fleet average, since vehicles with heavy usage of 50,000 or more miles annually command higher premiums than those with moderate mileage. Note the primary business use for each vehicle-whether it’s local delivery, long-haul trucking, construction site transport, or client visits-because usage patterns directly affect how insurers price your coverage. If any vehicles are leased rather than owned, have your lease agreements available, as leasing companies often impose specific insurance requirements that impact your quote.

Driver Information Shapes Your Rate Significantly

Collect driver’s license information and full legal names for every person who operates a company vehicle, including employees and owners. Insurers will conduct motor vehicle record checks on all drivers, so having this information ready accelerates the quoting process. If your business has experienced any at-fault accidents or claims in the past three to five years, compile those details now-dates, claim amounts, and what happened-since a single at-fault accident can increase premiums according to the Texas Department of Insurance. A clean driving history for your team represents one of the most valuable assets in reducing your rates. Disclose violations, suspensions, or other driving infractions honestly, because insurers will discover them anyway, and misrepresenting driver records can invalidate your coverage later. If you’ve enrolled any drivers in defensive driving courses, document that as well, since some Texas insurers offer discounts for completed safety training programs.

Coverage Limits and Deductible Strategy

Determine what liability limits make sense for your business before requesting quotes. Texas minimum liability coverage is 30,000 dollars per person and 60,000 dollars per accident for bodily injury, plus 25,000 dollars per accident for property damage, but most insurers recommend around 1 million dollars in liability coverage for commercial operations. If your business handles high-value cargo or operates in sectors like construction or oil and gas, you may need higher limits. Decide whether you want collision coverage, which pays to repair or replace your vehicles after an accident, and comprehensive coverage, which handles theft, vandalism, or weather damage. Consider uninsured motorist coverage as well, since it protects your business when involved in an accident with an uninsured or underinsured driver-this is particularly important in Texas given the prevalence of uninsured drivers on busy corridors. Choose a deductible amount you can actually afford to pay out of pocket if a claim occurs, because higher deductibles reduce your monthly premium but require more cash reserves. One Houston delivery service saved about 12 percent on premiums by raising their deductible while maintaining core coverage, demonstrating that this strategy works when your cash flow allows it. If you use vehicles your business doesn’t own (such as rental trucks or employee personal vehicles for work tasks), mention this to insurers so they can quote hired and non-owned auto coverage, which extends liability protection without covering repairs to those vehicles.

With your fleet details, driver information, and coverage preferences documented, you’re ready to contact insurers and request quotes that accurately reflect your business operations.

How to Compare Quotes and Find Your Best Option

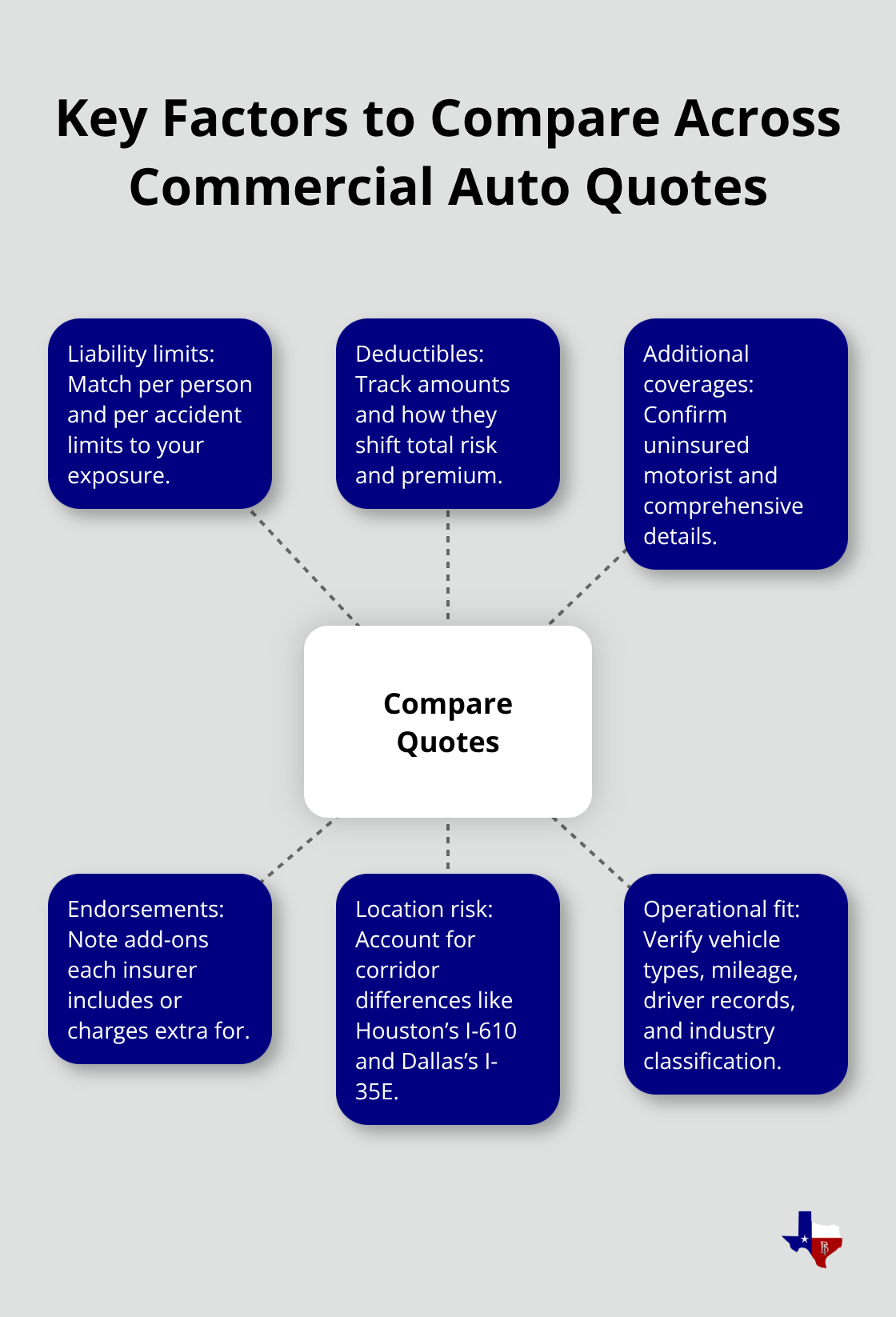

Once you submit your information to multiple insurers, you’ll receive quotes that may vary significantly in price and coverage. The difference between the lowest quote and the highest can easily exceed 30 to 40 percent, which means taking time to evaluate properly will pay off. Don’t simply choose the cheapest option, since a lower premium often reflects reduced coverage or higher deductibles that could leave your business exposed. Instead, pull together all the quotes you receive and create a simple spreadsheet comparing liability limits, deductible amounts, additional coverages like uninsured motorist protection and comprehensive coverage, and any endorsements each insurer includes. Note which quotes include hired and non-owned auto coverage if your business uses leased or employee vehicles. Check whether each quote factors in your location risk accurately, since Houston’s I-610 loop and Dallas’s I-35E experience 600 and 500 crashes monthly respectively, and insurers price these corridors differently based on their actual underwriting. Verify that each quote accounts for your specific vehicle types, annual mileage, driver records, and industry classification, because quotes missing these details won’t be reliable once you bind coverage.

Compare Coverage Details Side by Side

Create columns for each insurer and list the exact liability limits they offer (per person and per accident), deductible amounts, and whether they include uninsured motorist coverage. Note any additional endorsements like medical payments coverage, collision, comprehensive, towing, or bobtail coverage if your fleet includes tractors. Some insurers add these automatically while others charge extra, so this comparison reveals true cost differences. Check the policy language for uninsured motorist coverage to confirm it defines “underinsured motor vehicle” properly, since Texas law requires specific language that affects your actual protection. If your business operates in construction, oil and gas, or other high-risk sectors, verify that each quote reflects appropriate limits for your industry risk profile.

Evaluate Insurer Reputation and Claims Handling

The Texas commercial auto market includes more than 80 insurers available through independent brokers, giving you genuine options beyond household names. Progressive leads the market as the largest commercial auto insurer in the U.S. according to the Insurance Information Institute, while Travelers ranks second with relatively few complaints compared to its market share. Cincinnati Insurance finished second in JD Power’s 2025 U.S. Small Commercial Insurance Study and had significantly fewer complaints from 2022 to 2024 than competitors. American Family Insurance scores above average on JD Power ratings and can issue online quotes in minutes, while Auto-Owners Insurance demonstrates strong financial strength with 24/7 roadside assistance included. Allstate, Geico, and State Farm actually show more complaints relative to their commercial auto market share, making them less ideal choices despite their brand recognition.

Check Complaint Data and Claims Speed

Check NAIC complaint data before deciding, since this three-year average reveals which insurers handle claims efficiently and respond to customer concerns. An insurer with fewer complaints relative to its size typically delivers faster claims processing and better customer service when you actually need coverage. Contact each insurer’s claims department directly and ask about their average claims resolution time and whether they offer digital claim filing, since a carrier that settles claims quickly reduces your business disruption and cash flow pressure.

Identify Additional Discounts and Programs

Some carriers now provide telematics programs that monitor driver behavior and can generate discounts if your team maintains safe driving habits, so ask about these options during the quote process. These programs identify additional savings you might not see listed on the initial estimate. Inquire whether each insurer offers discounts for bundling commercial auto with general liability or other business coverages, since this strategy can reduce your overall costs substantially. Ask if they provide discounts for completed defensive driving courses or safety certifications your drivers have earned.

Final Thoughts

Accurate Texas commercial auto quotes require preparation and comparison, not guesswork. You now understand the rate factors that matter most-vehicle type, driver history, location risk, and coverage limits-and you know exactly what information insurers need to generate reliable estimates. The effort you invest upfront in documenting your fleet details, driver records, and coverage preferences directly translates to quotes that reflect your actual business operations.

Comparing multiple quotes reveals significant price differences, often 30 to 40 percent between the lowest and highest options, because different insurers assess risk differently and offer different coverage combinations. Your responsibility is matching the right coverage to your business needs at a price that works for your budget, not simply selecting the cheapest option available. Review each quote’s liability limits, deductibles, additional endorsements, and the insurer’s reputation for claims handling before you make your final decision.

We at Brooks Insurance represent multiple top-rated carriers, which means you have access to a larger selection of coverage options, pricing, and payment plans tailored to your specific situation. Our licensed agents understand Texas commercial auto requirements and can help you navigate the quote process, identify coverage gaps, and find discounts you might otherwise miss. Contact Brooks Insurance today to request quotes from our network of carriers and select coverage that protects your business.

Disclaimer: The information provided in this blog is for general informational purposes only and does not constitute legal, financial, or insurance advice. Coverage options, terms, and availability may vary. Please consult with a licensed professional for advice specific to your situation