One lawsuit can drain your business finances and damage your reputation for years. General liability risk management isn’t optional-it’s how smart business owners protect what they’ve built.

At Brooks Insurance, we’ve seen firsthand how the right strategies and coverage prevent costly claims from becoming catastrophic losses. This guide walks you through the risks your business faces and the practical steps to manage them.

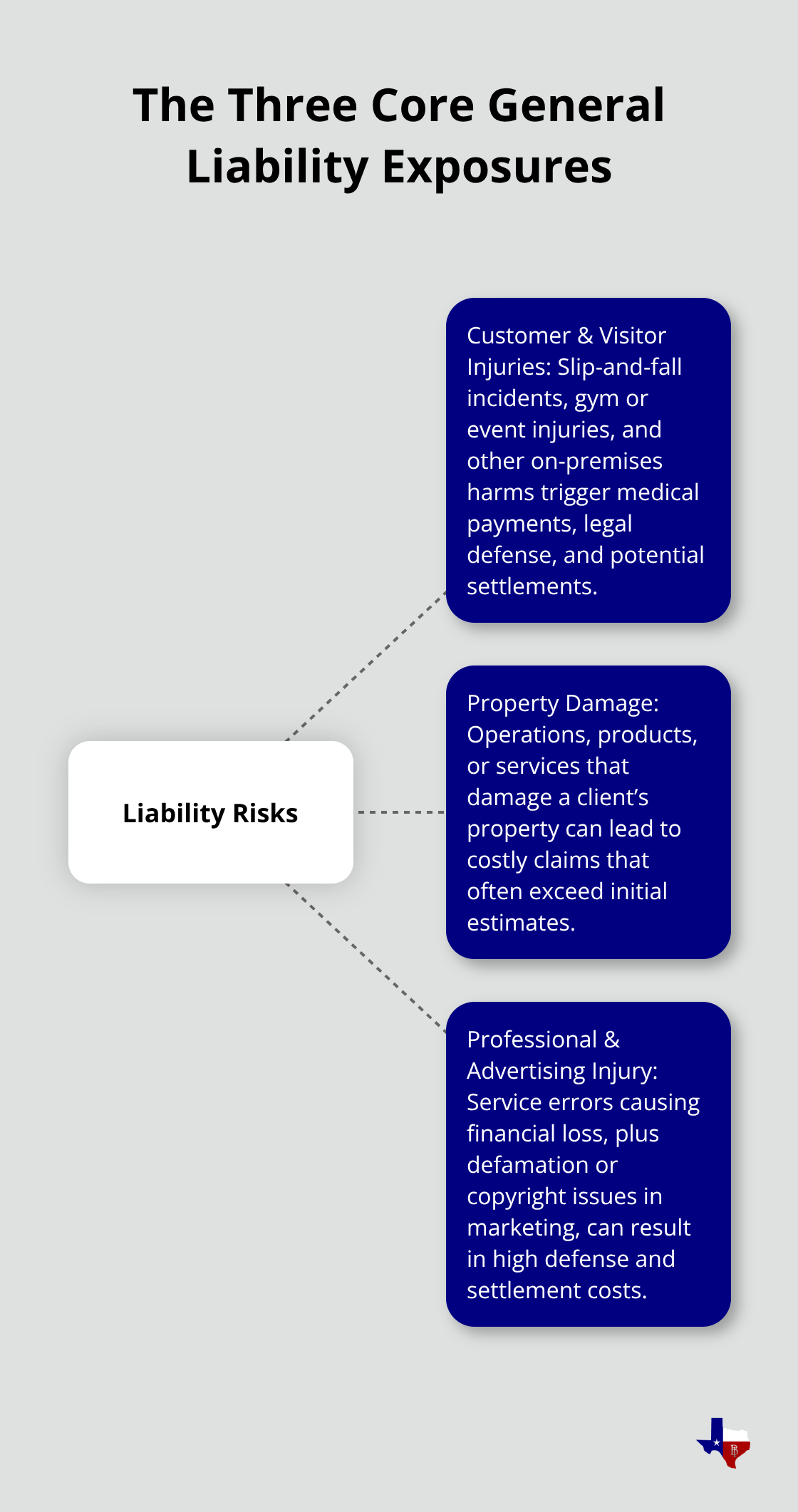

What Liability Risks Actually Threaten Your Business

Slips and falls on your premises, injuries from products you sell, damage to customer property, and claims that your work harmed someone financially-these aren’t hypotheticals. According to the National Safety Council, workplace injuries cost American businesses approximately $163 billion annually in direct and indirect expenses. In Texas specifically, nonfatal workplace injuries totaled 175,900 in 2023, with the most common incidents involving overexertion from lifting, slips on wet floors or clutter, impacts from falling objects in construction, and burns in food service. Your business faces real exposure here.

Customer and Visitor Injuries Lead the Claims

A customer who slips in your retail location and breaks their leg can sue for medical bills, lost wages, and pain and suffering. A contractor you hired damages a client’s equipment on a job site. An employee makes a careless comment that harms someone’s reputation or business. These situations happen constantly, and they cost money. General liability insurance covers third-party bodily injury, property damage, personal injury claims like defamation, and medical payments for others, plus your legal defense costs. But insurance alone isn’t enough-you need to understand your actual exposures first.

Customer and visitor injuries represent the largest category of general liability claims. Retail businesses, restaurants, gyms, and service providers with foot traffic face the highest frequency. A customer trips over a box in your store, a guest at your event gets injured, or someone is hurt using your service. The cost of even a minor injury claim-medical treatment, legal fees, settlement-typically ranges from thousands to tens of thousands of dollars.

Property Damage Liability Adds Up Quickly

Property damage liability is equally serious. If your business operations, products, or services damage someone else’s property, you’re liable. A contractor accidentally damages a client’s existing structure. A product you manufacture or distribute fails and destroys customer equipment. A delivery driver hits a parked car. These claims pile up fast and often exceed initial estimates.

Professional Liability and Advertising Injury Hit Service Businesses Hard

Professional liability and advertising injury claims target service-based businesses especially hard. If you provide advice, design work, consulting, or creative services, clients expect results. When they claim your work caused them financial loss, they’ll sue. Advertising injury claims-covering defamation, copyright infringement, or misrepresentation in your marketing-hit businesses that advertise aggressively. Your industry and operational model determine which exposures matter most, but service businesses face significant professional liability exposure, with actual claim payouts reaching hundreds of thousands of dollars when settlements and defense costs combine.

Understanding these three liability categories helps you identify which exposures matter most to your operation. The next section shows you how to build practical strategies that reduce claim frequency and severity before they happen.

How to Build a Risk Management System That Actually Works

Reducing liability claims starts with systems, not luck. The businesses that avoid costly claims aren’t the lucky ones-they’re the ones with documented safety protocols, clear training programs, and regular coverage reviews. A business that implements structured safety training reduces injury frequency significantly. Texas nonfatal workplace injuries declined 13% from 2023 to 2025, with the steepest drops occurring in industries that invested in formal safety programs. The reason is straightforward: when employees know what they’re doing wrong, they stop doing it.

Identify Hazards and Train Your Team

Start by identifying the specific hazards in your operation. Retail businesses need slip-and-fall prevention. Construction companies need fall protection and equipment safety. Restaurants need burn and cut prevention. Food service operations should train staff on proper footwear, floor maintenance, and hazard signage. Once you know your hazards, build training around them and require every employee to complete it annually. Document that training happened-dates, attendees, topics covered. This documentation becomes critical evidence if a claim arises, showing an insurer that you took reasonable precautions.

Create and Maintain Incident Records

Documentation and record-keeping separate businesses that win claims from those that lose them. When a customer claims they slipped in your store three months ago, you need incident reports, maintenance logs, and witness statements from that exact date. Without them, you’re fighting blind. Create a simple incident log that captures date, time, location, what happened, who was involved, injuries reported, and corrective action taken. Photograph hazardous conditions before fixing them. Keep maintenance records for equipment, flooring, and facilities-these prove you weren’t negligent.

For service businesses, document client communications, project scope, deliverables, and acceptance criteria in writing before work starts. This prevents the professional liability nightmare where a client claims you promised something you didn’t deliver. Texas contract law is strict about written terms, so precision matters.

Review Coverage When Operations Change

Schedule a comprehensive coverage review annually, not just at renewal. Business operations change-you add a new service line, hire contractors, expand to a new location, or launch an advertising campaign. Each change shifts your liability profile. Review your general liability policy against your current operations. Check that your liability limits match your exposure level. If you operate in multiple locations or manage high-risk activities, your coverage may be inadequate.

These three practices-hazard identification with training, detailed documentation, and regular coverage assessment-form the foundation of effective risk management. The next section explains why general liability insurance itself matters as the final layer of protection when prevention alone isn’t enough.

Why Insurance Protects What Prevention Alone Cannot

Prevention reduces claims, but it doesn’t eliminate them. A customer can still slip despite your best safety efforts. A product defect can still cause damage. An employee can still make a costly mistake. General liability insurance fills the gap between what you prevent and what actually happens. Without it, a single serious claim depletes your business reserves, forces you to choose between paying medical bills and making payroll, and potentially forces closure. With it, an insurer covers defense costs, settlements, and judgments up to your policy limits, letting you stay operational while the claim resolves.

Protection Against Financial Shock

This protection matters most in Texas, where the state’s economy drives high commercial activity and litigation is common. A contractor’s accidental damage to a client’s property, a restaurant customer’s burn injury, or a service provider’s professional error can each result in claims exceeding $50,000 when medical costs, legal fees, and settlements combine. General liability insurance absorbs that financial shock instead of your business absorbing it.

Tailored Coverage Matches Your Actual Exposures

Your policy can be tailored to match your actual exposures through endorsements and coverage options. If you operate multiple locations, you add each one. If you hire contractors, you add hired and non-owned auto liability. If you provide professional services, you add professional liability coverage. If you advertise, you add advertising injury protection.

This customization means you avoid overpaying for irrelevant coverage or underpaying for gaps. The typical cost for general liability in Dallas ranges from $40–$80 per month depending on your industry, location, and claims history-far less than the cost of defending even a minor lawsuit out of pocket.

Coverage Strengthens Your Business Relationships

Carrying documented general liability insurance changes how you’re perceived in business relationships. Clients, vendors, and partners expect proof of coverage before engaging with you. When you provide a certificate of insurance showing active coverage with reputable insurers, you signal that you’re a stable, responsible business. Without it, you lose contracts, appear unprofessional, and face pressure to explain why you’re uninsured. In Texas, many service contracts explicitly require proof of general liability insurance, so coverage becomes a business requirement, not just a safety net.

Final Thoughts

General liability risk management works best when prevention and insurance work together. You’ve learned how to identify your actual exposures, build systems that reduce claim frequency, and understand why coverage matters when prevention alone falls short. The businesses that thrive in Texas aren’t the ones hoping nothing goes wrong-they’re the ones with documented safety protocols, clear incident records, and active general liability insurance backing their operations.

Your next step is straightforward: schedule a risk assessment with a qualified broker who understands your specific industry and operations. Bring your current policies, recent incident reports, and a list of your main liability concerns. A thorough assessment takes a few hours but reveals gaps you might not see on your own, and it helps you review your coverage limits against your actual exposures. If you operate in high-risk industries like construction, food service, or professional services, your limits may need adjustment.

We at Brooks Insurance work with Texas businesses to assess their coverage needs and find solutions that match their actual risk profile. As an independent agency, we represent multiple top-rated insurance companies, giving you access to a larger selection of coverage options and pricing. Contact Brooks Insurance to schedule your free annual risk assessment and get a quick certificate of insurance for your contracts.

Disclaimer: The information provided in this blog is for general informational purposes only and does not constitute legal, financial, or insurance advice. Coverage options, terms, and availability may vary. Please consult with a licensed professional for advice specific to your situation