Starting a business in Texas means taking on new risks you’ve never faced before. General liability for startups isn’t optional-it’s the foundation that protects your company when customers get hurt or property gets damaged on your watch.

At Brooks Insurance, we’ve seen firsthand how quickly a single incident can derail a young business. The right coverage gives you peace of mind and shows your clients and partners that you take responsibility seriously.

Why General Liability Protects Your Startup

The Real Cost of Uninsured Claims

A single incident can cost your startup thousands in medical bills, legal fees, and settlements. General liability insurance covers what happens when a customer trips in your office, a visitor’s property gets damaged during your operations, or your marketing accidentally injures someone’s reputation. A San Antonio shop faced a $45,000 bodily injury claim and relied on general liability to cover both the defense costs and the settlement-a loss that would have devastated an uninsured startup. Defense costs alone for advertising or marketing claims can reach around $15,000 per incident, showing how quickly legal expenses accumulate even before a claim gets resolved.

Understanding Premium Costs and Coverage Limits

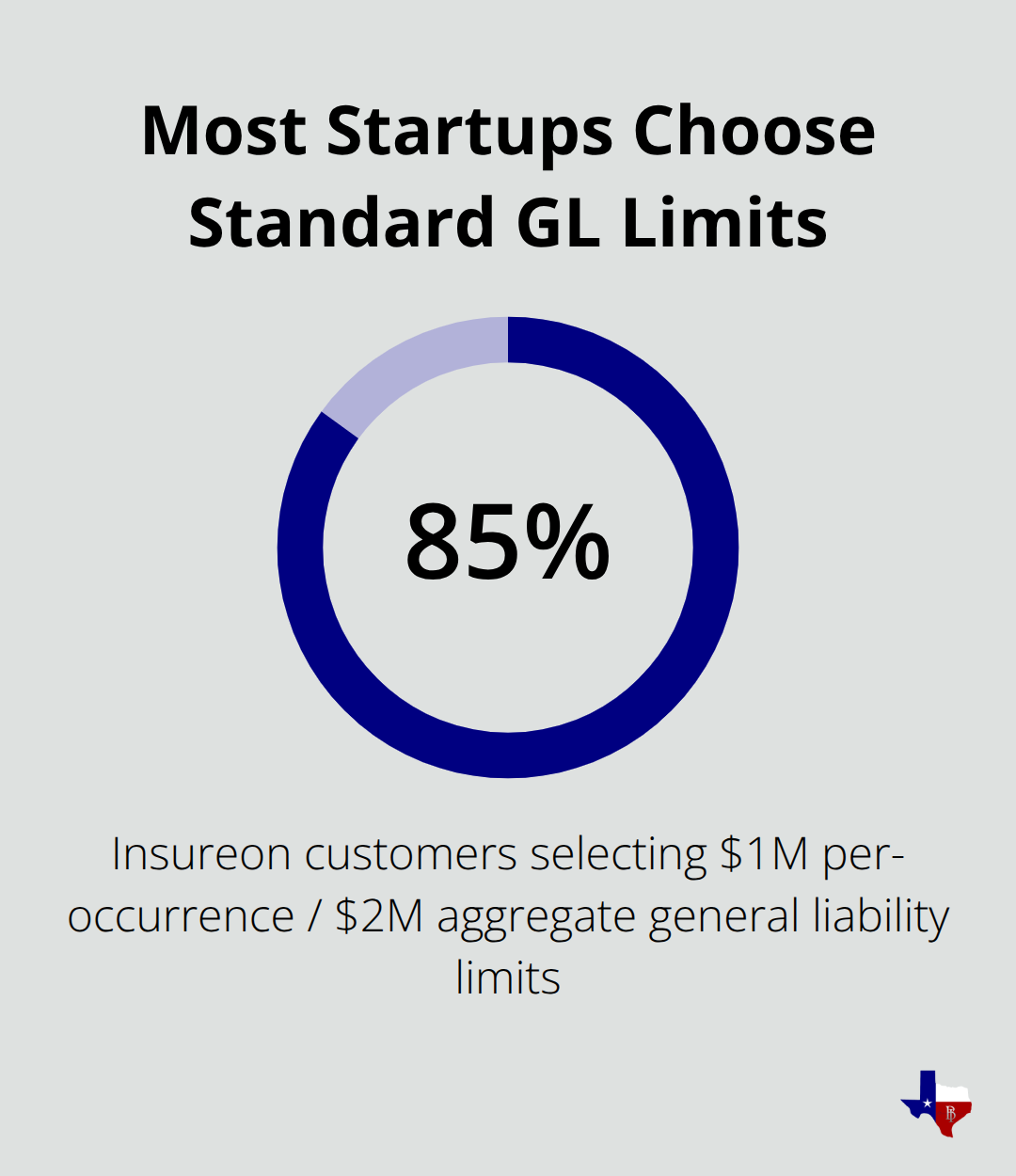

According to data from Insureon’s analysis of 100,000 small business policies, the average general liability premium runs about $45 per month, with annual costs typically ranging from $250 to $3,000. Most startups choose $1,000,000 per-occurrence and $2,000,000 aggregate limits-about 85% of Insureon customers select this baseline combination. A coffee shop open to the public averages about $47 per month in Texas, while an IT consultant working from home averages about $32 per month.

Your industry and location determine your rates more than anything else.

Why Landlords and Lenders Demand Coverage

70% of Texas small businesses carry general liability insurance. Lenders and investors also expect to see this coverage in place. If you hire employees, workers’ compensation becomes mandatory under Texas law, but general liability protects your business from third-party claims separate from employee injuries.

Selecting Limits and Deductibles That Fit Your Business

The right coverage limits depend on your revenue, employee count, and premises size. Higher revenue generally increases premiums, though office-based service businesses experience less impact than construction or manufacturing operations. Deductibles commonly fall between $500 and $1,000, and you should choose one you can actually afford-that’s your out-of-pocket cost when a claim happens. Bundling general liability with commercial property coverage through a business owner’s policy typically saves 12–18% versus buying separate policies, a meaningful reduction for startups managing tight budgets.

Understanding your specific risks and coverage needs sets the stage for the next critical decision: identifying which liability exposures pose the greatest threat to your startup’s survival.

What Liability Risks Actually Threaten Your Startup

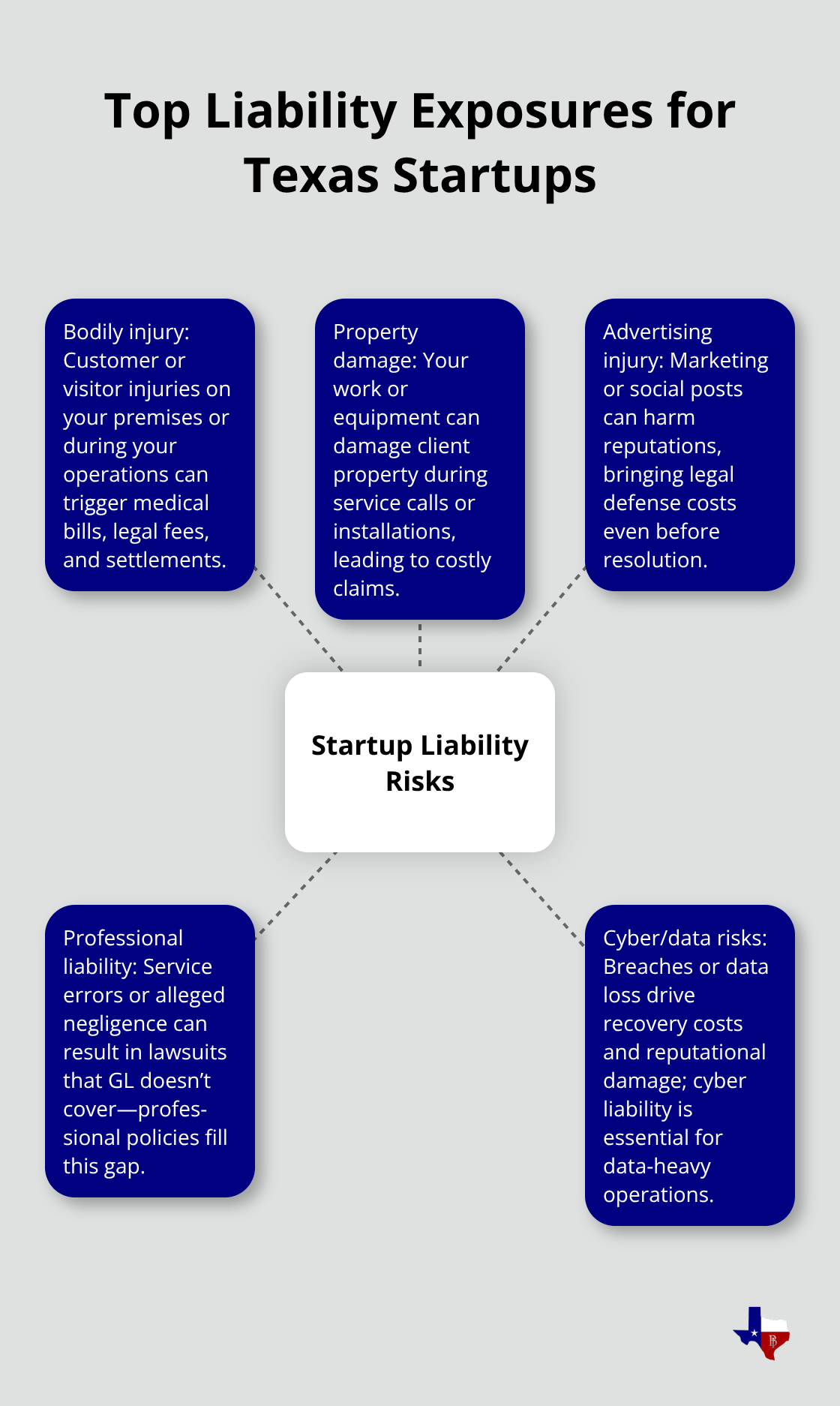

Every startup operates in a web of liability exposure that extends far beyond what founders typically anticipate. A customer slips on wet flooring in your retail space, a vendor’s equipment gets damaged during your installation work, or your social media post inadvertently harms someone’s reputation-these scenarios happen regularly. According to SBA data, about 25% of small businesses face employee-related or third-party claims within a decade, which means substantial odds that you’ll encounter at least one incident requiring coverage. The Texas Department of Insurance reports that non-compliance with basic liability requirements triggers fines up to $25,000 per violation, making proper coverage not just a risk management tool but a legal necessity. Most Texas commercial leases demand general liability insurance as a condition of occupancy, with about 80% of urban commercial landlords requiring it before you sign.

Bodily Injury Claims from Customers and Visitors

Bodily injury claims from customers or visitors represent the most common trigger for general liability payouts. A Dallas restaurant experienced a $20,000 knee-injury claim that workers’ compensation didn’t cover because the injured party wasn’t an employee-general liability stepped in to handle the full cost. Slip-and-fall incidents, allergic reactions to products, or injuries from defective equipment all fall under this category. Your startup faces liability the moment customers or visitors step onto your premises or interact with your services.

Property Damage and Operational Liability

Property damage caused by your business operations extends far beyond obvious scenarios. If your team accidentally damages a client’s building during a service call or your equipment ruins someone else’s inventory, you’re liable. These incidents occur frequently in construction, installation, and service-based industries where your work directly affects client property. The financial exposure can reach tens of thousands of dollars without proper coverage in place.

Advertising Injury and Professional Liability

Advertising injury claims are often overlooked by startups, yet defensive costs for these claims alone can reach around $15,000 per incident, according to industry data. A San Antonio shop discovered this the hard way when a marketing campaign created a $45,000 exposure that general liability covered entirely. Professional liability exposure affects service-based startups especially hard-a Dallas consulting firm faced a $40,000 lawsuit for alleged negligence in their work, and professional liability insurance absorbed the legal defense and settlement costs. Texas’s service sector grew about 4.8% in 2024 according to the Texas Economic Development Corporation, meaning more startups enter fields where professional liability becomes critical.

Cyber and Data-Related Exposures

If your startup handles any client data or relies on digital operations, cyber liability becomes essential. 43% of cyberattacks target small businesses, with average recovery costs around $120,000. Texas’s tech workforce expanded about 3.9% in 2024 according to CompTIA, underscoring how many startups now operate in data-intensive environments. A breach or data loss can devastate your reputation and finances without proper cyber coverage.

Identifying Your Specific Risk Profile

The specific risks your startup faces depend entirely on your industry, location, and operational model. A retail business faces different exposures than a consulting firm or a construction company. Your premises size, employee count, and the nature of your customer interactions all shape your liability profile. Selecting appropriate coverage limits matters more than chasing the lowest premium available-mismatched coverage leaves dangerous gaps when claims actually occur. Understanding which exposures pose the greatest threat to your startup’s survival sets the stage for the next critical decision: determining the right coverage limits and policy structure for your specific situation.

Picking Coverage Limits That Match Your Real Exposure

Your industry determines your baseline coverage needs more than anything else, and selecting the wrong limits leaves you exposed when claims arrive. A coffee shop needs different limits than a consulting firm, which needs different limits than a construction company. Start by examining what similar businesses in your field carry-not because it’s trendy, but because they’ve already learned what claims cost in your sector. According to Insureon’s analysis of 100,000 small business policies, about 85% of startups choose $1,000,000 per-occurrence and $2,000,000 aggregate limits, and this combination works for most service and retail operations. However, if your startup involves installation work, equipment use, or higher-risk customer interactions, you should seriously consider $2,000,000 per-occurrence and $4,000,000 aggregate limits-roughly 8% of Insureon customers select this tier because their exposure justifies it. The San Antonio shop that faced a $45,000 bodily injury claim would have been fine with standard limits, but a construction startup installing commercial systems might face claims triple that amount.

When unsure about coverage limits appropriate for your industry and business type, it’s wise to consult a broker to determine appropriate limits based on the specific industry and level of risk.

Selecting Your Deductible Strategy

Your deductible matters equally to your coverage limits. Choose between $500 and $1,000 based on what you can actually afford to pay out of pocket when a claim happens. Too many startups pick low deductibles to feel safer, then face premium increases that hurt their cash flow worse than the deductible ever would. A higher deductible reduces your monthly premium significantly, which matters when you’re managing tight startup budgets.

Location, Employees, and Cost Factors

Location and employee count push your costs higher or lower, so factor these into your comparison. Texas commercial leases demand general liability in about 80% of urban markets, which means your landlord will specify minimum limits-don’t negotiate below what your lease requires. If you have employees, workers’ compensation becomes mandatory under Texas law regardless of your startup size, and this separates from general liability because it covers employee injuries specifically.

Bundling Policies for Maximum Savings

Bundling general liability with commercial property coverage through a business owner’s policy saves you 12–18% versus buying policies separately, according to industry data-an Austin retail startup saw about 14% savings this way. This approach reduces your total premium while simplifying your coverage management.

Shopping Rates and Verifying Your Agent

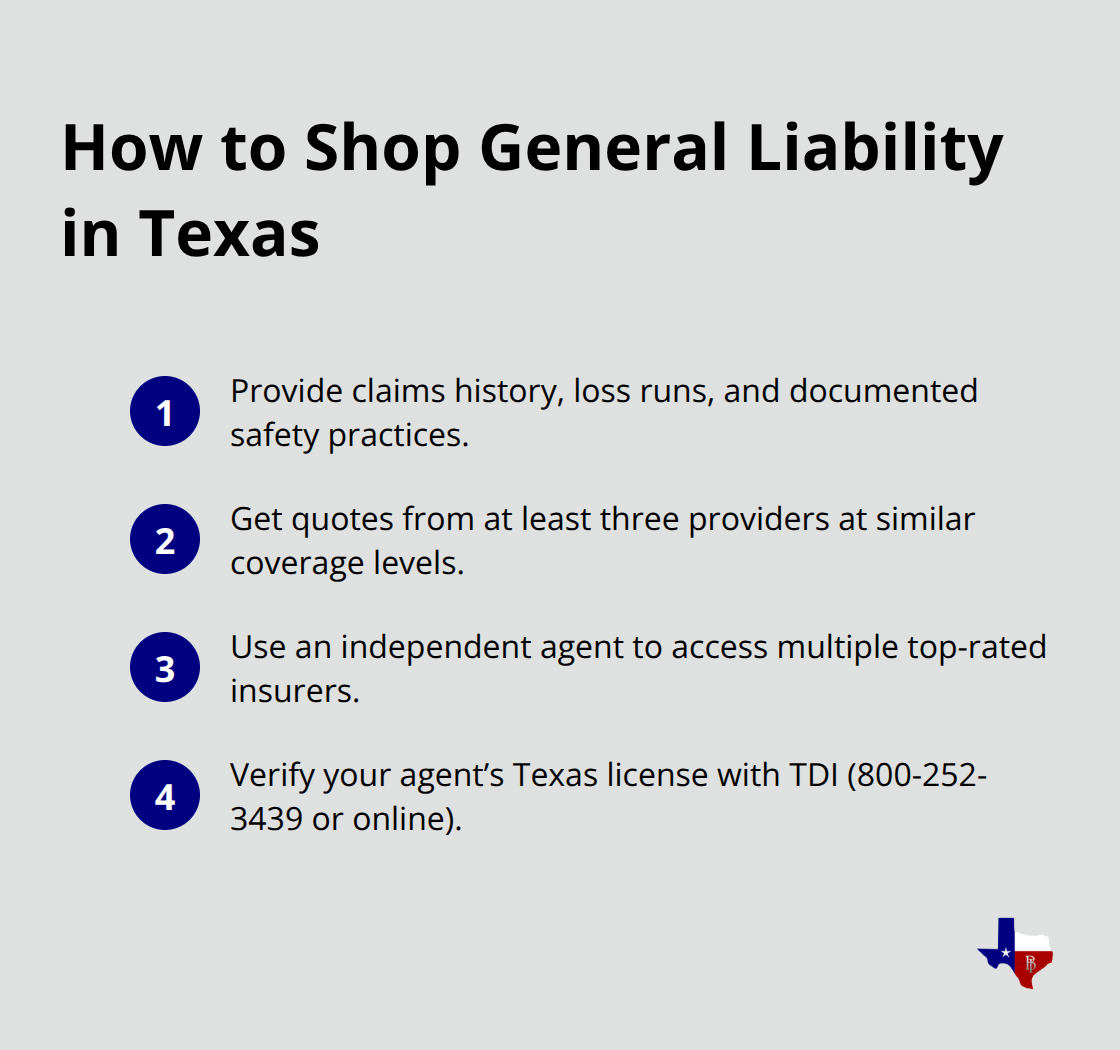

When you shop rates, provide your claims history, loss runs, and detailed risk management practices to agents; startups that document their safety procedures and training programs receive better quotes than those offering vague descriptions.

Get quotes from at least three different providers because rates vary significantly based on how each insurer assesses your specific risk profile. An independent agent can access multiple top-rated insurers simultaneously, saving you time and often delivering better pricing than shopping direct with individual companies. Verify that your agent holds a Texas license by checking with the Texas Department of Insurance at 800-252-3439 or through their online lookup tool-unlicensed agents create compliance problems that cost far more than any premium savings.

Final Thoughts

General liability for startups protects your business from the financial devastation that follows a single incident. You’ve learned that coverage costs as little as $45 per month for many startups, that most Texas landlords require it before you sign a lease, and that a single uninsured claim can cost tens of thousands of dollars. The $1,000,000 per-occurrence and $2,000,000 aggregate limits work for most service and retail operations, though your specific industry may demand higher protection.

Your next step is straightforward: gather your business details, claims history if you have one, and information about your premises and operations. Contact multiple insurance providers to compare quotes at similar coverage levels, then select the policy that matches both your risk profile and your budget. Bundling general liability with commercial property coverage through a business owner’s policy saves 12–18% compared to separate policies, a meaningful reduction when you’re managing startup cash flow.

At Brooks Insurance, we represent multiple top-rated insurance companies, which means you get access to a larger selection of coverage options and pricing than you would shopping with a single carrier. Our licensed agents understand Texas requirements and can help you avoid the compliance mistakes that trigger fines up to $25,000 per violation. Contact us today to get quotes and secure the protection your startup deserves.

Disclaimer: The information provided in this blog is for general informational purposes only and does not constitute legal, financial, or insurance advice. Coverage options, terms, and availability may vary. Please consult with a licensed professional for advice specific to your situation