Commercial vehicles face unique risks on Texas roads. At Brooks Insurance, we help business owners find the best commercial auto insurance that matches their actual needs and budget.

Your policy should protect both your vehicles and your bottom line. We’ll walk you through what coverage options exist, what affects your rates, and how to pick the right protection for your business.

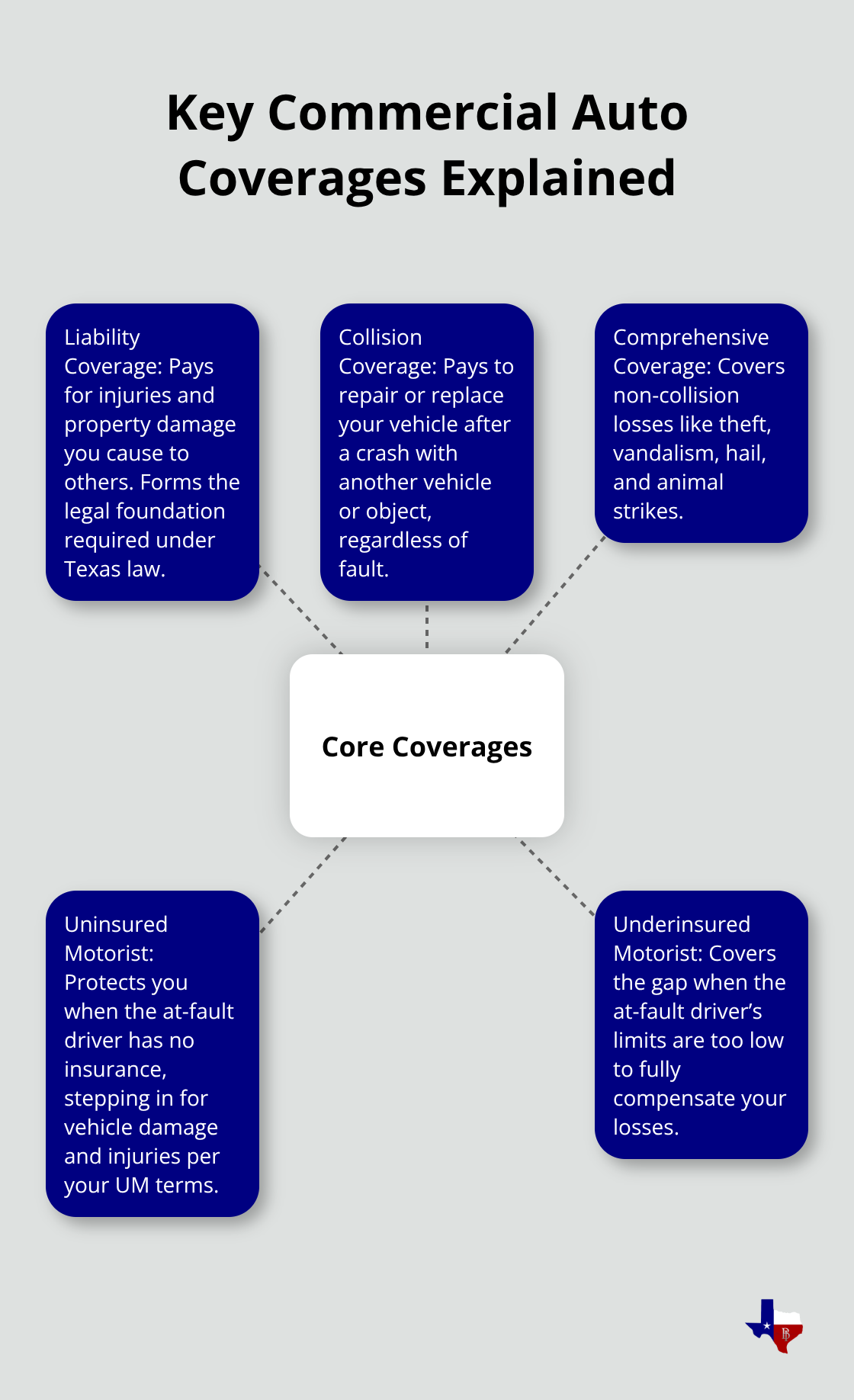

What Your Commercial Auto Insurance Actually Covers

Liability Coverage: Your First Line of Defense

Liability coverage is non-negotiable in Texas. State law requires a minimum of 30/60/25, meaning $30,000 for bodily injury per person, $60,000 per accident, and $25,000 for property damage. However, these minimums leave you dangerously exposed. If your delivery driver hits a family of four in a sedan, medical bills can easily exceed $200,000. We recommend moving to at least 100/300/100 limits for most small business operations. The premium jump is modest, but the protection difference is substantial.

Bodily injury liability covers medical expenses, lost wages, and pain and suffering for people injured in accidents your vehicle causes. Property damage liability covers repairs to other vehicles, buildings, or infrastructure. Without adequate limits, a single accident could bankrupt your business through legal judgments that exceed your policy’s maximum payout.

Collision and Comprehensive: Protecting Your Own Vehicles

Collision and comprehensive coverage protects your own vehicles rather than third parties. Collision pays for damage when your vehicle hits another car, a pole, or a ditch, regardless of fault. Comprehensive covers theft, vandalism, weather damage, and animal strikes.

Many business owners skip these coverages to save money, but that’s a tactical mistake. A food truck with refrigeration equipment and a deep fryer can cost $40,000 to $60,000 to replace, and premiums for comprehensive and collision typically run $80 to $150 monthly per vehicle. The math becomes clear when you calculate replacement costs against monthly premium increases.

Uninsured and Underinsured Motorist Coverage

Uninsured and underinsured motorist coverage protects you when the other driver caused the accident but has insufficient insurance. In Texas, roughly one in eight drivers carries no insurance. If an uninsured driver causes $15,000 in damage to your work vehicle, your uninsured motorist property damage coverage steps in.

Underinsured motorist bodily injury coverage is equally important if your driver suffers injury from someone with inadequate liability limits. This coverage pays the difference between what the at-fault driver’s insurance covers and what you’re legally entitled to recover. Most Texas businesses operating multiple vehicles should carry uninsured and underinsured motorist coverage with limits matching their liability limits.

Understanding these coverage types sets the foundation for selecting a policy that actually protects your operation. The next step involves examining what factors insurers use to calculate your rates-and how your business decisions directly impact your premiums.

What Actually Drives Your Commercial Auto Insurance Premium

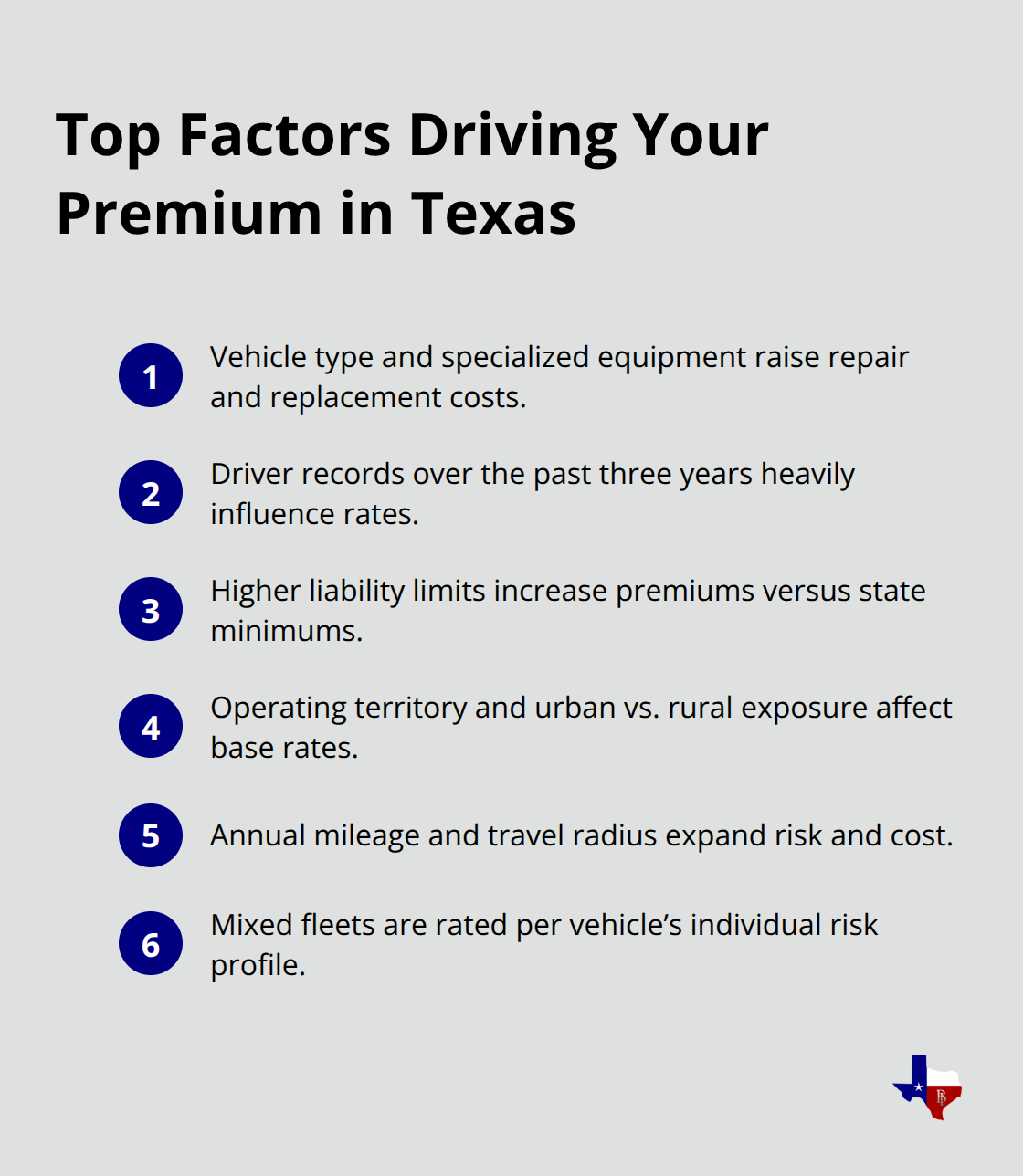

Vehicle Type Creates Your Starting Point

Your vehicle type determines risk from the moment you apply for coverage. A single sedan used for local client visits costs far less to insure than a food truck with refrigeration and deep fryer equipment. Insurers know that specialized equipment increases replacement costs and claims severity. A food truck with commercial cooking equipment typically carries higher premiums because the vehicle itself costs more to repair or replace, and the business use pattern creates additional exposure. Similarly, dump trucks and box trucks used for construction or hauling command higher rates than passenger vans.

The vehicle’s age, mileage, and repair costs all factor into the insurer’s calculation. If you operate multiple vehicle types, your premium reflects each vehicle’s individual risk profile rather than an average across your fleet.

Driver Records Shape Your Rates More Than You Think

Your drivers’ motor vehicle records shape your rates more than almost any other factor. Commercial auto insurers review the past three years of driving history for every driver with access to your business vehicles. A single at-fault accident or moving violation on one driver’s record can increase your entire fleet’s premium by 10 to 25 percent. Texas has over 3 million small businesses, and many owners underestimate how much their drivers’ records matter. If your primary delivery driver maintains a clean record for three years, that becomes your strongest negotiating point with insurers. Conversely, if you employ someone with two accidents in the past two years, expect significantly higher premiums or potential coverage restrictions. Some insurers will exclude specific high-risk drivers from coverage entirely, which requires your written acceptance. The driving history review happens at renewal too, so a driver’s recent accident discovered during renewal can trigger a substantial premium increase or nonrenewal.

Coverage Limits and Location Drive Premium Differences

Higher coverage limits increase your premium, but the relationship isn’t linear. Moving from the Texas minimum of 30/60/25 to 100/300/100 typically costs 15 to 40 percent more annually, depending on your vehicle type and location. However, a catastrophic accident involving serious injury generates damages far exceeding the minimum. If your business operates in a major Texas city like Houston or Dallas, claims activity runs heavier, and your base rates start higher than rural operations. Location matters because insurers track loss experience by territory, and urban territories with higher accident frequency command higher premiums. Your annual mileage and travel radius also influence rates. A contractor who drives 200 miles weekly within a single city pays less than one covering multiple counties. Statewide or regional travel exposes your vehicles to more hazards and increases accident probability, so your premium reflects that expanded risk zone.

Understanding these rate drivers positions you to make smarter decisions about your coverage. The next step involves assessing your specific business needs and comparing policies that actually match your operation’s risk profile.

How to Choose the Right Commercial Auto Insurance Policy

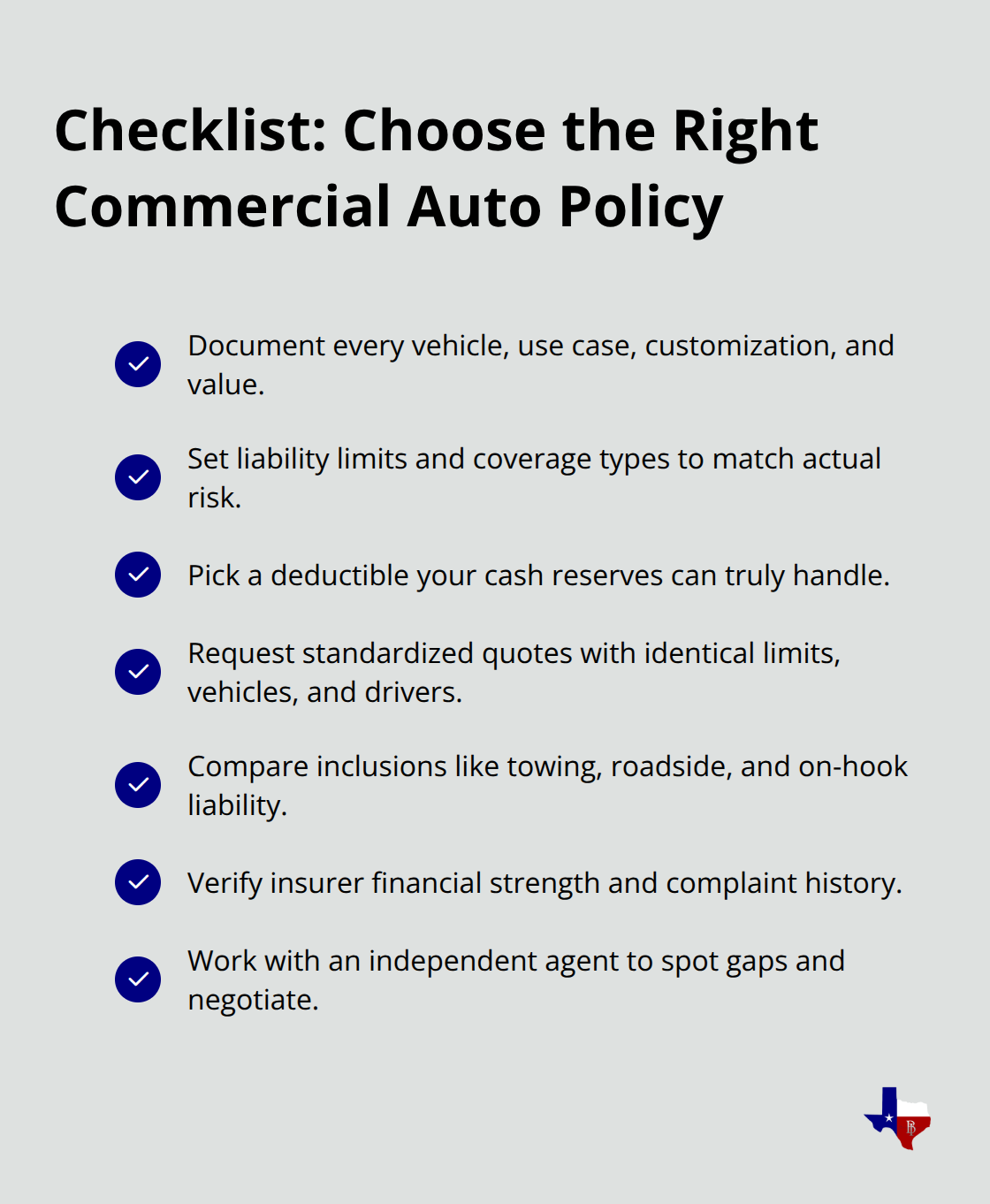

Document Your Fleet and Operation

Selecting commercial auto insurance demands a systematic approach grounded in your actual operation, not generic coverage templates. Start by documenting your fleet and operation: take inventory of all vehicles, their uses, customizations, and values to determine appropriate liability limits and coverage types. A single electrician with one service van has vastly different needs than a landscaping company running six trucks across multiple counties. Your business type determines coverage gaps that standard policies won’t address. Food trucks need higher comprehensive limits because specialized equipment replacement costs spike premiums but protects against catastrophic loss. Construction contractors operating dump trucks in multiple counties face higher rates due to expanded travel radius and increased accident exposure.

Calculate Your Deductible Capacity

Once you’ve catalogued your fleet and operation, identify your financial capacity to absorb losses. A deductible of $1,000 per incident cuts premiums by roughly 15 to 20 percent compared to a $500 deductible, but only if you can cover that amount from cash reserves when an accident happens. Many business owners choose deductibles too low to save minimal premium dollars, then face financial strain when they actually need to pay the deductible after a claim. Your deductible choice should reflect what your business can realistically afford to pay out of pocket without disrupting operations.

Request Standardized Quotes from Multiple Insurers

Comparing quotes across multiple insurers reveals substantial rate variations that directly impact your annual costs. Texas commercial auto base rates vary significantly by territory, meaning your location creates a starting point that different insurers price differently. Request quotes from at least three providers and verify they’re quoting identical coverage limits, vehicle types, and driver information. A quote for 100/300/100 limits with a $1,000 deductible from one insurer means nothing if another quotes 50/100/50 limits with a $2,500 deductible. Standardizing the quote parameters lets you compare actual pricing differences rather than coverage variations.

Evaluate Coverage Inclusions and Insurer Stability

When comparing policies, examine what each insurer includes in their commercial auto package. Some carriers include roadside assistance and towing coverage automatically, while others charge extra. If your business depends on vehicle availability, towing coverage and on-hook liability for customer vehicles in your possession become essential rather than optional. An insurer offering the lowest premium means nothing if they deny claims or lack the financial strength to pay them. Verify insurer financial stability and complaint history before selecting a provider.

Final Thoughts

Selecting the best commercial auto insurance for your business requires understanding what coverage protects you, what factors affect your rates, and how to compare policies systematically. Liability coverage forms your legal foundation in Texas, while collision and comprehensive protection safeguard your vehicles from accidents and unexpected damage. Uninsured and underinsured motorist coverage fills gaps when other drivers lack adequate insurance, and your rates depend heavily on vehicle type, driver records, coverage limits, and location.

The process of choosing the right policy demands more than picking the lowest quote. You need coverage tailored to your fleet’s composition, your drivers’ experience, and your business’s travel patterns. A food truck operation requires different protection than a consulting business with a single sedan, and your deductible choice should reflect what your business can realistically afford to pay after a loss without disrupting operations.

Contact us at brooksinstx.com to discuss your commercial auto insurance needs with an agent who understands Texas business operations and the specific risks your industry faces. We represent multiple top-rated insurance companies, giving you access to a larger selection of coverage options and pricing than you’d find working with a single carrier. Our licensed agents work with you to identify coverage gaps, compare quotes across insurers, and select policies that match your actual needs rather than generic templates.

Disclaimer: The information provided in this blog is for general informational purposes only and does not constitute legal, financial, or insurance advice. Coverage options, terms, and availability may vary. Please consult with a licensed professional for advice specific to your situation