Choosing between a captive and independent insurance agency shapes your coverage options and costs. At Brooks Insurance, we’ve seen Texas consumers struggle with this decision because the differences matter significantly.

Captive agencies represent one company, while independent agencies work with multiple carriers. Understanding these models helps you find the right fit for your insurance needs.

What Captive Agencies Actually Are

How Captive Agencies Operate

A captive insurance agent works exclusively for one insurance company and sells only that insurer’s policies. State Farm, Allstate, GEICO, and Farmers operate this model across Texas. When you meet with a captive agent, they possess deep knowledge of their single company’s products, training programs, and underwriting guidelines because that’s all they handle. The captive model provides agents with structured support, marketing materials, office setup assistance, and brand recognition that comes from representing a well-known insurer.

The Single-Carrier Limitation

This exclusive arrangement creates a fundamental constraint: captive agents cannot offer you policies from other carriers, regardless of whether another company might provide better coverage or pricing for your situation. If you need home insurance and the captive carrier doesn’t offer competitive rates for your property type, the agent cannot shop elsewhere on your behalf. If your business requires commercial coverage that falls outside the captive company’s appetite, the agent cannot help. Captive agents solve problems within one company’s product box rather than across the market.

How Compensation Shapes Their Options

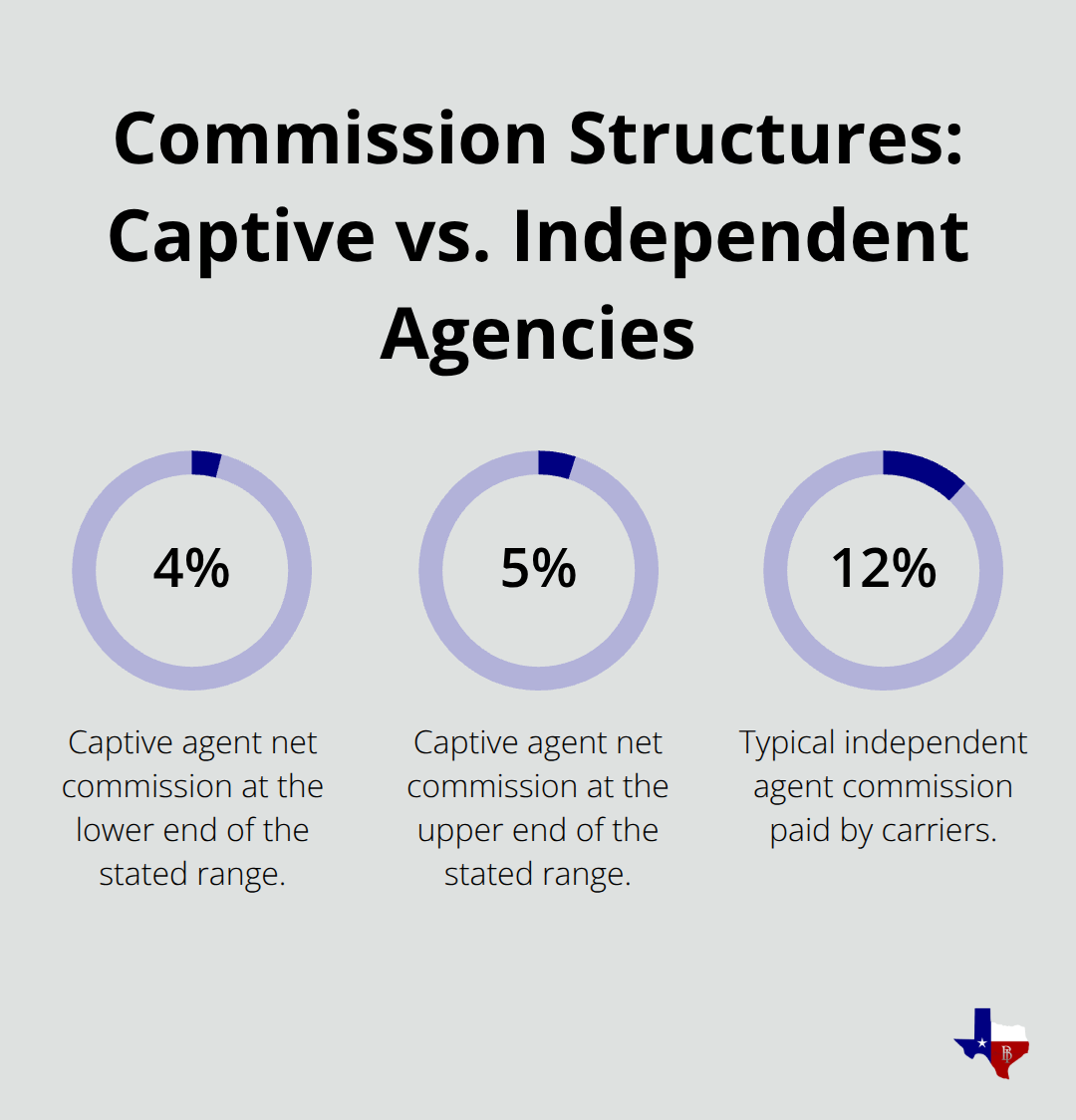

Their compensation structure reinforces this limitation. Captive agents typically earn 4 to 5 percent net commission after the carrier takes its split, and their income depends directly on meeting sales quotas tied to their employer’s goals. This financial arrangement means they have no incentive to recommend competitors’ products, even when those products might better serve your needs.

The captive model ties agent success to company success, not client success.

What This Means for Texas Consumers

For consumers in Texas seeking personalized solutions that consider multiple carrier options and competitive pricing across the market, the captive model’s single-company approach creates real restrictions on what coverage possibilities exist. You receive solutions limited to one carrier’s appetite and pricing. When you work with an independent agency instead, you gain access to multiple carriers and the flexibility to compare options that captive agents simply cannot provide.

How Independent Agencies Work

Multiple Carriers Mean More Options

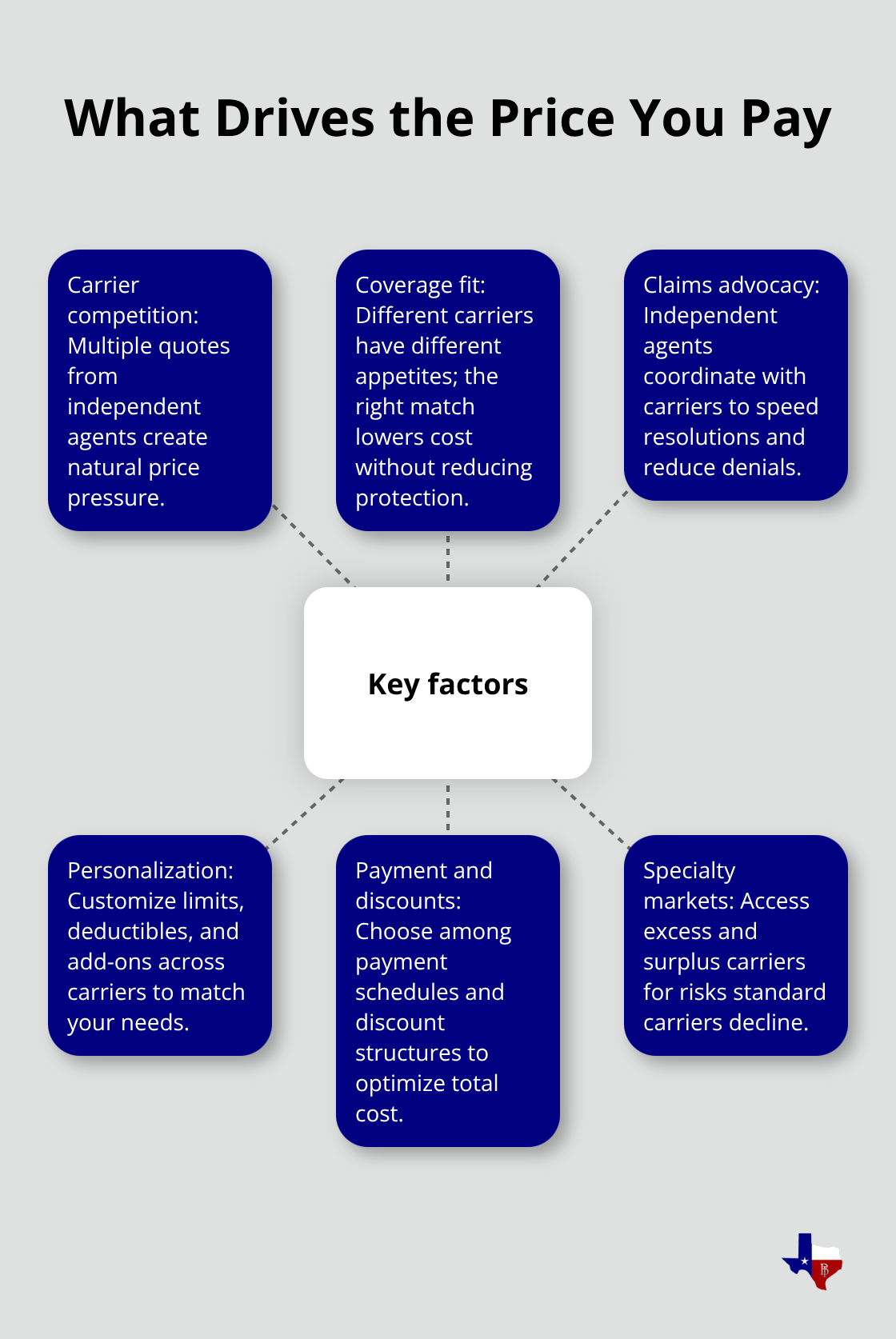

An independent insurance agency represents multiple carriers rather than just one, which fundamentally changes how agents serve clients. We at Brooks Insurance operate this model, partnering with multiple top-rated insurance companies to give you a larger selection of coverage, pricing, and payment options. Unlike captive agents who can only present one company’s solutions, independent agents access dozens or even hundreds of carriers depending on the agency’s network. This access matters because insurance carriers have different appetites for different risk types. One carrier might excel at insuring historic homes while another specializes in new construction. One might offer competitive rates for young drivers while another focuses on mature customers. Independent agents know these differences and can match your specific situation to the carrier most likely to provide the best coverage at the best price.

No More “We Can’t Help You”

When you work with an independent agency, you avoid the limitations that captive agents face. If your home doesn’t fit a carrier’s guidelines or your business falls outside their appetite, the independent agent simply moves to another carrier instead of telling you no. This flexibility solves problems that captive agents cannot address.

You receive solutions tailored to your actual risk profile rather than solutions limited to what one company will underwrite.

Financial Incentives Align With Your Interests

The financial structure of independent agencies creates alignment with your interests rather than working against them. Independent agents typically earn the full commission available from carriers rather than splitting it with an employer, which means they have every incentive to find you the right coverage at competitive rates. This compensation reality means independent agents benefit when they solve your problems efficiently and earn your loyalty through better service.

Relationship-Focused Service

We at Brooks Insurance built our business on relationships, not transaction volume. Our licensed agents and staff remain just a phone call or email away if you have questions about your coverage. When you need to file a claim or adjust your coverage, we guide you through the process rather than leaving you to navigate alone, which improves outcomes and reduces your stress during difficult situations. This hands-on approach distinguishes independent agencies from captive operations that often prioritize volume over individual client outcomes.

Why This Matters for Your Coverage Decisions

The independent model gives you access to carriers and products that captive agents simply cannot offer. This broader marketplace means you compare options across multiple underwriters, not just one company’s limited product box. The next section examines the specific advantages this creates when you evaluate cost, service quality, and claims support.

Key Differences Between Captive and Independent Insurance Agencies

Where Price Really Comes From

Captive agents and independent agents operate under fundamentally different financial structures that directly affect what you pay for insurance. Captive agents earn 4 to 5 percent net commission after their employer takes a cut, which means they have no financial incentive to negotiate better rates or find you alternatives. Independent agents earn the full commission available from carriers, typically 12 percent, which creates a direct incentive to solve your problem efficiently and earn your business through competitive pricing. This structural difference matters more than most consumers realize.

When a captive agent presents a quote, that quote reflects one company’s pricing on one set of underwriting criteria. When an independent agent presents quotes, you see multiple carriers competing for your business, which naturally drives prices down. Texas consumers shopping for homeowners insurance often discover this difference immediately. One carrier might quote $1,200 annually while another quotes $950 for identical coverage because carriers price risk differently based on their underwriting appetite and loss history in specific regions.

A captive agent cannot show you that $950 option. An independent agent presents both and explains the differences in deductibles, coverage limits, and service levels so you make an informed choice.

The pricing flexibility extends beyond initial quotes. When your life changes or claims history shifts, captive agents recalculate rates within one company’s guidelines. Independent agents can move your coverage to a different carrier if that carrier now offers better pricing for your updated risk profile. This flexibility proves especially valuable during hard market conditions when some carriers restrict coverage or raise rates significantly. Independent agents solve this problem by shifting clients to carriers with better appetite for their specific risk type, keeping premiums stable when captive agents have no alternative but to pass along their company’s rate increases.

How Service Quality Differs When You Need Help

Captive agents handle more administrative tasks than independent agents because they manage everything in-house, which diverts time from actually serving you. Independent agents focus on understanding your risks and finding solutions because they delegate administrative work to staff, keeping licensed agents available for client relationships. This distinction reveals itself when you call with questions or need coverage adjustments.

Claims support demonstrates this difference most clearly. When you file a claim with a captive carrier, you interact with that company’s claims department directly, and if complications arise, your agent has limited leverage to influence the outcome. Independent agents guide you through claims by maintaining relationships with carriers and advocating on your behalf when questions emerge. This hands-on approach reduces claim denials and accelerates payment because your agent communicates directly with adjusters and underwriters. Texas consumers filing homeowners claims after weather events consistently report that independent agents resolve complications faster than captive agents because the agent has incentive and ability to push for resolution, whereas captive agents simply relay information between you and the claims department.

Why Personalization Actually Matters for Your Specific Situation

Personalized service means an agent understands your actual risks rather than fitting you into a company’s standard product categories. Captive agents work within preset product packages designed for broad customer segments. Independent agents design policies around your specific circumstances by selecting coverage from multiple carriers and customizing deductibles, limits, and additional protections to match your needs and budget.

A business owner in Houston with a home-based consulting practice needs different coverage than a retail shop owner, yet captive agents often present similar policies because their company’s products don’t account for these differences. Independent agents build custom solutions by accessing excess and surplus carriers that underwrite specialized risks that standard carriers decline. This capability transforms what coverage options exist for your business.

The personalization extends to payment flexibility. Some carriers offer monthly payments while others require quarterly or annual payments. Some offer discounts for bundling home and auto while others discount based on claims-free history. Independent agents access these variations across dozens of carriers and select the combination that reduces your total cost while improving your coverage. Captive agents present one payment structure and one discount structure regardless of your preferences or financial situation.

Final Thoughts

Captive agencies offer stability through brand recognition and structured training, but they solve problems within a single company’s constraints. Independent agencies provide flexibility, broader coverage options, and financial incentives aligned with your interests rather than their employer’s quotas. When you evaluate the captive vs independent insurance agency choice, you should focus on what matters most to your specific situation.

Evaluate whether one carrier’s products meet your needs or whether you benefit from comparing multiple options across the market. Assess how important personalized service becomes during claims or coverage adjustments, and examine total cost including premiums, deductibles, and available discounts rather than accepting one company’s pricing. Determine whether you need specialized coverage that standard carriers decline, which only independent agents can access through excess and surplus markets.

For Texas consumers, independent agencies consistently deliver better value because they eliminate the single-company limitation that captive agents cannot overcome. You receive competitive pricing from multiple carriers, personalized solutions tailored to your actual risks, and claims support from agents who advocate on your behalf. Contact Brooks Insurance to discuss your personal or commercial coverage needs and discover how our independent agency model serves your situation better.

Disclaimer: The information provided in this blog is for general informational purposes only and does not constitute legal, financial, or insurance advice. Coverage options, terms, and availability may vary. Please consult with a licensed professional for advice specific to your situation