Running a business with vehicles comes with real risks. At Brooks Insurance, we help Texas business owners understand commercial auto insurance definition and coverage options so you can protect your company properly.

Whether you operate a single service vehicle or a fleet, the right policy makes a difference. This guide walks you through what commercial auto insurance covers and how to choose the right protection for your business.

What Commercial Auto Insurance Actually Covers

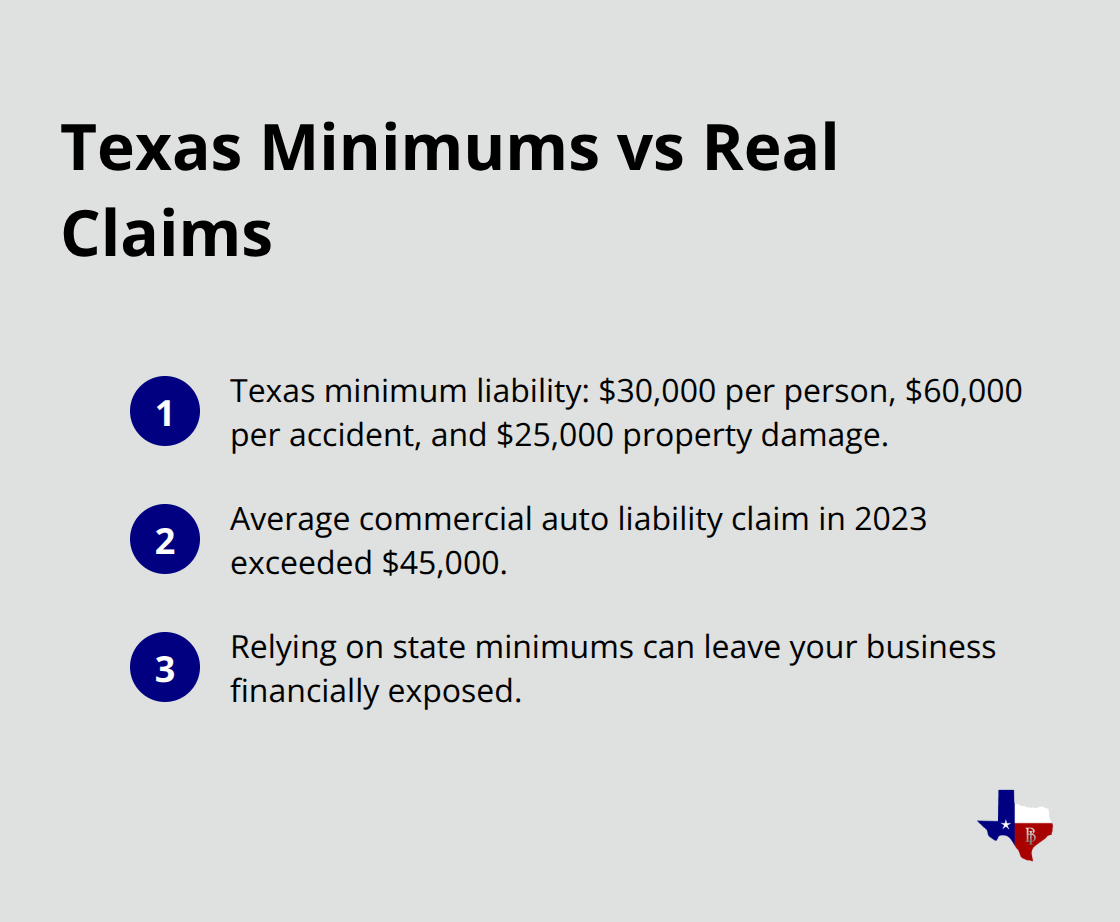

Commercial auto insurance protects your business vehicles and the people they carry from financial loss due to accidents, theft, and other incidents. Unlike personal auto policies that explicitly exclude business use, commercial coverage is built specifically for vehicles used to generate income or conduct business operations. Many Texas business owners discover too late that their personal policy won’t cover them if they use a vehicle for work. The core coverages include bodily injury liability, which pays medical expenses and lost wages for people injured in an accident you cause; property damage liability, which covers repairs to other vehicles or property you damage; collision coverage for damage to your own vehicle from crashes; and comprehensive coverage for theft, vandalism, weather, and other non-collision incidents. Texas requires minimum liability coverage limits of $30,000 per person and $60,000 per accident for bodily injury, plus $25,000 for property damage. However, these minimums often fall short for businesses. According to data from the National Association of Insurance Commissioners, the average commercial auto liability claim in 2023 exceeded $45,000, which means relying on state minimums could leave your business financially exposed.

Why Your Personal Policy Won’t Work

Personal auto insurance policies contain exclusions that eliminate coverage the moment a vehicle is used for business purposes. If you deliver products, provide a service, or transport clients and you have an accident, your personal insurer can deny the entire claim and refuse to defend you. This happens regularly in Texas, and it devastates small business owners who didn’t realize the gap in their coverage. A food truck operator, electrician, landscaper, or cleaning service owner all need commercial coverage because their vehicles generate income. Even if an employee uses their personal vehicle for work, your business faces liability exposure. Commercial policies extend coverage to multiple drivers, hired vehicles, and borrowed vehicles, whereas personal policies typically cover only household members. The coverage limits are also substantially higher. Most commercial policies start at $500,000 to $1,000,000 in combined single limits, compared to the $100,000 to $300,000 typical on personal policies. If you operate a box truck, van, or any vehicle that carries equipment, tools, or inventory, you absolutely need commercial coverage.

Who Needs This Coverage Right Now

If your business owns vehicles or if employees drive for work, you need commercial auto insurance. The Texas Small Business Administration reports that Texas has over 3 million small businesses employing nearly 45% of the state’s workforce, and many operate vehicles without proper coverage. You need this coverage if you deliver goods, provide services at client locations, transport employees, offer rideshare or livery services, or operate specialty vehicles like tow trucks or food trucks. Even sole proprietors with a single service vehicle must have commercial coverage in Texas. If your business vehicle is financed, your lender will require proof of commercial insurance. The cost varies significantly based on your industry, vehicle type, driving records, and location. A contractor’s truck with a higher risk profile costs more than a consultant’s sedan used for occasional client meetings. Getting quotes from multiple carriers helps you understand your actual rates rather than guessing at costs.

Coverage Limits That Match Your Risk

Texas minimums provide a starting point, but they rarely match what your business actually needs. A single serious accident can generate medical bills, lost wages, and property damage claims that far exceed the baseline. Many business owners try higher limits like $500,000 or $1,000,000 per accident to protect their assets and operations. Your industry and vehicle type determine what makes sense for your situation. A delivery service with multiple drivers and daily routes faces different exposure than a consultant who occasionally meets clients. The right limits protect your business from catastrophic financial loss while keeping premiums manageable. As an independent agency, we at Brooks Insurance represent multiple top-rated insurance companies, which means you have a larger selection of coverage options and pricing to choose from. Understanding your specific risk helps you select limits that actually protect your business rather than just meeting legal minimums.

Next Steps to Protect Your Business

The gap between personal and commercial coverage is significant, and closing that gap starts with understanding what your business actually needs. Your vehicle type, industry, number of drivers, and annual mileage all factor into the right policy for your operation. Getting a quote from multiple carriers shows you the real cost of proper protection and helps you compare coverage options side by side.

Coverage Options and What They Protect

Liability Coverage Forms Your Foundation

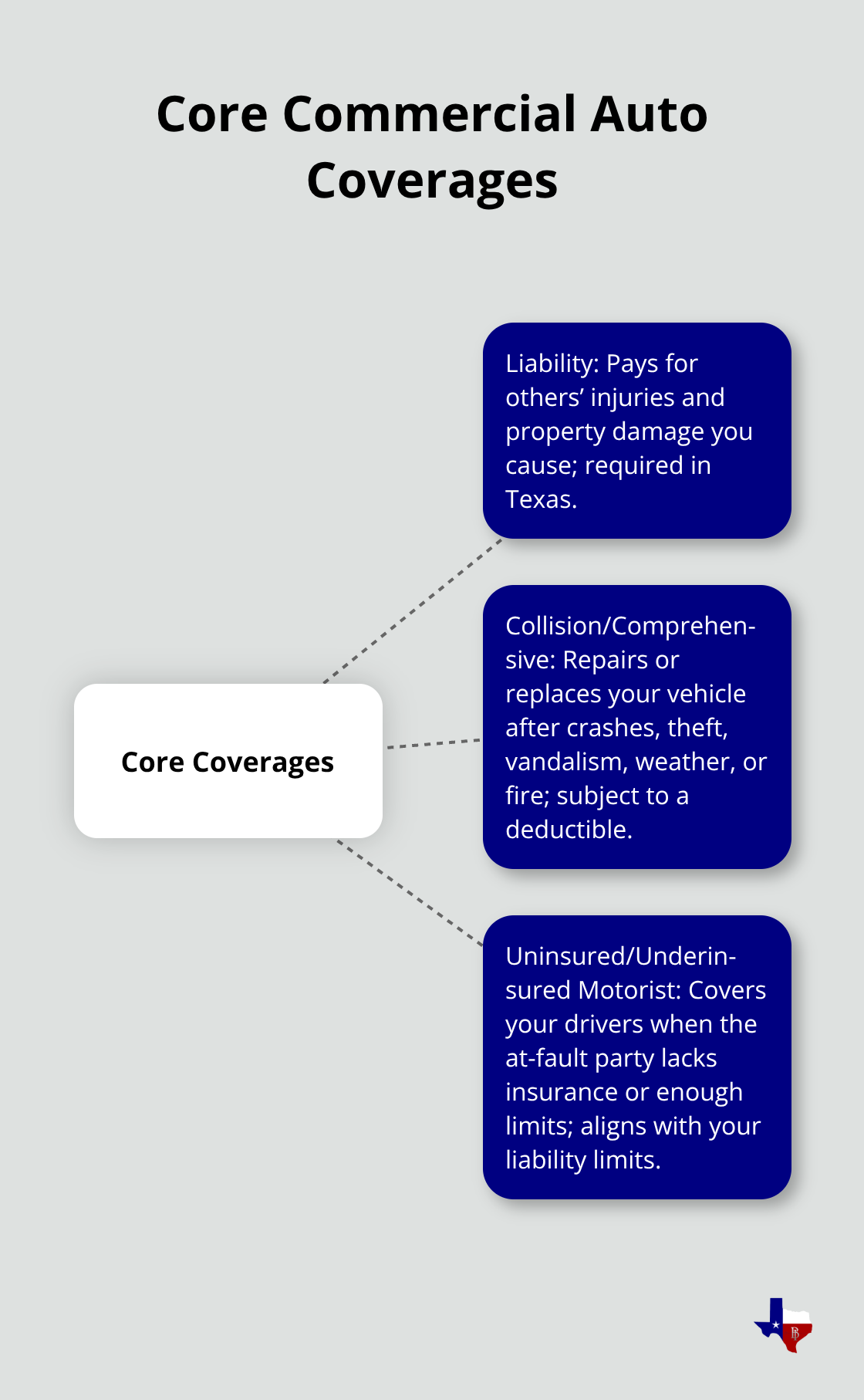

Liability coverage forms the foundation of commercial auto insurance, and Texas law requires you to carry it. Bodily injury liability pays medical bills, rehabilitation costs, lost wages, and pain and suffering for people injured in accidents you cause. Property damage liability covers repairs to other vehicles, buildings, fences, or equipment your vehicle damages. These two coverages work together to protect your business from lawsuits and financial ruin.

Most Texas business owners struggle to choose limits that actually match their exposure. A single serious accident can generate claims well above state minimums. According to the National Association of Insurance Commissioners, commercial auto liability claims can significantly exceed the Texas minimum of $30,000 per person, which means serious accidents leave you personally liable for the difference.

Match Your Limits to Your Industry

A contractor operating a service vehicle, a food truck owner making deliveries, or a cleaning service with multiple employees all face different liability exposure based on their routes, client locations, and daily operations. Higher limits like $500,000 or $1,000,000 per accident cost more in premiums but protect your business assets and future earnings from catastrophic claims. The industry you operate in and your annual mileage should drive your limit selection, not just what the law requires.

Collision and Comprehensive Protect Your Vehicles

Collision and comprehensive coverage protect your own vehicles from damage, and they operate differently based on what causes the loss. Collision coverage pays to repair or replace your vehicle after a crash, rollover, or impact with another object, and it applies regardless of who caused the accident. Comprehensive coverage handles theft, vandalism, weather damage, fire, and other non-collision incidents. Both coverages include a deductible you choose, typically $500, $1,000, or higher, which reduces your premium in exchange for paying more out of pocket when a loss occurs.

A food truck operator or contractor with expensive equipment inside the vehicle might choose a lower deductible to minimize out-of-pocket costs after damage. A consultant using a vehicle for occasional client meetings might select a higher deductible to reduce premiums.

Uninsured and Underinsured Motorist Coverage Protects Your Drivers

Uninsured and underinsured motorist coverage protects your drivers when the at-fault party lacks adequate insurance or carries no insurance at all. This coverage pays medical expenses, lost wages, and other damages your drivers suffer in an accident caused by someone else. Texas law allows you to reject this coverage in writing, but doing so exposes your drivers to financial hardship if hit by an uninsured driver.

The data from the Texas Department of Transportation shows uninsured drivers remain a significant problem on Texas roads, making this coverage essential for protecting your employees and business operations. Carrying uninsured and underinsured motorist limits that match your liability limits ensures consistent protection across all scenarios. The right combination of these three coverage types-liability, collision/comprehensive, and uninsured/underinsured motorist-creates a solid foundation, but your specific business needs may call for additional protections that we explore in the next section.

How to Select the Right Commercial Auto Insurance Policy

Document Your Business Operations First

Selecting commercial auto insurance means matching your actual business operations to coverage that protects your assets, not just checking boxes on a form. Start by documenting what you operate: vehicle make, model, and year; annual mileage; primary business use; number of drivers; and whether vehicles carry equipment or inventory. A food truck operator needs different protection than a consultant, and a contractor with $50,000 in tools inside the vehicle faces different risk than one with an empty service van. The National Association of Insurance Commissioners reports that commercial auto liability claims exceed $45,000 on average, so your coverage limits must reflect realistic exposure rather than legal minimums.

Assess Your Liability Exposure Realistically

Texas requires $30,000 per person and $60,000 per accident for bodily injury liability, but a single serious accident involving multiple injuries or property damage can easily exceed these thresholds. If you operate in high-traffic areas like Houston or Dallas, or if your routes involve highways and longer distances, your exposure increases significantly. Document your typical routes, client locations, and whether you transport employees or customers. Higher-risk operations like tow trucks or livery services should carry $500,000 to $1,000,000 in combined single limits. Lower-risk operations like occasional client visits might operate safely at $300,000 to $500,000.

Choose Deductibles That Match Your Financial Capacity

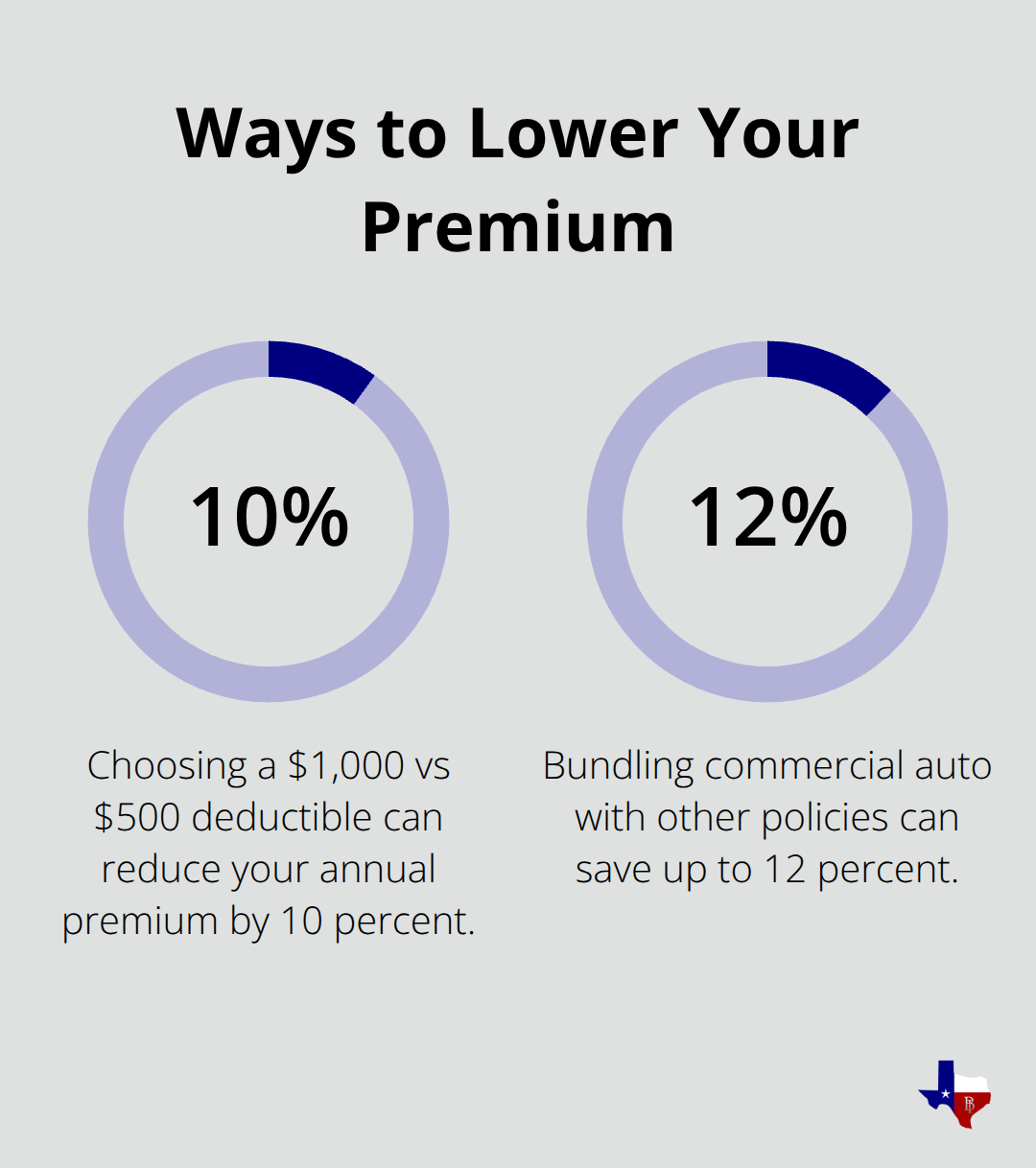

Your deductible selection matters more than many business owners realize: selecting $1,000 instead of $500 can reduce your annual premium by 10 to 15 percent, but only if you can absorb that cost when damage occurs. Contractors with expensive equipment should lean toward lower deductibles because a single claim could cost thousands in repairs. This decision directly impacts both your monthly costs and your out-of-pocket exposure after a loss.

Compare Multiple Carriers and Coverage Options

An independent insurance agency represents multiple carriers, which means you get genuine rate comparisons instead of a single company’s pricing. When you contact an agent, provide your vehicle information, driver information including driving records, and your typical annual mileage so quotes reflect your actual risk profile. Agents who specialize in commercial coverage understand how industry type, vehicle use, and driver experience affect your rates in ways that online quote tools miss. A contractor’s premium differs from a delivery service’s premium because the risk profiles differ.

Ask carriers specifically whether they offer discounts for safety equipment, GPS tracking, or driver training programs, as these can reduce costs significantly. Some insurers provide bundling discounts when you combine commercial auto with general liability or property insurance, potentially saving 10 to 12 percent on your total coverage.

Request quotes from at least three carriers before deciding, and compare not just price but also claims handling reputation, customer service availability, and coverage options. The cheapest policy often provides the least protection when claims occur.

Review Your Policy Annually for Changes

Your policy needs adjustment as your business evolves. Review your coverage annually because your business changes, your vehicle fleet may grow or shrink, and your driving patterns may shift. What protected your business last year might leave you exposed this year.

Final Thoughts

Commercial auto insurance definition matters because it shapes how you protect your business from real financial exposure. Understanding what coverage actually does-and what it doesn’t-prevents costly gaps that personal policies leave exposed. The right policy matches your vehicle type, industry, driving patterns, and financial risk so you operate with confidence rather than worry.

Texas minimums provide a legal baseline, but they rarely match the real cost of serious accidents. A single claim exceeding $45,000 can devastate a business relying on state minimum limits, which is why higher coverage limits, appropriate deductibles, and the right combination of liability, collision, comprehensive, and uninsured motorist protection create a foundation that actually protects your assets and operations. Your contractor’s truck with expensive equipment faces different risk than a consultant’s sedan, and your food truck operation needs different protection than a delivery service with multiple drivers.

At Brooks Insurance, we represent multiple top-rated insurance companies, which means you get genuine rate comparisons and coverage options tailored to your actual business needs. Our licensed agents understand how commercial operations differ from personal use and match protection to your specific risk profile. Contact us today to discuss your business vehicles and get protection that matches your operation.

Disclaimer: The information provided in this blog is for general informational purposes only and does not constitute legal, financial, or insurance advice. Coverage options, terms, and availability may vary. Please consult with a licensed professional for advice specific to your situation