Running a business in Texas means protecting your vehicles and drivers on the road. Commercial auto insurance meaning goes beyond basic coverage-it’s a legal requirement and financial safeguard for any company operating vehicles.

At Brooks Insurance, we help Texas business owners understand exactly what commercial auto insurance covers and why it matters for your operation.

What Commercial Auto Insurance Actually Covers

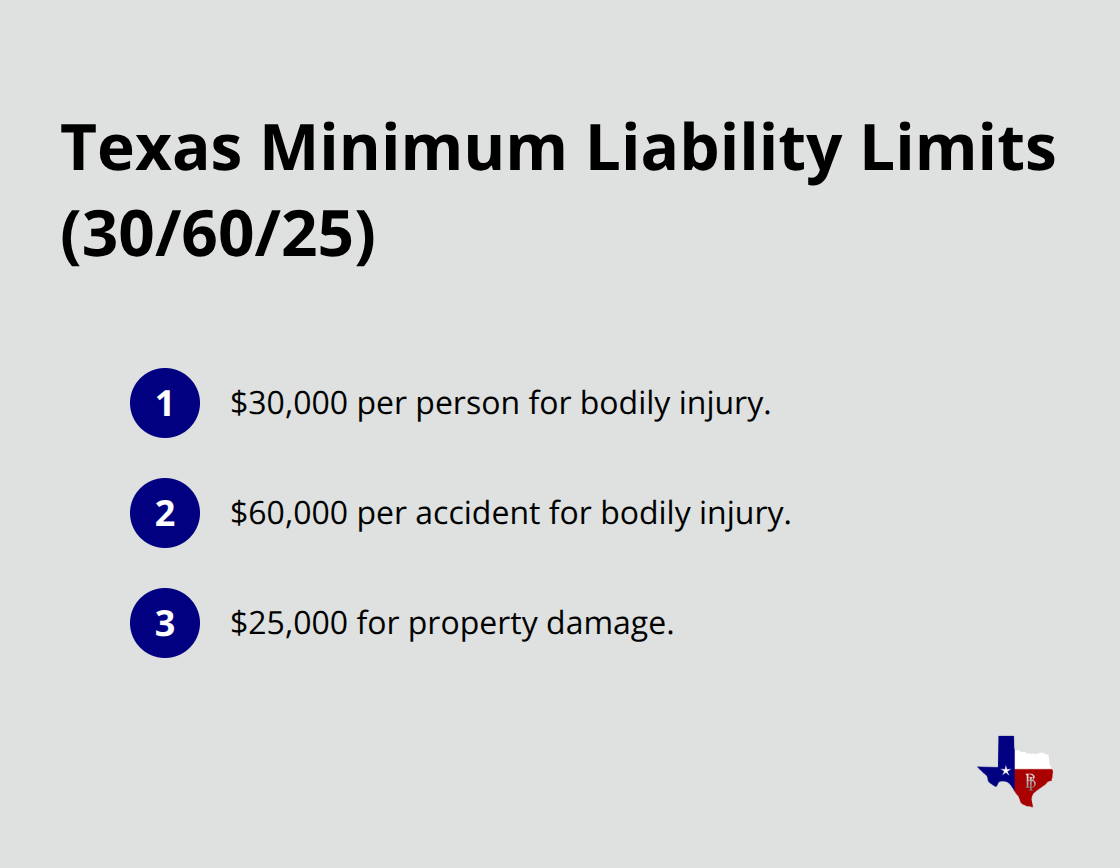

Commercial auto insurance protects your business vehicles and the people driving them when accidents happen on the job. Unlike personal auto policies that cover your commute or weekend errands, commercial auto insurance applies specifically to vehicles used for business operations, whether that means delivery trucks, service vans, or company cars your employees drive for work. The policy pays for vehicle repairs after collisions, medical expenses for injured drivers and passengers, and legal liability if your vehicle damages someone else’s property or causes injury. Texas has over 2.7 million small businesses, and most of them rely on commercial auto insurance to keep operations running without financial disaster when accidents occur. This coverage is legally required in Texas if you own company vehicles, and the state mandates minimum liability limits of 30/60/25 ($30,000 per person for bodily injury, $60,000 per accident for bodily injury, and $25,000 for property damage). Many businesses actually need higher limits than these minimums depending on their operations, equipment value, and risk exposure.

The Key Difference from Personal Policies

Your personal auto insurance explicitly excludes business use, which means you lack coverage if you deliver packages, pick up clients, or make service calls. Insurance companies treat business vehicles as higher risk because they typically travel more miles, operate in varied locations, and involve different drivers than a personal vehicle. Commercial policies also offer higher coverage limits and broader protections because businesses face greater liability exposure than individual drivers. If an employee causes an accident while making a delivery in a company vehicle, your personal policy will not pay anything, leaving your business responsible for all costs. Texas law and your policy language make this distinction clear, so operating a business vehicle without commercial coverage creates serious financial and legal exposure.

Who Actually Needs This Coverage

You need commercial auto insurance if your business owns vehicles or if employees regularly use personal vehicles for work activities. Food truck operators, plumbers, electricians, landscapers, and delivery services obviously need coverage, but so do many other businesses. Real estate agents who transport clients, contractors who travel to job sites, and consultants who visit client offices all need commercial auto insurance. Even if you operate a small business with just one vehicle, if that vehicle serves any business purpose beyond commuting to a single fixed location, commercial coverage is both legally required and financially essential. The U.S. Small Business Administration reports that small businesses employ about 45% of Texas’s workforce, and most of those operations involve vehicle use that requires proper commercial auto insurance protection.

What Happens When You Skip Coverage

Operating without commercial auto insurance exposes your business to catastrophic financial risk. If your uninsured vehicle causes an accident that injures someone or damages property, your business becomes personally liable for all medical bills, repair costs, and legal fees. Texas courts have awarded settlements that far exceed what most small businesses can absorb, and creditors can pursue your personal assets to satisfy judgments. Your business license and operating authority may also face suspension or revocation if you fail to maintain required coverage. Understanding these consequences makes the next step clear: you need to evaluate which specific coverages protect your operation best.

Coverage Types and What They Protect

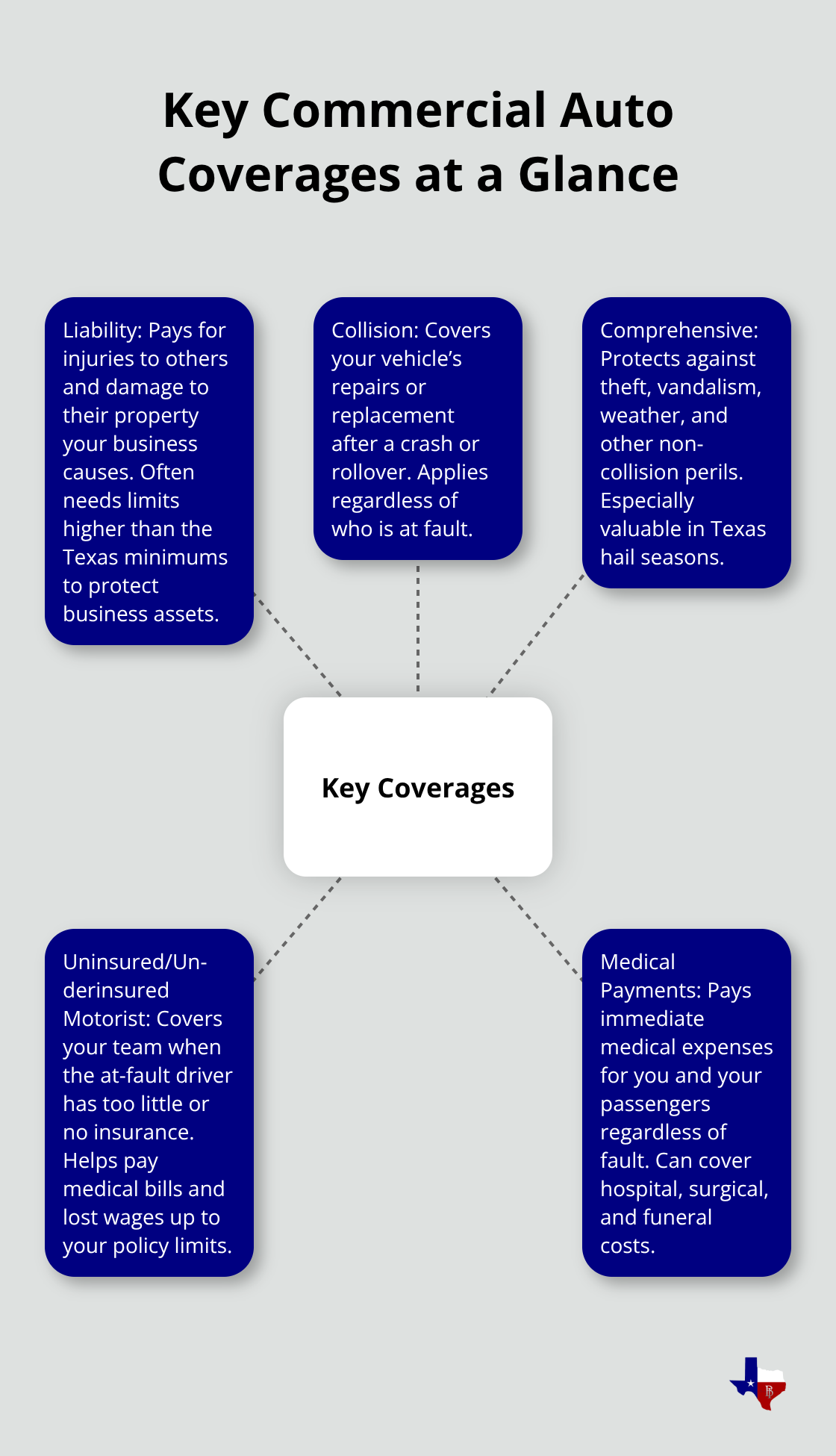

Liability Coverage: The Foundation of Your Protection

Liability coverage forms the backbone of commercial auto insurance in Texas because it covers the damage your business causes to other people and their property. If your delivery driver hits another vehicle and injures the occupants, liability coverage pays their medical bills, lost wages, and legal fees if they sue your company. Property damage liability covers repairs to their vehicle, structures, or equipment your vehicle damages.

Texas mandates minimum liability limits of 30/60/25, but most businesses need higher limits because one serious accident can easily exceed these minimums. Your business assets become vulnerable if you carry only minimum limits, so evaluate your actual risk exposure before settling on coverage amounts.

Collision and Comprehensive: Protecting Your Own Vehicles

Collision and comprehensive coverage protect your own vehicles rather than the other party’s property. Collision pays for repairs or replacement when your vehicle hits another object or rolls over, while comprehensive covers theft, vandalism, weather damage, and other perils unrelated to collisions.

If your vehicle is financed or leased, your lender or lessor will require both coverages as a condition of the loan or lease agreement. Many Texas business owners overlook the fact that comprehensive coverage also protects against hail damage, which causes significant claims in Texas during spring and early summer months. This protection directly affects your ability to keep operations running after weather events strike.

Uninsured and Underinsured Motorist Coverage: Your Safety Net

Uninsured and underinsured motorist coverage protects your drivers when the at-fault driver carries insufficient insurance or no insurance at all. Texas law, specifically the Stracener v. United Services Automobile Association ruling, requires that underinsured motorist coverage pay the amount your insured is legally entitled to recover after applicable deductions.

If an uninsured driver causes an accident that injures your employee, this coverage pays medical expenses and lost wages up to your policy limits without waiting for the other driver’s insurance to act. Since the Texas Department of Transportation reports significant numbers of uninsured drivers on Texas roads, this coverage protects responsible business operators from financial harm caused by other drivers’ failures to maintain adequate coverage.

Medical Payments Coverage: Immediate Protection for Your Team

Medical payments coverage works alongside uninsured motorist protection by covering immediate medical expenses for you and your passengers regardless of fault, with limits typically ranging from $1,000 to $10,000 per person. This coverage pays hospital bills, surgical costs, and funeral expenses directly without requiring proof of liability, which means your injured employees receive treatment quickly while liability questions are resolved separately.

The combination of these four coverage types creates a comprehensive safety net for your business operations. Understanding how each type protects different aspects of your business helps you make informed decisions about which coverage levels match your actual risk exposure. The next step involves examining the specific factors that determine what you’ll pay for this protection.

Factors That Affect Your Commercial Auto Insurance Costs

Vehicle Type and Equipment Value

Your commercial auto insurance premium depends on factors that directly reflect your business’s risk profile, and understanding these drivers helps you control costs without sacrificing protection. Vehicle type shapes your premium significantly because a food truck with expensive refrigeration equipment costs more to insure than a basic service van, and insurers factor in replacement costs when calculating rates. A dump truck carrying heavy loads faces higher premiums than a delivery car because payload weight increases accident severity and repair expenses. The Texas Department of Insurance recognizes that equipment-heavy vehicles like those used in construction or mobile food service generate more substantial claims, which translates directly to higher premiums.

Usage Patterns and Driver Records

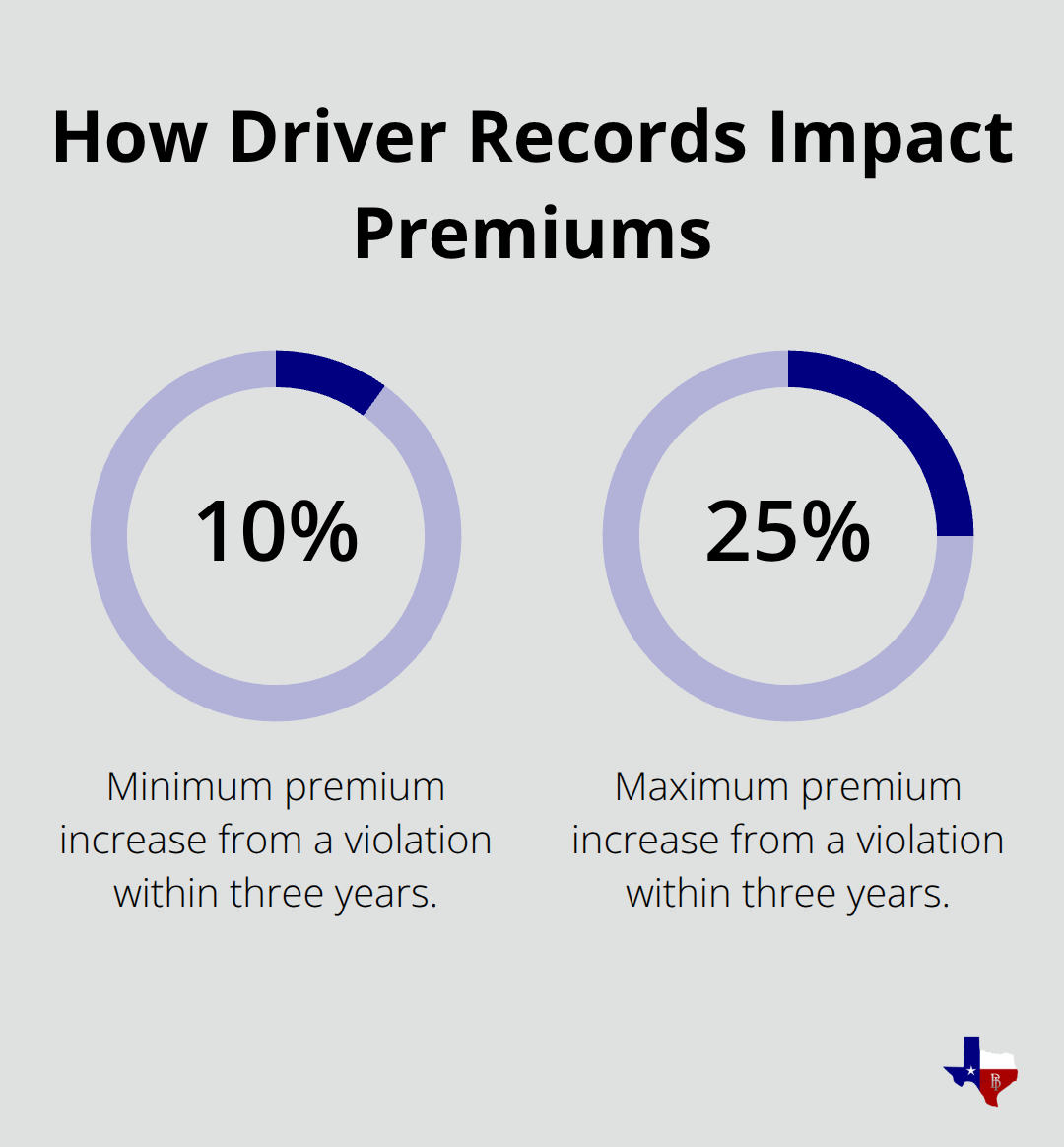

Your usage patterns matter just as much as the vehicle itself because a service vehicle that travels 50 miles daily within Austin faces lower premiums than one covering 200 miles across multiple Texas regions. Insurers pull motor vehicle reports on every driver with access to your commercial vehicles, and a single accident or violation from three years ago can increase your premium by 10 to 25 percent depending on severity. Hiring drivers with clean records isn’t just good safety practice-it’s a direct cost control measure that affects your bottom line.

Territory and Annual Mileage

Drivers operating primarily in rural areas typically pay less than those in Dallas or Houston because metropolitan areas generate more claims and costlier settlements due to higher traffic density and expensive repair shops. Regional routes that require longer distances command higher premiums than local city deliveries because extended travel increases exposure to accidents. Your annual mileage and territory create the third major premium factor because distance traveled and location both predict accident frequency and claim costs.

Loss Prevention and Vehicle Safety Features

Installing GPS tracking systems on your vehicles demonstrates commitment to safety and loss prevention, which many insurers reward with discounts. Securing your vehicles with anti-theft devices reduces theft risk and typically qualifies for additional savings. Choosing vehicles with strong safety ratings and modern anti-theft technology directly influences what you pay because insurers recognize that certain vehicles experience fewer claims and lower loss severity. When you shop for quotes, review your actual mileage patterns and service territories carefully because misrepresenting these details can void your coverage when you need it most.

Final Thoughts

Commercial auto insurance meaning extends far beyond a simple policy document-it represents the financial protection that keeps your Texas business operating safely when accidents happen on the road. The coverage types we’ve outlined, from liability to comprehensive protection, work together to shield your vehicles, drivers, and business assets from the unpredictable costs of vehicle-related incidents. Your specific costs depend on factors unique to your operation, including the vehicles you drive, where you drive them, and the experience of your drivers.

We at Brooks Insurance have spent over 50 years helping Texas business owners find the right commercial auto coverage for their operations. As an independent agency, we represent multiple top-rated insurance companies, which means you access a larger selection of coverage options, pricing, and payment plans tailored to your specific needs. Our licensed agents understand Texas commercial auto requirements and can guide you through the process of selecting appropriate limits and endorsements for your business type and vehicle usage patterns.

Contact Brooks Insurance today to discuss your commercial auto insurance needs with an agent who understands your Texas business. We answer your questions about coverage, help you compare quotes from multiple carriers, and get your business protected with the right policy at the right price.

Disclaimer: The information provided in this blog is for general informational purposes only and does not constitute legal, financial, or insurance advice. Coverage options, terms, and availability may vary. Please consult with a licensed professional for advice specific to your situation