Running a business with vehicles comes with real responsibilities. If you’re asking do I need commercial auto insurance, the answer depends on your specific situation-but for most business owners in Texas, it’s not optional.

We at Brooks Insurance help business owners understand their coverage requirements and find policies that actually protect their operations. This guide walks you through when coverage is legally required, what types of protection matter most, and how to choose the right policy for your fleet.

When Commercial Auto Insurance Is Required in Texas

Texas law mandates commercial auto insurance for business vehicles. If your vehicle operates for business purposes, Texas Transportation Code sections 601.071 and 601.072 require minimum liability coverage of $30,000 bodily injury coverage per person, $60,000 per accident, and $25,000 for property damage. These are legal minimums, not optional guidelines. Many business owners mistakenly assume their personal auto policy covers work use, but that assumption creates serious problems. Personal policies explicitly exclude business activities, which means you operate illegally and without insurance if you use a personal vehicle for deliveries, client visits, or equipment transport.

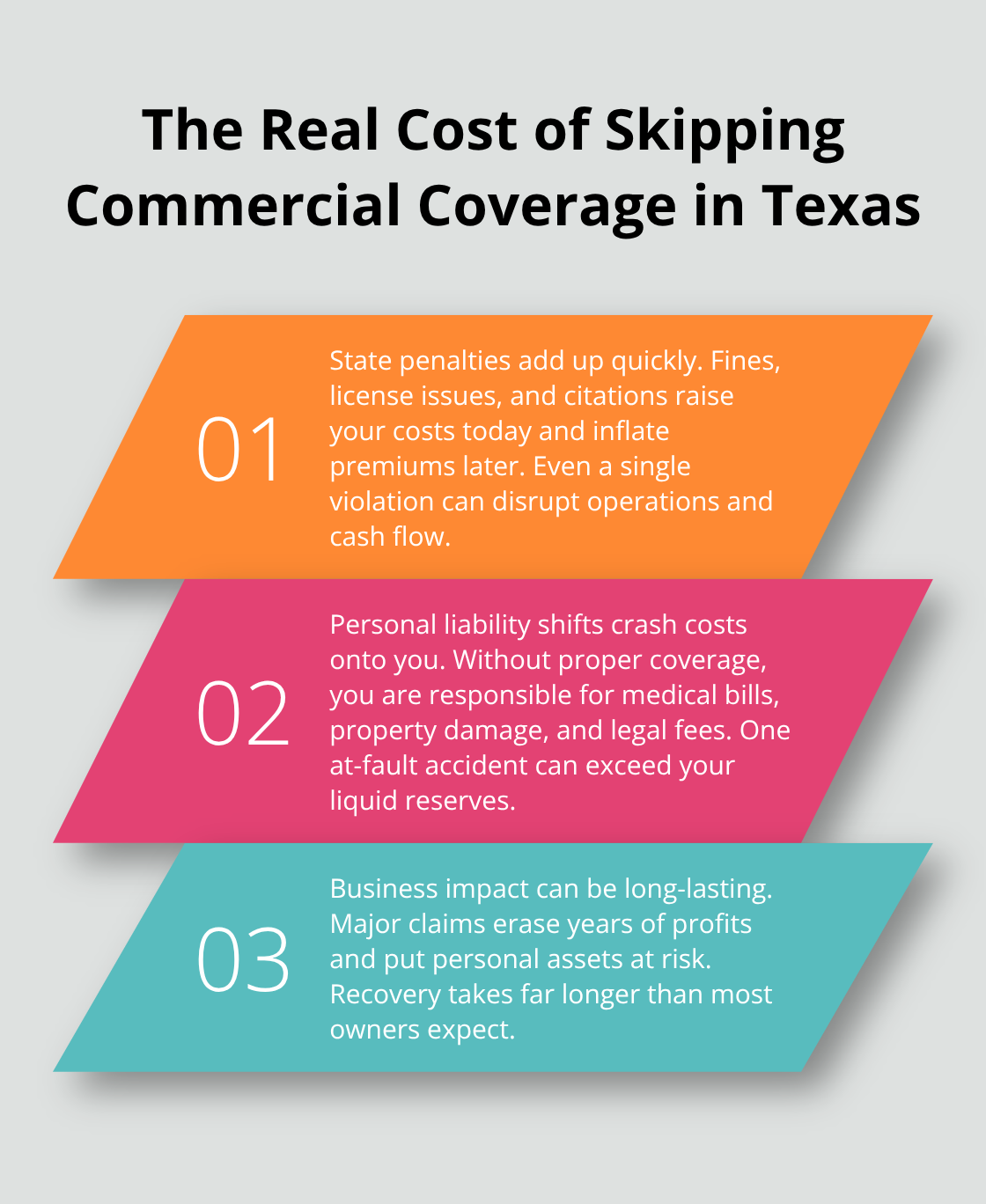

The Real Cost of Operating Without Coverage

Texas imposes steep penalties for operating without proper coverage. The state can levy fines up to 600 dollars, suspend your business license, and issue citations that damage your driving record and inflate future insurance costs. Beyond state penalties, you face personal liability for accident damages.

If you cause a collision while using a personal vehicle for business and that vehicle lacks commercial coverage, you personally owe medical bills, property damage, and legal fees-potentially tens of thousands of dollars. A single serious accident can wipe out years of business profits and threaten your personal assets.

Federal Requirements for Specific Industries

Some industries face additional federal requirements beyond Texas state law. If you transport hazardous materials, operate a commercial truck over 10,001 pounds, or provide services across state lines, the Department of Transportation may require higher liability limits or specialized coverage. Towing companies typically need commercial auto insurance with higher limits because they transport other people’s vehicles. Rideshare and delivery services operate in gray areas where coverage requirements depend on whether you use personal or commercial vehicles. Contact your state licensing board or industry association to verify exact requirements for your business type. Operating without proper coverage in these industries results in federal fines, loss of operating authority, and permanent damage to your business reputation.

Why Minimum Coverage Falls Short

Many business owners purchase the minimum required coverage and stop there. That approach leaves you dangerously exposed. Texas minimum liability of 30/60/25 covers almost nothing in a serious accident. A single hospitalization exceeds 50,000 dollars. A commercial vehicle accident involving multiple vehicles or injuries generates 200,000 to 500,000 dollars in damages. If your policy maxes out at 60,000 dollars and damages reach 150,000 dollars, you owe the 90,000 dollar difference personally. Higher liability limits (such as 100/300/100) protect your personal assets and business earnings from catastrophic claims, though they cost more upfront.

Collision and Comprehensive Coverage Matter

Skipping collision and comprehensive coverage creates another major gap. If your work vehicle is stolen or totaled in an accident, you replace it out of pocket-potentially 20,000 to 50,000 dollars depending on your fleet. Business vehicles face higher accident rates and theft risk than personal vehicles, making these coverages essential rather than optional extras. The next step involves understanding what specific coverage types actually protect your operation and which ones fit your business model best.

Types of Commercial Auto Coverage You Should Consider

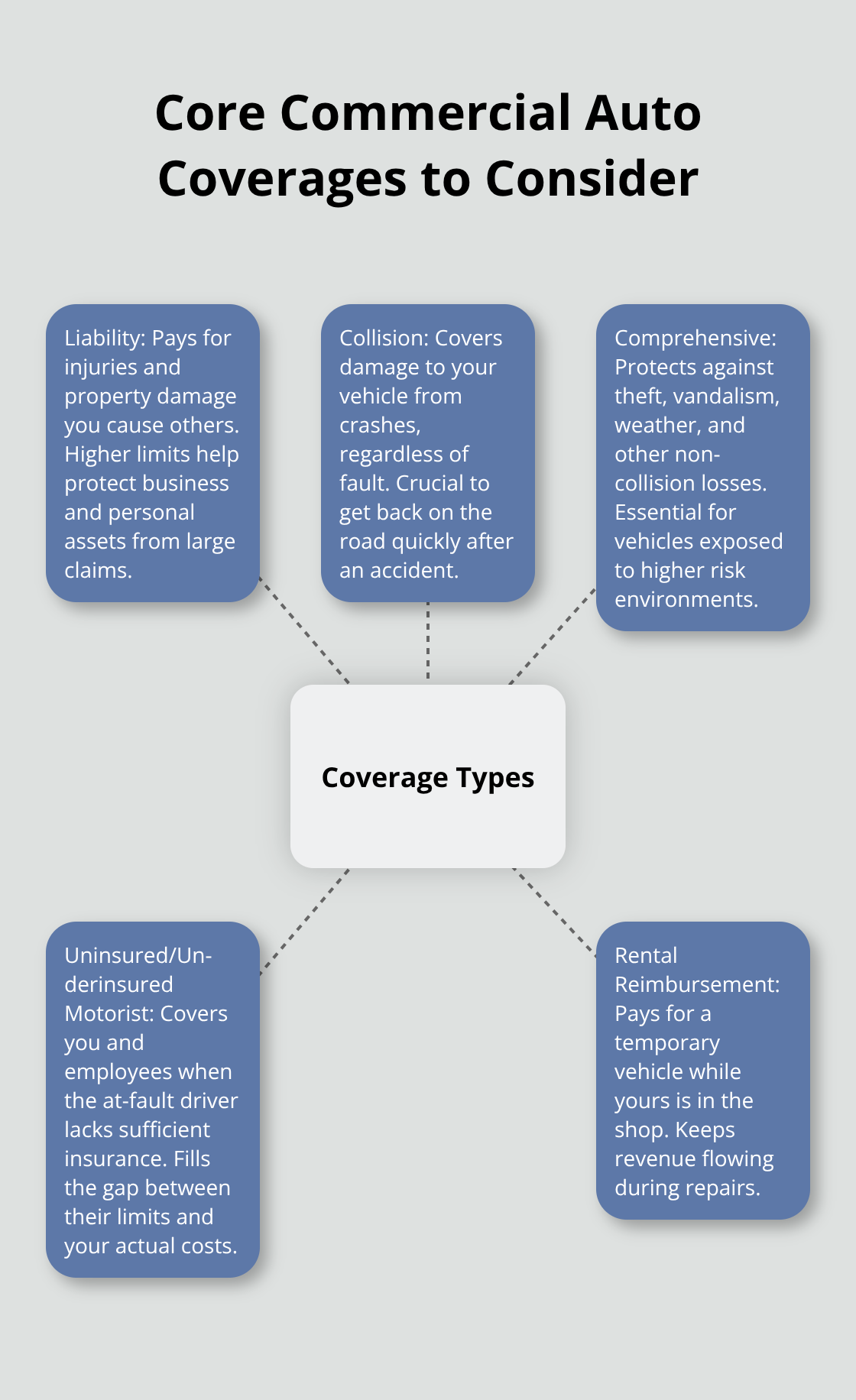

Liability Coverage Forms Your Foundation

Liability coverage forms the foundation of commercial auto insurance, and it’s where most business owners make costly mistakes. Texas law requires minimum liability coverage, but that bare minimum leaves you exposed to massive out-of-pocket losses. A single accident involving serious injuries generates claims exceeding $200,000 to $500,000, meaning inadequate policy limits cover only a fraction of actual damages.

You personally owe the difference. Most Texas businesses benefit from liability limits of at least 100/300/100, particularly those operating multiple vehicles or transporting high-value equipment. The cost difference between minimum and adequate coverage runs roughly $30 to $50 per month per vehicle-a trivial expense compared to personal bankruptcy from an underinsured claim.

Bodily injury liability covers medical expenses, lost wages, and pain and suffering for people injured in accidents you cause. Property damage liability covers repairs to other vehicles, buildings, or infrastructure. Both are non-negotiable for any business operating on Texas roads.

Collision and Comprehensive Protection for Your Assets

Collision and comprehensive coverage protect your actual business assets, not just your liability exposure. Collision coverage pays for damage to your vehicle from accidents regardless of fault, while comprehensive coverage handles theft, vandalism, weather damage, and other non-collision losses. If you finance or lease commercial vehicles, your lender requires both coverages. More importantly, if your work vehicle is totaled, you replace it immediately or your business stops generating revenue. A commercial truck worth $40,000 represents significant capital, and operating without collision coverage means absorbing that full loss yourself.

Uninsured and Underinsured Motorist Coverage Protects Your Team

Uninsured and underinsured motorist coverage protects you when another driver causes an accident but lacks sufficient insurance. Texas law allows you to reject this coverage in writing, but rejecting it is financially reckless. Uninsured motorist claims cover medical expenses and lost wages for you and your employees when hit by an uninsured driver. Underinsured motorist coverage kicks in when the at-fault driver’s policy limit falls short of your actual damages. If an employee driving your company vehicle suffers $80,000 in medical costs from an accident caused by a driver with only $30,000 in coverage, your underinsured motorist protection covers the $50,000 gap. These coverages cost roughly $15 to $25 monthly per vehicle and prevent catastrophic financial exposure.

The next critical step involves matching these coverage types to your specific business operations and risk profile.

How to Determine the Right Coverage for Your Business

Assess Your Fleet Size and Vehicle Types

Start with your vehicle inventory and nothing else. Count your vehicles, note their weights, and document what each one does. A contractor with two pickup trucks under 10,001 pounds faces different requirements than a delivery service with vehicles with a gross weight rating of 26,001 pounds or more. Heavier commercial vehicles trigger federal DOT requirements and higher liability minimums. Your vehicle’s primary use determines whether you need basic commercial coverage or specialized policies. Construction vehicles hauling equipment need cargo coverage that standard policies exclude. Delivery vehicles need higher liability limits because they operate in high-traffic areas.

Evaluate Your Business Operations and Risk Exposure

Write down exactly how each vehicle operates. Does it transport goods, equipment, or employees? Does it cross state lines? Does it sit parked most days or run continuously? A plumbing van visiting five job sites daily absorbs more accident risk than a real estate agent driving to client showings twice weekly. Once you document your fleet composition and operational patterns, you have the foundation for accurate quotes. Most business owners skip this step and request generic quotes, then wonder why their actual coverage falls short.

Compare Quotes from Multiple Insurance Providers

Request quotes from at least three providers using identical coverage limits and deductibles so you compare apples to apples. A $500 deductible costs more upfront but saves money if your vehicles rarely claim. A $1,000 deductible works for established businesses with cash reserves but exposes startups to financial strain after minor accidents. Texas businesses with multiple vehicles should ask about fleet discounts, which typically reduce per-vehicle costs by 10 to 15 percent.

Ask each insurer about bundling commercial auto with property or general liability coverage, as bundled policies often cost 15 to 25 percent less than purchasing separately. Request quotes that include rental reimbursement coverage, which pays for vehicle rentals while yours undergoes repairs. This coverage costs roughly $15 to $30 monthly per vehicle but prevents your business from stopping during repairs.

Understand Rate Variations Across Insurers

Rates vary dramatically between insurers for identical businesses and vehicles. One insurer might quote $1,200 annually while another quotes $1,800 for the same coverage. The difference compounds across multiple vehicles. An independent insurance agency can access multiple carriers and negotiate better rates than you’ll find requesting quotes individually. We at Brooks Insurance represent multiple top-rated insurance companies, which gives you a larger selection of coverage options and pricing without shopping endlessly yourself.

Final Thoughts

The answer to “do I need commercial auto insurance” is straightforward if your business operates vehicles on Texas roads: yes, you do. Texas law mandates minimum liability coverage of 30/60/25, and operating without proper coverage exposes you to fines up to $600, license suspension, and personal liability for accident damages. The real challenge lies in purchasing adequate coverage that actually protects your business when accidents happen.

Most business owners make costly mistakes by purchasing minimum liability limits and skipping collision coverage. When a serious accident generates $150,000 in damages and your policy maxes out at $60,000, you owe the $90,000 difference personally. Adequate coverage-liability limits of 100/300/100 plus collision and comprehensive protection-costs roughly $100 to $200 monthly per vehicle and prevents financial catastrophe. Your specific needs depend on your fleet size, vehicle types, and how you operate them, which is why comparing quotes from multiple insurers reveals dramatic price variations.

We at Brooks Insurance represent multiple top-rated insurance companies and can match your business operations to appropriate coverage without overpaying for unnecessary extras. Contact us today to discuss your commercial auto insurance needs and receive quotes tailored to your business.