Electrical contractors face real risks on every job site. One accident or property damage claim can threaten your entire business.

At Brooks Insurance, we know that electrical contractor general liability insurance isn’t optional-it’s essential protection. This coverage shields you from costly third-party claims and legal expenses that could otherwise drain your resources.

What General Liability Insurance Actually Covers

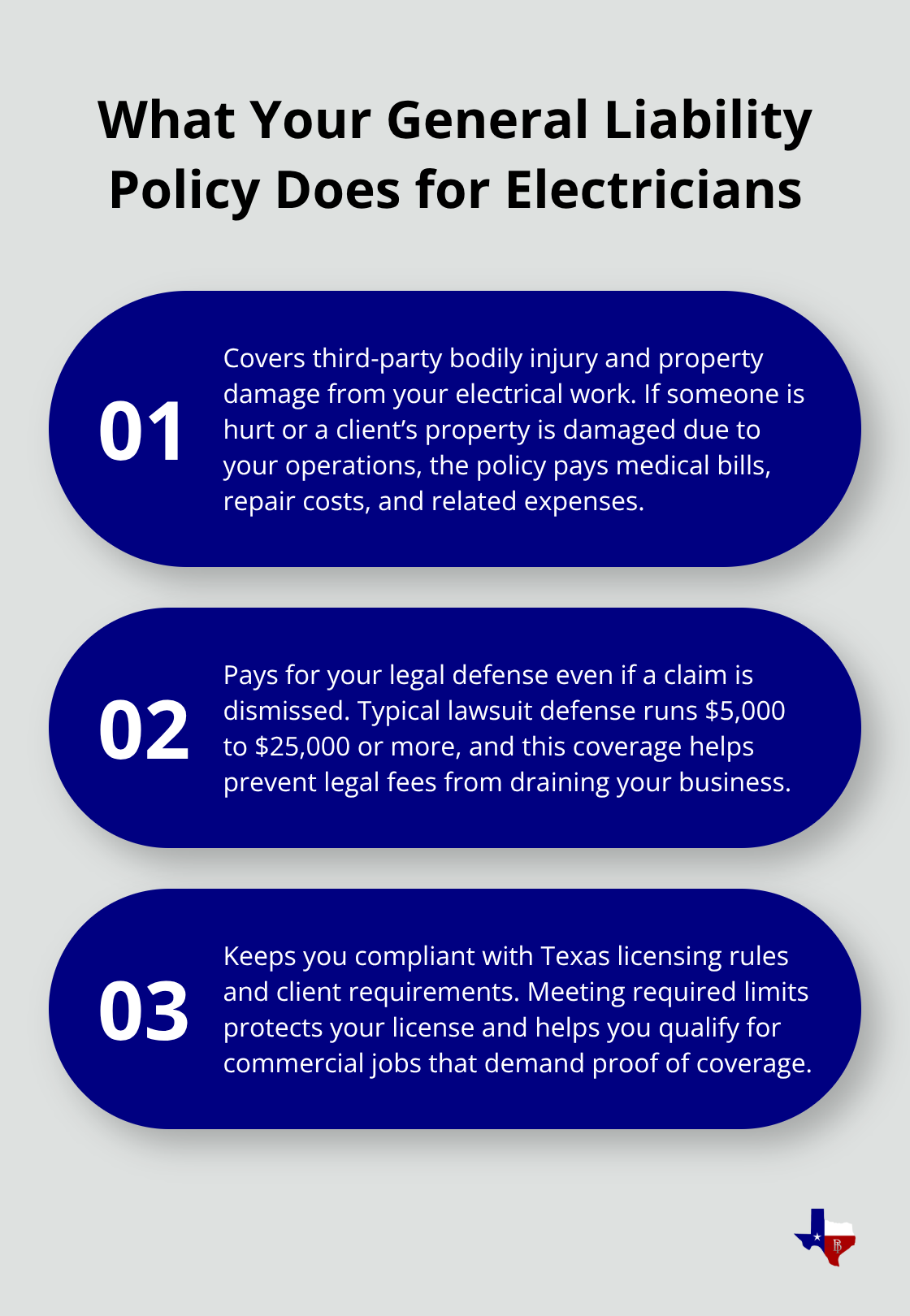

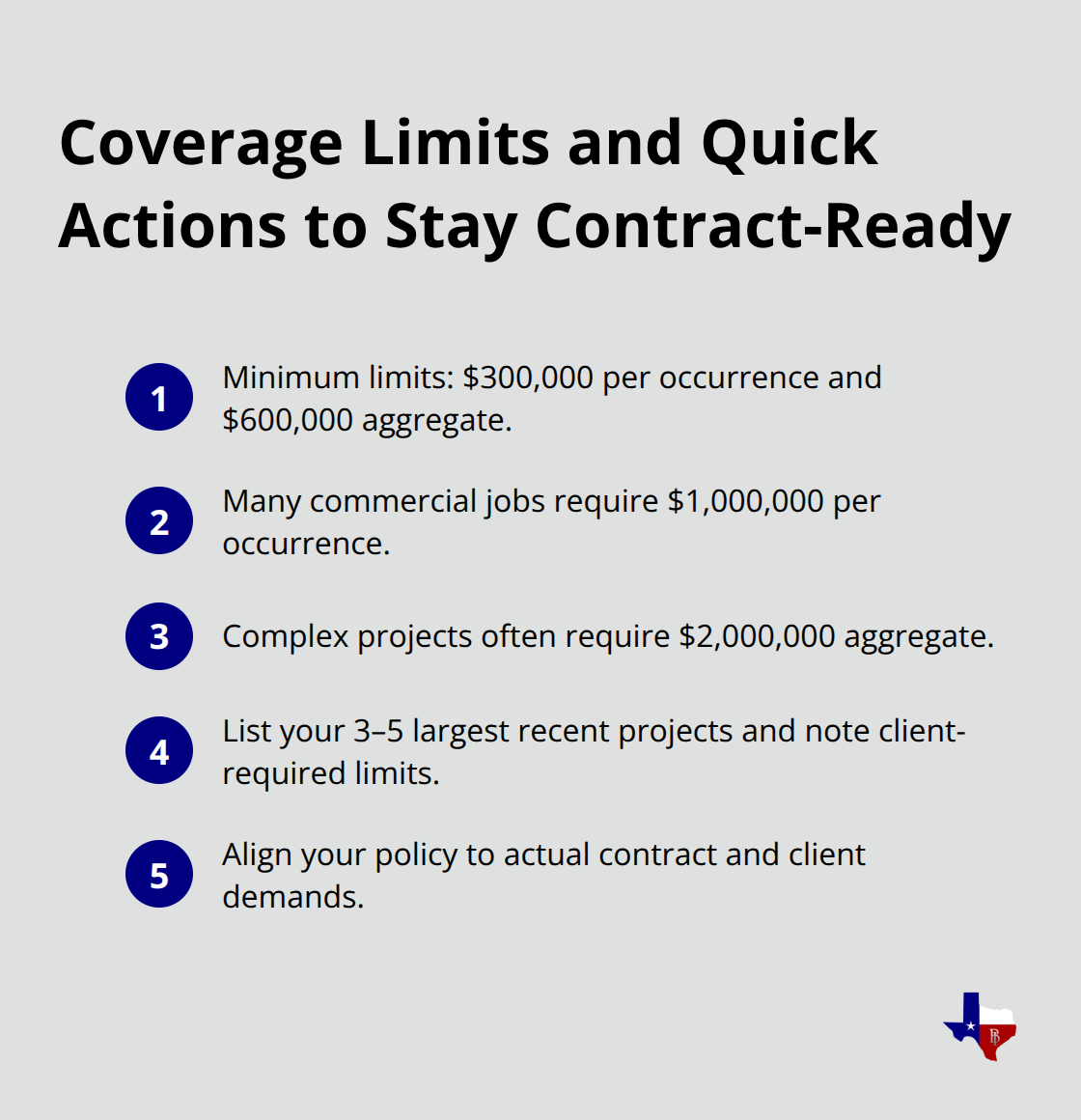

General liability insurance for electrical contractors covers bodily injury and property damage claims caused by your work or negligence on the job. If a homeowner slips on wet flooring you created while running conduit, or if your equipment damages a client’s drywall during installation, this coverage pays for their medical bills, repair costs, and legal defense. The Texas Department of Licensing and Regulation requires electrical contractors to maintain minimum coverage of $300,000 per occurrence and $600,000 aggregate, which means you need proof of this protection to keep your license active. Without it, a single accident forces you to pay thousands out of pocket and likely costs you your contracting license.

Third-Party Claims Happen on Every Job Site

Third-party claims occur when someone other than you or your employees suffers injury or property damage because of your electrical work. A property owner’s guest trips over your extension cord and breaks their arm. A neighboring business sustains water damage when you accidentally puncture a pipe while drilling. These situations happen regularly in the field, and general liability insurance handles the financial fallout so your business survives. The policy covers not just the medical or repair bills but also the legal fees if the injured party decides to sue. Most clients and general contractors won’t hire you without proof of this coverage, which makes it genuinely non-negotiable if you want steady work in Texas.

Legal Defense Costs Protect Your Bottom Line

The legal defense component of general liability insurance often gets overlooked but delivers incredible value. When someone files a claim against you, your insurer pays your attorney’s fees to defend the case, regardless of whether you actually lose. A single lawsuit defense costs $5,000 to $25,000 or more in legal fees alone, even if the claim gets dismissed. Your general liability policy covers these defense costs in addition to any settlement or judgment, so you never face the choice between hiring a lawyer and keeping your business solvent. This protection alone justifies the coverage cost, especially on complex commercial jobs where disputes tend to be more contentious and expensive to resolve.

Coverage Limits Matter for Your License and Your Contracts

Texas requires you to carry specific minimum limits ($300,000 per occurrence, $600,000 aggregate) to maintain your electrical contractor license. However, many general contractors and large commercial clients demand higher limits (often $1 million per occurrence or more) before they’ll award you work. Your policy limits determine how much your insurer pays toward claims, and limits that fall short of what clients require can cost you jobs. Choosing the right limits requires you to assess the types of projects you pursue and the contractual requirements your clients impose. The next section walks you through how to select coverage that protects your license, satisfies your clients, and fits your budget.

Why Electrical Contractors Must Carry This Coverage

Real Hazards Create Real Financial Threats

Electrical work produces genuine dangers that surface on nearly every job site. A worker on a residential rewiring project contacts a live wire and suffers a serious shock. An electrician’s ladder shifts and damages a homeowner’s kitchen cabinet during an installation. A faulty conduit installation causes a fire weeks after the job completes, destroying a business owner’s property. These incidents occur regularly in Texas, and without general liability insurance, you absorb the financial damage personally. The Texas Department of Licensing and Regulation mandates minimum coverage of $300,000 per occurrence and $600,000 aggregate specifically because these risks are real and frequent. Your license renewal depends on maintaining this coverage, but the actual protection extends far deeper than regulatory compliance. A single property damage claim or injury lawsuit costs $50,000 to $250,000 or more once medical bills, repair costs, and legal fees accumulate. That amount destroys most electrical contracting businesses operating with typical profit margins. General liability insurance transfers this financial catastrophe to an insurance carrier, allowing you to continue operating instead of facing bankruptcy from one accident.

Clients Require Proof Before They Hire You

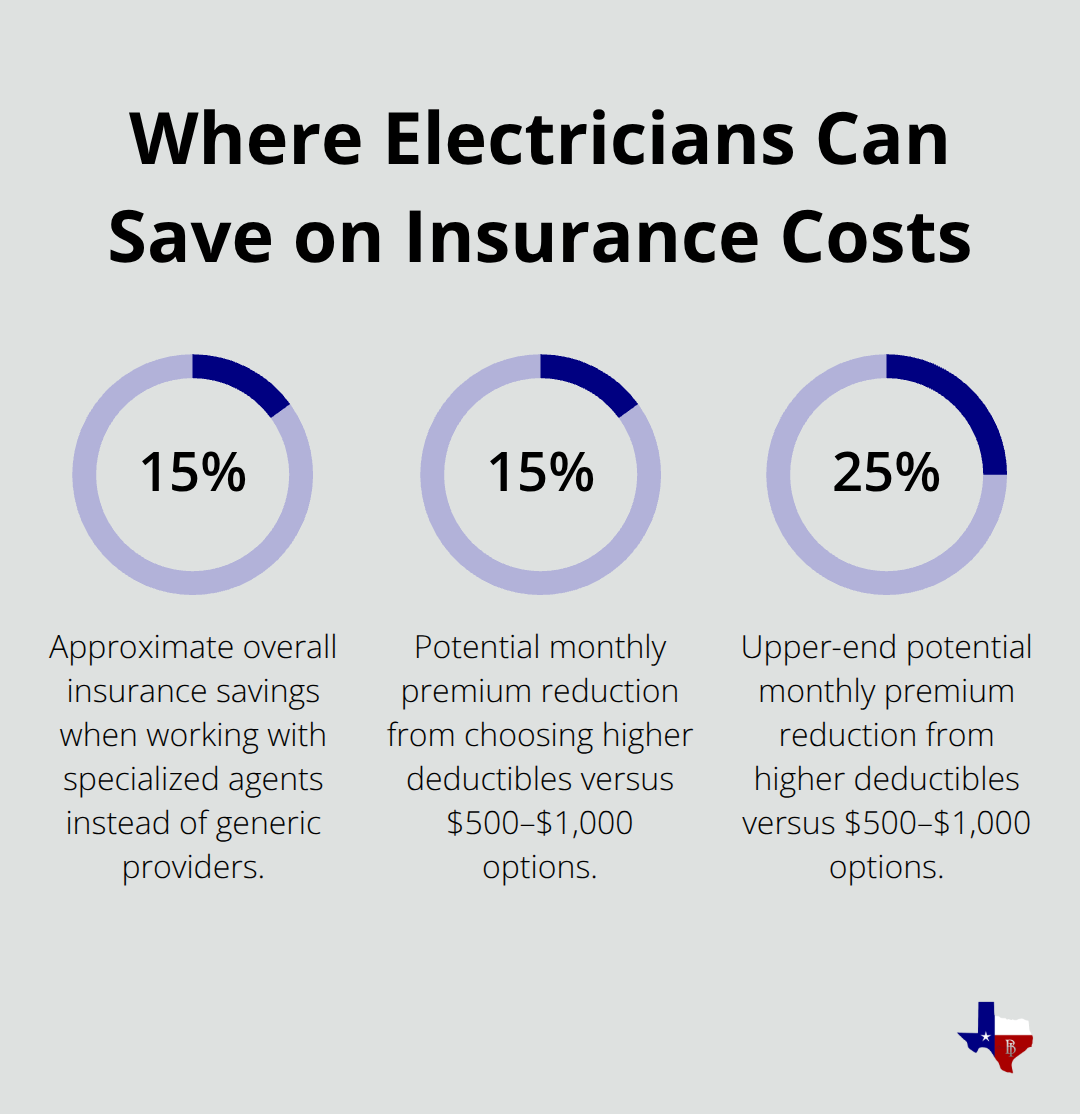

Your clients and the general contractors who hire you won’t work with you without proof of this coverage. Most commercial projects explicitly require proof of insurance before you can even bid the job. Residential clients increasingly demand certificates of insurance before allowing you on their property. If you lack coverage or carry inadequate limits, you lose access to steady work and higher-paying commercial projects. Texas electricians save approximately 15 percent on their overall insurance costs when working with specialized agents rather than generic providers, because specialists structure your coverage to match actual project requirements and client demands.

Coverage Selection Determines Your Competitive Position

Selecting the right policy upfront prevents both compliance problems and lost business opportunities. General liability protection must align with both your license requirements and the specific contracts you pursue. The next section walks you through how to assess your coverage needs and compare quotes from multiple insurers to find the protection that fits your business model and client base.

How to Choose the Right General Liability Policy

Document Your Actual Work and Client Requirements

Start by listing the specific electrical work you perform and the clients you serve. Residential rewiring jobs carry different risk profiles than commercial industrial installations, and your coverage must reflect this distinction. If you primarily handle residential work, your baseline coverage aligns with Texas regulatory minimums of $300,000 per occurrence and $600,000 aggregate. However, commercial contracts often demand $1 million per occurrence or higher before general contractors award you the job. Commercial property owners and large developers routinely require $2 million aggregate limits on complex projects.

The type of work matters significantly: high-voltage installations or work in occupied commercial spaces present greater exposure than standard residential rewiring. Document your three to five largest projects from the past year and note what coverage limits each client required. This exercise reveals your actual market demands rather than theoretical minimums.

Understand Pricing Based on Your Project Profile

General liability insurance for electricians in Texas typically costs $400 to $1,500 annually, but that range assumes standard residential work with minimum limits. Commercial-focused contractors paying for $1 million per occurrence limits often spend $1,200 to $2,500 yearly depending on claims history and project complexity. Your documented project list becomes the foundation for requesting accurate quotes from multiple carriers.

Compare Quotes from Multiple Carriers

Obtain quotes from at least three carriers before making a final decision, because pricing and available limits vary substantially between insurers. When requesting quotes, provide your actual project details rather than generic descriptions-mention specific job types, average project values, and typical client requirements. A streamlined quoting process with specialized agents often delivers estimates within two business hours for straightforward contracting needs.

As you review quotes, compare not just the premium but the deductible options available. Higher deductibles of $2,500 or $5,000 can lower your monthly costs by 15 to 25 percent compared to $500 or $1,000 deductibles, but you must have cash reserves to cover the deductible if a loss occurs. Some carriers offer endorsements like Additional Insured status, which extends coverage to your clients-this increasingly becomes a contract requirement on commercial jobs.

Verify Coverage Details and Compliance Requirements

Verify that each quote includes products and completed operations coverage, which protects you from claims arising weeks or months after a job finishes when faulty electrical work causes damage. Request certificates of insurance from your top carrier choices and confirm they match the exact format the Texas Department of Licensing and Regulation requires for license renewal applications. A carrier that generates compliant certificates quickly prevents delays when you’re renewing your license or bidding new projects.

Final Thoughts

General liability insurance for electrical contractors protects your business when accidents happen on the job site. Without this coverage, a single claim wipes out your savings, costs you your license, and damages your reputation with clients. The protection you carry today determines whether your business survives tomorrow’s unexpected incident.

We at Brooks Insurance help Texas electrical contractors secure the right coverage at competitive rates. Our licensed agents understand the specific risks you face and the exact requirements Texas imposes on your license, so we handle the compliance paperwork and generate certificates that meet TDLR specifications. Contact us today to discuss your coverage needs and receive quotes that reflect your actual project profile and client requirements.

Disclaimer: The information provided in this blog is for general informational purposes only and does not constitute legal, financial, or insurance advice. Coverage options, terms, and availability may vary. Please consult with a licensed professional for advice specific to your situation