Running a business in Texas means protecting yourself from unexpected financial losses. Two policies stand out as essential: general liability and workers’ comp insurance.

At Brooks Insurance, we see firsthand how these two coverages work together to shield your company from different risks. One protects you against customer injuries and property damage claims, while the other covers your employees’ medical costs and lost wages from workplace accidents.

What General Liability Insurance Actually Protects

Three Core Areas of Coverage

General liability insurance protects your business across three main risk areas that can quickly drain your finances. First, it covers bodily injury claims when someone gets hurt on your property or because of your business operations. If a customer slips in your office and breaks their arm, or you accidentally damage a client’s equipment during a service call, general liability pays the medical bills and repair costs. Second, it covers property damage you cause to others-such as knocking over a display at a vendor’s location or damaging a client’s building during construction work. Third, it covers personal injury claims like defamation or false advertising, plus your legal defense costs and settlements if someone sues.

What the Policy Actually Pays For

Commercial General Liability insurance protects business owners against claims of liability for bodily injury, property damage, and personal injury. The coverage also includes medical payments for minor injuries, which often prevents small incidents from escalating into lawsuits. Your policy pays for legal defense costs and settlements when claims arise. This protection applies whether the incident happens at your location, at a client’s site, or anywhere your business operations extend.

Premium Costs and Coverage Limits

Typical annual premiums vary significantly by industry. Office-based operations pay around $400 to $800 per year, retail businesses pay $750 to $1,500, and contractors and restaurants face substantially higher costs depending on their risk exposure. Most Texas businesses start with $1,000,000 per occurrence and $2,000,000 aggregate coverage, though higher-risk industries often need $2,000,000 or more per occurrence. Your premium reflects several factors: industry classification, business size, location, claims history, and the coverage limits you select. If you operate in multiple locations or take on higher-risk work, your premium increases accordingly.

Why Landlords and Clients Demand It

Many landlords require you to carry general liability before you can rent space, and clients often demand proof of coverage before you sign service contracts. This requirement isn’t optional if you want to grow your business or secure new locations. Without this coverage in place, you’ll struggle to meet contractual obligations and may lose opportunities entirely.

What General Liability Does Not Cover

One critical distinction: general liability does not cover injuries to your own employees. That protection comes from a completely separate policy-workers’ compensation insurance-which addresses employee medical costs, lost wages, and rehabilitation support from workplace accidents.

What Workers Compensation Actually Pays For

Medical Coverage for Work-Related Injuries

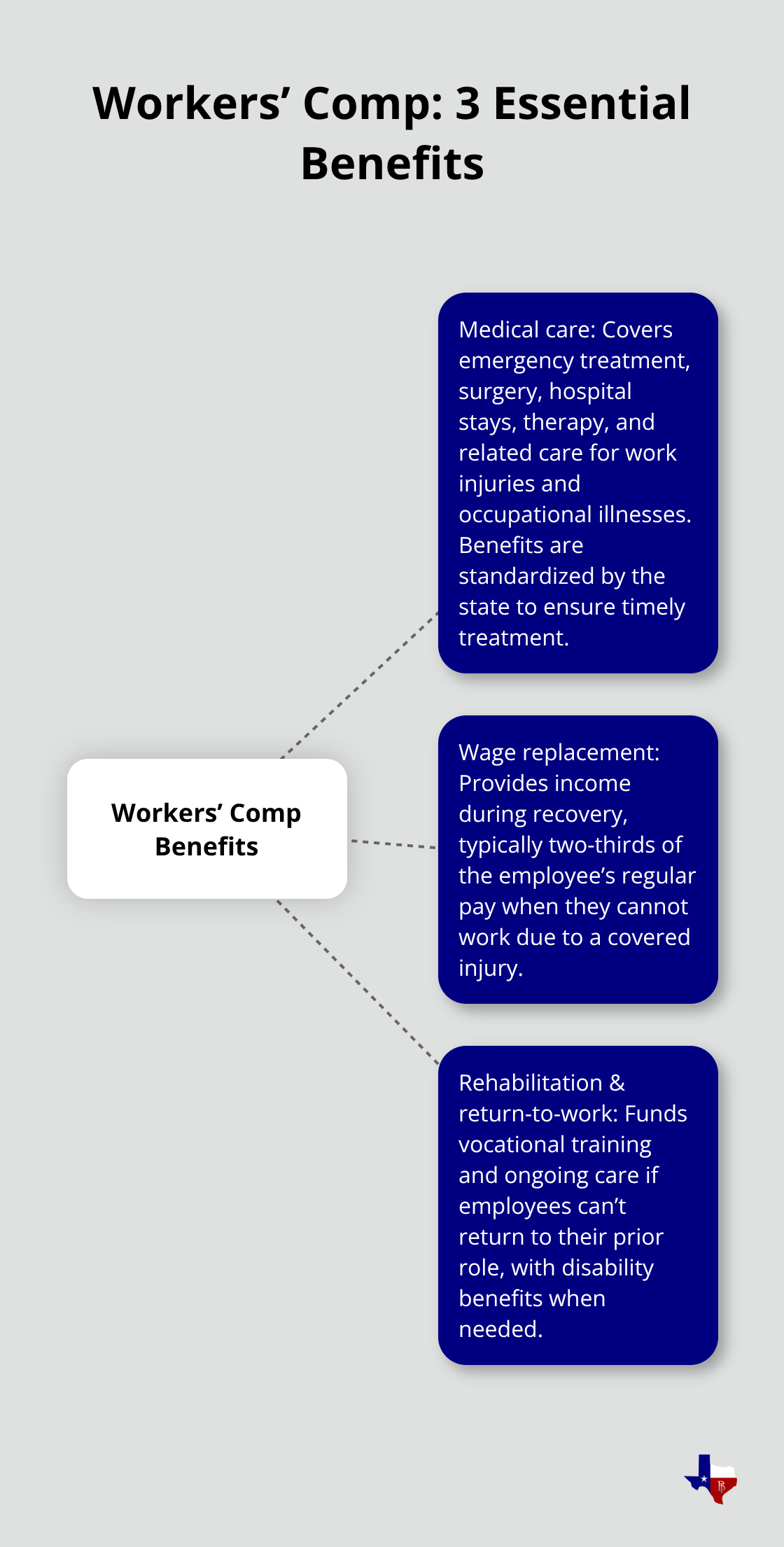

Workers’ compensation in Texas covers three essential financial protections when your employees get hurt on the job. Medical expenses come first-the policy pays for emergency care, surgery, hospital stays, physical therapy, and any treatment related to work injuries or occupational illnesses. If an employee develops carpal tunnel from repetitive work or suffers a back injury lifting equipment, workers’ comp covers all medical costs without deductibles. The Texas Department of Insurance Division of Workers’ Compensation regulates these benefits to maintain consistency across carriers and ensure employees receive necessary care promptly.

Wage Replacement During Recovery

The second protection is wage replacement, typically two-thirds of the employee’s regular pay during recovery periods. Texas law mandates this wage replacement when an employee cannot work due to a workplace injury. This income protection matters significantly because lost wages combined with medical bills can devastate a family quickly. An employee who takes eight weeks to recover from a workplace injury receives ongoing income support rather than facing financial hardship while healing.

Rehabilitation and Return-to-Work Programs

The third component is rehabilitation and return-to-work support, which includes vocational training if the employee cannot return to their original position and ongoing medical care needed for recovery. This structure recognizes that some injuries prevent workers from performing their previous jobs, so the policy funds retraining programs that help them transition to new roles. Employees who cannot work again receive disability benefits that continue based on the nature and severity of the injury.

Coverage Extends Beyond Acute Injuries

The scope of coverage extends beyond obvious accidents. Workers’ comp covers occupational diseases that develop over time, such as respiratory conditions from workplace exposure or repetitive strain injuries. An employee who develops hearing loss from years working in a loud manufacturing environment qualifies for benefits, as does someone diagnosed with an occupational illness linked to their job. If an injury or illness results in death, the policy provides burial benefits and ongoing financial support to the employee’s dependents.

Legal Protection Through Exclusive Remedy

Coverage limits in Texas follow state-mandated schedules rather than traditional policy caps, meaning benefits continue based on the nature and severity of the injury, not an arbitrary maximum. Most importantly, workers’ comp operates as the exclusive remedy in most situations-employees cannot sue their employer for workplace injuries if the employer carries coverage, eliminating costly litigation that could threaten your business. This legal protection exists because the employee receives guaranteed benefits regardless of who was at fault, creating a fair trade-off that protects both parties. Understanding how these protections work sets the stage for recognizing why general liability and workers’ comp serve fundamentally different purposes in your business risk management strategy.

Key Differences Between General Liability and Workers Comp

Who Each Policy Protects

General liability and workers’ compensation address completely separate exposures, which is why confusing them or relying on just one leaves dangerous gaps in your protection. General liability protects third parties-customers, vendors, visitors, and the public-from injuries or property damage caused by your business operations. If a client visits your office and slips on wet flooring, or you damage a vendor’s equipment during a service call, general liability covers their medical bills and repair costs. Workers’ compensation, by contrast, protects only your employees from work-related injuries and occupational illnesses, covering their medical expenses and lost wages. This distinction matters tremendously because the two policies have no overlap whatsoever.

How Claims Work Under Each Policy

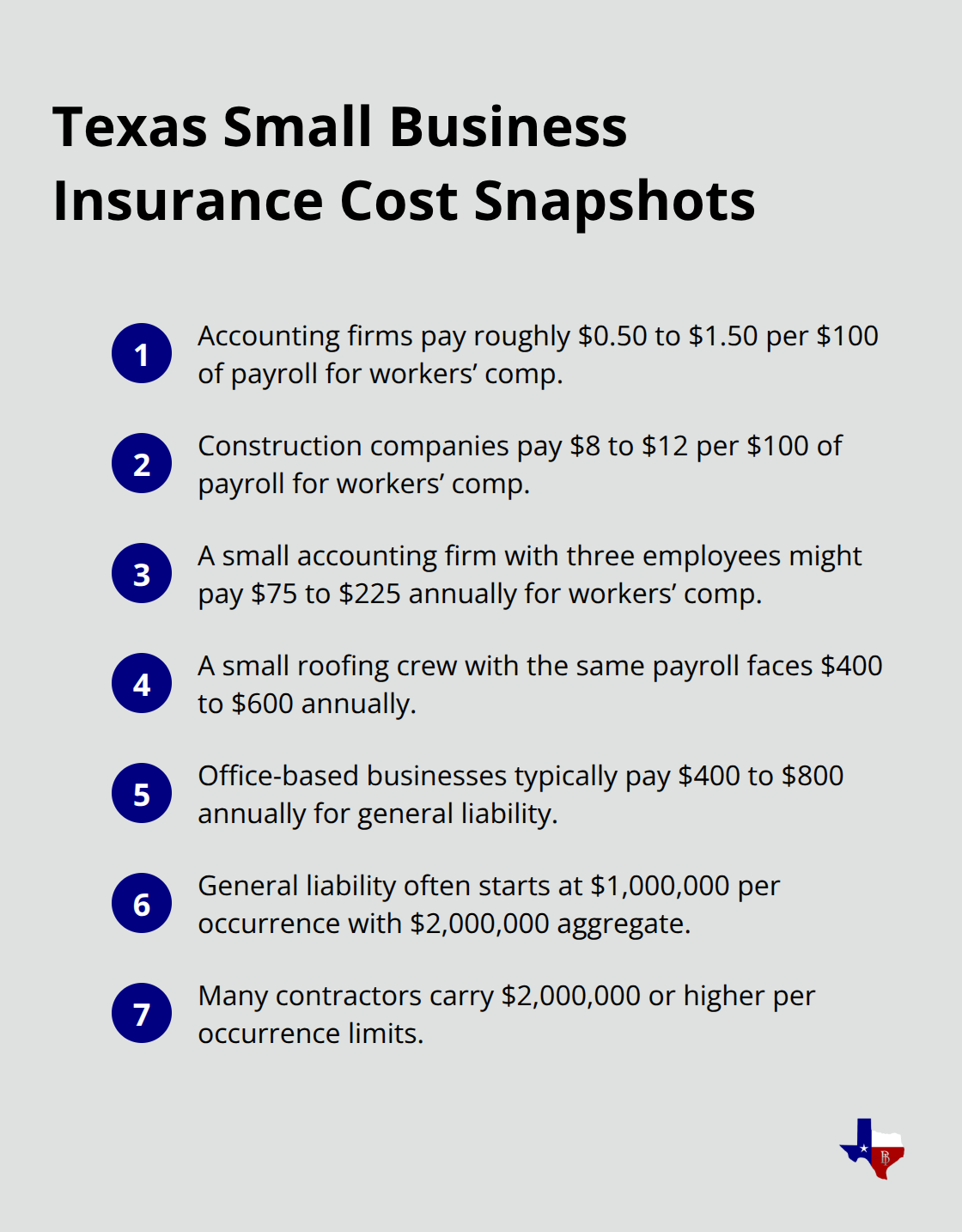

An employee injured on the job cannot claim under your general liability policy, and a customer injured at your location cannot claim under your workers’ comp policy. Each policy serves a single, specific purpose, and operating without both creates serious financial and legal exposure. The Texas Department of Insurance rate guide shows how dramatically costs vary by industry classification. Accounting firms pay roughly $0.50 to $1.50 per $100 of payroll for workers’ comp, while construction companies pay $8 to $12 per $100 of payroll-a dramatic difference driven by injury frequency and severity in each industry.

Cost Variations by Industry and Business Type

A small accounting firm with three employees earning $50,000 each might pay $75 to $225 annually for workers’ comp, whereas a small roofing crew with the same payroll faces $400 to $600 annually. Office-based businesses typically pay $400 to $800 annually for general liability. Coverage limits also diverge significantly.

General liability typically starts at $1,000,000 per occurrence with $2,000,000 aggregate, and many contractors carry $2,000,000 or higher per occurrence limits.

How Coverage Limits Work

Workers’ compensation in Texas follows state-mandated benefit schedules rather than traditional policy caps, meaning benefits continue based on injury severity and type rather than hitting a maximum dollar limit. This structure protects employees with serious, long-term injuries from losing benefits mid-recovery while simultaneously protecting your business from unlimited liability exposure through the exclusive remedy doctrine. The exclusive remedy protection means employees cannot sue their employer for workplace injuries when coverage exists, eliminating costly litigation that could threaten your business operations.

Final Thoughts

Most Texas businesses operate with incomplete protection, and that gap exposes you to financial ruin. A single uninsured employee injury costs $50,000 to $200,000 in medical expenses and lost wages, while a customer lawsuit over property damage or bodily injury easily reaches $100,000 or more. General liability and workers comp insurance address fundamentally different risks, and skipping either one leaves your company vulnerable to claims that exceed your annual revenue.

The math favors protection. Combined coverage typically costs under $100 per month for small businesses, making the investment remarkably affordable compared to the financial devastation of an uninsured claim. If you have employees, workers comp provides legal protection in Texas. If customers visit your location, you work at client sites, or you sign service contracts, general liability becomes essential. Most businesses need both policies working together to cover all their risk areas.

We at Brooks Insurance help Texas business owners select coverage that matches their actual operations and budget. Our licensed agents understand Texas-specific requirements and identify gaps in your current protection. Contact us today to review your policies, request quotes from multiple carriers, and get started protecting your business.

Disclaimer: The information provided in this blog is for general informational purposes only and does not constitute legal, financial, or insurance advice. Coverage options, terms, and availability may vary. Please consult with a licensed professional for advice specific to your situation