Flood insurance quotes in Texas vary wildly depending on where your property sits and what coverage you choose. Getting the lowest price isn’t the same as getting the right protection, and we at Brooks Insurance see too many homeowners make costly mistakes by comparing quotes without understanding what they’re actually buying.

This guide walks you through the exact process we recommend to evaluate flood insurance quotes like someone who knows what matters.

Understanding Flood Insurance in Texas

Flood insurance in Texas covers two main categories: your building structure and your personal property inside it. Under the National Flood Insurance Program, which dominates the market, building coverage maxes out at $500,000 and contents coverage at $100,000. The average NFIP flood claim payout in Texas was about $32,074 per claim according to NFIP data, which tells you most claims fall well below these limits-but some don’t. Private flood insurers can bridge this gap, offering building coverage from $500,000 up to $2.5 million or more, which matters significantly for higher-value Texas properties.

What Flood Policies Exclude

What flood policies exclude is equally important to understand. Sewer backups, sump pump overflow, burst sprinklers, vehicle damage, and top-down water from rain that doesn’t come through flooding receive no protection. Basement contents get no coverage under NFIP policies, even though basements flood regularly. Loss of temporary housing expenses after a flood also isn’t included in NFIP coverage, though some private policies do cover this-a protection that can save thousands during recovery.

Why Your Homeowners Policy Won’t Protect You

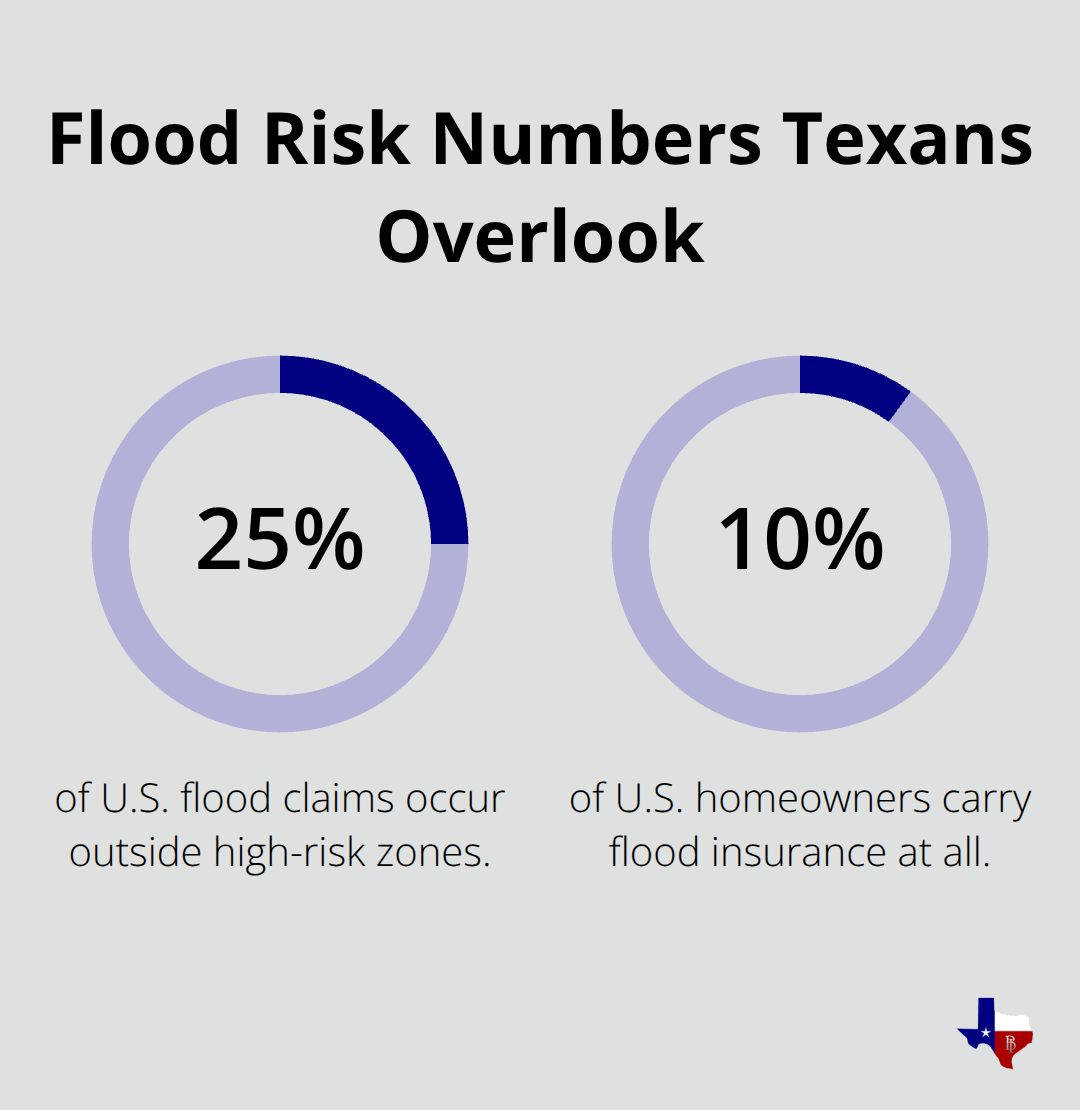

Your standard homeowners insurance deliberately excludes flood damage. This isn’t an oversight; it’s a deliberate exclusion written into nearly every homeowners policy sold in Texas. Flooding qualifies as a separate peril that requires its own dedicated policy, which is why about 25% of flood claims in the U.S. occur to homes outside high-risk zones-many homeowners assume they’re covered when they absolutely aren’t. Just 1 inch of floodwater causes approximately $25,000 in damage according to FEMA data, making this exclusion potentially catastrophic.

Texas has more flood-prone land than any other state with over 20 million acres at risk, yet only about 10% of U.S. homeowners carry flood insurance at all. In Texas specifically, roughly 6.78% of owner-occupied homes have NFIP coverage, leaving the vast majority vulnerable. Your mortgage lender will require flood insurance if your property sits in a Special Flood Hazard Area, but this protection only applies if you actually purchase the policy-and many Texans still don’t.

Finding Your Risk Zone and What It Means

FEMA flood maps divide Texas properties into zones, and your zone directly influences your quote price and coverage requirements. Zone C and X areas represent minimal to moderate risk, while Zones A, AE, and VE are Special Flood Hazard Areas where lenders typically demand coverage. The interactive Flood Claims in My Area map on FEMA’s website shows historical claim activity in your locality, providing real data about flooding patterns rather than guesses.

Being in Flash Flood Alley or coastal areas pushes premiums higher than lower-risk regions like parts of the Texas Panhandle. Baylor County averages around $1,266 annually for NFIP coverage while Martin County runs about $1,513, demonstrating how dramatically location affects cost within the same state. Texas averages about $779 per year for NFIP flood insurance, which is close to the national average of $786, but individual quotes vary wildly based on first-floor elevation above base flood level and distance from flood sources.

Your actual risk level isn’t determined solely by your perception or even your flood zone-it’s calculated using your specific elevation, proximity to water, and property replacement cost combined. These factors work together to shape what you’ll pay and what protection you actually need. Understanding this foundation prepares you to evaluate the specific factors that insurers use to build your quote.

Key Factors That Affect Your Flood Insurance Quote

How Elevation Shapes Your Premium

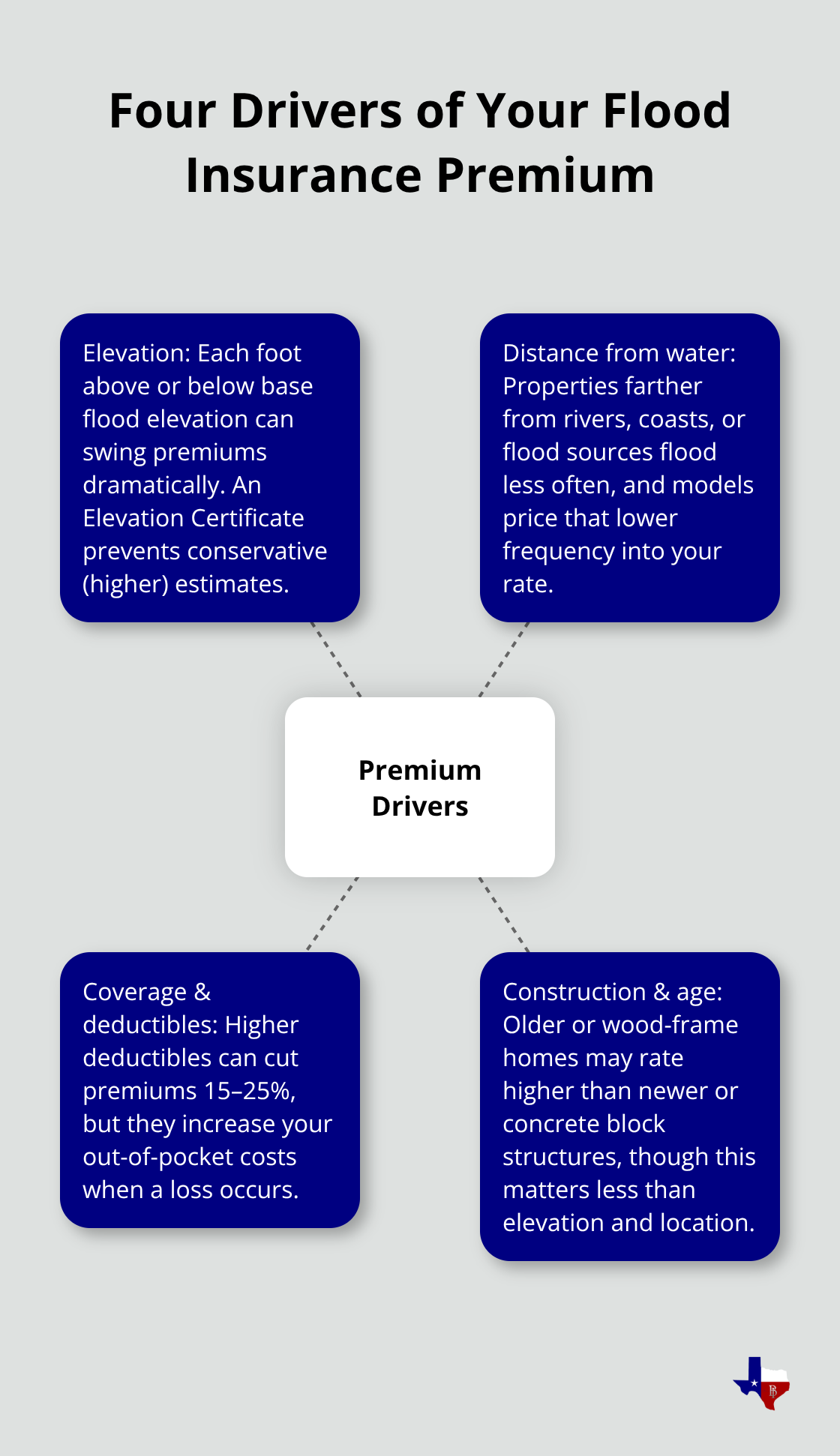

Elevation sits at the center of every flood insurance quote in Texas, and this single factor often determines whether your premium costs $600 or $6,000 annually. FEMA calculates your first-floor elevation relative to the base flood elevation for your area, and every foot matters dramatically. A property with a first floor sitting 3 feet above base flood level pays substantially less than one at the same elevation or below it, because insurers price risk based on the mathematical probability of water reaching your living spaces.

You can obtain an Elevation Certificate from a surveyor, and this document becomes your most powerful tool when comparing quotes. Without it, insurers estimate your elevation conservatively, which inflates your quote. Securing this certificate before requesting quotes from multiple carriers prevents you from overpaying on every single estimate you receive.

Distance From Water and What You Cannot Control

Distance from flood sources compounds elevation’s impact on your price. A property 2 miles from a river floods less frequently than one 200 feet away, and your insurer’s actuarial data reflects this reality. When you request quotes, the underwriters pull this information automatically from FEMA flood maps and their own flood modeling, so you cannot negotiate around it.

Coverage Limits and Deductibles: Where You Control Cost

What you can control is your coverage limits and deductible structure, which represent the second major lever affecting your quote price. Selecting a $5,000 deductible instead of $1,000 typically reduces your annual premium by 15 to 25 percent, depending on your risk profile and the insurer. However, this strategy backfires if you experience a flood and suddenly face $5,000 out of pocket before insurance kicks in. Try matching your deductible to the amount you could actually pay after a loss without financial hardship, not simply chasing the lowest premium.

Building coverage limits tell the real story about whether a quote protects you adequately. If your home’s replacement cost totals $450,000 but you quote only $250,000 in building coverage through NFIP, you create a $200,000 protection gap that a flood would expose catastrophically. Private flood insurers fill this gap by offering limits up to $2.5 million or beyond, which costs more upfront but eliminates the scenario where your claim payout falls short of rebuilding expenses.

Construction Type and Age

Older homes and those built with wood frame construction sometimes attract higher premiums than newer concrete block structures, though this factor matters far less than elevation and location in Texas flood pricing. Request identical coverage limits and deductibles across all your quotes to make true price comparisons, because quoting $250,000 building coverage from one carrier and $500,000 from another makes the quotes useless for comparison purposes. These apples-to-apples comparisons reveal which insurers actually offer the best value for your specific situation, setting the stage for the detailed analysis that separates a good quote from the right one.

How to Effectively Compare Flood Insurance Quotes

Start by gathering quotes from at least three to five different carriers operating in Texas, because FEMA’s Risk Rating 2.0 system means NFIP quotes from different insurers will be nearly identical, but private flood carriers compete aggressively on price and terms. The NFIP provider directory lists 50 participating flood insurers nationwide, with Texas included, so you have genuine options beyond the standard NFIP path. Major national insurers like Allstate, American Family, and Auto Owners participate in Texas NFIP, while private carriers such as Chubb, Neptune Flood, and Aon Edge operate separately with their own pricing models. Use the NFIP Get a Quote tool to pull your baseline NFIP estimates, then request quotes directly from at least two private insurers to see the actual price difference.

Request Identical Information Across All Quotes

When you request quotes, provide identical information to each carrier: your property’s elevation certificate if available, the same coverage limits, and the same deductible amounts. Requesting $250,000 building coverage from one insurer and $500,000 from another creates worthless comparisons because you cannot determine which carrier offers better value. Specify whether you want replacement-cost or actual cash value basis for contents coverage, since this choice affects both premium and claim payout significantly. Private insurers typically offer replacement-cost coverage for contents, while NFIP defaults to actual cash value, meaning you recover less after a loss under NFIP’s approach. Request quotes with identical deductibles-try $2,500, $5,000, and $10,000 from each carrier to see how deductible choices shift premiums across the board.

Look Beyond the Annual Premium

The annual premium matters far less than understanding what protection you actually receive for that price. A $600 annual quote sounds attractive until you discover it includes only $100,000 contents coverage when your household goods total $175,000, leaving a $75,000 gap that no claim will cover. Review each quote’s exclusions with genuine attention: does it cover sewer backup, and if so, what is the limit and what triggers coverage?

Some private policies include loss of use coverage for temporary housing after a flood, while NFIP excludes it entirely, yet this protection can save thousands during recovery if you must rent elsewhere while your home rebuilds. Check whether increased cost of compliance appears in the policy, because some private carriers cover the expense of bringing your home up to current building codes after a flood, while NFIP specifically excludes this cost. Basement contents coverage separates strong quotes from weak ones-NFIP covers nothing in basements, but private policies often extend coverage to belongings stored below ground. Verify the waiting period each quote specifies before coverage activates: NFIP typically requires 30 days, while private policies often start in 7 to 15 days or sooner, which matters enormously if you purchase coverage before flood season arrives. Request that each insurer confirm they accept your specific lender’s requirements, because some lenders restrict which private carriers they accept, and switching from NFIP to a private policy requires lender approval before your prior coverage ends.

Assess Financial Strength and Claims Handling

Price and coverage terms mean nothing if the insurer cannot pay your claim when flooding occurs. Verify financial strength using AM Best or S&P Global ratings before selecting any carrier, because an insurer offering the lowest premium becomes worthless if it fails financially during a catastrophic year. Research customer service reputation through independent reviews on Google and the National Association of Insurance Commissioners website, where you can check complaint ratios for each carrier operating in Texas. Ask about claims handling directly: how many days does the insurer typically take to respond to a claim, and can you file claims online or only through phone calls and paperwork? Contact the insurer’s claims department with a hypothetical scenario to assess responsiveness-if they answer your questions thoroughly, they likely handle actual claims professionally.

Work With an Independent Agent

An independent agent from the TrustedChoice network can provide professional guidance comparing multiple quotes simultaneously, since agents coordinate carrier acceptability with your lender and prevent coverage gaps when transitioning between policies. An independent agency represents multiple carriers and can navigate lender requirements across several options at once, rather than forcing you to contact each insurer individually and verify acceptance separately.

Final Thoughts

Comparing flood insurance quotes in Texas requires discipline and attention to detail, but the effort pays dividends when you avoid both underinsurance and overpaying for protection you don’t need. The process boils down to three concrete steps: gather quotes from multiple carriers using identical coverage specifications, analyze what each policy actually covers beyond the annual premium, and verify financial strength before committing to any insurer. Most Texans accept the first quote they receive, which typically costs them hundreds of dollars annually in unnecessary premiums or leaves them exposed to catastrophic gaps in coverage.

Your flood insurance quotes Texas comparison should include at least one NFIP estimate and two private carrier quotes, since private insurers often undercut NFIP pricing significantly while offering superior coverage terms. Request identical deductibles and building limits across all quotes so you can actually determine which carrier delivers better value rather than comparing apples to oranges. Pay special attention to what each policy excludes and what additional protections it includes, because a $200 annual savings means nothing if the cheaper policy omits sewer backup coverage or loss of use protection that you desperately need after a flood.

The final step involves working with a professional who understands Texas flood risk and can coordinate your coverage transition without gaps. We at Brooks Insurance represent multiple top-rated carriers rather than pushing you toward a single option, and our licensed agents can compare quotes from different insurers simultaneously while verifying lender acceptance before you switch policies. Contact Brooks Insurance today to discuss your flood insurance needs and receive personalized guidance on selecting the right protection for your Texas property.

Disclaimer: The information provided in this blog is for general informational purposes only and does not constitute legal, financial, or insurance advice. Coverage options, terms, and availability may vary. Please consult with a licensed professional for advice specific to your situation