A single liability claim can cost you hundreds of thousands of dollars-or more. Most business owners and professionals in Texas underestimate their exposure to lawsuits and damages.

This liability policy guide walks you through what you actually need to know about protecting yourself. At Brooks Insurance, we help Texas residents and business owners understand their real risks and build coverage that matches their situation.

What Liability Insurance Actually Covers

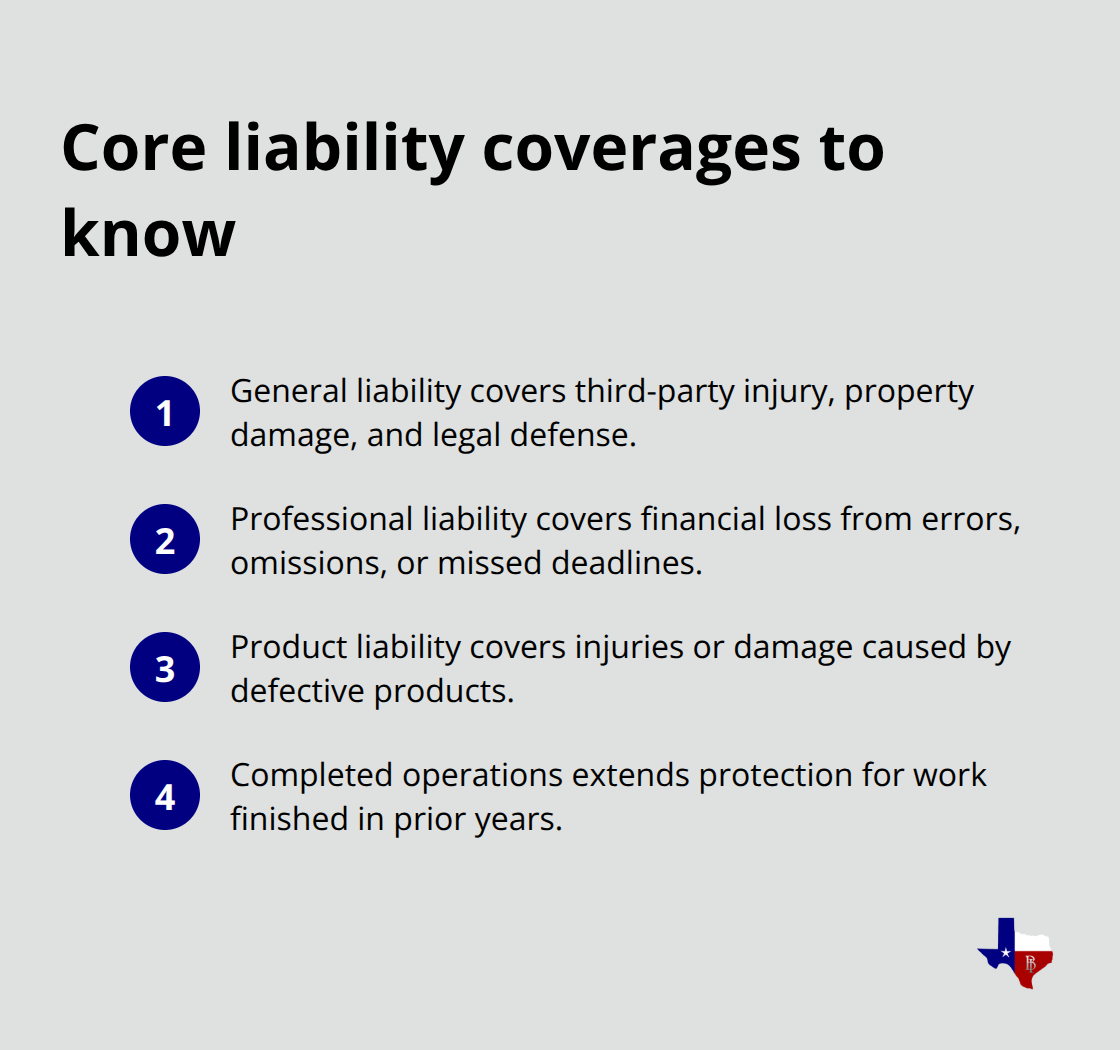

Liability insurance protects you when someone claims you caused them bodily injury, property damage, or financial harm. We at Brooks Insurance view this protection as the foundation of smart risk management, not an optional add-on. The core coverage pays for legal defense costs, medical bills, repair expenses, and court settlements up to your policy limits. General liability covers third-party claims that arise from your business operations or premises. Professional liability protects service providers like consultants, accountants, and IT firms against claims that your work caused financial loss or damage. Product liability covers injuries or property damage caused by something you manufactured or sold. Most Texas business owners carry these three types, though your specific needs depend entirely on what you actually do and who you serve.

Why the Numbers Matter in Texas

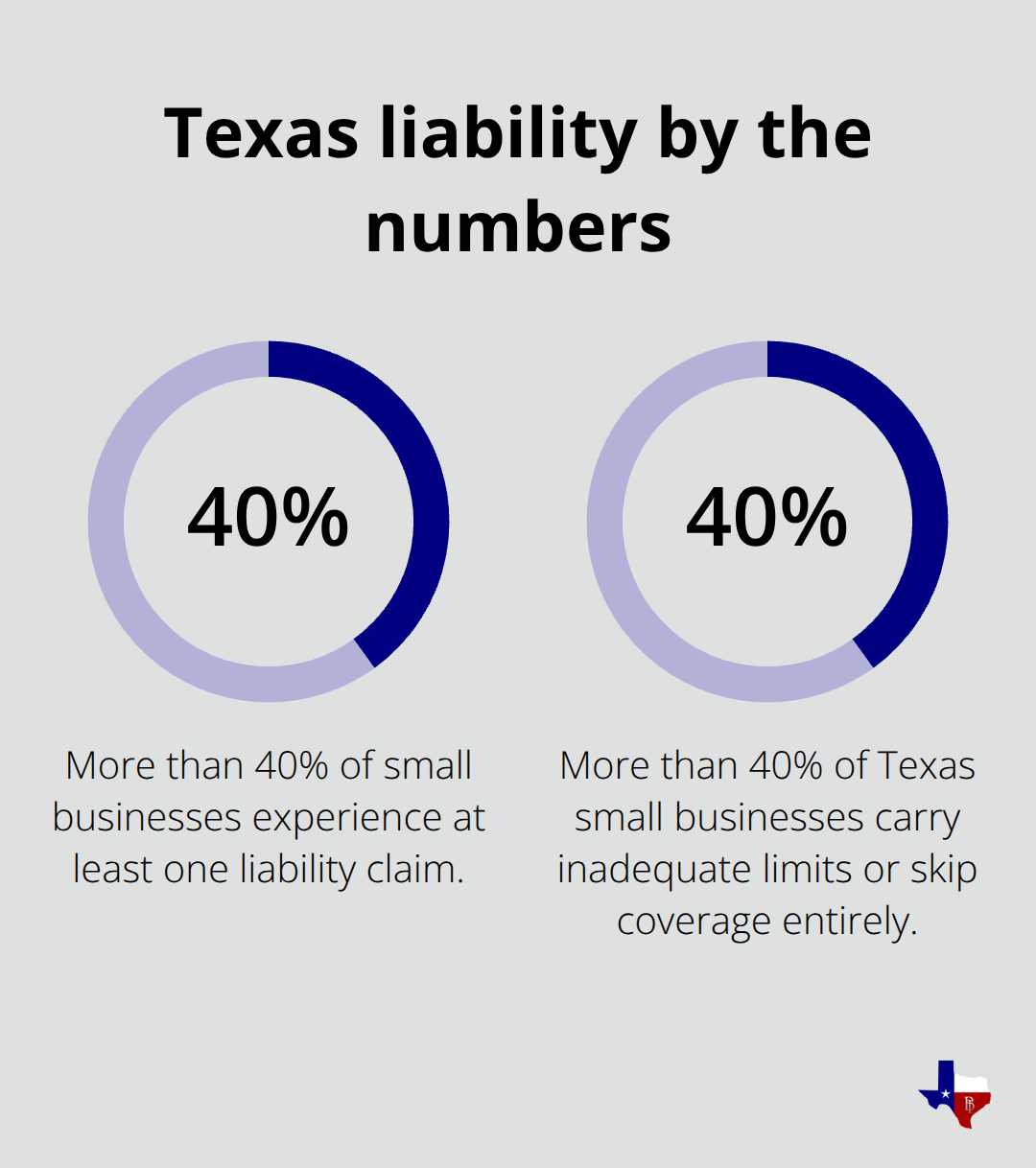

More than 40% of small businesses experience at least one liability claim, according to Progressive Commercial data. That statistic alone should shift how you think about coverage. A single lawsuit can exceed $100,000 in legal fees before any settlement is paid.

Texas courts award substantial damages in personal injury cases, especially when negligence is clear. The median monthly premium for general liability runs around $60 for small businesses, making this protection genuinely affordable compared to the financial devastation of an uninsured claim. Your industry shapes your risk profile significantly. Construction firms, healthcare providers, and hospitality businesses face higher exposure than others, which is why many clients and landlords now require proof of active coverage before hiring contractors or signing leases. If you operate in Texas and work with commercial clients, expect certificate of insurance requests to become routine.

Correcting What Business Owners Get Wrong

Many Texas business owners believe their homeowner’s or personal auto policy covers their business liability. It does not. Business activities are explicitly excluded from personal policies, leaving you completely unprotected when a client gets hurt on your job site or claims your service caused damage. Others assume their business liability covers employee injuries. It does not-workers’ compensation covers that instead. Some think higher limits cost proportionally more, so they carry the absolute minimum to save money. This false economy backfires when a legitimate claim exceeds your limits and your personal assets become vulnerable. A few business owners skip liability coverage entirely because they believe they are too small to get sued. Size does not matter. A slip-and-fall incident, a mistake in your professional work, or a product defect can trigger claims regardless of your revenue. The cost of coverage is insignificant compared to the financial exposure you accept when you go without it.

What Happens When You Underestimate Your Exposure

Texas business owners often carry limits that sound reasonable until a real claim arrives. A contractor’s error on a commercial project can cost far more than the $300,000 general liability limit they thought was sufficient. A consultant’s missed deadline that costs a client millions in lost revenue creates liability exposure that standard professional coverage may not fully address. A product defect that injures multiple people multiplies your exposure across several claims. These scenarios (which happen regularly in Texas) expose the gap between what you think you need and what you actually need. The solution is not to panic-it is to assess your actual risk based on your industry, your client base, and your revenue. Higher limits cost more, but the difference is often modest when you compare it to the catastrophic cost of an uninsured or underinsured claim.

Moving Forward With Confidence

Understanding what liability insurance covers and what it does not is the first step toward real protection. The next step is evaluating whether your current limits match your actual exposure. Different industries face different risks, and different business models create different claim patterns. Your construction company faces different liability exposure than your consulting firm or your product manufacturing operation. The limits that protect one business may leave another dangerously exposed.

Types of Liability Coverage You Need to Know

General Liability: Your Foundation for Protection

General liability forms the bedrock of business protection in Texas. This coverage pays for bodily injury claims when someone gets hurt on your premises or during your operations, property damage claims when you accidentally damage a client’s belongings, and legal defense costs regardless of whether you ultimately lose the case. The median monthly premium around $60 for small businesses makes this genuinely affordable, yet more than 40% of Texas small businesses still carry inadequate limits or skip it entirely.

Your general liability limit structure typically uses a per-claim and aggregate format, such as $1 million per claim and $2 million aggregate annually. This means one serious injury claim could consume your entire annual protection if your limits are set too low. Construction companies, contractors, and service providers face the highest exposure here because their work directly impacts client property and safety. If you work on someone else’s property or deliver services in their location, a $300,000 general liability limit is dangerously low when a single mistake can exceed $100,000 in legal fees alone before any settlement is paid.

Professional Liability for Service-Based Work

Professional liability protects service providers like consultants, accountants, IT professionals, and engineers against claims that your work caused financial loss, missed deadlines, or professional errors. This coverage differs fundamentally from general liability because it covers the quality and outcome of your services, not just physical accidents. A consultant who misses a critical deadline that costs a client millions, an accountant whose tax advice creates an audit problem, or an IT firm whose security recommendation leaves a client vulnerable to a data breach all face professional liability exposure that general liability simply does not cover.

Product Liability and Completed Operations

Product liability applies if you manufacture, distribute, or sell anything tangible, covering injuries or property damage caused by defects in design, manufacturing, or warnings. If you sell imported goods, verify they meet applicable safety standards and include proper labeling and instructions, because product liability claims multiply quickly when multiple customers experience similar injuries from the same defect. Completed operations coverage extends your general liability protection for work you finished in prior years, which matters significantly in construction and contracting where claims sometimes surface months or years after a project ends.

Industry-Specific Exposure Levels

Texas businesses in hospitality, healthcare, and construction industries face the highest liability exposure across all three types, which is why clients and landlords now routinely require certificates of insurance before engaging contractors or approving leases. Your specific coverage needs depend on whether you work with high-value clients, operate in regulated industries, or sell products with inherent safety risks. The limits that protect one business may leave another dangerously exposed, which is why the next step involves assessing your actual industry exposure and matching your coverage to your real operational risks.

How to Choose the Right Liability Limits for Your Situation

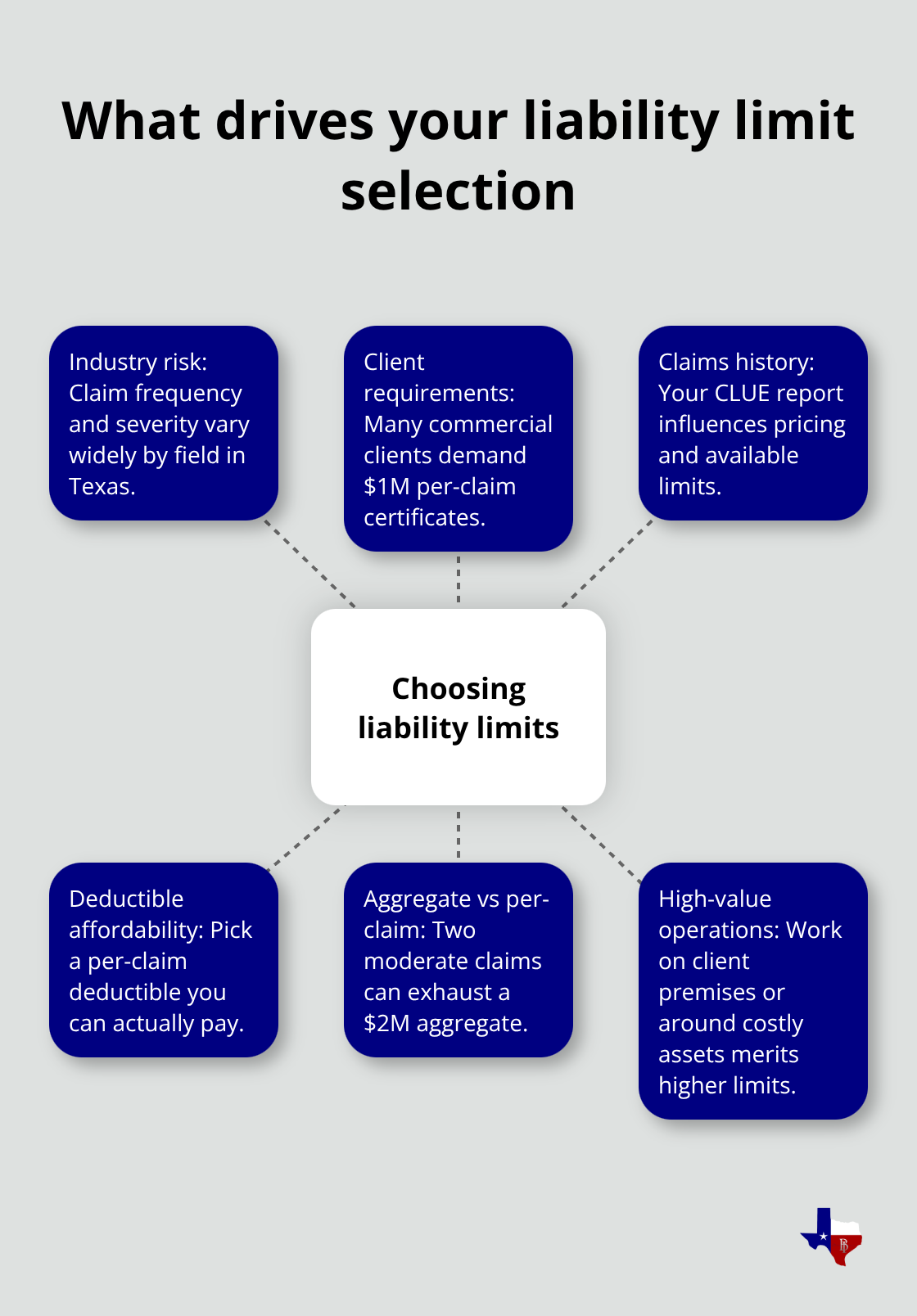

Your industry determines your exposure more than any other factor. A consulting firm handling client data faces vastly different risks than a plumbing contractor working on residential properties, yet many Texas business owners apply generic limits across completely different operational models. Construction companies, healthcare providers, and product manufacturers in Texas face significantly higher claim frequencies and severity than other industries, which means your limits must reflect what actually happens in your field, not what sounds reasonable in theory. The Texas Transportation Code establishes minimum motor vehicle liability at $30,000 per person and $60,000 per accident for bodily injury, plus $25,000 for property damage, but these statutory minimums represent financial responsibility baselines, not adequate business protection. A single commercial liability claim regularly exceeds $100,000 in legal defense costs alone before any settlement is paid. If you work with high-value clients, operate on their premises, or sell products with inherent safety risks, carrying limits near the minimum is essentially operating uninsured.

Assessing Your Industry-Specific Risk Exposure

Start by identifying what your clients and landlords actually require. Many commercial clients now demand certificates of insurance showing $1 million general liability before they hire contractors or approve service providers. If your current limits fall below what clients are requesting, you are already losing business opportunities and signaling financial weakness to potential customers. Your claim history shapes how insurers price your coverage and what limits they will offer. Request your CLUE report from LexisNexis, which documents all property and liability claims filed on your business over the past five years. If your CLUE report shows frequent small claims, insurers may require higher deductibles or lower limits, forcing you to address the underlying operational issues causing claims rather than simply buying more coverage.

Understanding Coverage Limits and Deductibles

Deductible structure matters as much as limit selection because deductibles directly impact your out-of-pocket exposure when a claim arrives. Most Texas business policies use per-claim deductibles ranging from $250 to $1,000, meaning you pay that amount toward each separate incident before your insurance coverage activates. A higher deductible reduces your monthly premium, but only if you can genuinely afford to pay it when a claim happens. Try setting your deductible at a level your business can absorb without financial stress, because choosing a $1,000 deductible to save $20 monthly becomes a terrible decision when you face a legitimate claim and cannot afford to pay it. Your aggregate limit determines your total annual coverage across all claims combined. A $2 million aggregate limit sounds substantial until you experience two moderate claims that together consume your entire year’s protection, leaving you uninsured for any subsequent incidents.

Practical Steps to Evaluate Your Current Protection

Calculate your actual exposure by identifying your highest-value client relationships, the maximum revenue at risk if your services fail, and the costliest injury scenario your operations could realistically produce. A consultant managing a $5 million client project faces different exposure than a consultant managing $100,000 projects, yet many service providers carry identical limits regardless of client size. Match your professional liability limits to your actual client engagement values, and match your general liability limits to the property values you work around and the number of employees or contractors you manage. Your specific coverage needs depend on whether you work with high-value clients, operate in regulated industries, or sell products with inherent safety risks. The limits that protect one business may leave another dangerously exposed, which is why this assessment process directly shapes whether your current protection actually matches your real operational risks.

Final Thoughts

Liability protection demands regular attention as your business evolves. Your client base grows, your revenue increases, and your operational risks shift with each new project or service line you add. The liability policy guide you have just read provides the framework for understanding what you actually need, but the real work happens when you assess your specific situation and match your coverage to your actual exposure.

More than 40% of Texas small businesses experience at least one liability claim, and a single uninsured or underinsured incident can cost you hundreds of thousands of dollars or more. Your industry determines your exposure level, your client relationships determine your limit requirements, and your claims history determines what coverage options are available to you. A $300,000 general liability limit disappears quickly when legal defense costs alone exceed $100,000 before any settlement is paid.

Review your current liability coverage and compare it against the actual exposure you identified while reading this guide. If your limits fall below what your clients require or what your industry typically experiences, contact Brooks Insurance to discuss your options. Our licensed agents understand Texas business risks and can help you evaluate whether your current protection actually works when claims happen.

Disclaimer: The information provided in this blog is for general informational purposes only and does not constitute legal, financial, or insurance advice. Coverage options, terms, and availability may vary. Please consult with a licensed professional for advice specific to your situation