Floods are the most expensive natural disaster in Texas, with homeowners filing over 100,000 claims annually. Standard homeowners insurance won’t protect you-that’s where flood coverage becomes essential.

We at Brooks Insurance help Texas homeowners understand their options. This Texas flood insurance guide walks you through everything from risk assessment to finding the right policy for your situation.

Why Your Homeowners Policy Leaves You Exposed to Floods

Standard homeowners insurance simply does not cover flood damage-this is a hard fact that catches most Texas homeowners off guard. Your policy covers wind, hail, theft, and fire, but water damage from flooding falls into a separate category that insurers deliberately exclude. This exclusion exists because flood risk is too unpredictable and concentrated in specific geographic areas for traditional homeowners policies to absorb. If you live in Texas, you need to understand this gap immediately, because a single flood event can cost tens of thousands of dollars in damages. According to FEMA, average claim payment of $66,000 from 2016 to 2022 came through the NFIP-money that your homeowners policy will not provide.

Texas Flood Risk Extends Far Beyond High-Risk Zones

Texas holds six of the twelve highest rainfall amounts ever recorded in a 24-hour period worldwide, and this extreme weather pattern shows no signs of slowing down. Central Texas earned the nickname Flash Flood Alley because flash flooding is the number one natural disaster threat to that region. In May 2015 alone, 35 trillion gallons of rain fell across Texas, enough to cover the entire state with eight inches of water. This wasn’t a rare occurrence-from 2013 to 2016, Texas experienced seven federally declared disasters due to flooding.

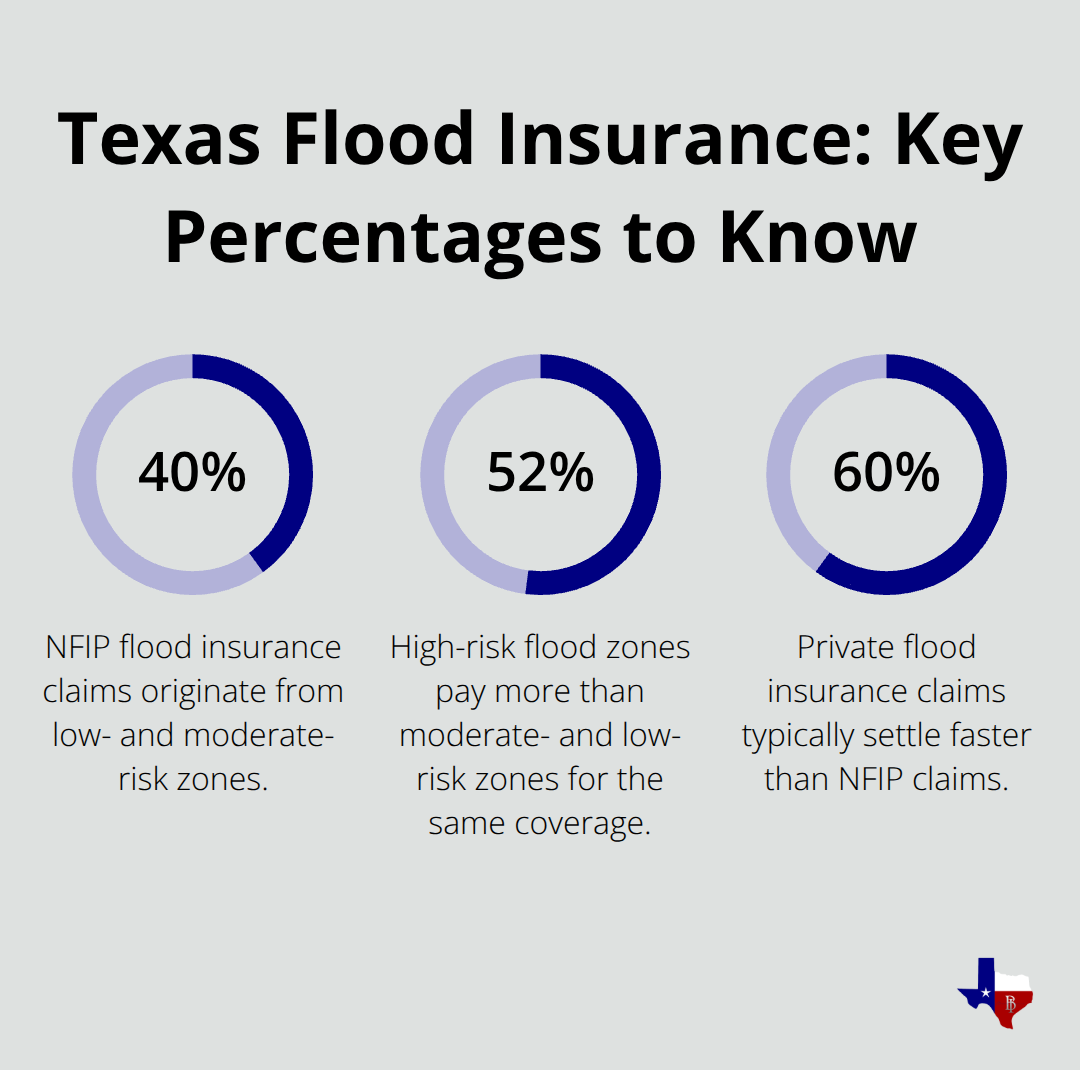

The critical insight here is that about 40 percent of NFIP flood insurance claims come from low- and moderate-risk flood zones, not just the high-risk areas that FEMA designates. You can live outside a designated flood zone and still face serious flood risk. Check your specific flood zone on FEMA’s Flood Map Service Center to see your property’s designation, but understand that this map represents only part of your actual exposure.

Flood Claims Drive Rising Premiums Across Texas

Texas homeowners filed over 100,000 flood insurance claims annually in recent years, creating upward pressure on premiums across the state. In 2015 alone, Texas had approximately 9,950 flood insurance claims that totaled $468.46 million in payouts. This volume of claims has pushed NFIP premiums higher, and private insurers have responded by tightening their underwriting standards and increasing rates in high-risk areas.

The average cost of NFIP flood insurance in Texas is about $783 per year, but this figure masks significant regional variation. Galveston County averages around $992 annually, while Harris County sits near $786. High-risk flood zones pay approximately 52 percent more than moderate- and low-risk zones for the same coverage. The message is clear: waiting to purchase flood insurance until after a storm forecast appears will be too late, because NFIP policies carry a 30-day waiting period before coverage takes effect. Starting your flood insurance process now gives you time to compare options and avoid the rush that follows storm warnings.

With this understanding of Texas flood risk and the gaps in standard homeowners coverage, you’re ready to explore the flood insurance options available to you.

Navigating Your Two Main Flood Insurance Paths

The National Flood Insurance Program: Standardized Coverage and Federal Backing

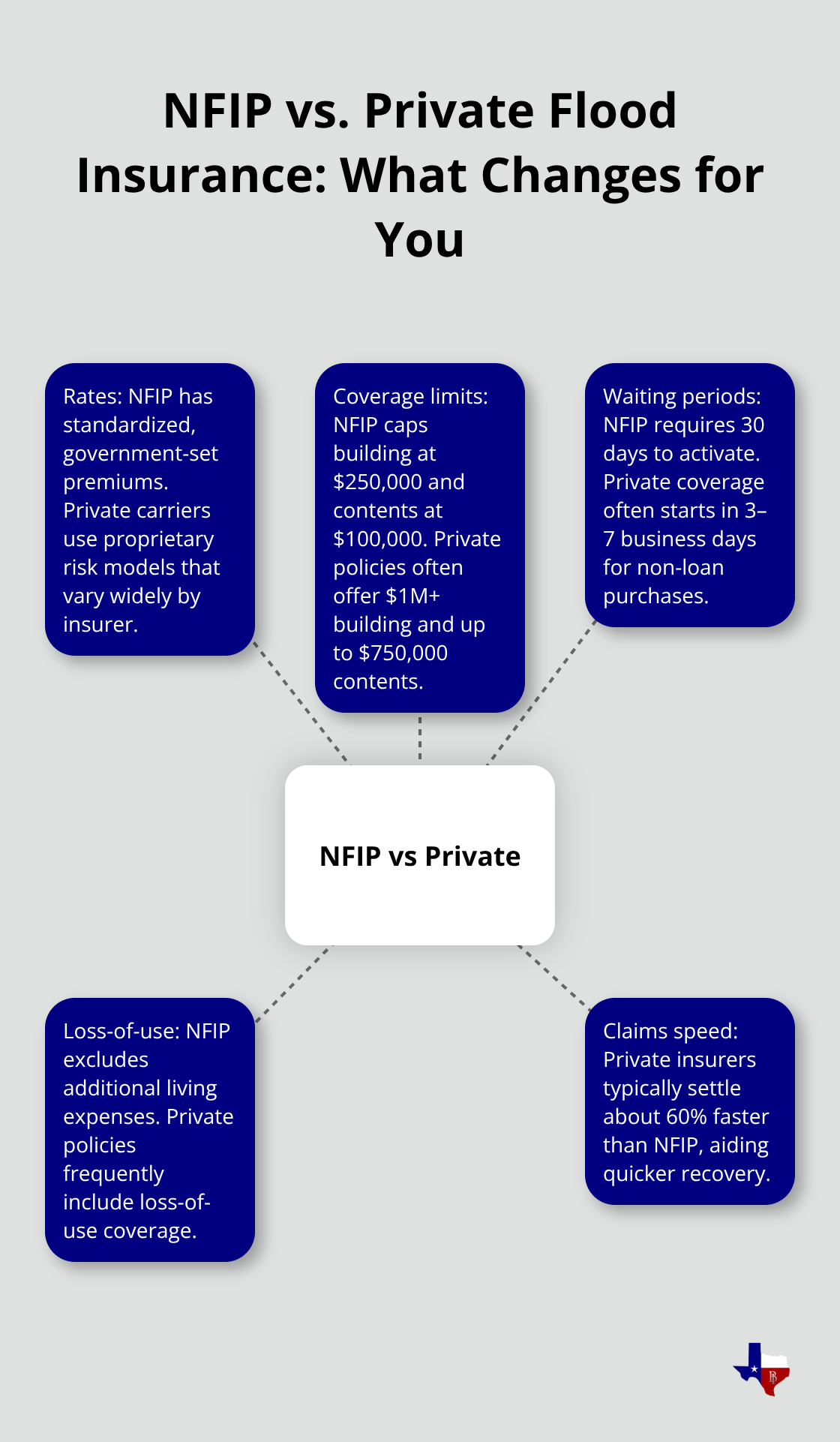

The National Flood Insurance Program operates as the federally backed option that works through thousands of participating agents nationwide. NFIP offers standardized coverage at rates set by the government, which means all insurers charge identical premiums for the same property and risk profile. The program caps dwelling coverage at $250,000 and personal belongings at $100,000, with deductibles ranging from $1,000 to $10,000. According to FEMA data, the average NFIP claim payout between 2016 and 2022 was $66,000, meaning most Texas homeowners receive payouts well within these limits.

However, NFIP policies exclude loss-of-use coverage, additional living expenses, and basement damage in many cases. The 30-day waiting period presents a critical timeline issue: your NFIP policy won’t activate for 30 days after purchase unless your mortgage lender requires immediate coverage for closing. This waiting period means you must start your application months before hurricane season arrives.

Private Flood Insurance: Higher Limits and Faster Claims

Private flood insurance operates with fundamentally different terms and often serves Texas homeowners better. Private insurers typically offer building coverage up to $1 million or higher and contents coverage up to $750,000, with waiting periods as short as three to seven business days for non-loan purchases. Industry data shows private flood claims settle approximately 60 percent faster than NFIP claims, a significant advantage when you’re trying to recover from flood damage.

Private policies commonly include loss-of-use coverage and additional living expenses that NFIP doesn’t provide, and they handle basement flooding more flexibly. The trade-off is that private premiums vary by insurer and risk model, though Texas homeowners typically save 50 to 60 percent on average compared to NFIP rates.

How Your Property Characteristics Shape Premium Costs

Your specific premium depends on replacement cost, elevation, distance to water, and flood loss history. Shopping multiple private quotes against NFIP options reveals your true savings potential for your property. Coverage amount should reflect at least 80 percent of your home’s replacement cost to avoid penalties under the NFIP coinsurance rule, which reduces payouts if you underinsure.

An independent agent can help you obtain quotes from both NFIP and multiple private insurers, because the right choice depends entirely on your home’s characteristics, flood zone designation, and budget constraints. The comparison process takes time but delivers clarity on which option protects your Texas property most effectively.

Comparing NFIP and Private Flood Insurance for Your Texas Home

How NFIP and Private Insurance Differ Fundamentally

NFIP and private flood insurance operate on completely different business models, and your choice determines how much you pay, how quickly you recover after a flood, and what damages actually get covered. NFIP offers federally standardized rates that don’t vary between insurers, meaning a property in Harris County pays the same NFIP premium regardless of which agent you buy from. This uniformity creates predictability but eliminates negotiation on price. Private insurers use proprietary risk models that produce wildly different quotes for the same property.

A home in a moderate-risk area might receive quotes ranging from $400 to $900 annually from different private carriers, making shopping essential.

Coverage Limits and Claims Speed Matter Most

The real advantage of private insurance emerges when you examine coverage limits and claim speed. NFIP caps building coverage at $250,000 and contents at $100,000, while private policies routinely offer $1 million or more in building coverage and up to $750,000 for contents. When a flood destroys your home, these higher limits matter enormously. Private insurers typically settle claims 60 percent faster than NFIP, according to industry data observed after recent hurricanes. NFIP also excludes loss-of-use expenses and additional living costs, meaning you won’t recover hotel bills or temporary housing if you’re displaced. Private policies frequently include these coverages.

Waiting Periods Create Timing Risks

The 30-day waiting period on NFIP policies creates another practical disadvantage. If you purchase NFIP coverage today, you’re not protected until 30 days pass, unless a mortgage lender requires immediate coverage for closing. Private insurers often activate coverage within three to seven business days for non-loan purchases. This timing matters because Texas hurricane season peaks between August and October, and waiting until September to apply for flood insurance guarantees you’ll miss the activation window.

Getting Actual Quotes Reveals Your True Costs

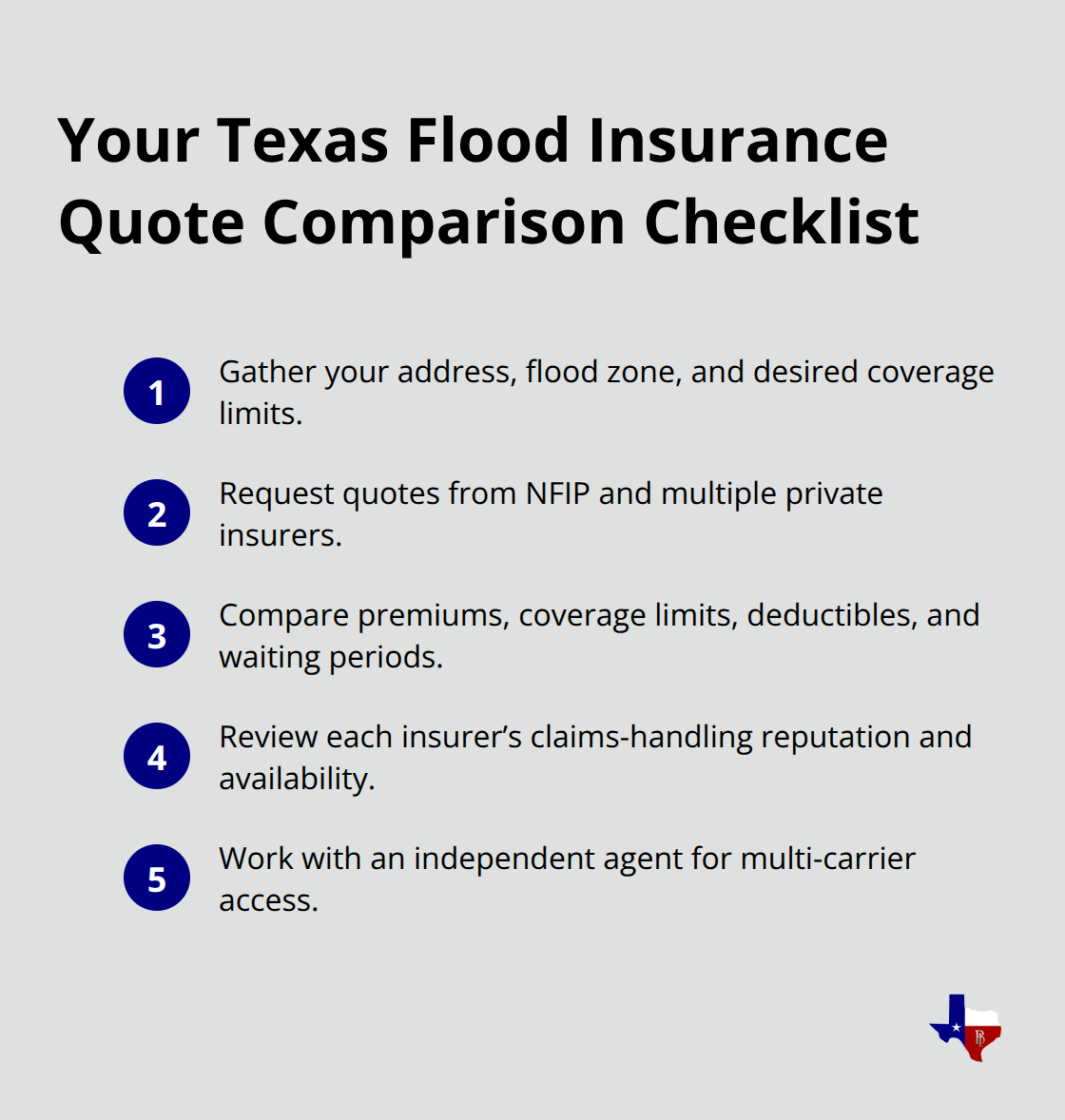

Your best approach involves obtaining quotes from both NFIP and multiple private insurers, then comparing the actual numbers side by side. Request quotes for your specific property address, flood zone designation, and desired coverage limits, then examine the premium differences, coverage limits, deductibles, waiting periods, and claims-handling reputation of each insurer. Some private insurers have pulled out of Texas markets due to high claim frequency after Hurricane Harvey, so availability varies by location and property characteristics. Your elevation, distance from water sources, roof condition, and flood loss history all influence private insurance availability and pricing. An independent agent can access multiple private insurers and NFIP simultaneously, eliminating the need to contact carriers individually. The comparison process takes one or two hours but reveals which option delivers the best protection for your property’s specific situation.

Don’t Assume Which Option Costs Less

For some Texas properties in moderate-risk zones, NFIP actually costs less than private alternatives. For others, private insurance saves thousands annually while providing superior coverage. The only way to know your personal numbers is to obtain actual quotes and compare them directly.

Final Thoughts

Texas flood risk demands action now, not after a storm warning appears. This Texas flood insurance guide has shown you that standard homeowners insurance excludes flood damage entirely, that 40 percent of NFIP claims originate from low- and moderate-risk zones, and that waiting until hurricane season arrives guarantees you’ll miss critical activation windows. The choice between NFIP and private flood insurance depends on your specific property characteristics, flood zone designation, and budget constraints.

Your next step is straightforward: obtain actual quotes from both NFIP and multiple private insurers for your property address and desired coverage limits. Compare the premiums, coverage limits, deductibles, waiting periods, and claims-handling records side by side. Check your flood zone on FEMA’s Flood Map Service Center, then contact an independent agent who can access multiple carriers simultaneously.

We at Brooks Insurance understand that navigating flood insurance options feels overwhelming, which is why our licensed agents stand ready to guide you through every step. Contact Brooks Insurance today to start protecting your Texas home from flood damage before hurricane season arrives.

Disclaimer: The information provided in this blog is for general informational purposes only and does not constitute legal, financial, or insurance advice. Coverage options, terms, and availability may vary. Please consult with a licensed professional for advice specific to your situation