Fleet insurance costs eat into your bottom line, but most business owners don’t realize how many commercial auto insurance discounts they’re leaving on the table. We at Brooks Insurance work with Texas fleets every day and see firsthand how the right strategy can cut premiums significantly.

This guide walks you through the discounts available to you, how to qualify for them, and the practices that keep your rates low year after year.

What Discounts Actually Lower Your Fleet Premiums

Safety Features Reduce Claims and Premiums

Safety features on your vehicles directly reduce insurance rates because they lower claim frequency and severity. Anti-lock braking systems, electronic stability control, collision avoidance technology, and backup cameras all qualify for discounts with most carriers. Vehicles equipped with forward collision warning systems reduce crash risk. If your fleet runs older trucks without these systems, upgrading even a portion of your vehicles can produce measurable premium reductions at renewal.

Telematics Programs Reward Safe Driving Behavior

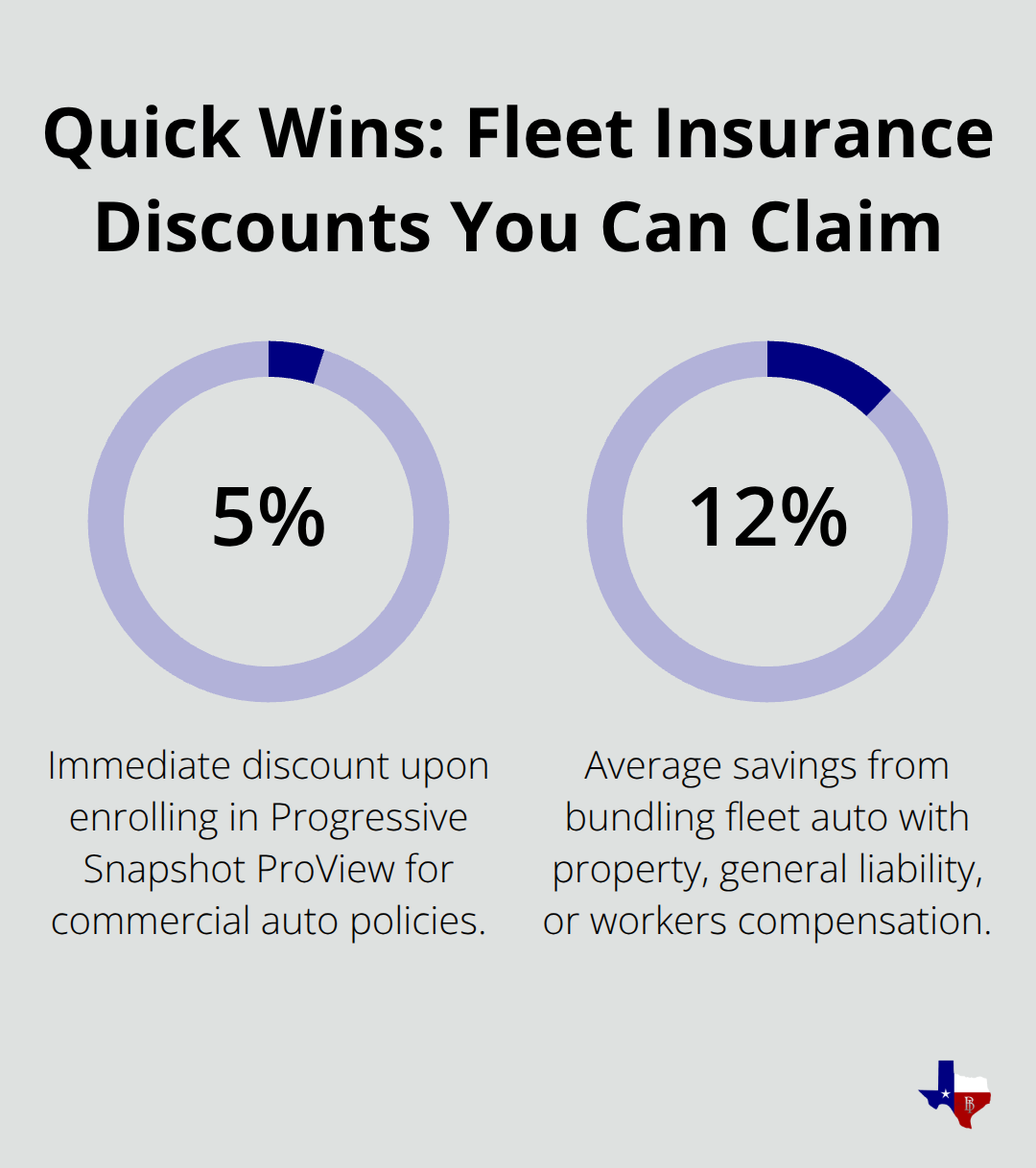

Telematics systems go beyond passive safety features-they actively monitor driver behavior and reward safe driving with ongoing discounts. Progressive’s Snapshot ProView program automatically saves 5% on commercial auto policies upon enrollment and provides fleet management tools for operations with three or more vehicles. The real value emerges when you combine safety equipment with actual driving data, creating a complete picture of risk that insurers reward. This approach transforms your fleet from a static risk profile into a dynamic one that improves as your drivers demonstrate safer habits.

Driver Training Demonstrates Commitment to Safety

Formal driver training and certification programs demonstrate commitment to risk reduction and qualify for substantial discounts. Defensive driving courses, commercial driver’s license CDL training, and hazmat certifications all signal to underwriters that your operation prioritizes safety. More importantly, training directly impacts loss frequency-fleets that invest in annual training programs typically see measurable improvements in their claims history within 12 to 18 months. Continuous coverage for 12 months or longer qualifies you for prior insurance savings with most carriers, but only if you maintain clean records during that period.

Multi-Vehicle Bundles Consolidate Savings

Multi-vehicle bundles work differently than individual discounts-they reward you for consolidating your entire fleet under one policy rather than splitting coverage across multiple carriers or policies. Bundling your fleet auto coverage with property insurance, general liability, or workers compensation can yield average savings around 12% on your auto premiums alone. This consolidation approach simplifies administration while your insurer recognizes the reduced risk that comes from managing your entire operation. The next section shows you exactly how to position your fleet to qualify for these discounts and maximize your savings potential.

Getting Your Fleet Ready for Maximum Discounts

Qualifying for the discounts we mentioned requires more than just asking your agent. It demands intentional fleet management decisions that insurers can verify and measure. Too many fleet operators miss substantial savings because they haven’t implemented the systems that underwriters actually reward. The good news is that most of these steps improve your operation regardless of insurance savings, making them investments in your business rather than expenses.

Start with Telematics Data

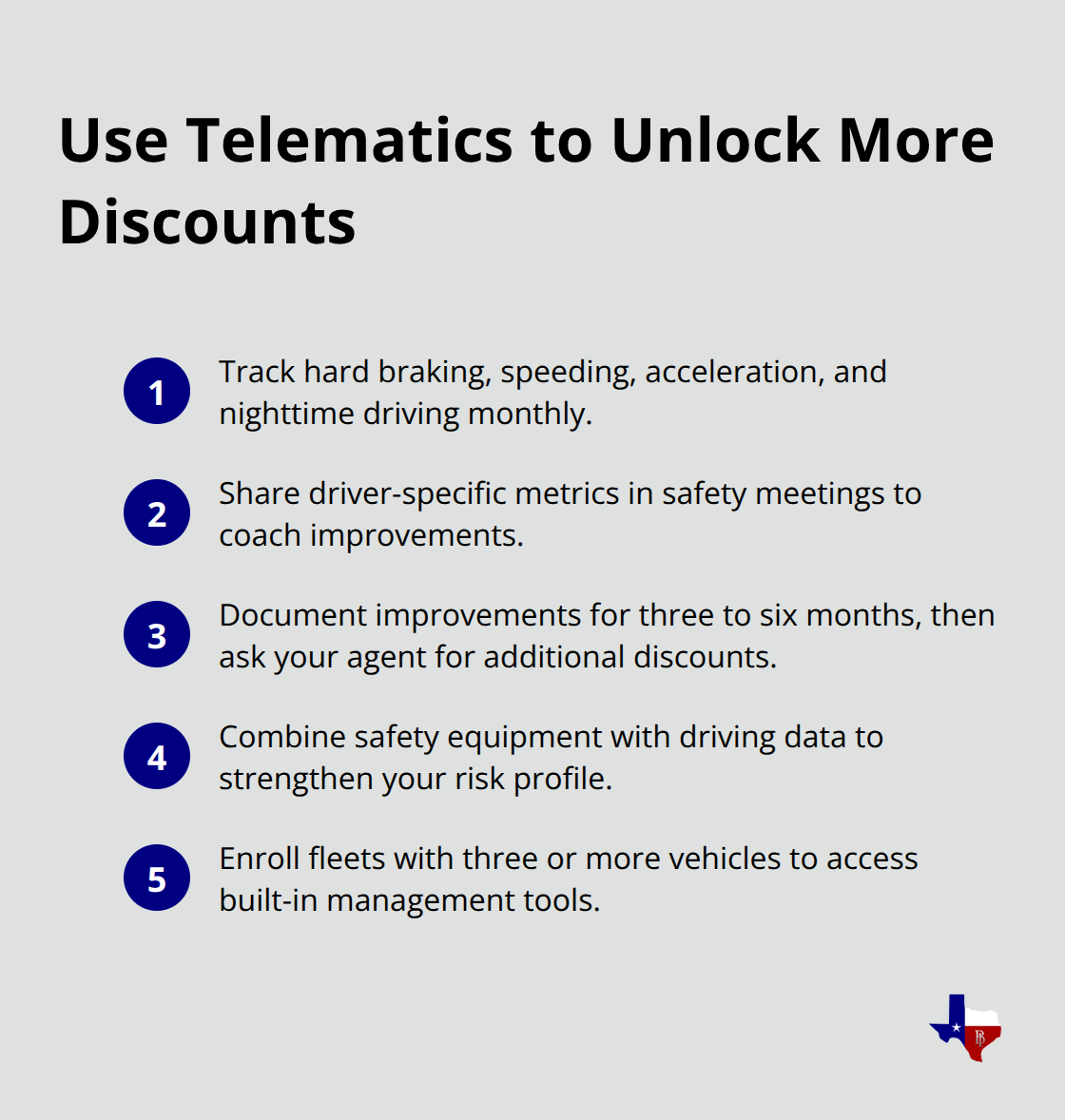

Telematics enrollment delivers immediate discounts while providing fleet management tools at no extra cost for fleets with three or more vehicles. The real advantage emerges when you track which drivers generate the highest-risk behaviors and address them directly. Your telematics data reveals hard braking events, speeding patterns, rapid acceleration, and nighttime driving-the specific behaviors that correlate with claims. Extract this data monthly and share it with your drivers during safety meetings. Drivers who see their own metrics improve focus on behavior change rather than feeling lectured.

After three to six months of consistent safe driving data, contact your agent about additional discounts tied to improved telematics scores. Most carriers offer incremental rate reductions for fleets demonstrating measurable improvement.

Maintain Documented Driving Records

Texas law requires insurers to evaluate driver risk individually, and your fleet’s claims history directly affects renewal rates. Conduct motor vehicle record checks on every driver annually, not just at hire. Many fleet operators run MVRs only when they suspect a problem, missing violations that occurred months earlier. Schedule these checks in January or whenever your policy renews so you have current data during underwriting conversations. Drivers with violations should receive documented retraining within 30 days of discovery. If a driver accumulates three violations in 24 months, seriously consider whether that position is sustainable for your fleet’s insurance costs. One high-risk driver can increase your entire fleet’s premium by thousands annually. Document all training completion, route assignments for high-risk drivers, and any performance improvements. When you renew, provide this documentation to your agent so underwriters see your proactive management approach.

Create a Maintenance Schedule and Keep Records

Vehicle maintenance directly impacts underwriting decisions because poorly maintained fleets generate more claims. Establish a preventive maintenance program with scheduled inspections every 10,000 to 15,000 miles or quarterly, whichever comes first. Document every service, repair, and inspection in a centralized system accessible during policy reviews. Include tire condition, brake pad thickness, fluid levels, light functionality, and safety equipment checks. Fleets with documented maintenance histories receive better rates because underwriters view them as lower risk. When you meet with your agent for renewal, bring your maintenance records. Carriers often adjust rates favorably for fleets demonstrating consistent roadworthiness. Neglected maintenance creates liability exposure that insurers cannot ignore, regardless of other discounts you qualify for.

Align Your Safety Culture with Underwriter Expectations

Underwriters reward fleets that demonstrate a genuine commitment to safety through measurable actions, not just policy statements. Your telematics data, maintenance records, and driver training documentation work together to create a complete safety profile. Carriers view fleets that actively monitor and improve driver behavior as fundamentally lower risk than those that treat safety as a checkbox exercise. The combination of these three elements-telematics monitoring, documented driving records, and preventive maintenance-positions your fleet to access the deepest discounts available in the Texas market. Your next step involves translating this preparation into actual conversations with your insurance agent about which specific discounts apply to your operation and how to implement them effectively.

Building a Documentation System That Carriers Actually Reward

The gap between fleets that qualify for maximum discounts and those that leave money on the table comes down to one thing: proof. Insurers cannot reward behavior they cannot verify, and most fleet operators maintain safety investments without the documentation that underwriters need to justify rate reductions. The fleets receiving the best rates share a common trait-they maintain organized, accessible records that demonstrate consistent safety practices. Creating this documentation system takes effort upfront, but it transforms your fleet from an unknown risk into a measurable, verifiable one that carriers compete to insure at lower rates.

Establish a Centralized Documentation Platform

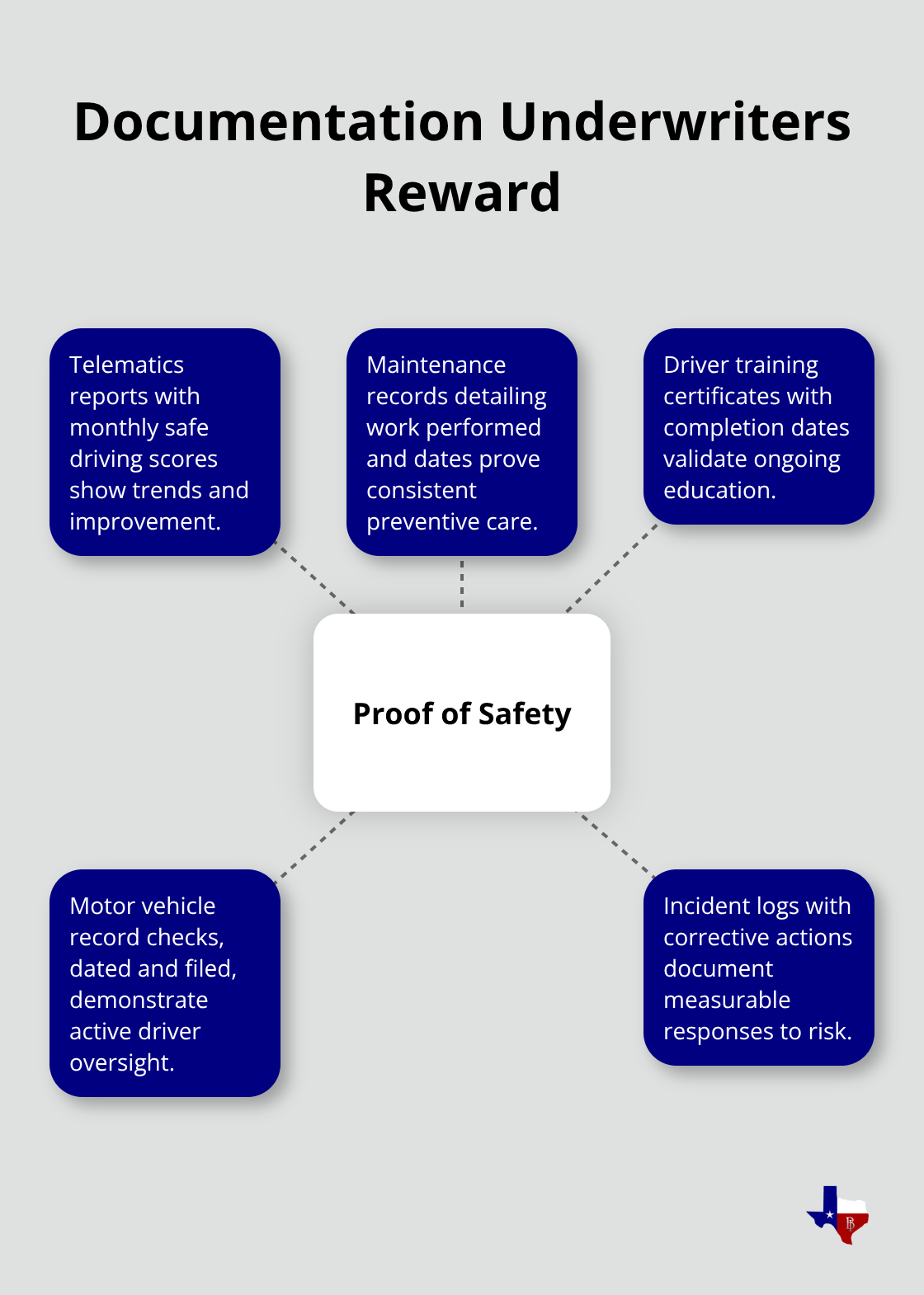

Create a centralized system where every safety-related activity gets recorded with dates and driver or vehicle identification. This includes telematics reports showing monthly safe driving scores, maintenance records with specific work performed and dates completed, driver training certificates with completion dates, motor vehicle record checks dated and filed, and any safety incidents with documented corrective actions taken. When your policy renews, extract the previous 12 months of this documentation and present it to your agent before underwriting conversations begin.

Carriers use this information to justify rate adjustments at renewal, and fleets providing comprehensive documentation receive better outcomes than those who provide nothing.

Schedule Annual Safety Reviews with Your Agent

Schedule a formal annual review meeting with your agent specifically to discuss how your safety investments should translate into premium reductions. Many fleet operators meet with their agent only when renewing, missing opportunities to discuss mid-year adjustments or additional discounts that became available. During this meeting, walk through your telematics improvement trends, highlight maintenance records showing consistent preventive care, and discuss any training programs completed. Ask your agent explicitly which specific discounts you qualify for based on this documentation, and request written confirmation of which carriers offer rate credits for each activity. This creates accountability and prevents vague promises about discounts that never materialize.

Monitor Claims and Loss History Quarterly

Monitor your claims and loss history quarterly rather than waiting until renewal. Request a loss run report from your current carrier every three months and analyze which vehicles or drivers generate the most claims. A loss run shows claim frequency, severity, and types of incidents, revealing patterns that your safety program should address. If one vehicle consistently shows collision claims, consider whether that route or driver assignment needs adjustment. If one driver appears on multiple claims, that individual represents an immediate threat to your fleet’s rates.

Respond to Claims Data with Measurable Action

Document the corrective actions you take in response to claims data-reassignment, additional training, route changes, or vehicle retirement-and share these with your agent. Carriers view fleets that respond to claims data with measurable action as serious about risk reduction, and this proactive approach often results in rate adjustments that offset the cost of addressing the underlying problem.

Final Thoughts

The path to lower fleet insurance costs starts with understanding what carriers actually reward. Safety features, telematics enrollment, driver training, and multi-vehicle bundles represent real opportunities to reduce your premiums, but only if you implement them strategically and document your efforts. Most Texas fleet operators leave thousands of dollars on the table annually because they treat safety as a compliance requirement rather than an insurance strategy.

Your competitive advantage comes from building a documented safety culture that underwriters can verify and measure. Telematics data showing improved driver behavior, maintenance records proving consistent vehicle care, and training documentation demonstrating commitment to risk reduction work together to create a compelling case for commercial auto insurance discounts at renewal. Carriers compete aggressively for fleets that present this level of organization and accountability.

Start by implementing telematics if you haven’t already, then establish a centralized documentation system for maintenance, training, and driver records. Contact Brooks Insurance today for a fleet quote and let our licensed agents show you exactly how much you can save with the right commercial auto insurance discount strategy.

Disclaimer: The information provided in this blog is for general informational purposes only and does not constitute legal, financial, or insurance advice. Coverage options, terms, and availability may vary. Please consult with a licensed professional for advice specific to your situation