Running a fleet in Texas means managing real risks on real roads. Commercial auto insurance in Texas isn’t optional-it’s a legal requirement that protects your business, your employees, and your bottom line.

At Brooks Insurance, we help Texas business owners find policies that match their actual fleet needs. The right coverage can mean the difference between a manageable claim and a business-threatening loss.

Why Texas Requires Commercial Auto Insurance

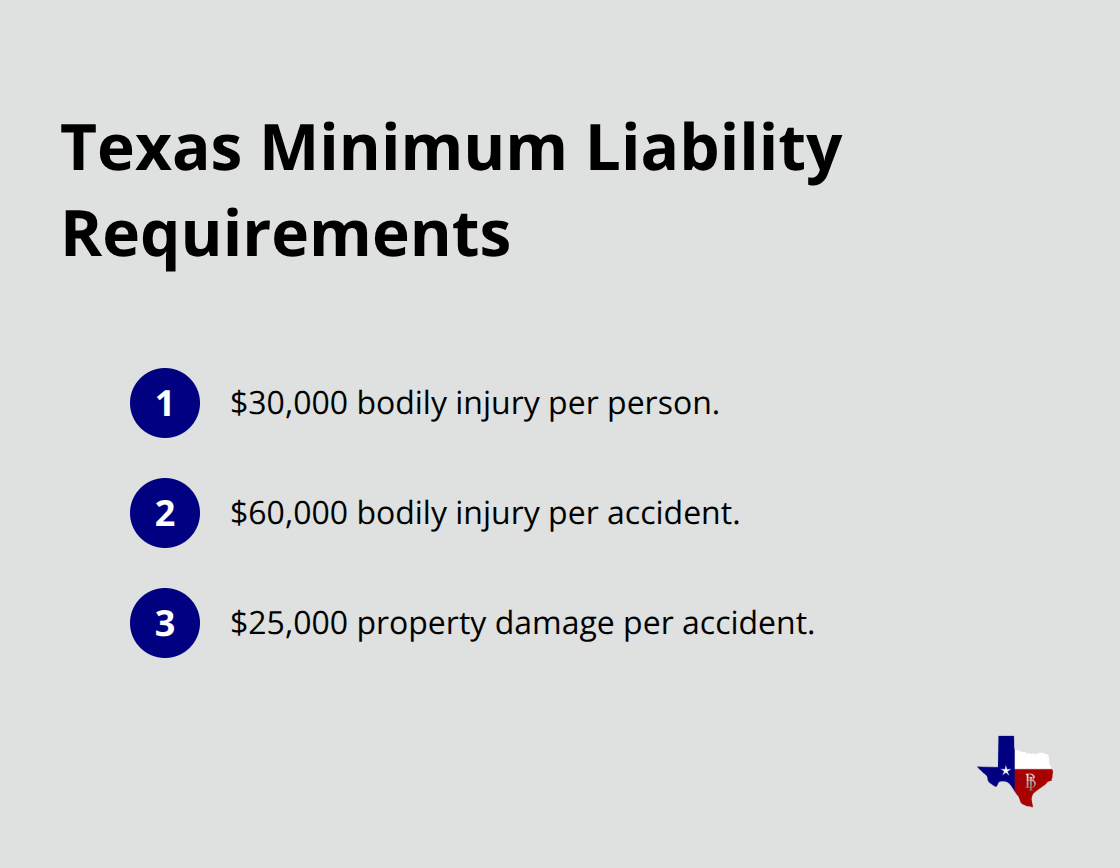

Texas law mandates commercial auto insurance for any vehicle used in business operations, and the state’s minimum liability requirements reflect serious exposure. You need at least $30,000 per person and $60,000 per accident for bodily injury, plus $25,000 for property damage per accident, according to the Texas Transportation Code. These minimums exist because accidents happen regularly on Texas roads, and without insurance, a single collision can wipe out a small business.

First-time violations for driving without commercial auto insurance in Texas carry fines up to $350, with repeat offenses reaching $1,000 and potential license suspension. The financial penalty is just the surface problem-an uninsured accident leaves your business liable for all damages out of pocket, which typically far exceeds what most businesses can absorb.

Many Texas business owners operate with only minimum coverage, thinking it protects them adequately. The reality is different. If your driver causes a serious injury accident, $60,000 in bodily injury coverage disappears in minutes once medical bills, lost wages, and legal fees accumulate. Businesses that operate multiple vehicles face significantly higher exposure and need coverage limits well above state minimums to protect their assets.

The Real Cost of an Accident Without Proper Coverage

An accident involving your fleet vehicle creates immediate financial pressure and legal liability. Your business pays for medical expenses, vehicle repairs, lost income for injured parties, and potential legal judgments. Texas is an at-fault state, meaning the driver deemed responsible has their liability insurance cover damages. If your coverage limits fall short, your business pays the difference from operating funds.

Consider a delivery vehicle hitting another car and injuring two people. Medical treatment, rehabilitation, and lost wages easily reach $200,000 or more. With minimum coverage, you owe $140,000 from business funds. That single accident drains resources meant for payroll, equipment, and growth.

Protecting Your Employees and Third Parties

Your employees need protection when they drive company vehicles. If an employee sustains injury while driving a company vehicle, they deserve medical coverage and wage replacement. Texas commercial auto policies typically include Personal Injury Protection (PIP) for medical payments after an accident, though you can waive it. Waiving PIP creates unnecessary risk-the cost savings are minimal compared to the exposure of leaving employees without immediate medical coverage.

Third-party protection matters equally. A pedestrian or cyclist hit by your vehicle can pursue substantial damages. Uninsured motorist coverage protects your business when the at-fault driver carries no insurance at all. Underinsured motorist coverage applies when the other driver’s coverage limits cannot cover all damages. These coverages prevent your business from absorbing losses caused by other drivers’ negligence or insufficient insurance.

Moving Beyond Minimum Coverage

State minimums provide a legal floor, not a business protection strategy. A serious accident involving multiple vehicles or severe injuries quickly exhausts $60,000 in bodily injury limits. Your business assets, equipment, and future revenue face exposure when coverage falls short. Many Texas fleets benefit from higher liability limits that match their actual risk profile and asset value. The next section explores the specific coverage options available to you and how each one protects different aspects of your fleet operations.

Coverage Options That Protect Your Fleet

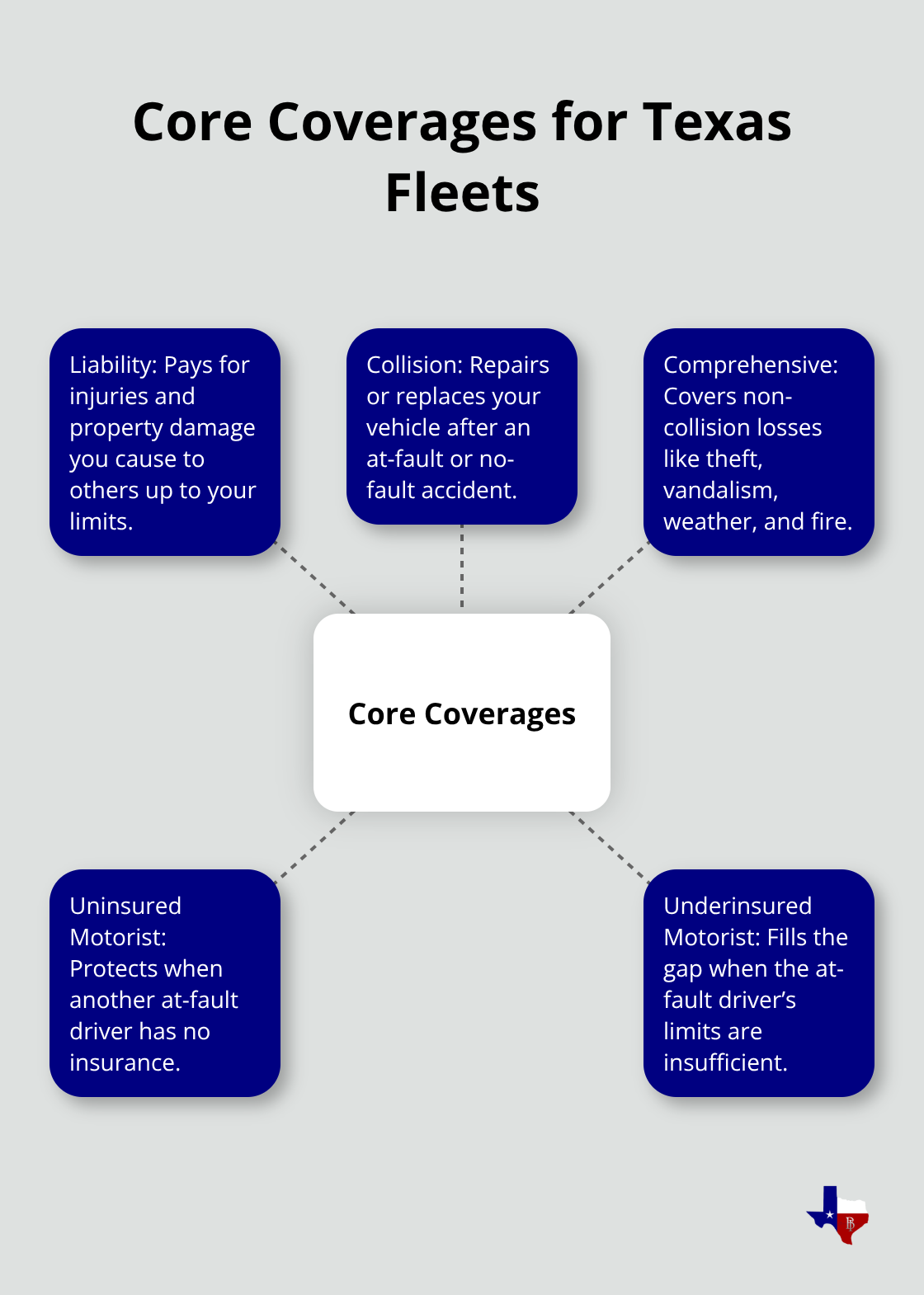

Liability coverage forms the backbone of commercial auto insurance, and Texas law requires it for good reason. Your liability policy pays for injuries and property damage your vehicle causes to others, up to your chosen limits. The state minimum of Texas minimum liability coverage limits is $30,000 per person and $60,000 per accident. A single serious injury involving surgery, physical therapy, and lost wages reaches $100,000 to $300,000 in damages within months.

If your policy maxes out at $60,000, your business absorbs the remaining $40,000 to $240,000.

Bodily Injury and Property Damage Liability

Texas fleets benefit from carrying bodily injury limits of at least $100,000 per person and $300,000 per accident. This higher threshold aligns with typical severe injury costs and protects your business assets from judgment exposure. Property damage liability covers vehicle repairs and other property harm your fleet causes. The $25,000 minimum disappears quickly with modern vehicle repair costs. A collision involving two vehicles with resulting repairs, rental cars, and business interruption easily exceeds $25,000. Increasing property damage limits to $50,000 or $100,000 adds minimal premium cost but eliminates a significant gap.

Collision and Comprehensive Protection

Collision coverage repairs or replaces your vehicle after an accident regardless of who caused it. This coverage matters because liability only covers damage to the other party’s property, not your own vehicle. A delivery truck involved in a collision with another car needs collision coverage to repair the truck itself. Without it, your business pays thousands from operating funds while the vehicle sits in a shop.

Comprehensive coverage protects against non-collision losses like theft, vandalism, weather damage, and fire. Texas fleets operating in urban areas face higher theft risk, making comprehensive coverage practical rather than optional. Together, collision and comprehensive coverage (often called “full coverage”) keeps your vehicles operational and your business running smoothly.

Uninsured and Underinsured Motorist Coverage

Uninsured motorist coverage handles situations where another driver causes an accident but carries no insurance. Texas has approximately 12 to 15 percent uninsured drivers on the road, according to industry data. When an uninsured driver hits your vehicle and injures your employee, uninsured motorist coverage pays medical bills and damages your liability policy won’t cover.

Underinsured motorist coverage applies when the at-fault driver’s insurance proves insufficient for actual damages. A serious multi-vehicle accident can generate $500,000 in total damages while the responsible driver carries only $60,000 in coverage. Your underinsured motorist policy fills that $440,000 gap, protecting your employee’s recovery rights and your business from absorbing the shortfall. These protections work together to shield your fleet from the financial impact of other drivers’ negligence or inadequate coverage.

The specific combination of coverages your fleet needs depends on your vehicle types, operational patterns, and risk exposure. Understanding what each coverage option protects helps you make informed decisions about your policy structure and limits.

How to Choose the Right Commercial Auto Policy for Your Texas Fleet

Assess Your Fleet Size and Vehicle Types

Start with your fleet inventory to identify the difference between adequate coverage and expensive gaps. List every vehicle your business operates, including owned trucks, leased equipment, and employee-owned vehicles used for work. Note each vehicle’s value, age, and primary use. A delivery van worth $35,000 requires different coverage than a $150,000 refrigerated truck. Document whether vehicles carry cargo, equipment, or hazardous materials, as these factors directly impact premium calculations and necessary coverage limits. Texas commercial auto insurance costs vary based on your detailed vehicle profile. Once you know exactly what you’re insuring, you can evaluate coverage needs realistically rather than guessing at minimums that leave you exposed.

Evaluate Your Annual Mileage and Routes

Your annual mileage and operational patterns shape your risk profile more than most business owners realize. A service company with three vehicles traveling 500 miles weekly within a metro area faces different exposure than a delivery fleet covering 2,000 miles daily across rural Texas highways. Document your typical routes, peak traffic periods, and whether drivers operate during high-risk hours like early morning or late night. Vehicles operating in congested urban areas like Houston and Dallas experience higher accident rates than those in less dense regions. Route complexity and mileage directly correlate with claim frequency. Share this operational information with potential insurers because it allows them to price your policy accurately rather than applying generic rates that may overcharge or undercharge your actual risk. This transparency also prevents coverage surprises later when claims reveal operational details your policy wasn’t designed to handle.

Compare Quotes from Multiple Insurers

Contact State Farm, Progressive, and Travelers directly or work with an independent agent representing multiple carriers. Progressive offers usage-based telematics through Smart Haul that tracks actual driving behavior and can reduce premiums substantially for safer fleets. Travelers emphasizes risk-management resources and online tools that help prevent accidents before they happen. Each carrier structures coverage options differently, so identical liability limits may carry different premiums and deductibles. Request quotes with identical coverage limits and deductibles across all carriers so you’re comparing actual pricing, not just numbers on different policy structures. A certificate of insurance typically issues within 24 hours after you select coverage, allowing you to activate protection quickly once you’ve made your decision.

Understand What Drives Your Premium

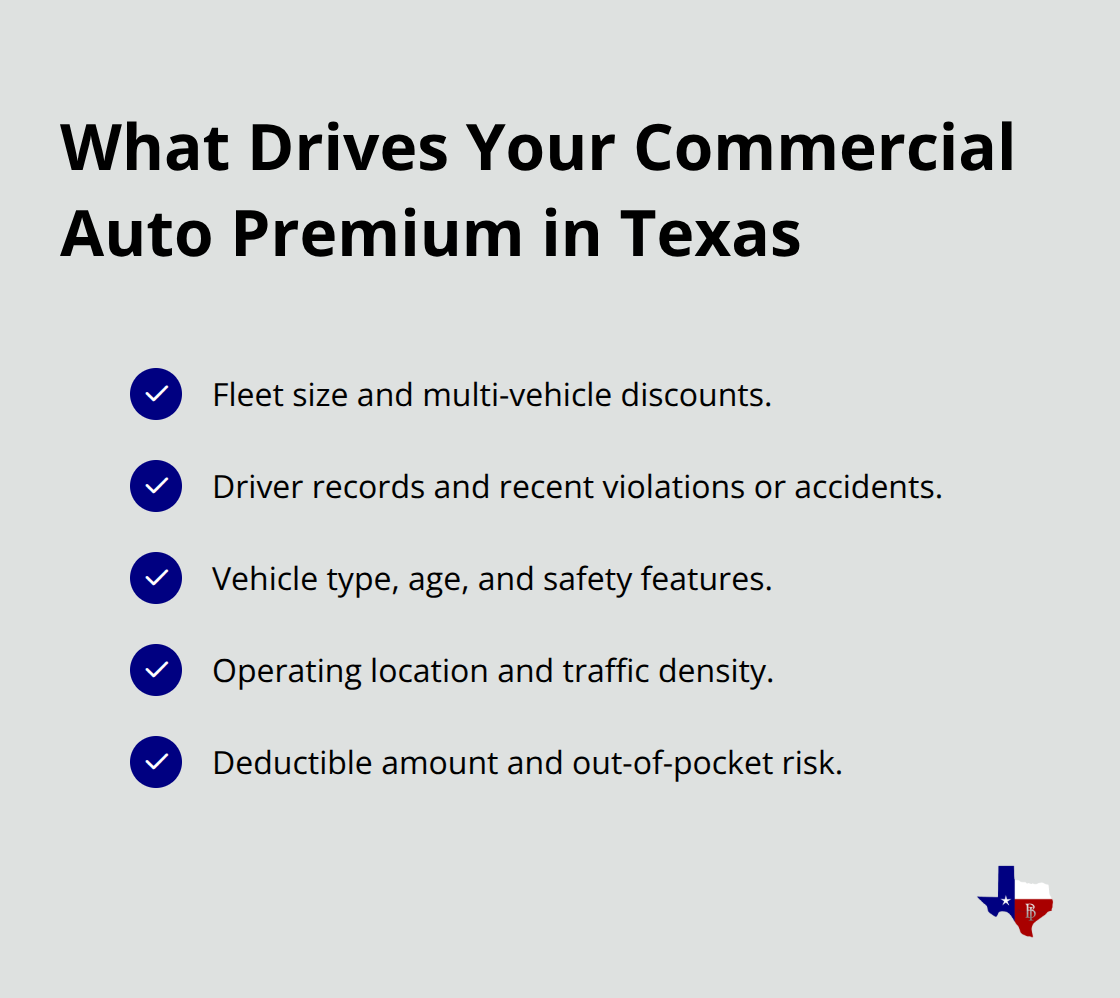

Fleet size matters significantly because insurers apply volume discounts to multi-vehicle policies. A business adding a fourth vehicle to an existing policy pays less per vehicle than the first vehicle because the insurer spreads administrative costs across more units. Driver records create the largest premium variation because serious violations and accidents indicate higher future claim risk. A driver with two accidents in three years increases your fleet premium by 15 to 25 percent compared to a clean driving record.

Vehicle type and age affect rates because newer vehicles often cost less to repair and may include safety features that reduce accident severity. Location influences premiums substantially because urban fleets in high-density areas pay more than rural operations due to higher accident frequency. Your deductible choice directly affects your monthly premium, with higher deductibles reducing cost but increasing your out-of-pocket exposure when claims occur. Most Texas fleets benefit from $1,000 deductibles that balance affordable premiums against manageable claim costs.

Final Thoughts

Protecting your Texas fleet requires matching your coverage to your actual operational risk, not settling for legal minimums that leave your business exposed. The decisions you make about liability limits, collision protection, and uninsured motorist coverage directly determine whether an accident becomes a manageable claim or a business-threatening loss. Your fleet size, vehicle types, annual mileage, and driver records all factor into the right policy structure for your situation.

Commercial auto insurance in Texas works best when you assess what you operate and how you operate it honestly. Gather details about every vehicle, document your typical routes and mileage patterns, and share your actual risk profile with insurers so they can quote you accurately. Request quotes from multiple carriers with identical coverage limits so you can compare real pricing differences rather than policy structure variations.

We at Brooks Insurance help Texas business owners find practical coverage solutions that protect their operations without unnecessary complexity. Our licensed agents work directly with you to understand your fleet’s specific needs and find policies that match your risk profile. Contact us today to discuss your commercial auto insurance needs and get quotes tailored to your Texas fleet.

Disclaimer: The information provided in this blog is for general informational purposes only and does not constitute legal, financial, or insurance advice. Coverage options, terms, and availability may vary. Please consult with a licensed professional for advice specific to your situation