![Best Flood Insurance Companies [Reviews]](https://brooksinstx.com/wp-content/uploads/tosten/Best-Flood-Insurance-Companies-_Reviews__1767654719-1080x675.jpeg)

Flooding causes more property damage than any other natural disaster in Texas, with homeowners filing over 20,000 flood claims annually in our state. Standard homeowners insurance won’t cover flood damage, which is why finding the right flood insurance company matters so much.

At Brooks Insurance, we help Texas residents navigate flood coverage options and connect with providers that match their specific needs. This guide walks you through the best flood insurance companies, what to evaluate, and how to choose protection that actually fits your situation.

Top Flood Insurance Providers in Texas

Major National Carriers

Wright Flood stands out as the largest flood insurance company in the U.S., with nearly 40 years specializing in flood coverage. The company holds an A rating from A.M. Best and operates federal flood policies through FEMA while also offering private flood insurance through its Flood Insurance Marketplace. Wright’s private options deliver higher limits than the standard NFIP cap of $250,000 for dwelling coverage, with some policies reaching up to $5 million. The company expanded FocusFlood into 21 states in November 2025, giving more Texas residents access to customized coverage. Wright maintains a dedicated Flood Claims Team that processes claims rapidly, which matters when you’re dealing with water damage and need decisions made quickly.

Progressive Flood provides another major national option through various distribution channels and integrates flood coverage into broader homeowners policies for simplicity. Neptune Flood focuses on higher-value properties and includes basement contents coverage plus pool protection, covering dwelling amounts up to $4 million. Aon Edge through Goosehead advertises rates roughly 40 percent below NFIP premiums according to CNBC Select, though availability varies by state.

NFIP Direct and Private Options

NFIP Direct remains the baseline option available in all participating communities nationwide, capping dwelling coverage at $250,000 for residential buildings. Each carrier differs significantly on what they cover-basements, pools, personal belongings, and temporary living expenses during relocation-so comparing specific inclusions matters more than comparing names.

Selecting Between NFIP and Private Coverage

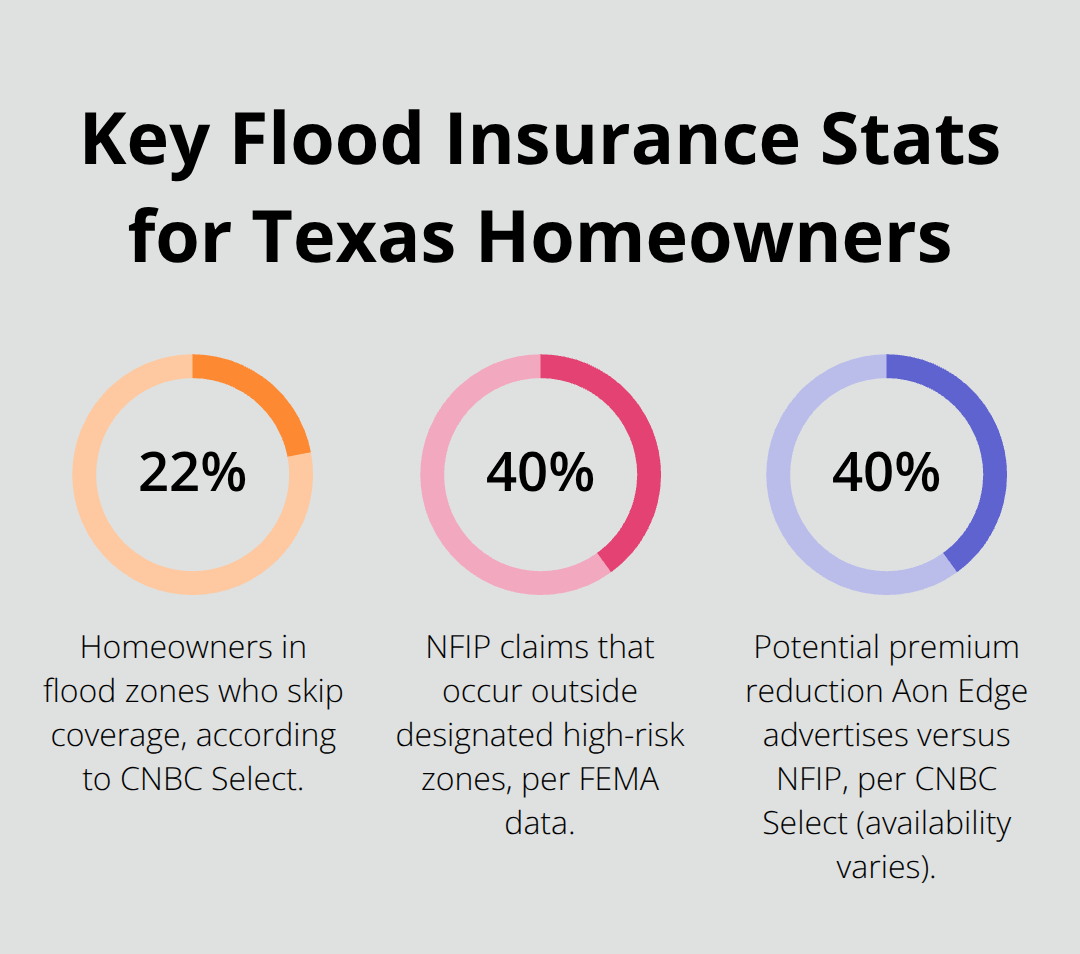

The choice between NFIP and private flood insurance hinges on your property value and coverage needs. If your home is worth significantly more than $250,000 or you have valuable items in your basement or pool area, private options typically make financial sense despite higher premiums. About 22 percent of homeowners in flood zones skip coverage entirely, according to CNBC Select, leaving themselves exposed. Waiting periods vary too-most impose 7 to 10 days before coverage activates, though some providers waive this during closing periods.

Getting Accurate Quotes

Try obtaining quotes from at least three different carriers because pricing depends heavily on your specific location, property construction, number of floors, and chosen deductible. Use FEMA’s flood zone mapping tool to identify your baseline risk tier, then request personalized quotes that reflect your actual property details rather than making assumptions based on price alone. Your next step involves assessing your specific property risk and location to narrow down which coverage options actually apply to your situation.

What to Look for in a Flood Insurance Company

Financial Strength and Ratings

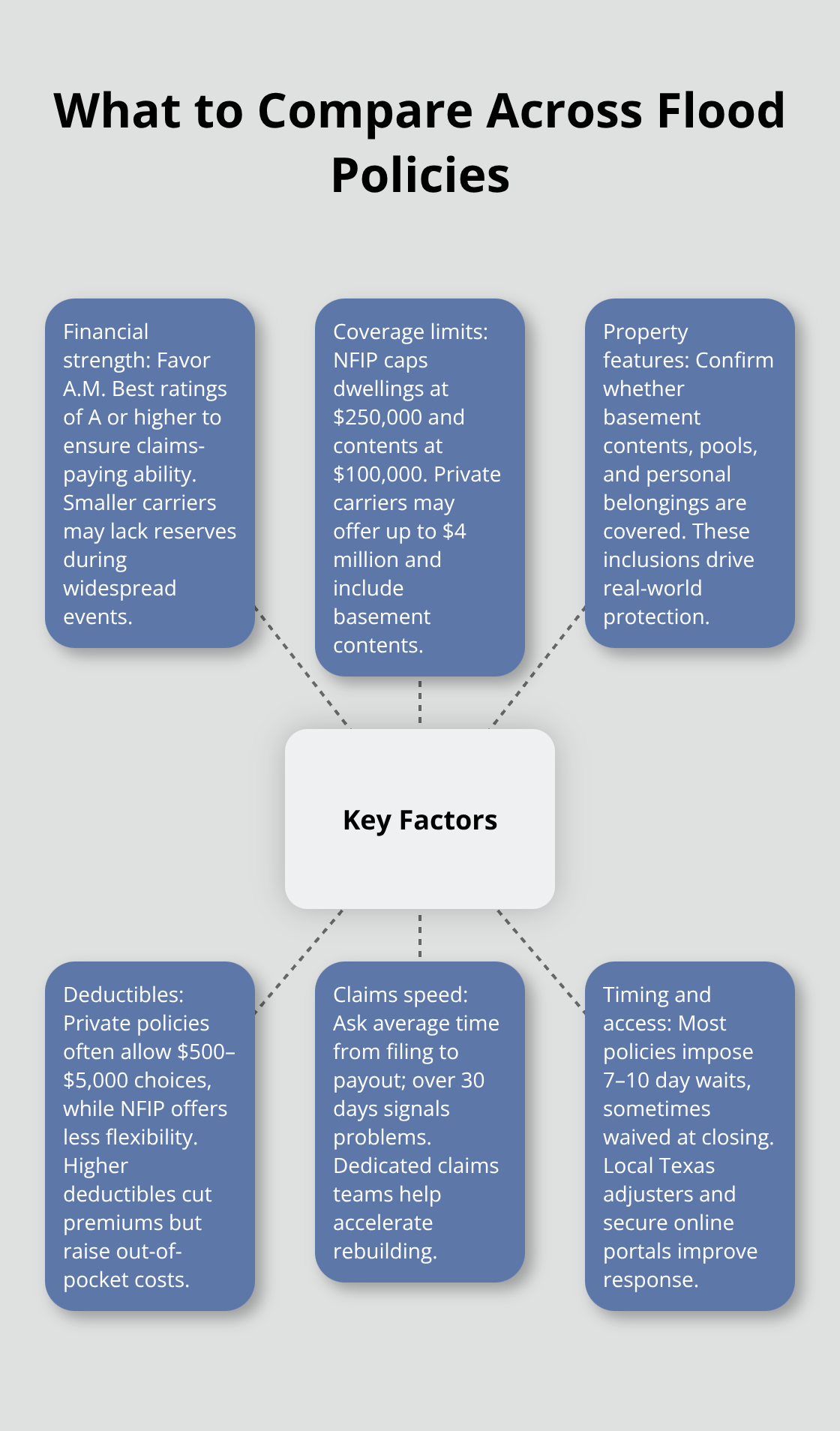

A flood insurance company’s financial strength directly impacts whether claims get paid when disaster strikes. Wright Flood holds an A rating from A.M. Best, which signals solid financial stability and the ability to cover large claims without delay. This rating matters because some smaller carriers lack the reserves to handle major flood events across their entire customer base. Check A.M. Best ratings on the company website or call their customer service line-anything below an A grade should raise concerns about whether they’ll be there when you need them most.

Coverage Limits and What’s Actually Protected

The differences between carriers are substantial and directly affect your protection. NFIP caps dwelling coverage at $250,000 and contents at $100,000, but private carriers like Neptune Flood offer up to $4 million in dwelling coverage and include basement contents protection that federal policies typically exclude. If your home sits in a basement-prone area or you have a pool, that coverage gap between NFIP and private options becomes critical. Deductible choices matter equally-private flood policies often let you select between $500 and $5,000 deductibles, while NFIP offers less flexibility.

Higher deductibles lower your monthly premium but increase out-of-pocket costs after a flood, so calculate what you can actually afford to pay before choosing the cheapest option.

Claims Processing Speed and Local Support

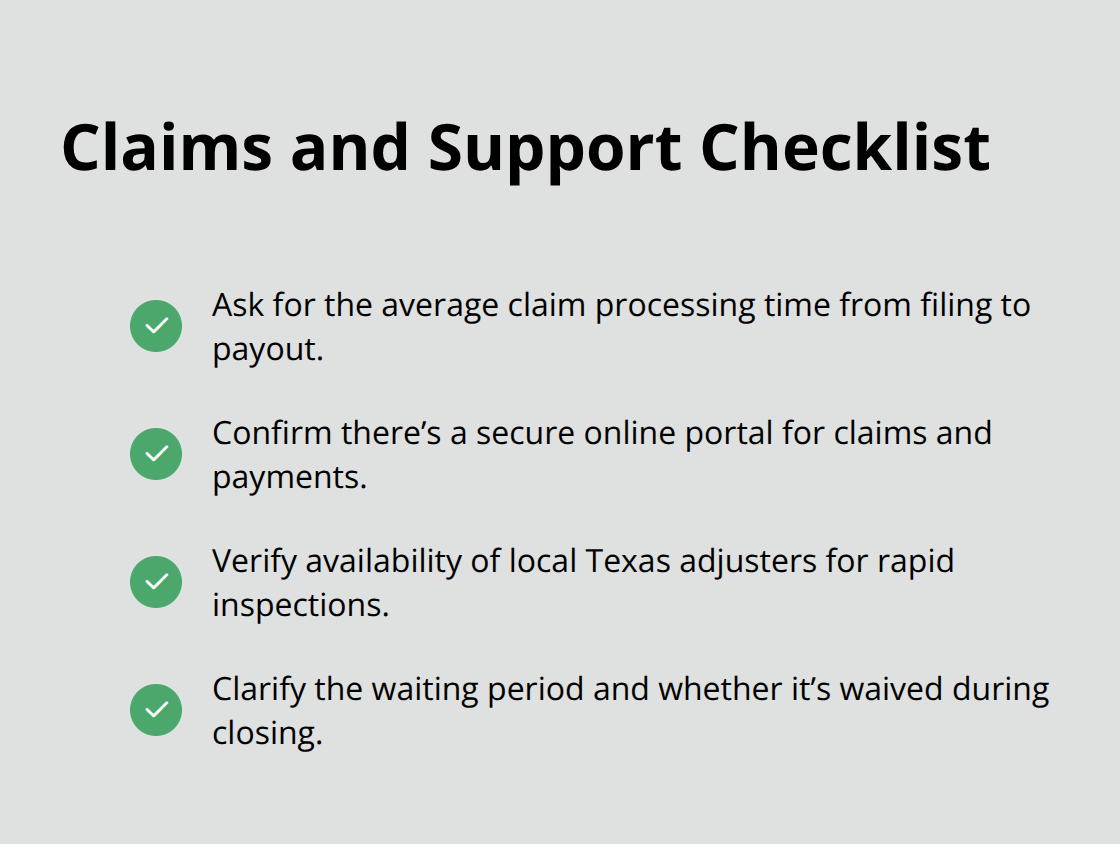

Local expertise and responsive support separate competent insurers from mediocre ones when water damage happens. Wright Flood operates a dedicated Flood Claims Team that processes claims rapidly, which accelerates the rebuilding timeline when every day counts. Call potential providers and ask how long their average claim takes from filing to payout; anything exceeding 30 days suggests staffing or process problems. Ask whether they have local adjusters in Texas who can inspect damage quickly rather than sending someone from another state.

Some carriers impose 7 to 10-day waiting periods before coverage activates, but others waive this during closing periods, so clarify these terms before purchasing. Verify that the company provides a secure portal for managing payments and claims online-this matters when you’re stressed about water damage and need quick access to your policy details. Understanding these operational details helps you identify which carriers will actually support you during the recovery process, not just collect premiums during calm years.

Choosing the Right Flood Coverage for Your Texas Property

Know Your Actual Flood Risk

Start with your actual flood risk rather than assuming your location is safe. Roughly 40 percent of NFIP flood insurance claims occur in areas not designated as high-risk zones, according to FEMA data, which means living outside an official flood zone provides false security. Use FEMA’s flood zone mapping tool to identify your baseline risk tier, then check the Historical Claims Map to see what flooding has actually occurred in your specific neighborhood. This data matters more than your gut feeling about whether water reaches your property.

Assess Your Home Value and Property Features

Once you know your risk level, assess whether your home value exceeds the NFIP dwelling limit of $250,000. If it does, private flood insurance becomes essential rather than optional. Properties with basements, pools, or expensive personal belongings stored below ground need private coverage because NFIP excludes these items. Contact at least three different carriers and request quotes based on your actual property details-construction type, number of floors, elevation, and chosen deductible all dramatically affect pricing. Aon Edge advertises rates roughly 40 percent below NFIP according to CNBC Select, but availability varies by state, so comparing your specific options beats chasing national averages.

Compare Coverage Details Across Carriers

When reviewing policy terms, focus on what each carrier actually covers rather than premium price alone. Read whether basement contents, pool damage, personal belongings, and temporary living expenses are included, because these differences determine whether you’re truly protected or just paying for a policy that leaves gaps. Most flood policies impose 7 to 10-day waiting periods before coverage activates, though some providers waive this during closing periods, so clarify timing before purchasing.

Evaluate Deductibles and Out-of-Pocket Costs

Examine deductible options carefully-NFIP offers less flexibility than private carriers, which often provide $500 to $5,000 choices. Calculate what you can realistically pay out-of-pocket after a flood event rather than automatically selecting the lowest deductible. This calculation prevents financial strain when you’re already dealing with water damage and recovery costs.

Verify Claims Processing and Local Support

Call each carrier’s customer service line and ask about average claim processing time; anything exceeding 30 days suggests operational problems. Verify they operate a secure online portal for claims filing and policy management, because you’ll need quick access during the chaos following water damage. Ask whether they employ local Texas adjusters who can inspect damage rapidly or if they send adjusters from distant states.

These operational details separate carriers that genuinely support recovery from those that simply collect premiums.

Final Thoughts

Selecting the best flood insurance companies for your Texas property requires evaluating financial strength, coverage limits, claims processing speed, and local support rather than chasing the lowest premium. Wright Flood delivers rapid claims processing and higher limits through private options, NFIP provides baseline federal coverage in all participating communities, and private carriers like Neptune Flood and Aon Edge offer customization for specific property needs. Your decision ultimately depends on your home value, property features such as basements or pools, and how quickly you need claims resolved after water damage occurs.

Working with an independent agent makes this comparison process significantly easier. We at Brooks Insurance represent multiple top-rated insurance companies, which means you have access to a larger selection of coverage options, pricing, and payment plans than you would find working directly with a single carrier. Our licensed agents understand Texas flood risks and can match you with carriers that actually fit your situation rather than pushing generic solutions.

Contact Brooks Insurance to discuss your specific property risk and receive personalized quotes from multiple carriers. Bring details about your home value, construction type, basement features, and any pools or valuable items stored below ground. Most flood policies impose 7 to 10-day waiting periods before coverage activates, so purchasing protection before storm season arrives matters far more than waiting until rain appears in the forecast.