Your business vehicles are on the road every day, and they need protection that goes beyond standard auto insurance. Commercial auto insurance for small businesses covers the unique risks you face-from liability claims to collision damage-and it’s fundamentally different from personal car coverage.

At Brooks Insurance, we help Texas small business owners understand what they actually need to protect their fleet. The right policy can save you thousands in unexpected costs and keep your business running smoothly when accidents happen.

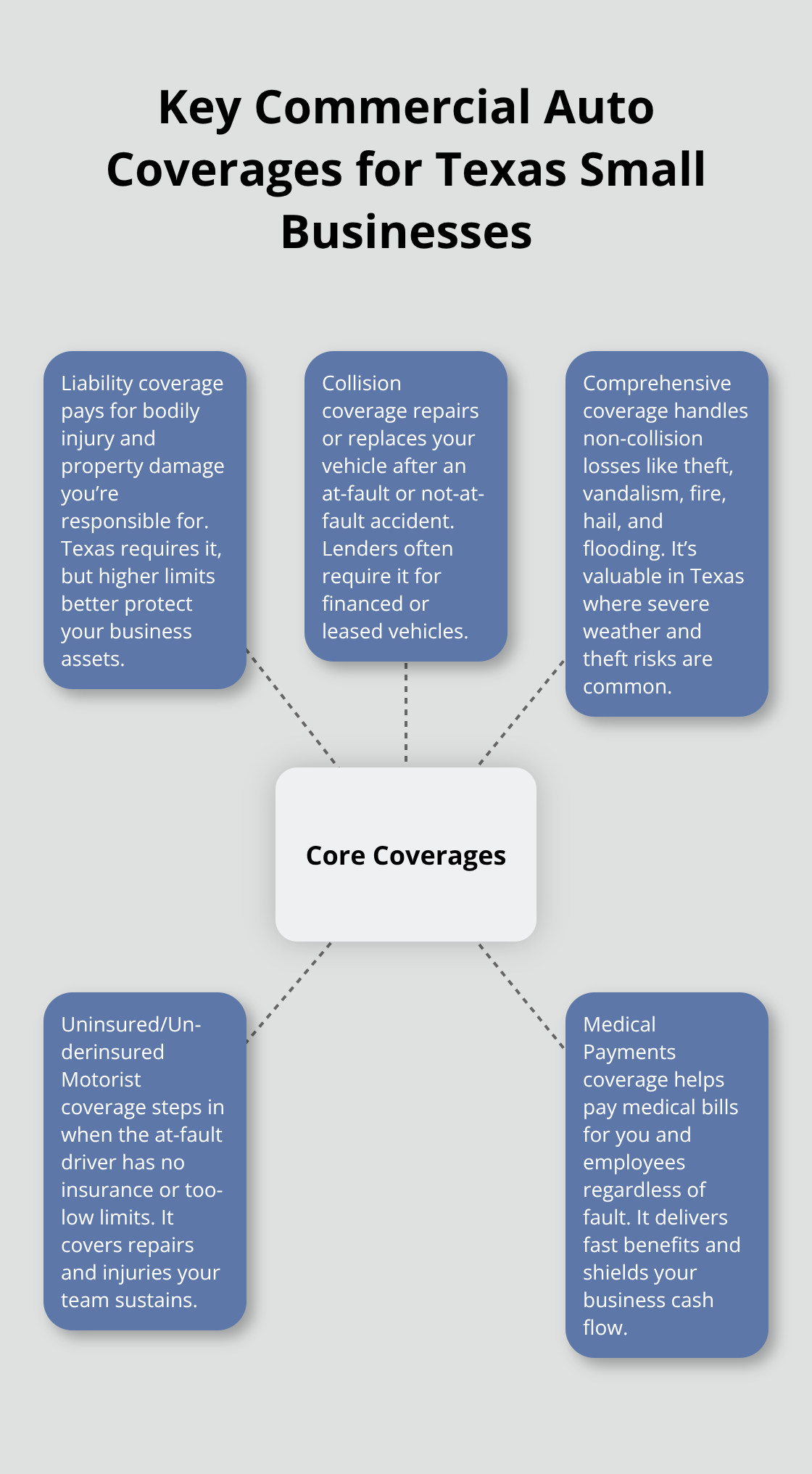

What Your Commercial Auto Policy Actually Covers

Liability coverage forms the foundation of any commercial auto policy, and Texas law requires it. The state mandates minimum limits of 30/60/25, meaning $30,000 per person for bodily injury, $60,000 per accident, and $25,000 for property damage. However, these minimums are dangerously low for most small businesses. A single serious accident involving an employee injury can easily exceed $30,000 in medical costs alone. Try pushing your bodily injury limits to at least $100,000 per person and $300,000 per accident if your business can manage the modest premium increase. Property damage claims also add up fast-hitting a utility pole, storefront, or parked vehicles can cost thousands. Many Texas businesses operate with state minimums and regret it when a claim arrives. Higher limits protect your business assets and personal finances from a catastrophic judgment.

Collision and Comprehensive Protection for Your Vehicles

Collision coverage pays to repair or replace your vehicle after an accident, regardless of who caused it. If you financed or leased your business vehicles, your lender likely requires this coverage. The catch is deductibles-a $500 deductible lowers your premium compared to a $250 option, but you’ll pay that amount out of pocket for each claim.

For small businesses operating tight margins, a higher deductible can save 15-20% on annual premiums. Comprehensive coverage handles non-collision damage like theft, vandalism, fire, or weather events. In Texas, comprehensive claims are common due to hail storms and flooding, particularly in Houston and coastal areas. If your vehicles sit unattended overnight or you park in high-theft neighborhoods, comprehensive coverage is worth the cost. Without it, a stolen work van or broken windshirt comes straight from your business bank account.

Uninsured and Underinsured Motorist Coverage

Uninsured and underinsured motorist coverage protects your business when the at-fault driver has no insurance or insufficient coverage. Texas doesn’t require this protection-you can reject it in writing-but rejecting it is a mistake. Roughly 12-15% of Texas drivers carry no insurance, according to state data. If an uninsured driver hits your company vehicle, your uninsured motorist coverage pays for repairs and medical expenses instead of your collision and medical payments coverage. Without it, you absorb the cost entirely. Underinsured motorist coverage steps in when the at-fault driver’s liability limits don’t cover your damages. For example, if another driver carries only $30,000 in bodily injury coverage but your employees suffer $80,000 in injuries, underinsured motorist coverage bridges that gap.

Medical Payments Coverage for Your Team

Medical payments coverage rounds out protection by paying for medical expenses for you and your employees after any accident, regardless of fault. This coverage pays directly to healthcare providers and prevents accident victims from draining your business finances. Your drivers face real risks on Texas roads, and medical payments coverage ensures they receive care without your business absorbing unexpected bills. As you evaluate these coverage options, the next step is understanding what actually drives your premium costs and how your choices impact your bottom line.

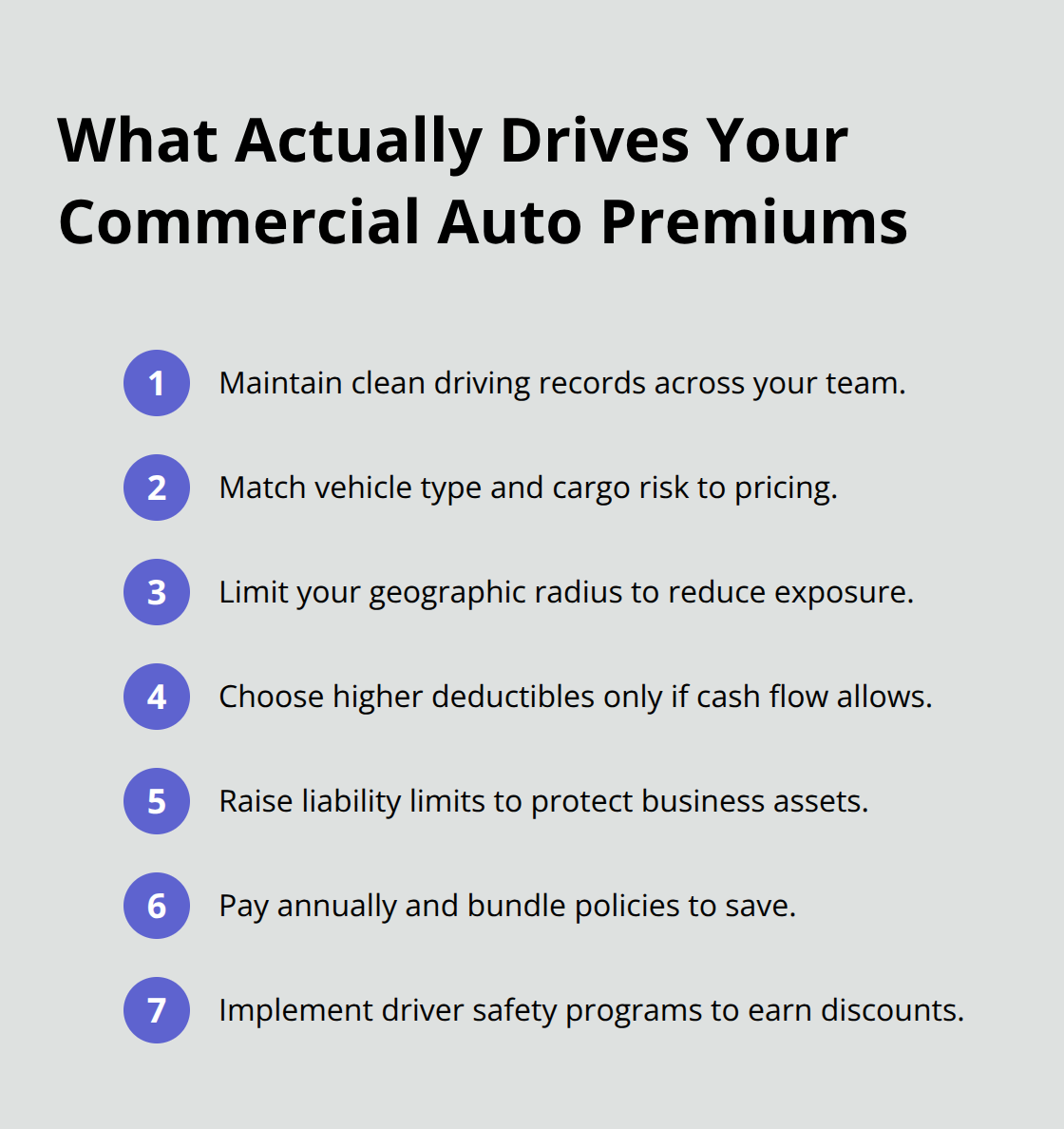

What Actually Drives Your Commercial Auto Premiums

Your premium isn’t arbitrary-insurers build it on specific factors they measure and price into every quote. Small business owners often feel shocked by renewal rates because they don’t understand what’s actually being charged. The average commercial auto policy in Texas costs about $218 per month or $2,610 annually, but that number varies wildly depending on your situation.

How Your Driving History Shapes Your Rate

Your driving history is the single biggest lever you control. Insurers review the past three years of accidents and violations for every driver on your policy, and even one at-fault accident increases your rate by 10-20% or more. A clean driving record across your team is worth real money-if your employees have multiple violations, you’ll pay substantially higher premiums than a competitor with safer drivers. This factor alone can swing your annual cost by thousands of dollars.

Vehicle Type and What You’re Hauling

Vehicle type directly impacts cost because risk varies dramatically by what you’re hauling. A food truck operating local delivery routes costs far less to insure than a contractor’s van loaded with tools and equipment traveling across multiple counties. Larger vehicles and those used for frequent stops in high-traffic areas naturally command higher premiums.

Equipment-heavy trucks and vehicles used for deliveries or field service typically cost more than lower-risk professional vehicles.

Geographic Territory and Location Matter

The geographic radius you operate within matters more than most business owners realize. Staying within your local city typically generates lower premiums than covering a multi-county service area, because insurers see expanded territory as expanded exposure to claims. Dallas and Houston command higher premiums than smaller Texas cities like Beaumont due to denser traffic, more accidents, and higher settlement costs in urban areas. Your location within Texas directly affects what you’ll pay.

Deductibles, Limits, and Payment Strategies

Your deductible and coverage limit choices directly translate to premium savings or costs. Increasing your deductible from $250 to $500 can save 15-20% annually, but only if your business cash flow can actually absorb that out-of-pocket hit when a claim occurs. Higher liability limits beyond Texas minimums do raise your premium, but the increase is modest compared to the protection you gain-pushing from 30/60/25 to 100/300/100 might add $30-50 monthly but shields your business from catastrophic exposure.

Paying your annual premium in full instead of monthly installments yields 13% or more in savings, which is substantial if you have the cash available. Bundling your commercial auto policy with other business coverage like general liability or property insurance saves approximately 12% on your auto premium alone. If you operate multiple vehicles, the number on your policy affects pricing-adding a second or third vehicle typically costs less per vehicle than insuring them separately because insurers offer volume discounts.

Safety Programs and Additional Discounts

Implementing a documented safe driving program for your team can unlock additional discounts from most carriers, though you’ll need to track training completion and maintain records showing your commitment to reducing accidents. These programs demonstrate to insurers that you take risk seriously, and they reward that commitment with lower rates. The combination of these factors-your drivers’ records, your vehicles, your territory, and your choices about coverage-determines what you’ll pay. Understanding each one helps you make smarter decisions about where to invest in protection and where you can safely reduce costs. As you evaluate these premium drivers, the next critical decision involves identifying which coverage gaps could expose your business to real financial danger.

Common Mistakes Small Business Owners Make with Commercial Auto Insurance

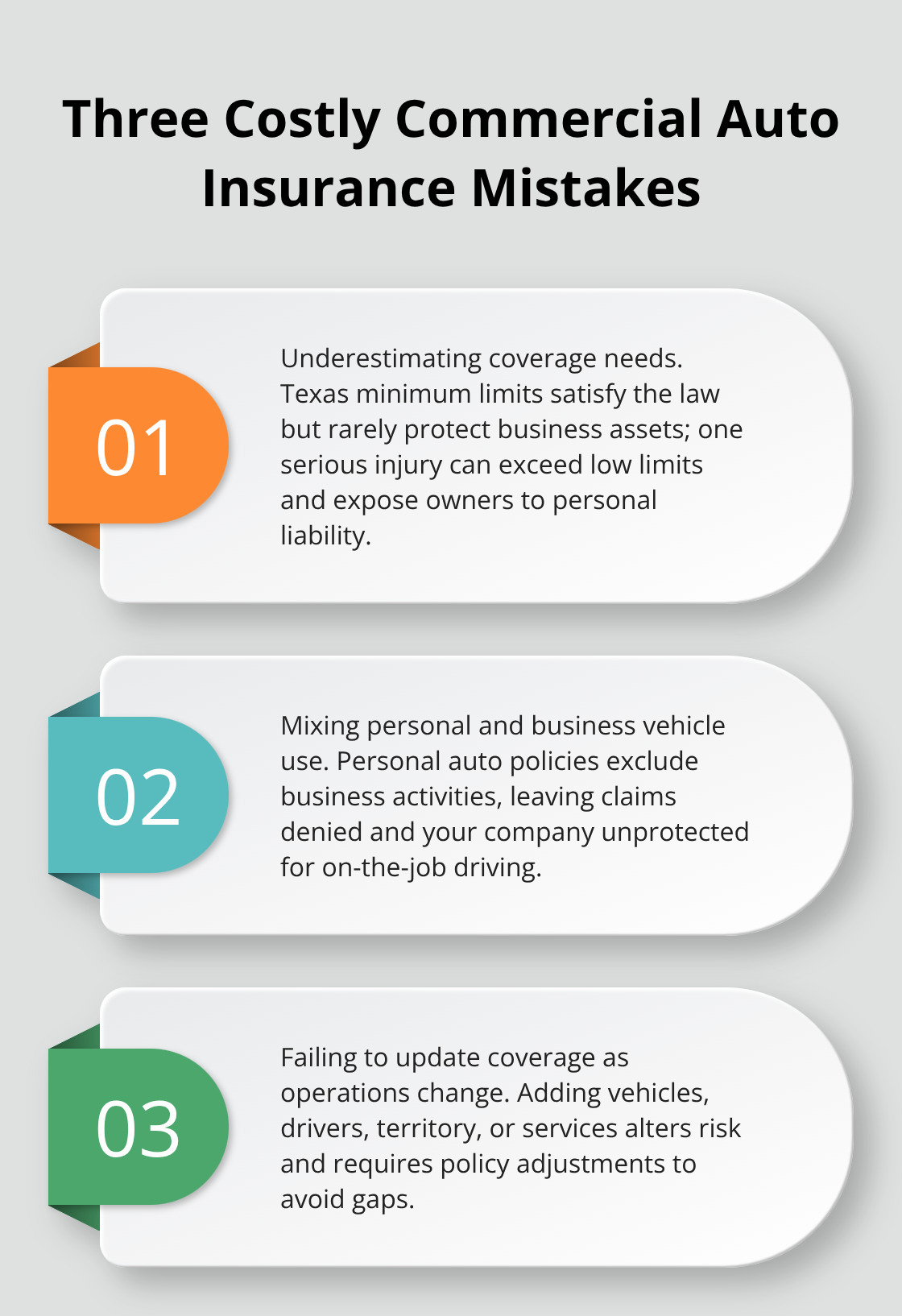

Most small business owners make three critical mistakes that expose their operations to financial disaster, and the first one costs them thousands in unnecessary risk. Underestimating coverage needs happens because owners compare their business to competitors and assume similar limits will work, but your specific operation determines what you actually need. A contractor hauling expensive equipment across multiple counties faces vastly different exposure than a local service business with one vehicle. Texas minimum liability limits exist only to satisfy legal requirements, not to protect your business assets. Owners renew policies year after year with these bare minimums, then face personal liability when a serious accident exceeds those limits. A single employee injury requiring surgery and long-term care easily surpasses $30,000 in medical costs, and if you’re personally liable for amounts above your coverage, creditors can pursue your personal assets.

Calculate Your True Coverage Needs

The solution involves matching your limits to your actual exposure: a food truck operating in one city needs different coverage than a contractor traveling across Texas. Calculate your worst-case scenario and add 20 percent to that number, then set your bodily injury limits there. Higher limits cost surprisingly little extra-moving from your state minimums to higher coverage typically adds only $30-50 monthly to your premium. This modest increase shields your business from catastrophic exposure far more effectively than operating with state minimums.

Avoid Mixing Personal and Business Vehicle Use

The second mistake involves mixing personal and business vehicle use, which creates commercial auto insurance coverage gaps that personal auto policies explicitly exclude. Your personal auto insurance will deny any claim involving business activities, period. If an employee drives their personal vehicle to make a work delivery and causes an accident, your business has zero coverage from their personal policy, and your personal policy won’t cover business use either. Texas law requires business-use vehicles to carry commercial auto coverage, but many owners try to stretch personal policies or ignore the requirement entirely. Penalties for operating without proper coverage include fines up to $350 for a first offense and up to $1,000 plus license suspension for repeat violations.

Update Coverage When Your Business Changes

The third critical mistake is failing to update your coverage when your business changes. If you add a second vehicle, hire more drivers, expand your service territory, or shift from local to regional operations, your existing policy does not automatically adjust to match that new risk profile. A landscaper who starts offering delivery services faces completely different exposure than one providing only on-site work, yet many owners never notify their insurer of the change. Coverage gaps emerge silently until a claim arrives and you discover your policy does not cover your current operations. Schedule a coverage review with your agent annually or whenever your business changes significantly-adding vehicles, hiring drivers, expanding territory, or changing what you transport all require policy adjustments.

Final Thoughts

Commercial auto insurance for small businesses isn’t a one-time purchase you make and forget about. The coverage decisions you make today directly determine whether your business survives a serious accident or faces financial ruin. You now understand what your policy actually covers, what drives your premiums, and which mistakes expose your operation to unnecessary risk.

Audit your current coverage against your actual business operations and calculate what a serious accident would cost your business. If you operate with Texas minimum limits, adjust your bodily injury and property damage limits accordingly-the premium increase for higher limits is modest compared to the protection you gain. Verify that every vehicle used for business purposes carries commercial auto insurance for small business operations, not personal auto insurance, because this distinction matters legally and financial.

We at Brooks Insurance represent multiple top-rated insurance companies, which means you have access to a larger selection of coverage, pricing, and payment options when you work with us. Our licensed agents understand Texas commercial auto requirements and can match your business to the right policy without overpaying for unnecessary coverage or leaving dangerous gaps. Contact Brooks Insurance today to discuss your commercial auto insurance needs and receive quotes tailored to your specific operation.