General liability insurance rate factors vary dramatically from one business to another. At Brooks Insurance, we’ve seen premiums swing by hundreds of dollars based on simple changes business owners can make.

Your industry, revenue, and claims history are the biggest drivers of your costs. Understanding what insurers look at helps you take control of your rates.

What Drives Your General Liability Rates

Industry Classification Sets Your Premium Foundation

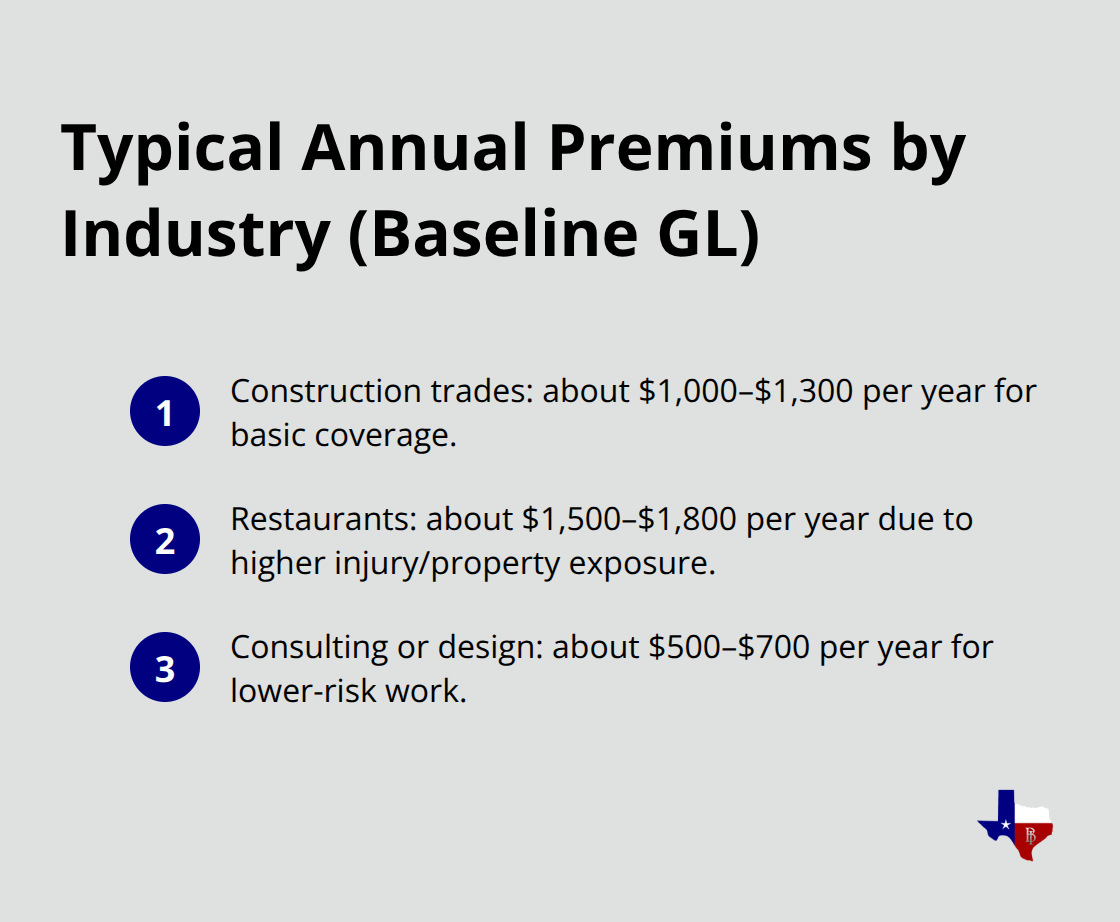

Your industry classification determines your starting point for premiums, and insurers take this seriously. Construction trades like roofing and demolition typically pay $1,000 to $1,300 annually for basic coverage, while restaurants face $1,500 to $1,800 yearly due to higher injury and property damage exposure. Consulting or design professionals often pay $500 to $700 annually. This isn’t arbitrary-insurers analyze claim frequency and severity data specific to your industry, and high-risk sectors simply generate more claims.

If you operate in construction, healthcare, or food service, expect your rates to reflect the actual risk profile of those industries rather than what you might pay for lower-risk work.

Revenue and Payroll Size Expand Your Exposure

Your business revenue and payroll size matter enormously because they signal exposure volume. A contractor with $500,000 in annual revenue faces different risk than one doing $2 million in work-more projects mean more opportunities for incidents. Payroll size works similarly; more employees increase third-party interaction exposure and potential liability claims. These metrics directly correlate with how much activity your business conducts, which insurers use to project claim likelihood.

Claims History Determines Your Long-Term Costs

Claims history is your most controllable rate factor, yet many business owners overlook its long-term impact. A single significant claim can elevate your premiums for years. Texas’s Composite Rating Plan rewards loss-free history with credits that reduce your long-term costs. This means maintaining a clean record directly reduces what you pay.

Location and Coverage Choices Shape Final Premiums

Location matters too-urban Dallas areas with high foot traffic and litigation activity typically see higher rates than quieter regions, reflecting local legal environments and disaster risk. Your coverage limits and deductible choices also shift premiums significantly. A policy with $1 million per occurrence and $2 million aggregate represents the common baseline, but raising limits to $2 million per occurrence increases your premium substantially, while raising your deductible from $500 to $2,500 can cut costs noticeably if you’re willing to absorb more risk out-of-pocket.

Understanding these rate factors positions you to make informed decisions about your coverage. The next section shows you exactly how to reduce these costs through practical steps you can take today.

Cut Your Premiums Without Cutting Coverage

Safety Protocols Reduce Your Rates Directly

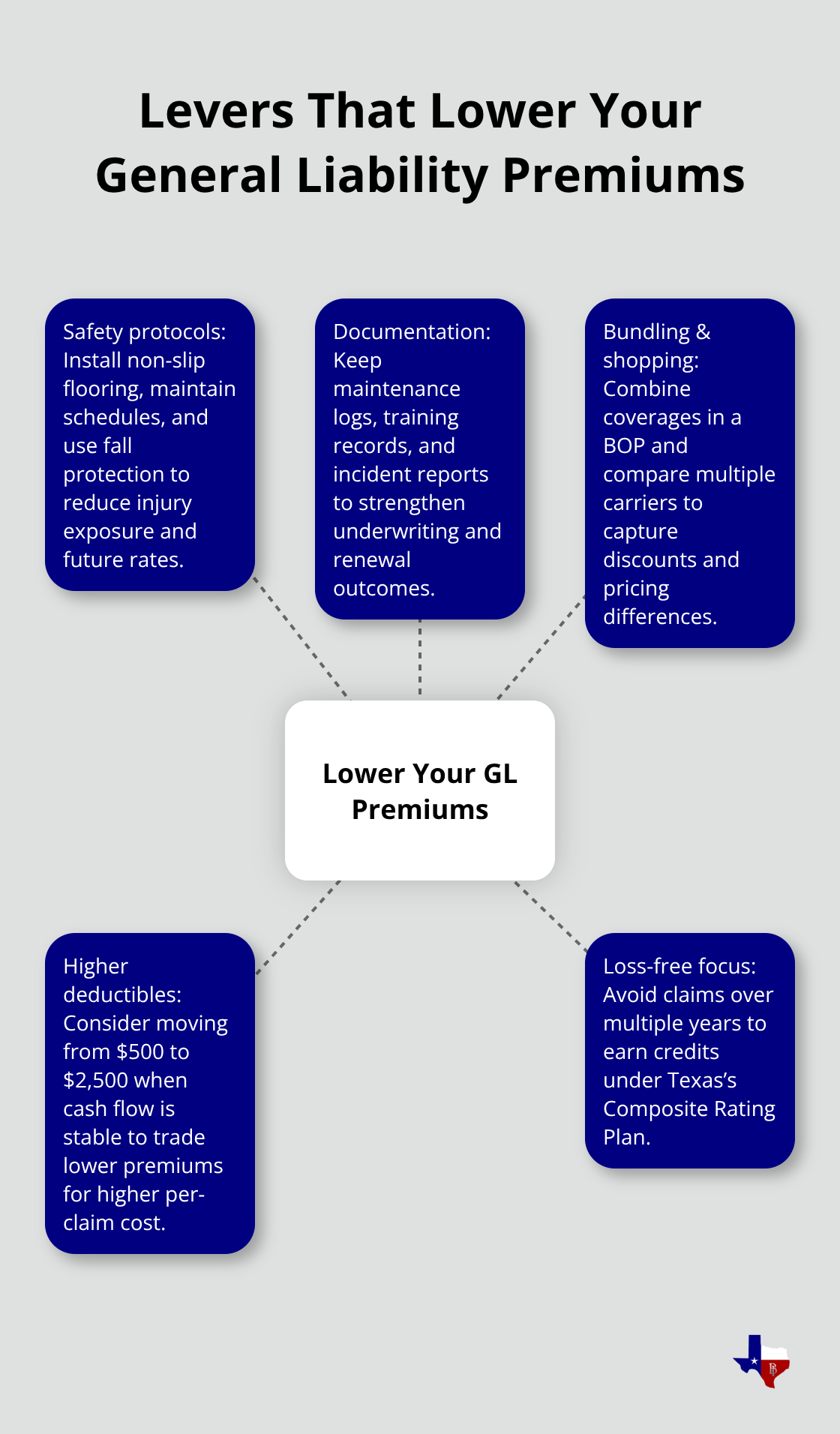

Safety protocols cut what you pay. We’ve seen businesses lower premiums by installing non-slip flooring, maintaining documented schedules, and conducting regular equipment inspections. Insurers offer measurable discounts for businesses that prevent claims through concrete actions. A roofing contractor who invests in fall protection systems and documents safety training reduces injury exposure, which translates to lower rates at renewal. The Texas Composite Rating Plan rewards loss-free histories with credits for businesses maintaining clean records over five years or more. Your safety investment compounds over time-one year of zero claims helps, but three to five years of clean history produces substantial rate reductions.

Documentation Strengthens Your Risk Profile

Documentation matters equally. Maintain detailed records of maintenance, safety training completion, incident reports (even minor ones), and corrective actions taken after near-misses. Insurers evaluate these records during underwriting and renewal, and thorough documentation strengthens your risk profile significantly. A restaurant owner who tracks daily cleaning logs, staff training certifications, and equipment maintenance creates a compelling case for lower rates compared to a competitor with no documented systems. This documentation also protects you if a claim occurs, as it demonstrates reasonable care and reduces your liability exposure.

Bundling Policies Cuts Costs Substantially

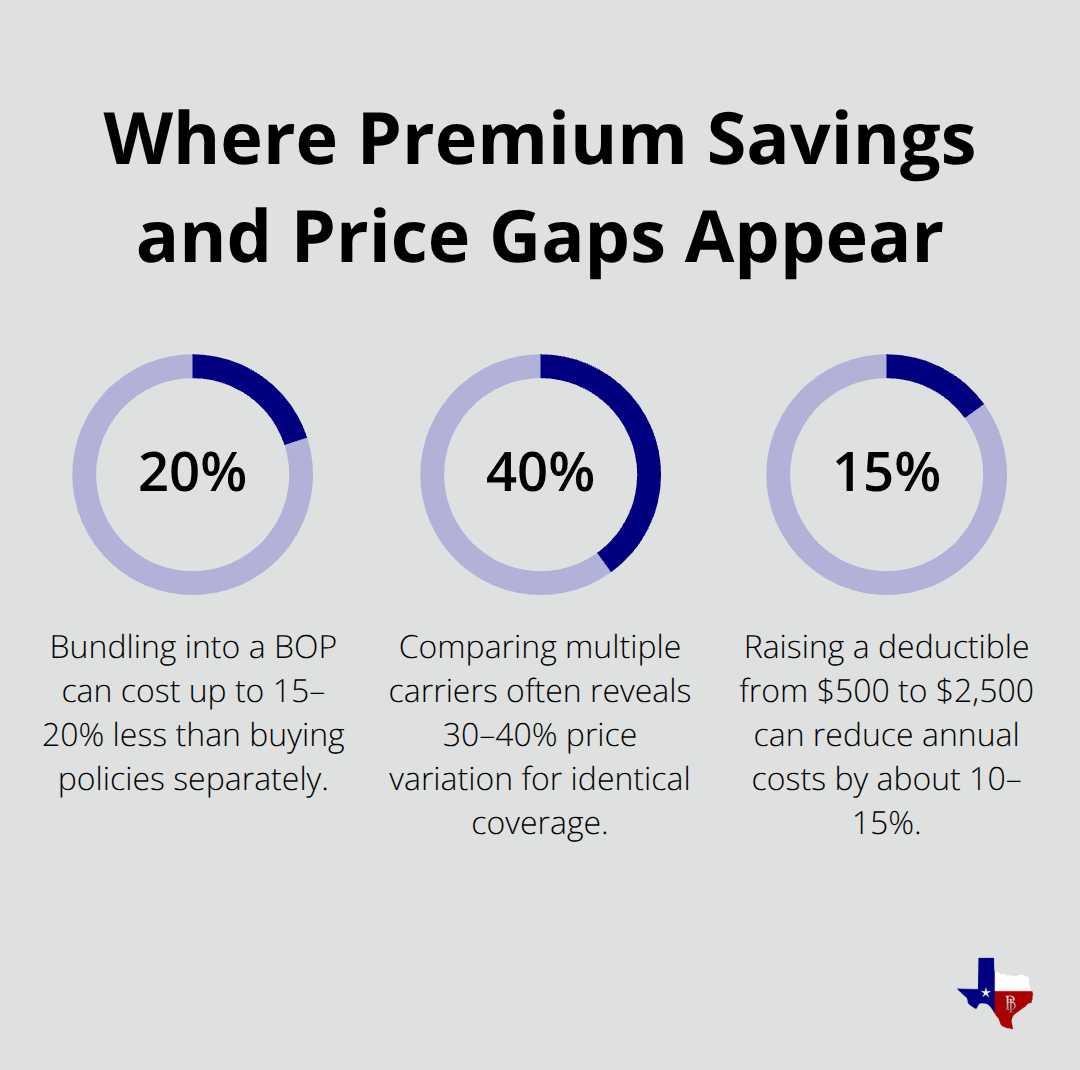

Bundling policies and comparing multiple quotes are non-negotiable cost-reduction tactics. A Business Owner’s Policy combining general liability with commercial property and business interruption coverage typically costs 15-20% less than purchasing policies separately. More importantly, comparing quotes from multiple insurers reveals pricing variations that can swing 30-40% for identical coverage.

Some insurers specialize in your industry and price accordingly, while others overprice because your business type falls outside their sweet spot. An independent agency accesses quotes from multiple carriers simultaneously, eliminating the tedious process of contacting five different insurers individually.

Higher Deductibles Lower Annual Premiums

Higher deductibles also cut premiums noticeably-raising your deductible from $500 to $2,500 can reduce annual costs by 10-15%, though you absorb more out-of-pocket risk if a claim occurs. The math works when your claims history is clean and your business generates stable cash flow. This trade-off between lower premiums and higher out-of-pocket exposure requires honest assessment of your financial position and risk tolerance. The next section addresses common misconceptions that prevent business owners from optimizing their coverage and costs.

Why Your Quote Matters More Than You Think

Quotes Vary Dramatically Across Carriers

General liability quotes are not interchangeable, yet most business owners treat them that way. Insurers price identical coverage differently based on their underwriting appetite, claims data by region, and how they classify your specific operations. A roofing contractor might receive a quote of $1,150 from one carrier and $1,450 from another for the same $1 million per occurrence limit. That $300 difference compounds over five years into $1,500 in unnecessary costs. Texas businesses often overpay simply because they accepted the first quote without shopping competitors.

Comparing quotes from multiple carriers reveals these pricing gaps immediately. An independent agency accesses quotes from numerous insurers simultaneously, eliminating the need to contact each carrier individually. This comparison process typically uncovers 20-40% pricing variations for identical coverage structures, making it the single most effective cost-reduction tactic available.

Your Rate Changes After Purchase

Your rate after purchase isn’t locked in stone, despite what many business owners believe. Texas’s Composite Rating Plan rewards loss-free history with credits that reduce premiums at renewal. Your actions directly control future rates.

A contractor who invests in safety equipment, maintains detailed training records, and avoids claims for three consecutive years qualifies for meaningful premium reductions at renewal. This reward structure means your safety investments compound over time rather than disappear after one year.

Coverage Limits Drive Premium Changes

Coverage limit choices directly influence what you pay monthly or annually. Raising limits from $1 million per occurrence to $2 million per occurrence increases premiums substantially, sometimes 30-50% depending on your industry and location. Conversely, selecting appropriate limits that match your actual contract requirements and risk exposure prevents overpaying for unnecessary coverage.

Many business owners purchase $2 million limits reflexively without evaluating whether their typical projects and client contracts actually require that protection. Reviewing your policy annually with an agent who understands your operations ensures your coverage limits align with genuine exposure rather than inflated protection you don’t need.

Final Thoughts

Your general liability insurance rate reflects factors you control and factors you cannot. Industry classification, revenue, and claims history form your premium foundation, but your safety practices, documentation, and policy structure determine whether you pay fair value or overpay significantly. The gap between the highest and lowest quotes for identical coverage often exceeds 30 percent, which means most Texas business owners leave substantial savings on the table by accepting the first offer without comparison.

An independent agency changes this equation entirely. We at Brooks Insurance represent multiple top-rated insurance companies, so you access quotes from numerous carriers simultaneously rather than contacting each one individually. Our licensed agents understand how general liability insurance rates vary by industry, location, and underwriting criteria, and we identify which carriers price your specific risk most competitively.

Contact Brooks Insurance to discuss your general liability coverage and receive quotes from multiple carriers. Our team has over 50 years of experience helping Texas businesses find coverage that matches their actual risk and budget, and we walk you through the rate factors affecting your premiums to show you exactly where you can reduce costs without sacrificing protection.

Disclaimer: The information provided in this blog is for general informational purposes only and does not constitute legal, financial, or insurance advice. Coverage options, terms, and availability may vary. Please consult with a licensed professional for advice specific to your situation