General liability insurance protects your Texas business from costly lawsuits and medical claims. But understanding how much general liability insurance costs requires looking at your specific situation.

At Brooks Insurance, we help business owners navigate pricing so they can find coverage that fits their budget. This guide breaks down the factors that impact your premiums and shows you practical ways to save.

What Drives Your General Liability Premium

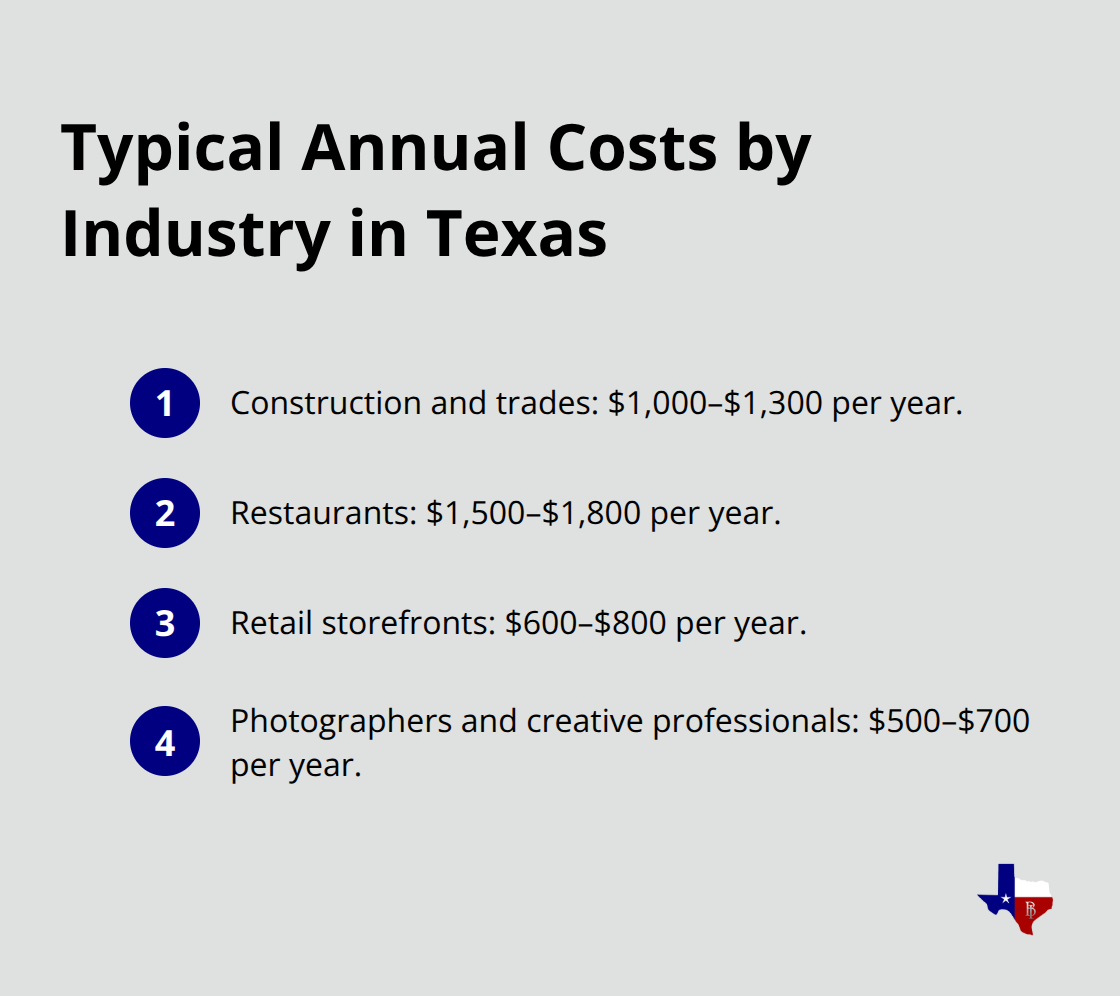

Your industry determines more than just what you do-it determines your insurance cost. Construction companies and restaurants pay significantly more than consulting firms because they face higher injury and property damage risks. According to data from policies sold through Insureon, construction and trades businesses typically pay $1,000–$1,300 annually, while restaurants run $1,500–$1,800 due to slip-and-fall exposure and high customer volume. Retail storefronts in Texas average $600–$800 per year, whereas photographers and creative professionals pay around $500–$700.

Insurers base premiums on industry-specific claim patterns in Texas. If you operate in a high-risk industry, expect higher costs, but don’t assume you’re overpaying-shop for quotes anyway since rates vary significantly between carriers even within the same industry.

How Revenue and Payroll Impact What You Pay

Business size matters, but not uniformly across all industries. Construction companies see premiums rise sharply as annual revenue increases, while office-based IT consulting typically experiences only small premium changes with revenue growth. This happens because construction work scales exposure-more revenue usually means more projects, more employees on-site, and more opportunities for claims. The standard baseline most Texas businesses use is $1 million per occurrence and $2 million aggregate limits, which about 91 percent of Insureon customers select. A business that generates $50,000 annually versus $500,000 faces a substantially different risk profile, and insurers price accordingly. A clean claims history and fewer employees keep costs down, but growth without strong safety practices pushes premiums up.

Claims History Determines Your Rate Tomorrow

Your past claims are the strongest predictor of future premiums. One accident or lawsuit can raise your rates for several years, sometimes dramatically. This is why risk management isn’t optional-it’s a financial investment. Practical steps like installing non-slip mats, maintaining clear walkways, scheduling regular maintenance, and documenting safety procedures actually lower claim frequency and reduce long-term costs. Location also matters within Texas; Dallas and DFW areas typically cost more than rural regions due to higher foot traffic, greater activity density, and more claim activity. A business with a spotless safety record in a lower-risk area pays far less than a similar business with previous claims in a busy urban location. When you apply for coverage, be honest about your history and proactive about preventing future incidents.

Location and Urban Risk Factors

Where your business operates significantly affects what you pay. Urban centers like Dallas experience higher premiums than rural Texas because foot traffic, activity density, and claim frequency all increase in populated areas. Landlords and contractors in DFW often require higher coverage limits and endorsements, which push premiums upward. A storefront on a busy street faces more slip-and-fall exposure than a quiet office building. These location-based differences aren’t just about geography-they reflect real differences in how often claims occur and how expensive they are to settle. Your address matters as much as your industry when insurers calculate your rate.

Coverage Limits and Deductibles Shape Your Cost

The protection level you choose directly affects your premium. Most Texas businesses select $1 million per occurrence and $2 million aggregate limits as their baseline, but moving to $2 million per occurrence typically adds about $30 per month to your cost. Higher limits mean higher premiums, but also more protection against catastrophic claims. Deductibles work the opposite way-increase your deductible and your premium drops, but you’ll pay more out of pocket if you file a claim. The typical deductible chosen by small business owners is around $500. Align your limits and deductibles with your actual risk exposure and financial capacity rather than choosing arbitrarily. This balance between protection and affordability determines whether your coverage truly fits your business needs.

What Texas Businesses Actually Pay for General Liability

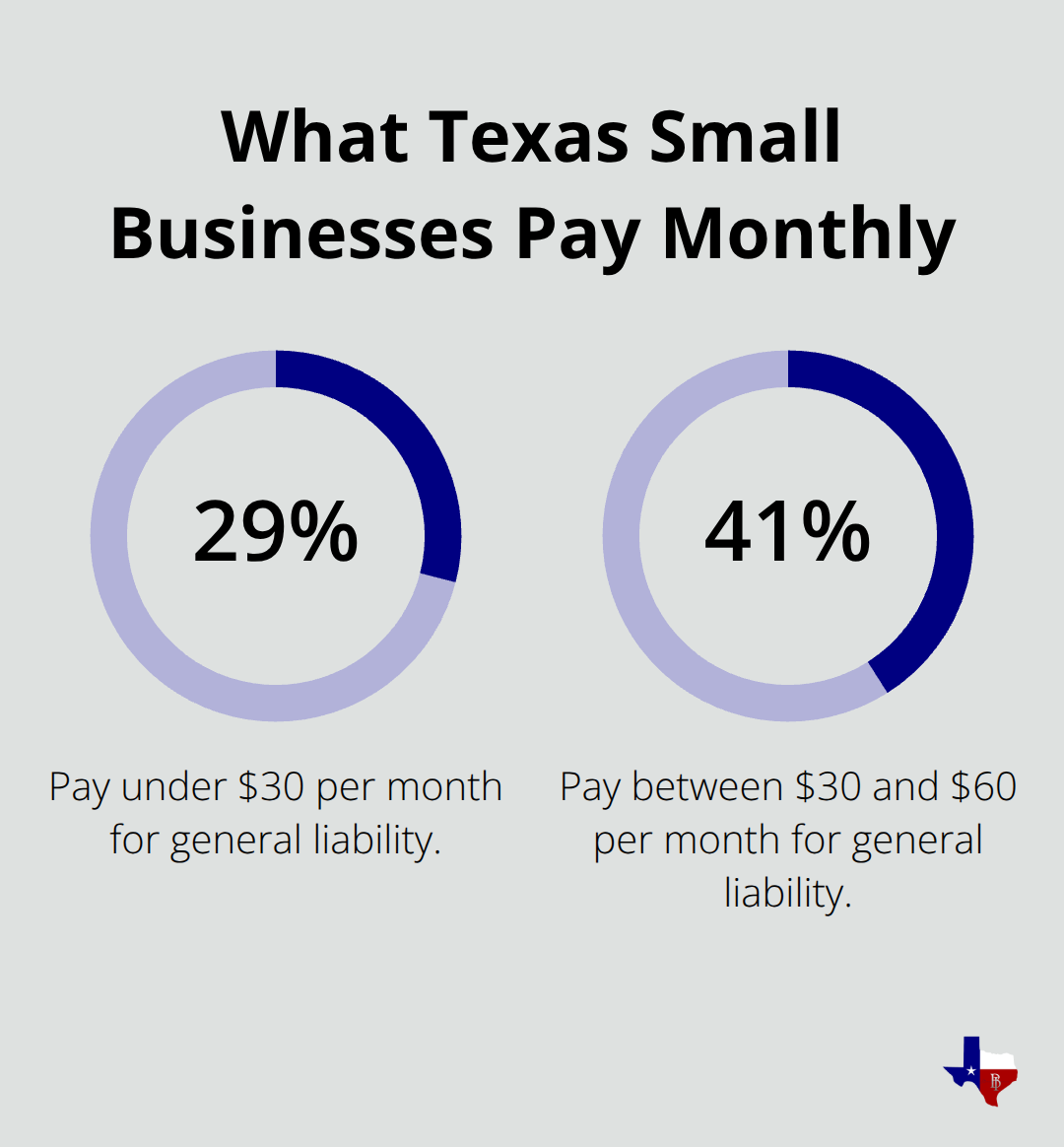

General liability insurance costs in Texas range from roughly $40 to $100 per month for most small businesses, but this wide spread reflects massive differences in what you actually do and where you do it. According to data from about 40,000 small business policies sold through Insureon as of January 2026, 29 percent of owners pay under $30 monthly while 41 percent fall between $30 and $60.

The median monthly cost across all Texas businesses sits around $45, or about $500 annually. However, these averages mask critical variations by industry and business structure. Very small, low-risk businesses like solo consultants or freelancers in Texas typically pay $40–$60 monthly, roughly $480–$720 per year. This affordability makes general liability accessible even for home-based operations, though you still need it because online and advertising risks still matter-even remote businesses face claims from copyright disputes, defamation, or ad issues.

Your Industry Determines the Real Price Tag

Stepping into retail or customer-facing work immediately changes your cost. Retail storefronts in Texas average $600–$800 annually, while photographers and creative professionals pay around $500–$700. This gap exists because foot traffic creates slip-and-fall exposure and property damage risk. Construction and trades businesses jump significantly higher, typically paying $1,000–$1,300 per year due to on-site hazards and mandatory contract requirements. Restaurants and food businesses face the steepest premiums at $1,500–$1,800 annually because slip-and-fall claims happen constantly and customer volume amplifies risk. If you operate in one of these high-risk sectors, understand that higher costs reflect genuine claim patterns, not arbitrary pricing. Your industry risk category is the single biggest driver of premiums, and it’s non-negotiable-you cannot shop your way out of being in a restaurant; you can only manage risk better and compare quotes across multiple carriers to find the best rate for your specific operation.

How Coverage Choices Impact Your Monthly Payment

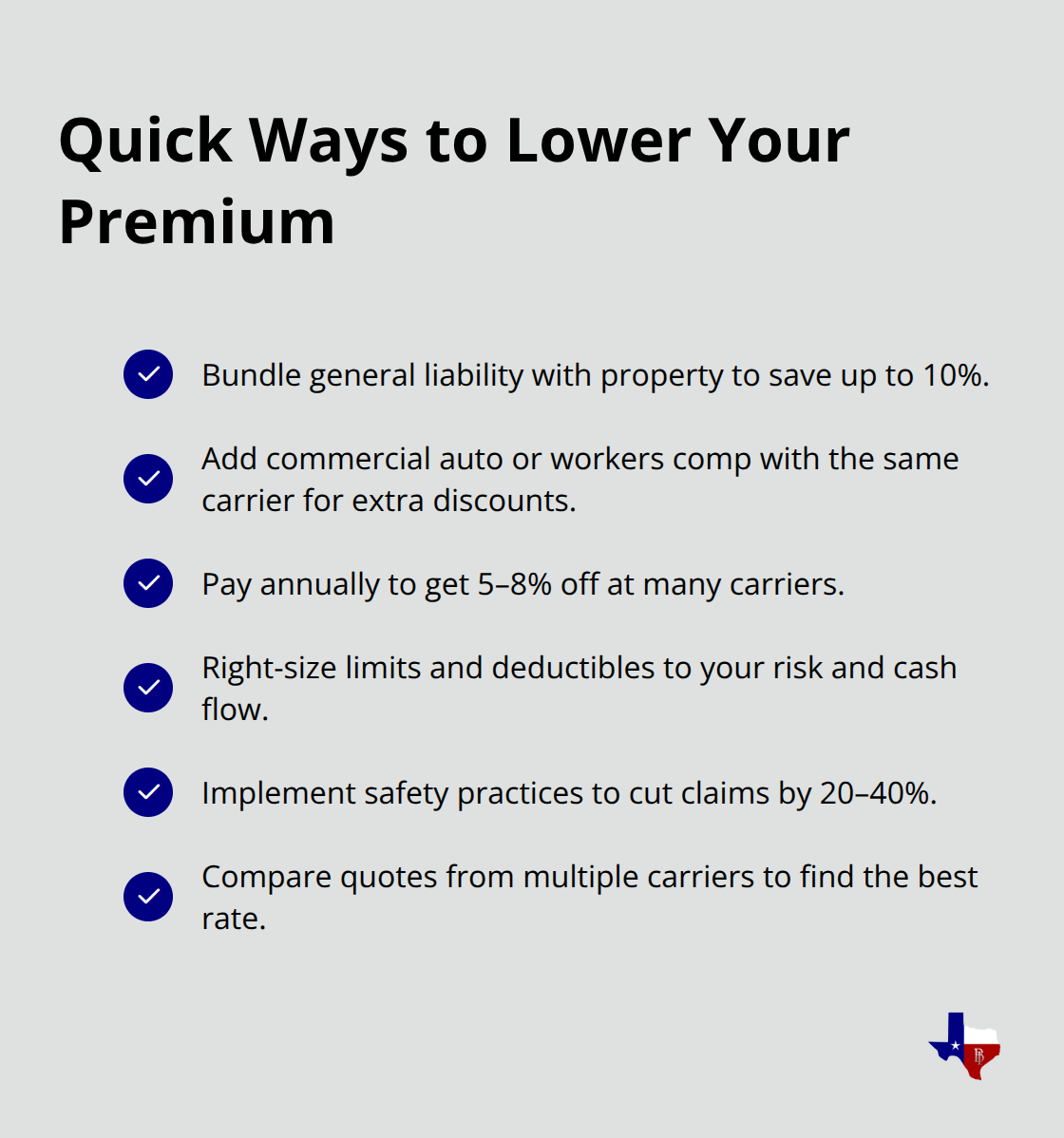

The protection level you select directly changes what you pay. Moving from the standard $1 million per occurrence and $2 million aggregate baseline to $2 million per occurrence typically adds about $30 monthly to your cost. Since about 91 percent of Insureon customers select the $1M/$2M combination while only 5 percent choose higher limits, most Texas businesses find this baseline appropriate. Your deductible choice works inversely-increasing it from $500 to $1,000 lowers your monthly premium but means you’ll pay more out of pocket if a claim occurs. The typical deductible small business owners select is around $500, which balances affordable premiums with manageable risk. Bundling policies matters significantly here; a Business Owner’s Policy combines general liability with property insurance and often costs substantially less than buying them separately, with some insurers offering discounts up to 10 percent when you bundle. Paying your premium upfront annually rather than monthly installments also yields discounts at most carriers. These aren’t minor tweaks-choosing the right limits, deductible, and bundle structure can reduce your annual cost by hundreds of dollars while maintaining appropriate protection.

Finding the Right Quote for Your Situation

Your actual premium depends on business-specific factors such as profession, risk exposure, location, and number of employees. Higher-risk professions (for example, landscapers) pay more for general liability than lower-risk roles (such as consultants). Location matters: premiums tend to be higher in highly populated areas or locations with more claim activity. The number of employees influences cost because more workers can increase the chance of accidents and claims. Time in business also affects pricing; newer businesses may pay more initially, while a longer safety track record can lower premiums over time. The most reliable way to know your cost is to obtain a quote, as prices reflect your unique risk and coverage choices. An independent insurance agency can compare quotes from multiple top-rated insurers, helping you decide between standalone general liability and a Business Owner’s Policy while guiding your annual coverage reviews.

Ways to Lower Your General Liability Insurance Costs

The difference between paying $500 annually and $2,000 annually often comes down to three deliberate choices you make right now. Business owners frequently leave hundreds of dollars on the table every year by accepting the first quote they receive or failing to implement basic risk controls. Your premium isn’t fixed-it responds directly to the actions you take.

Safety Investments Reduce Claims and Lower Rates

Safety practices can lower your insurance premiums by 20-40% because insurers reward risk reduction with lower rates. A construction company that documents daily safety inspections, maintains equipment properly, and trains workers on hazard prevention genuinely experiences fewer claims, and insurers price accordingly. Non-slip mats on wet floors, clear walkways free of obstacles, regular equipment maintenance, and written safety procedures form the foundation of lower premiums. These aren’t optional tasks-they’re financial investments that reduce your long-term costs. The practical steps you take today directly affect what you pay next year.

Adjust Your Deductible to Match Your Cash Flow

The typical deductible small business owners choose is around $500, but increasing it to $1,000 or $1,500 reduces your monthly premium significantly. This only makes sense if you can actually afford to pay that deductible without crippling your cash flow when a claim occurs. Calculate what your business can realistically handle out of pocket, then set your deductible there. Higher deductibles directly lower your annual cost, sometimes by $200 or more depending on your industry and coverage limits. The trade-off is straightforward: lower premiums now mean higher out-of-pocket costs if you file a claim.

Bundle Policies and Pay Annually for Maximum Savings

A Business Owner’s Policy combines general liability with property insurance and often costs substantially less than purchasing them separately, with some insurers offering discounts up to 10 percent when bundled. If you also need commercial auto or workers compensation, stacking these policies with one carrier typically yields additional discounts beyond the bundling savings itself. Paying your annual premium upfront rather than spreading payments across twelve months also generates discounts at most carriers-sometimes 5 to 8 percent, which on a $1,000 annual policy saves $50 to $80. These aren’t minor tweaks; choosing the right limits, deductible, and bundle structure can reduce your annual cost by hundreds of dollars while maintaining appropriate protection.

Shop Multiple Carriers to Find Your Best Rate

Rates vary dramatically between carriers even for identical coverage. One carrier might quote $60 monthly while another quotes $45 for the same business in the same location. An independent agency can compare quotes from multiple top-rated insurers, which matters because each carrier weights risk factors differently. Shopping takes thirty minutes but potentially saves hundreds annually. As an independent agency with over 50 years of experience, Brooks Insurance represents multiple top-rated insurance companies, which means you have a larger selection of coverage, pricing, and payment options to find the combination that actually fits your budget and protects your business.

Final Thoughts

Your general liability insurance cost reflects decisions you control right now. Industry type, business size, claims history, and location set the baseline, but your coverage choices and risk management practices determine whether you pay $500 or $2,000 annually. Texas businesses pay anywhere from $40 monthly for low-risk home-based operations to $150 monthly for high-risk industries like restaurants, with most falling between $30 and $60 monthly.

Three concrete actions move you forward. First, implement basic safety practices that reduce claims and lower your premiums by 20 to 40 percent-non-slip mats, clear walkways, regular maintenance, and documented safety procedures directly affect next year’s rate. Second, adjust your deductible and coverage limits to match your actual risk and cash flow rather than accepting defaults, and bundle general liability with property insurance into a Business Owner’s Policy to cut your total cost by 10 percent or more. Third, shop multiple carriers because rates vary dramatically for identical coverage.

Getting your quote takes thirty minutes but potentially saves hundreds annually. At Brooks Insurance, our licensed agents represent multiple top-rated insurance companies, which means you have a larger selection of coverage, pricing, and payment options to find what actually fits your budget. Contact us today to compare quotes and discover how much does general liability insurance cost for your specific situation.

Disclaimer: The information provided in this blog is for general informational purposes only and does not constitute legal, financial, or insurance advice. Coverage options, terms, and availability may vary. Please consult with a licensed professional for advice specific to your situation