Commercial auto insurance costs significantly more than personal auto policies, and business owners need to understand why. At Brooks Insurance, we’ve helped Texas business owners navigate these price differences and find coverage that fits their budgets.

The gap between personal and commercial rates depends on several factors-from how you use your vehicles to your driving history. This guide breaks down what drives those costs and shows you practical ways to reduce your premiums.

What Makes Commercial Auto Insurance More Expensive

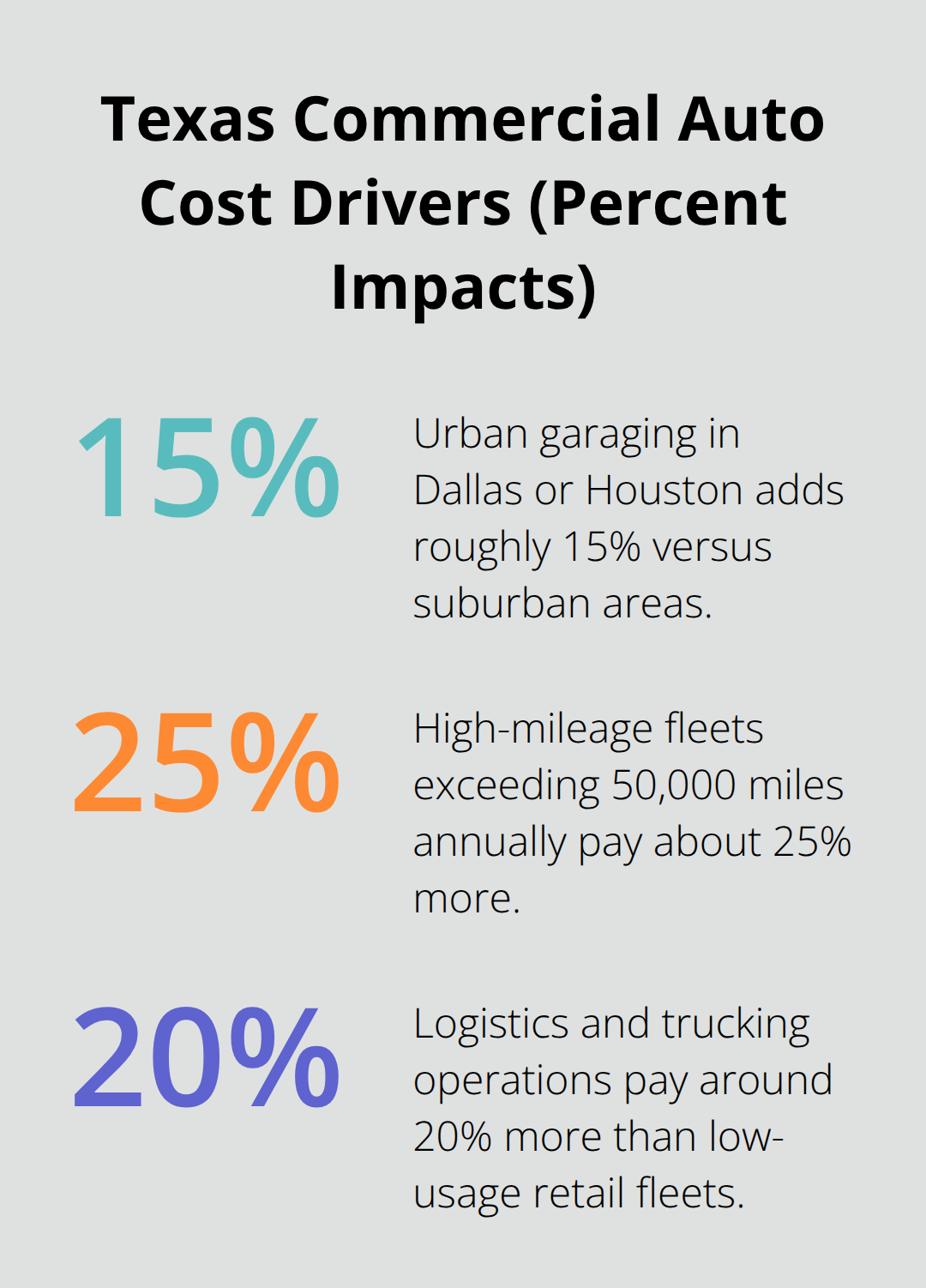

Vehicle type shapes your premium more than most business owners realize. A heavy-duty truck used in construction costs substantially more to insure than a sedan used for occasional client visits. Repair costs drive this difference-specialized parts for commercial vehicles run higher, and labor for complex repairs takes longer. If your business operates in Dallas or Houston with vehicles garaging in high-traffic urban areas, your premiums jump roughly 15 percent compared to suburban locations. Urban corridors like Dallas I-35E and Houston I-610 experience hundreds of crashes monthly, and insurers price accordingly. High-mileage fleets that exceed 50,000 miles annually see premium increases around 25 percent because more time on the road means greater exposure to accidents. Industry matters too-logistics and trucking operations along busy Texas corridors pay about 20 percent more than low-usage retail fleets due to elevated accident risk.

Driver Records Determine Real Costs

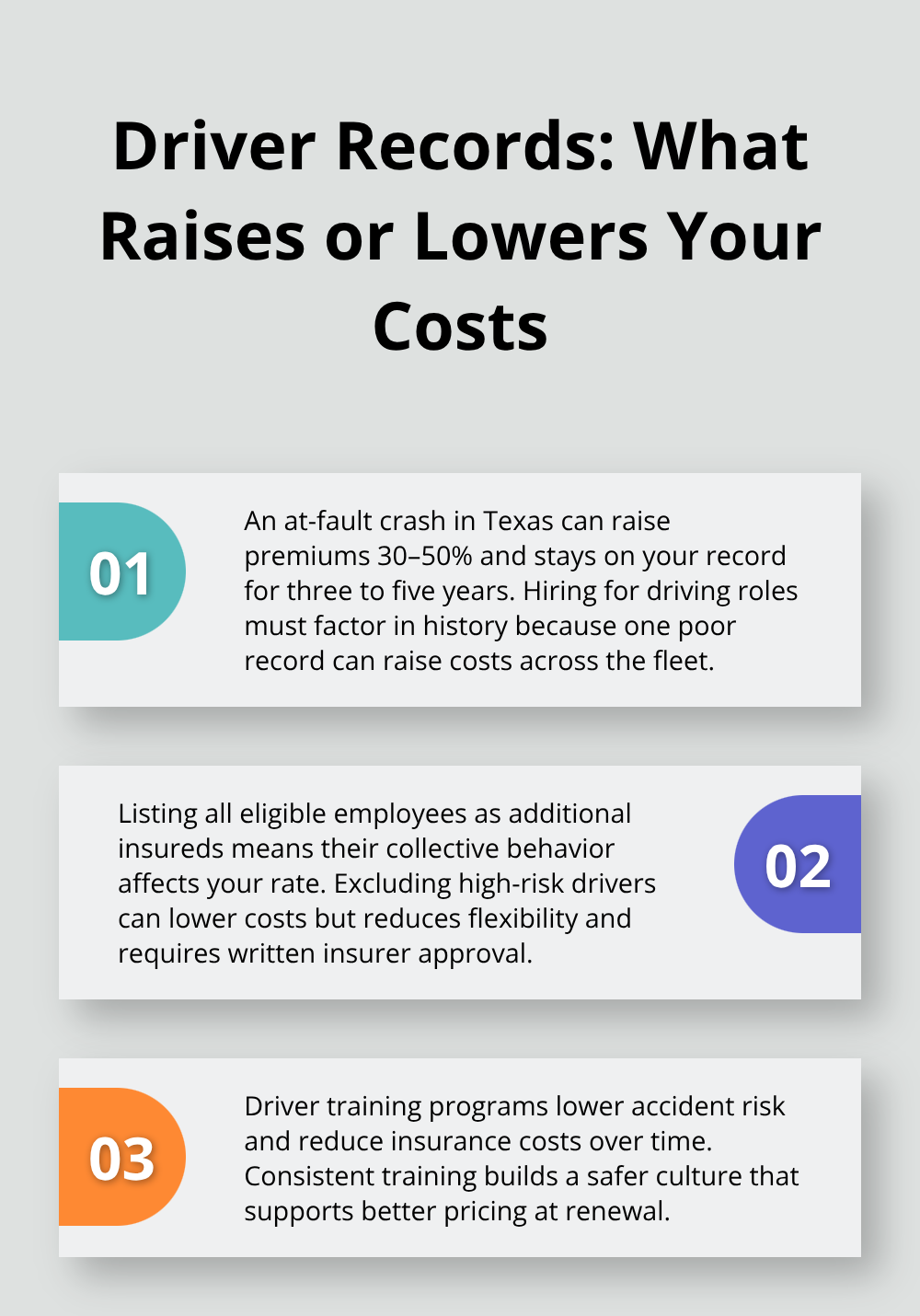

Your drivers’ histories directly impact what you’ll pay. A single at-fault crash in Texas raises premiums by 30 to 50 percent and could last three to five years. This makes hiring decisions about driving roles genuinely important-if a team member has a poor record, that affects your entire fleet’s cost. Commercial policies list all eligible employees as additional insureds, so their collective driving behavior influences your rate. Some businesses reduce costs by excluding high-risk drivers through named driver exclusions, though this requires written acceptance from your insurer and limits flexibility. Driver training programs substantially lower accident risk and reduce insurance costs over time, making this one of the most practical investments available.

Mileage and Coverage Choices Create the Real Price Gap

Texas commercial auto premiums average around 218 dollars monthly or 2,610 dollars annually, compared to roughly 147 dollars monthly for basic commercial coverage. This 50 percent difference reflects higher liability limits and broader protections that commercial policies provide. Commercial policies typically offer liability limits around 2 million dollars, whereas personal policies max out lower. Raising your liability limits increases premiums by roughly 15 to 25 percent but protects your business from catastrophic claims. Deductible choices matter significantly-increasing your deductible reduces premiums substantially, though it means higher out-of-pocket costs when claims occur. Safety technology like telematics and collision avoidance systems cuts premiums by 10 to 20 percent, and GPS tracking paired with driver safety programs can yield savings around 22 percent for operations like Fort Worth logistics firms.

Technology and Risk Management Lower Your Bottom Line

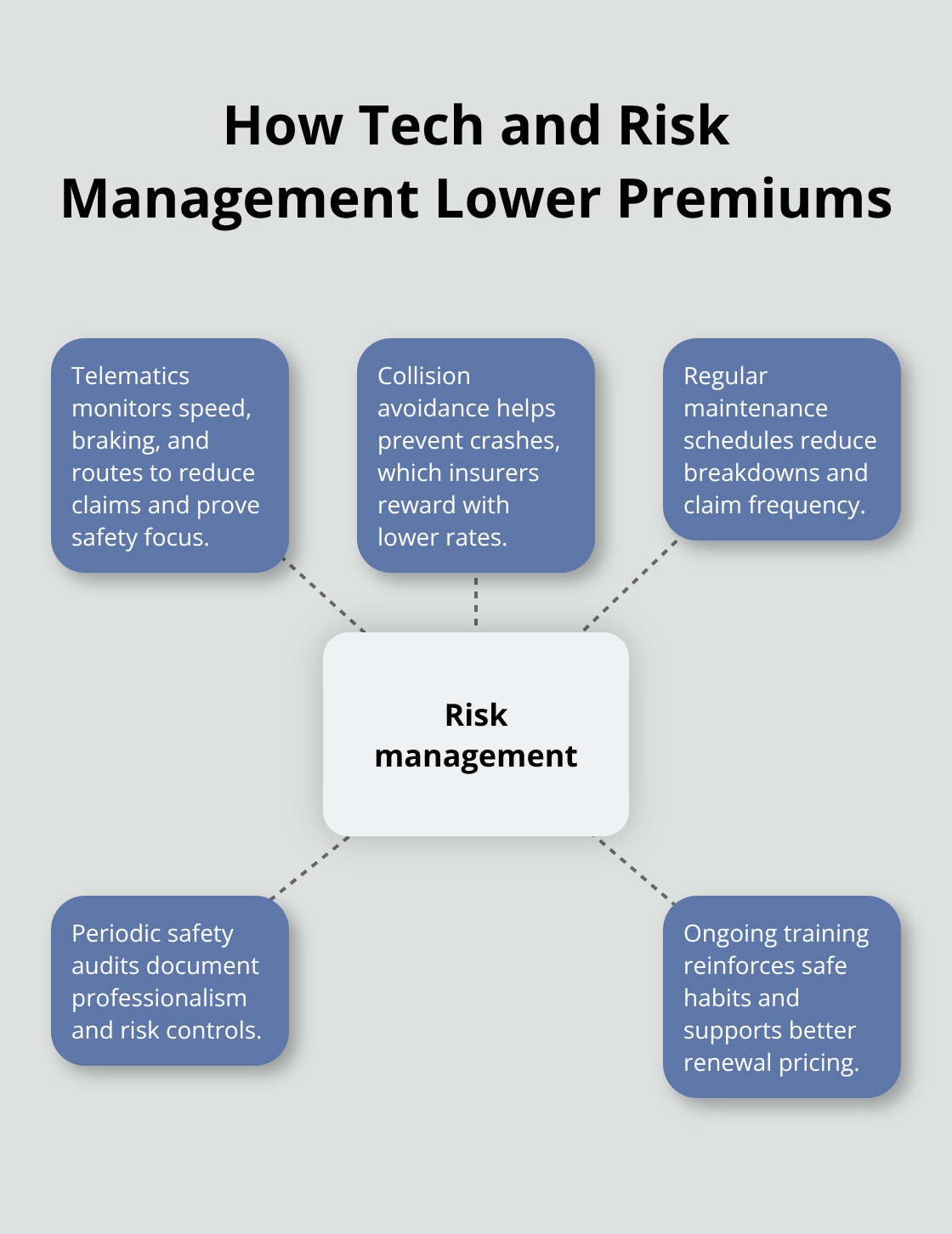

Safety investments pay dividends that extend beyond a single policy year. Telematics systems track speed, braking, and route efficiency to reduce claims and demonstrate your commitment to risk management. Collision avoidance technology prevents accidents before they happen, which insurers reward with lower rates. Regular maintenance and safety audits reduce claim frequency and signal to insurers that your operation runs professionally. These proactive measures (combined with driver training) create a track record that justifies better pricing at renewal time.

Understanding these cost drivers positions you to make smarter decisions about coverage and risk management. The next section shows you exactly how to compare prices across different vehicle classes and coverage options so you can find the right balance between protection and affordability.

How Much More Does Commercial Auto Cost

The Price Gap Between Personal and Commercial Coverage

Texas commercial auto insurance costs between $260 and $1,420 per month on average, compared to roughly 147 dollars monthly for basic personal coverage. That premium gap reflects real differences in what you’re buying. Commercial policies cover vehicles owned by your company, leased vehicles, and employee-driven cars, whereas personal policies explicitly exclude work-related driving. If an employee causes an accident while making a business delivery in a personal vehicle, your personal auto policy denies the claim entirely. This coverage gap forces business owners to choose between commercial policies or hired and non-owned auto insurance, which covers liability when personal or leased vehicles are used for work but excludes physical damage to the vehicle itself.

How Liability Limits and Vehicle Type Shape Your Premium

The price difference accelerates when you examine liability limits and vehicle types. Commercial policies typically offer 2 million dollars in liability coverage compared to lower limits in personal policies, and raising those limits increases premiums 15 to 25 percent depending on your industry and fleet size. A heavy-duty truck in Dallas costs substantially more than a sedan because specialized repair parts and labor run higher. Garaging location matters significantly in Texas-placing your fleet in urban Dallas or Houston adds roughly 15 percent to premiums versus suburban locations due to higher crash frequencies on corridors like I-35E and I-610.

Mileage, Deductibles, and Technology Impact

A high-mileage fleet exceeding 50,000 miles annually pays approximately 25 percent more because accumulated road time increases accident exposure. Deductible choices create another cost lever: raising your deductible from 500 dollars to 1,500 dollars cuts premiums substantially, though you absorb higher out-of-pocket costs when claims occur. Safety technology like telematics and collision avoidance systems reduce premiums 10 to 20 percent, making this investment genuinely worthwhile for operations running regular routes. One Fort Worth logistics firm saved around 22 percent through GPS tracking paired with driver safety programs, demonstrating that technology investments pay dividends beyond a single policy year.

These cost factors interact in ways that make each business’s premium unique. Your specific combination of vehicle types, mileage patterns, driver records, and safety investments determines where your rates land within the Texas market. The next section shows you concrete strategies to reduce what you pay without sacrificing the protection your business needs.

How to Actually Reduce Your Premiums

Safety programs and driver training produce measurable results that directly lower your premiums. One Fort Worth logistics firm saved approximately 22 percent through GPS tracking paired with driver safety programs, demonstrating that this investment pays for itself quickly. Telematics systems track speed, braking, and route efficiency to reduce claims and show insurers you take risk management seriously. Collision avoidance technology prevents accidents before they happen, which insurers reward with 10 to 20 percent rate reductions. Regular maintenance and safety audits reduce claim frequency and signal professionalism to underwriters at renewal time.

The strongest programs combine driver training with technology investments, creating a track record that justifies better pricing year after year. Skipping these investments leaves money on the table because insurers explicitly price lower rates for fleets that demonstrate commitment to accident prevention.

Bundle Multiple Vehicles and Policies Together

Combining commercial auto with other business insurance generates meaningful discounts that compound across your entire account. A business owner with separate policies for general liability, property coverage, and commercial auto pays more than someone consolidating everything with one carrier. This isn’t theoretical-insurers offer bundle discounts because managing one relationship costs them less than managing multiple policies. The discount percentage varies by carrier and policy combination, but the savings typically appear on your renewal notice as a line-item reduction.

Independent agencies represent multiple top-rated insurance companies, which means you have access to bundle deals that direct online quotes simply cannot match. Ask your agent specifically about bundle discounts before finalizing any quote-this single step often saves hundreds annually.

Your Driving Record Controls Your Future Costs

A clean driving record matters more than most business owners realize because a single at-fault crash can hike rates by 20-40% and impacts your rates for three to five years. This makes hiring decisions about driving roles genuinely consequential-if a team member has a poor history, that person’s accidents directly increase your fleet’s cost.

Some businesses reduce costs through named driver exclusions, though this requires written acceptance from your insurer and limits operational flexibility. The better approach involves driver training programs that prevent accidents from happening in the first place. Regular safety training reinforces defensive driving habits and reduces accident risk substantially, making it the most practical investment available for protecting both your premium costs and your employees’ safety.

Final Thoughts

Commercial auto insurance costs substantially more than personal coverage because you purchase broader protection, higher liability limits, and coverage that extends across multiple drivers and vehicles. Understanding how much more commercial auto insurance actually costs helps you make informed decisions about what your business needs versus what you can optimize for savings. Your specific premium depends on vehicle type, mileage patterns, driver records, safety investments, and garaging location-a heavy-duty truck in Dallas costs far more than a sedan in a suburban area.

The strategies that reduce your premiums work because they address what insurers actually price: safety programs lower accident frequency, telematics systems demonstrate risk management commitment, and bundle discounts reward consolidation with a single carrier. A clean driving record protects your rates from the 20 to 40 percent increases that follow at-fault crashes, while driver training programs prevent accidents before they happen. These represent concrete reductions that appear on your renewal notice, not theoretical savings.

Shopping with multiple insurers matters because premium quotes vary significantly across carriers. Contact Brooks Insurance to compare quotes from multiple carriers and discuss which cost-reduction strategies make sense for your business. Our licensed agents review your specific operation and identify which carrier offers the best combination of price and protection for your situation.