Commercial auto insurance is one of the biggest expenses for Texas business owners. Many companies overpay simply because they don’t know where to look or what factors drive their rates up.

We at Brooks Insurance help businesses find cheap commercial auto insurance by showing you exactly what affects your premiums and how to reduce them. This guide walks you through the strategies that actually work.

What Drives Your Commercial Auto Insurance Rates

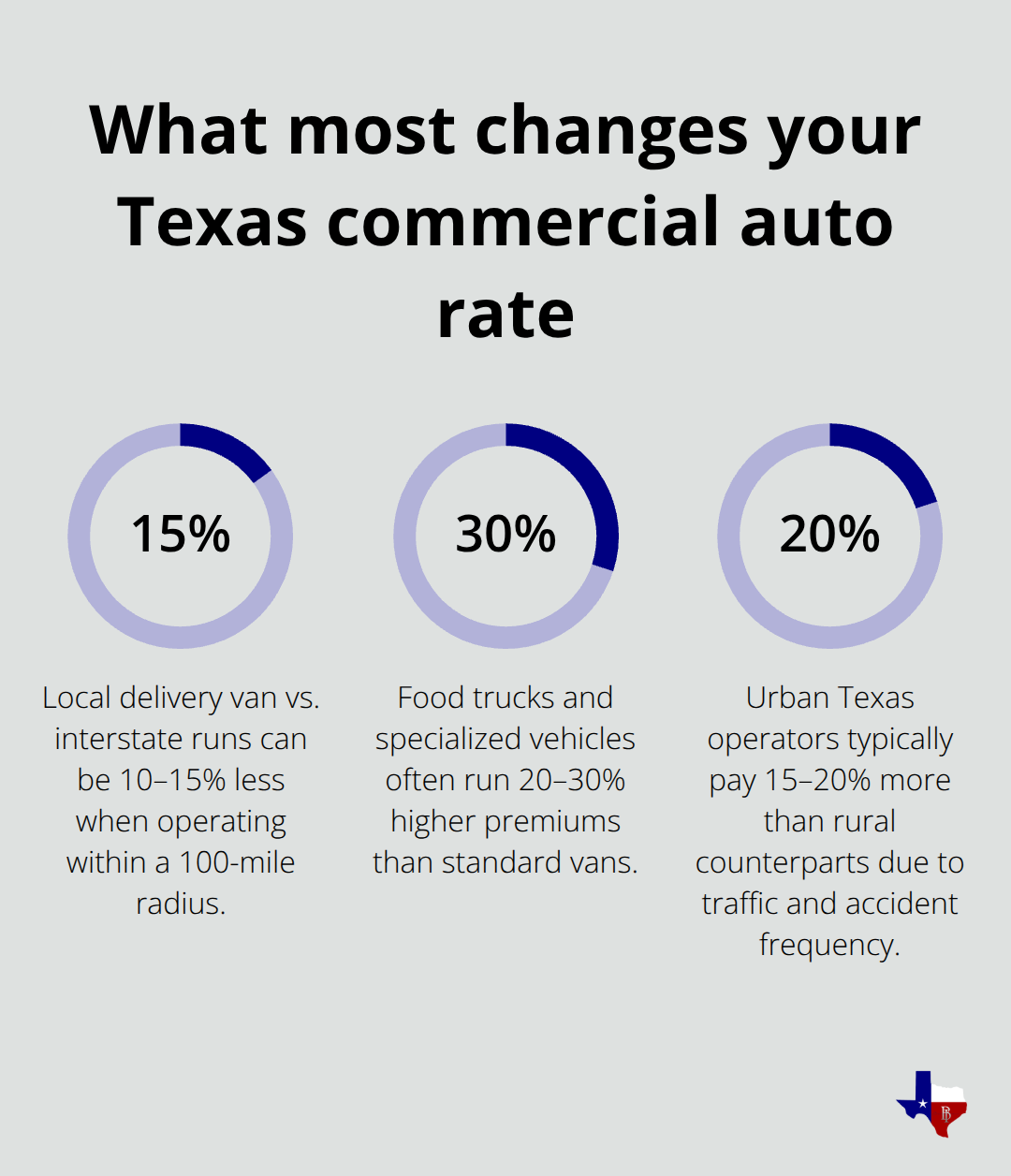

Vehicle type and usage patterns create the biggest pricing swings in commercial auto insurance. A delivery van operating within a 100-mile radius costs 10–15% less than the same vehicle making interstate runs. Food trucks and specialized vehicles run 20–30% higher premiums than standard vans because insurers view the equipment and operational risks differently.

A construction company with three pickup trucks used for local job sites pays substantially less than a courier service with the same vehicles running daily across multiple states. The number of miles your fleet accumulates annually matters enormously-high-mileage operations face higher accident exposure, which insurers price accordingly. Texas commercial operators in urban areas pay 15–20% more than rural counterparts due to increased traffic density and accident frequency.

How Your Drivers Impact What You Pay

Driver history is the second major cost factor, and clean records deliver measurable savings. Employees with no violations in the past 3–5 years lower your premiums by up to 25% compared to drivers with accidents or moving violations. A fleet with a three-year claims history of zero incidents saves approximately 30% versus operations that file claims regularly. One serious accident or DUI on an employee’s record spikes your entire policy cost-insurers view driver behavior as predictive of future losses. Many Texas business owners implement driver training programs and safety protocols; companies that do so often qualify for additional discounts of 10–15% when they document the training to insurers.

Industry Type Sets Your Baseline Cost

Your industry classification determines your starting price more than almost anything else. High-risk sectors like trucking, hazmat transport, and heavy construction pay up to 30% more than low-risk industries such as office supply delivery or light landscaping. Insureon data shows the average Texas commercial auto policy costs about $218 monthly, but this varies dramatically by sector and vehicle type. A plumbing contractor with two service vans faces different pricing than a staffing agency using the same vehicles. Your specific business use-whether you transport goods, people, equipment, or operate as a service vehicle-gets coded into your policy, and misclassifying this use is one of the costliest mistakes you can make.

What Happens When You Misclassify Your Business

Insurers assign risk codes based on how you actually use your vehicles. If you tell your insurer you operate a light delivery service but your drivers regularly transport hazardous materials, you’ve created a coverage gap that could leave you exposed. Claims filed under the wrong classification can be denied entirely, leaving your business liable for damages. Accurate classification from day one protects both your coverage and your rates going forward.

Understanding these rate drivers positions you to make smarter decisions about coverage and cost reduction. The next section shows you exactly which strategies lower your premiums without sacrificing the protection your business needs.

How to Cut Your Premium Without Cutting Coverage

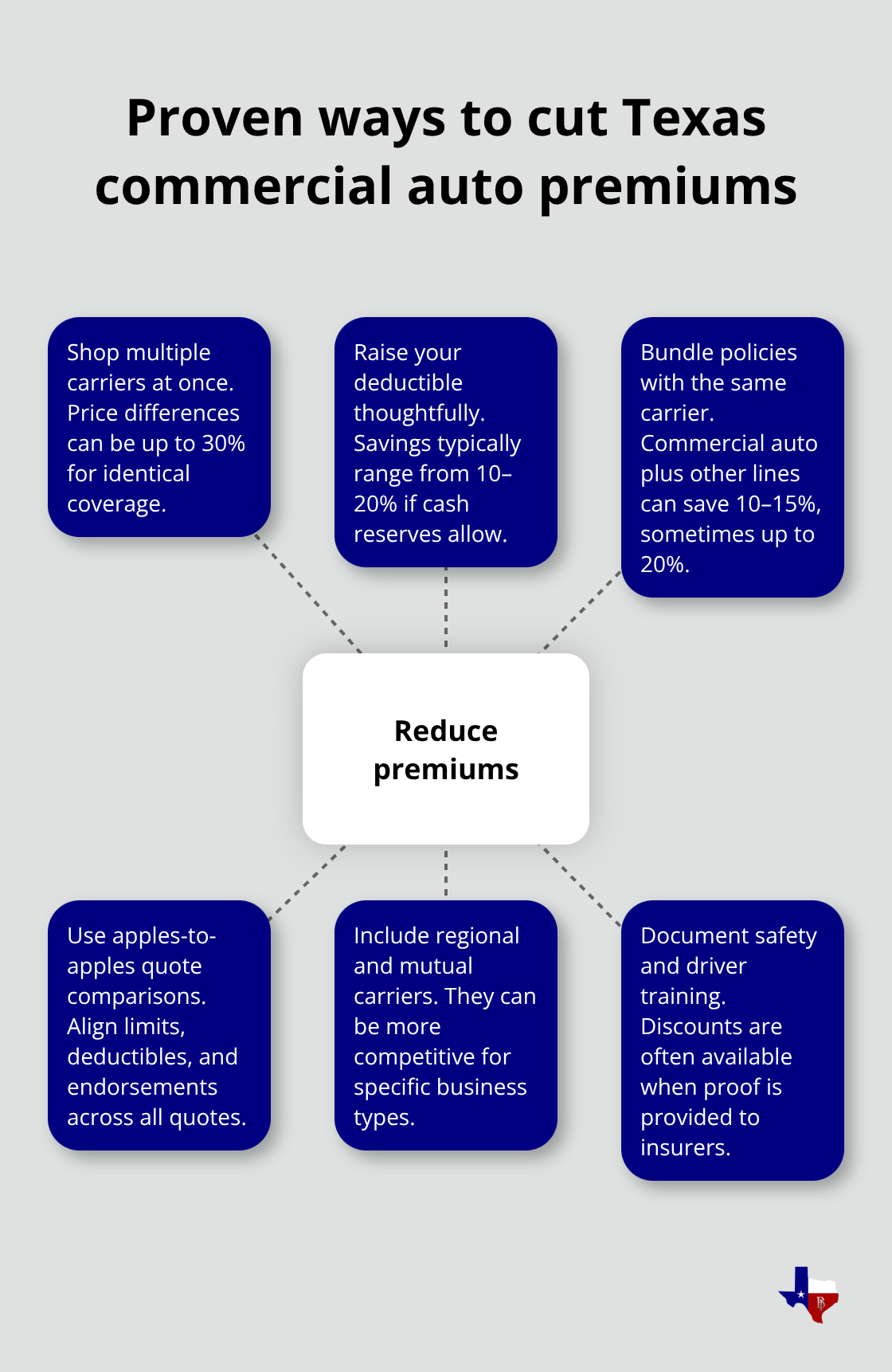

The most effective way to lower your commercial auto insurance cost is to shop across multiple carriers simultaneously, then strategically adjust your deductible and bundle policies. Texas insurers vary wildly on pricing-expect differences up to 30% between quotes for identical coverage. The top 11 carriers control roughly two-thirds of the Texas market, so starting with Progressive, State Farm, Allstate, and GEICO gives you access to the largest pricing competition. Regional carriers and mutuals like Texas Farm Bureau Mutual and Farmers Texas County Mutual often deliver better rates for specific business types, so include them in your quote process.

Once you have three to five solid quotes, you can identify which carriers value your specific risk profile favorably and which ones don’t.

Get Real Quotes, Not Estimates

Online quote platforms and direct carrier websites let you pull multiple quotes in under an hour. When you request quotes, ensure every single quote includes the same liability limits, deductibles, and coverage types-this is the only way to spot genuine price differences rather than comparing different protection levels. Many Texas business owners miss savings because they compare a $1,000-deductible quote from one carrier against a $500-deductible quote from another, then assume the higher-priced carrier is more expensive. The Texas Department of Insurance maintains a list of all licensed carriers operating in the state, which helps you identify credible insurers worth quoting. Once quotes are aligned on coverage, you’ll see exactly which carriers price your operation most competitively.

Increase Your Deductible Strategically

Raising your deductible from $500 to $1,000 reduces premiums by 10–20%, depending on your claims history and vehicle type. This strategy works best if your business has sufficient cash reserves to cover out-of-pocket costs after an accident. A construction company with strong cash flow and a three-year claims-free history can comfortably absorb a $1,500 deductible and save substantially. However, if your operation runs on thin margins or experiences frequent minor incidents, a higher deductible creates financial strain when claims occur. The math is straightforward: calculate your annual savings against your financial capacity to pay the deductible without disrupting operations.

Bundle Commercial Auto with Other Policies

Adding commercial auto to an existing general liability or business owners policy typically saves 10–15% on total premiums, with some combinations yielding up to 20% savings. If you already carry property insurance, workers compensation, or general liability through any carrier, request a bundled quote that adds commercial auto to your existing coverage. Many insurers price bundled policies more aggressively than standalone auto quotes because they want to consolidate your business. Bundling also simplifies administration-one renewal date, one agent contact, and one policy review process instead of managing multiple carriers. A plumbing contractor with general liability and commercial auto bundled through the same insurer pays less overall than splitting these coverages across two different carriers.

Move Forward with Apples-to-Apples Comparisons

When you compare quotes, align liability limits, physical damage coverages (collision and comprehensive), and any endorsements across all quotes. This alignment reveals true price differences rather than coverage variations that inflate one quote over another. For fleets or multiple vehicles, ask carriers about fleet or multi-vehicle discounts and whether a bundled business policy could reduce overall cost. Test quotes from both high-volume national carriers and regional or mutual insurers to identify the best overall value for your specific operation. The carriers that price your risk most favorably become your top candidates, and from there you can negotiate terms or request additional discounts based on safety programs or driver training documentation.

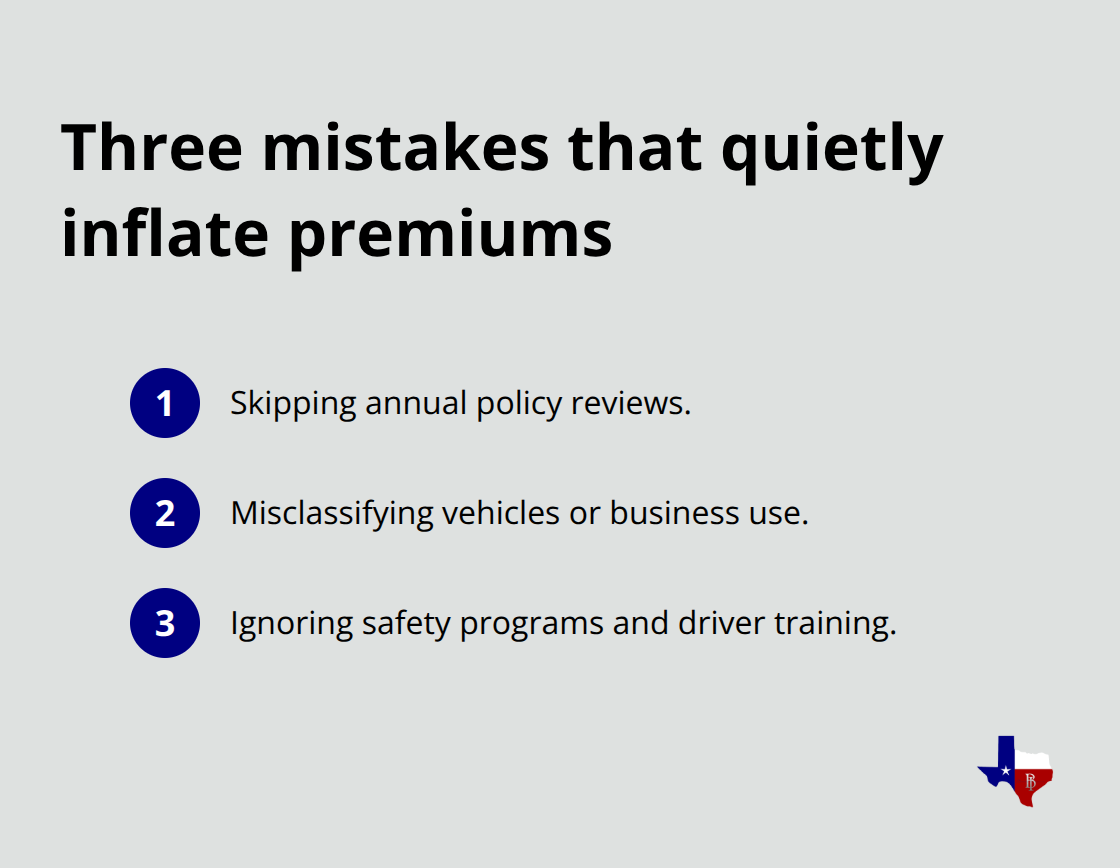

Three Mistakes That Quietly Inflate Your Premiums

Most Texas business owners make the same three errors that push their commercial auto insurance costs higher than necessary. Identifying and correcting these mistakes can save thousands annually while protecting your operation properly.

Neglecting Annual Policy Reviews

Your coverage needs change when you add vehicles, expand service areas, hire new drivers, or shift how you use your fleet. An annual policy review catches misalignments between your actual operations and your stated coverage before renewal time. If you add a second delivery route across state lines but fail to update your policy, you either overpay for coverage you don’t need or remain underinsured for the risk you’ve actually taken on.

Insurers base renewal premiums partly on claims history and partly on changes in your risk profile. A policy review each year before renewal prevents surprises and identifies cost-saving opportunities. Many Texas business owners discover during renewal that their coverage no longer matches their operations, forcing them to pay higher rates for misaligned protection.

Misclassifying Your Vehicle or Business Use

Vehicle or business use misclassification creates serious consequences beyond just higher premiums. When you apply for commercial auto insurance, you must accurately describe how your vehicles operate. If you classify your operation as light delivery service but your drivers regularly haul construction materials or transport hazardous goods, you’ve created a coverage gap.

Insurers can deny claims filed under incorrect classifications, leaving your business liable for damages that should have been covered. This isn’t a minor administrative issue-it’s the difference between protection and exposure. The Texas Insurance Code requires accurate risk disclosure, and material misrepresentation can void coverage entirely. Correct classification from the start protects both your coverage and your rates going forward.

Ignoring Safety Programs and Driver Training

Companies that implement driver training programs and document this investment to their insurers qualify for discounts on their premiums. A construction company that requires all drivers to complete defensive driving certification and maintains that documentation saves thousands annually compared to competitors without formal safety protocols.

Insurers view documented safety investments as proof that you actively manage risk, and they price accordingly. If you fail to capture these discounts, you leave money on the table while your competitors who implement safety programs pay less for identical coverage. Telematics programs and usage-based insurance can help you qualify for additional discounts while simultaneously improving driver behavior and reducing accident frequency.

Final Thoughts

Finding cheap commercial auto insurance in Texas requires you to compare quotes across multiple carriers, adjust your deductible to match your financial capacity, and bundle policies to capture available discounts. Expect to find differences up to 30% between carriers for identical coverage, which means shopping across the top 11 Texas carriers plus regional mutuals can save thousands annually. Once you have three to five solid quotes, you identify which insurers value your specific operation most favorably and negotiate from there.

Avoid the three mistakes that inflate premiums unnecessarily: skipping annual policy reviews, misclassifying your vehicles or business use, and ignoring safety programs that qualify for discounts. These errors cost money and create coverage gaps that expose your business to liability. Correct classification, documented safety investments, and annual reviews keep your coverage aligned with your actual operations while protecting your rates.

We at Brooks Insurance help Texas business owners find the right cheap commercial auto insurance at competitive prices. Our licensed agents understand Texas commercial operations and can guide you through the quote process, help you avoid costly mistakes, and identify discounts you might otherwise miss. Contact us at brooksinstx.com to start comparing quotes and see how much you can save.

Disclaimer: The information provided in this blog is for general informational purposes only and does not constitute legal, financial, or insurance advice. Coverage options, terms, and availability may vary. Please consult with a licensed professional for advice specific to your situation