General liability insurance protects your business from the financial fallout of accidents, injuries, and property damage claims. If you operate any kind of business in Texas-whether you’re a contractor, consultant, or retail owner-you need to understand your exposure.

At Brooks Insurance, we’ve seen firsthand how one accident can derail a business that lacks proper coverage. This guide walks you through who needs general liability insurance and how to pick the right limits for your operation.

Who Really Needs General Liability Insurance

General liability insurance isn’t optional for most Texas businesses. If you interact with customers, rent commercial space, or sign contracts with clients, you need it. The reality is stark: The Hartford reports that more than 40% of small businesses will experience a claim in the next 10 years, and when they do, the average general liability claim exceeds $75,000. That single claim can wipe out years of profit.

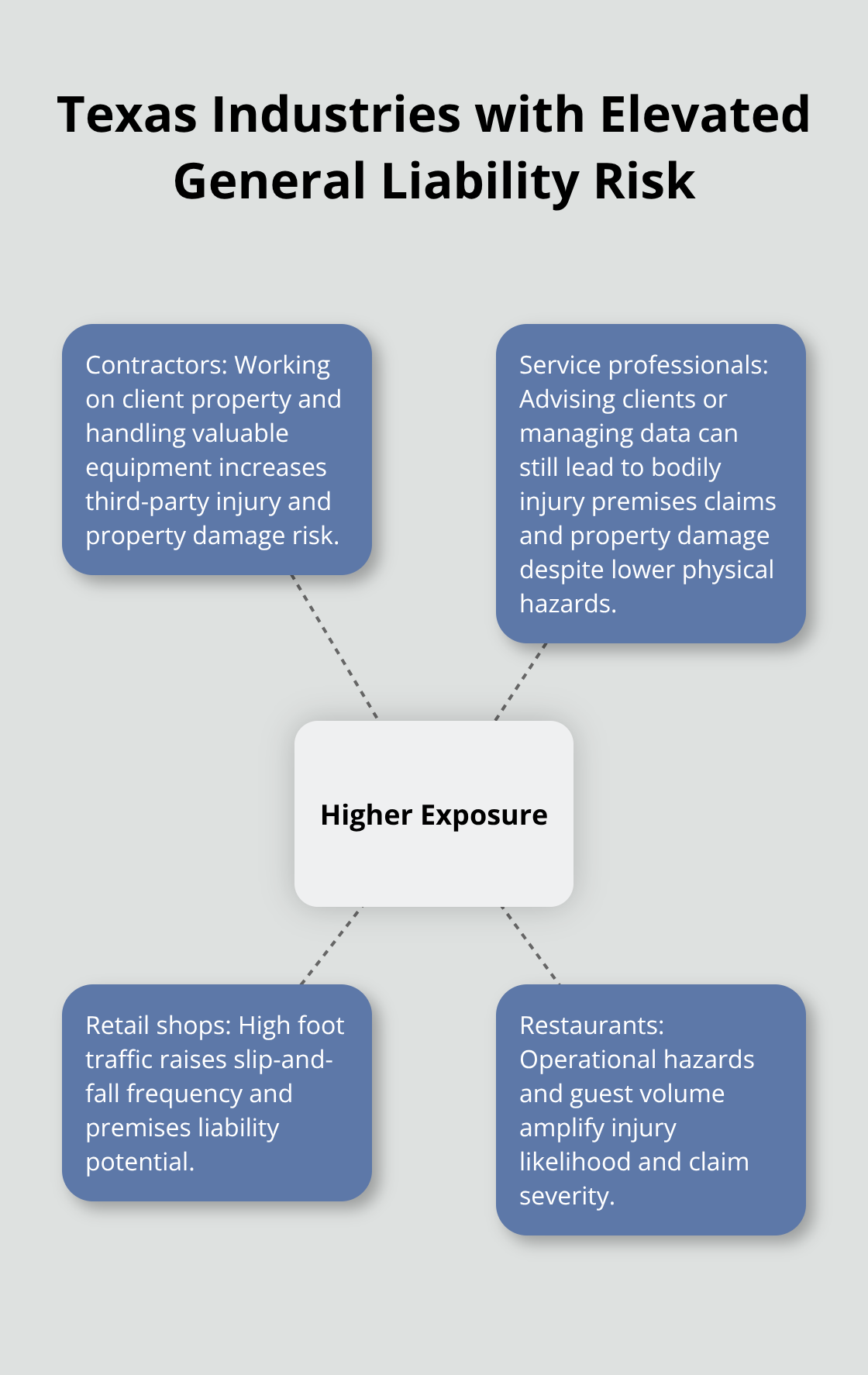

High-Risk Industries Face the Steepest Exposure

Contractors face especially high exposure because they work on client property and handle valuable equipment. A slip-and-fall on a job site, accidental damage to a customer’s home, or injury to a third party can trigger devastating costs. Service professionals like consultants, accountants, and IT specialists operate differently but face real risks too. When you advise clients or manage their data, mistakes or accidents still happen, and general liability covers bodily injury and property damage claims.

Retail shops and restaurants sit at the intersection of high foot traffic and operational hazards. Fall injuries at home and work claim tens of thousands of lives annually, which means your storefront or dining area is a liability magnet. If a customer slips on your floor or gets injured on your premises, general liability pays for their medical expenses, legal defense, and settlements.

Contracts and Leases Make Coverage Mandatory

Contracts and leases make general liability mandatory for many operations. Landlords require proof of coverage before you occupy commercial space. Clients demand a certificate of insurance before hiring you. Lenders often require it as a condition of financing. Without coverage, you personally pay all claims out of pocket, which means your personal assets become vulnerable.

Matching Coverage Limits to Your Business Size

The financial exposure scales with your business size and industry risk. A small consulting firm might operate with $1 million per occurrence coverage, while a construction company handling high-value projects should consider $2 million or higher limits. Texas doesn’t universally mandate general liability by law, but the market does. If you want contracts, clients, and credibility, you need it.

As your business grows and your risk profile changes, your coverage needs shift too. The next section explores how to assess your specific industry risks and evaluate which coverage limits actually protect your assets.

What Claims Actually Hit Your Business

Slip-and-Fall Injuries Lead the Pack

Slip-and-fall injuries remain the most common general liability claim Texas businesses face. According to the Consumer Product Safety Commission (CPSC), slip-and-fall injuries contribute to more than 2 million fall injuries annually across the country, and your commercial space is a prime target. A customer slips on a wet floor in your retail shop, a client trips on uneven pavement outside your office, or a visitor loses their footing on your stairs. These incidents trigger medical bills, lost wages, and legal fees that quickly spiral beyond $75,000 according to The Hartford’s data on average claim costs. General liability covers the injured party’s medical expenses up to your policy limit, plus the cost of defending yourself in court.

Property Damage Claims Follow Close Behind

Property damage claims follow a similar pattern but often involve third-party assets. You accidentally damage a client’s equipment during a service call, your contractor accidentally breaks a window at a rental property, or your delivery vehicle clips a parked car. These situations demand immediate payment for repairs or replacement, and without coverage, you personally pay every dollar. Regular safety reviews of your premises help reduce claims far more effectively than coverage limits after an accident occurs.

Legal Defense Costs Compound Your Exposure

Legal defense costs separate themselves from settlements and judgments, and this distinction matters enormously for your budget planning. When someone files a lawsuit against your business, your insurance company assigns an attorney and covers legal fees regardless of whether you win or lose the case. A modest slip-and-fall that settles for $25,000 might cost an additional $15,000 in legal defense alone if the claim becomes contested. Construction-related claims run even higher, with litigation expenses consuming significant portions of total claim payouts.

The Hartford’s research reveals that lawsuits push average general liability claims well above the initial injury costs, meaning your policy’s per-occurrence limit must account for both settlement amounts and legal expenses. This is why Texas businesses in high-traffic or high-contact industries should strongly consider $1 million per occurrence as a baseline rather than a luxury. Higher-risk operations in construction, hospitality, or property management benefit substantially from $2 million limits because a single catastrophic incident can exhaust lower limits before legal defense concludes. Understanding these real-world claim patterns shapes how you evaluate your coverage needs in the next section.

Picking the Right Coverage Limits for Your Business

Your industry determines how much coverage you actually need, and selecting the wrong amount costs money either way. Underinsure and a single claim wipes out your business. Overinsure and you waste premium dollars on protection you’ll never use. Start with your actual business exposures rather than picking a number off the shelf.

Construction and High-Risk Industries Demand Higher Limits

Construction companies operate in environments where property damage and bodily injury claims routinely exceed $100,000. A contractor working on high-value residential projects should start at $2 million per occurrence minimum because one mistake on a luxury home renovation can trigger claims that dwarf $1 million limits instantly. These operations face constant exposure to third-party property and worker safety risks that compound claim severity.

Retail and Food Service Face Slip-and-Fall Exposure

Retail businesses and restaurants face different but equally serious exposure through constant foot traffic and slip-and-fall risk. More than three million food service employees and over one million guests are injured annually as a result of slips, trips, and falls in America’s restaurants, meaning your storefront or dining area is statistically likely to produce a claim within the next decade. Most retail operations operate safely with $1 million per occurrence and $2 million aggregate limits, though high-traffic locations or venues serving alcohol should consider moving to $2 million per occurrence.

Service Professionals and Revenue-Based Assessment

Service professionals like consultants and accountants typically face lower frequency claims but can still encounter expensive litigation. Your revenue matters here too. If your business generates $500,000 annually, protecting $1 million in assets makes sense. If you generate $5 million in revenue with $3 million in equipment and inventory, you need limits that actually cover what you own. CBIZ research on 2025 general liability pricing shows that most renewals will carry 1 to 9 percent premium increases as the market stabilizes, meaning now is the time to lock in appropriate limits before your next renewal cycle pushes costs higher.

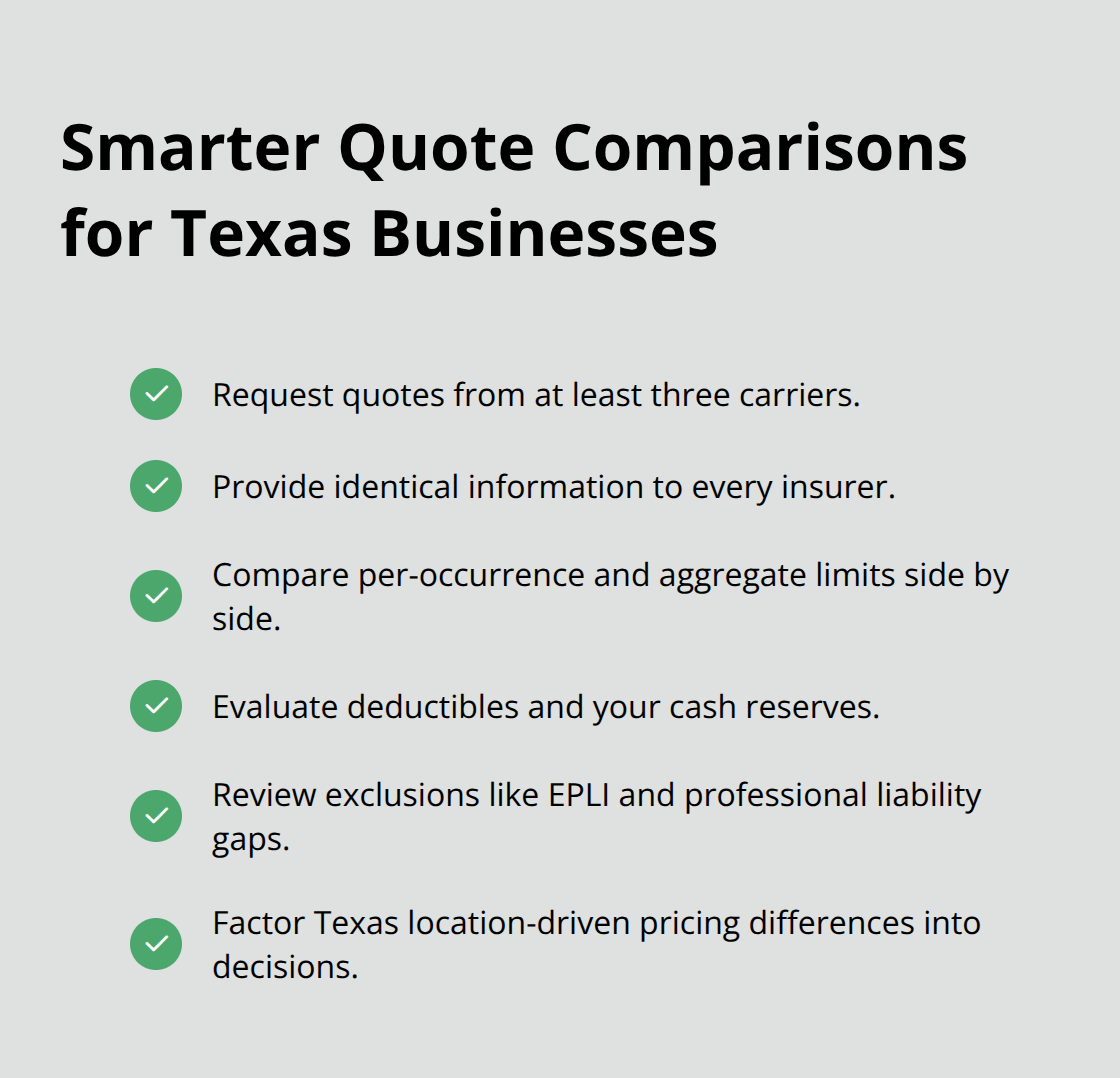

Comparing Quotes and Understanding Deductibles

Comparing quotes from multiple carriers reveals how dramatically premiums vary for identical coverage. One insurer might quote $600 annually for $1 million coverage while another charges $900 for the same limits, depending on how they underwrite your specific industry and claims history. Texas businesses should request quotes from at least three carriers before committing to a policy. When you get quotes, provide identical information to each insurer so the numbers stay comparable.

Your claims history matters enormously here. A business with no prior claims pays significantly less than one with previous incidents, and that gap widens as claim frequency increases. If you’ve had two claims in the past three years, expect premiums to reflect that risk profile. Location within Texas affects pricing too. Urban areas like Houston and Dallas often carry higher premiums due to increased litigation costs and jury verdicts, while rural areas may see lower rates. The Hartford’s research on nuclear verdicts shows that jury awards exceeding $10 million are increasingly shaping underwriting decisions, which means carriers price defensively in high-risk markets.

When comparing options, don’t just look at the premium. Examine the deductible carefully. A $500 deductible versus a $2,500 deductible might save you $200 annually, but that $2,000 difference comes directly from your pocket when a claim hits. For most Texas businesses, a $1,000 deductible balances affordability with reasonable out-of-pocket exposure. Higher deductibles work only if your cash reserves can absorb a claim without disrupting operations. Request quotes online and compare coverage details side by side, paying special attention to what exclusions each policy contains since standard general liability leaves gaps in areas like employment practices liability and professional negligence that may require separate coverage.

Final Thoughts

General liability insurance separates Texas businesses that survive claims from those that collapse under them. The data is unambiguous: more than 40% of small businesses will face a claim within the next decade, and when they do, costs exceed $75,000 on average. Who needs general liability insurance? Any business that interacts with customers, occupies commercial space, or signs contracts with clients must carry this protection.

Your next step is straightforward. Gather basic information about your business: your industry, annual revenue, number of employees, and the types of work you perform. Request quotes from multiple carriers and compare coverage limits, deductibles, and exclusions side by side, keeping in mind that most Texas businesses start with $1 million per occurrence and $2 million aggregate limits (though construction companies and high-traffic retail operations benefit from $2 million per occurrence).

We at Brooks Insurance have spent over 50 years helping Texas businesses find the right coverage at the right price. Our licensed agents understand Texas business risks and can tailor coverage to your specific operation, and as an independent agency, we represent multiple top-rated insurance companies to give you access to competitive pricing. Contact Brooks Insurance today to discuss your general liability needs and get a personalized quote that actually protects what you’ve built.